S&P, Nasdaq edge higher with gold spike, FOMC minutes in focus

Introduction & Market Context

Tourmaline Oil Corp . (TSX:TOU), Canada’s largest natural gas producer, has released its May 2025 corporate presentation highlighting the company’s strategic positioning, financial strength, and growth plans. The presentation comes as natural gas markets continue to evolve with increasing global demand for LNG and growing focus on environmental performance in the energy sector.

The company’s stock has been performing well, with shares trading at $63.68 as of May 7, 2025, up 3.43% and closer to its 52-week high of $70.73 than its low of $54.37. This performance reflects investor confidence in Tourmaline’s business model and growth strategy.

Executive Summary

Tourmaline’s May 2025 presentation emphasizes its scale as Canada’s largest natural gas producer and fourth largest in North America, with significant midstream assets and a growing liquids business. The company projects 2025 production of 635,000-665,000 boepd and has outlined a growth plan targeting a 4% production CAGR through 2029.

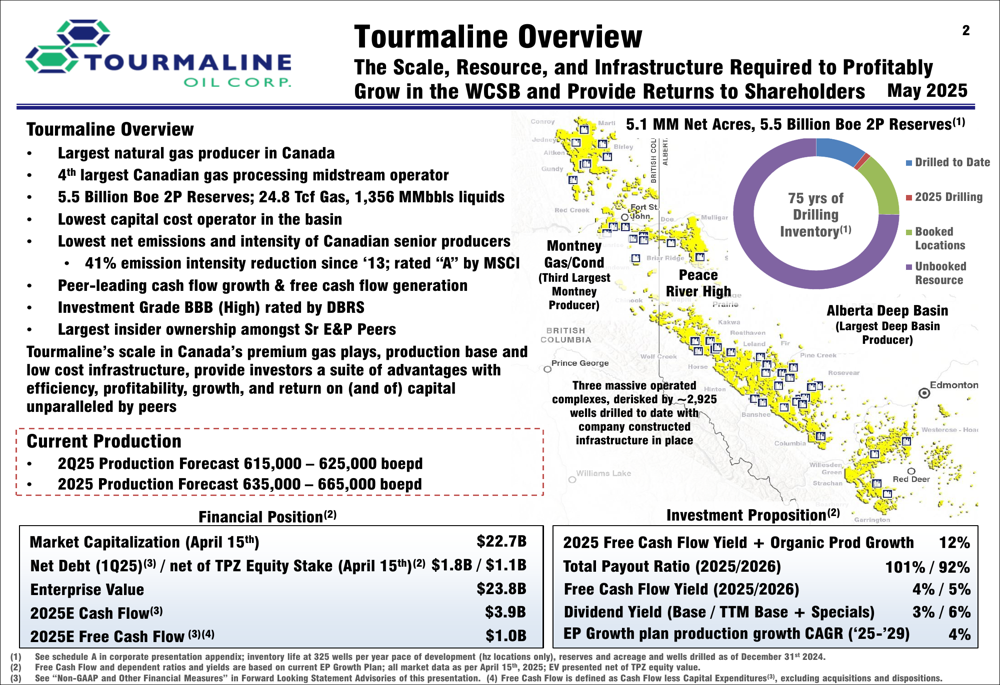

As shown in the following overview slide, Tourmaline boasts 5.5 billion boe in 2P reserves, an investment grade BBB (High) rating from DBRS, and the lowest capital cost structure among Canadian senior producers:

The company’s financial position remains strong with a market capitalization of $22.7 billion (as of April 15th) and net debt of $1.8 billion in Q1 2025, or $1.1 billion net of its equity stake in Topaz Energy. For 2025, Tourmaline forecasts cash flow of $3.9 billion and free cash flow of $1.0 billion, with a significant portion allocated to shareholder returns through base and special dividends.

Competitive Industry Position

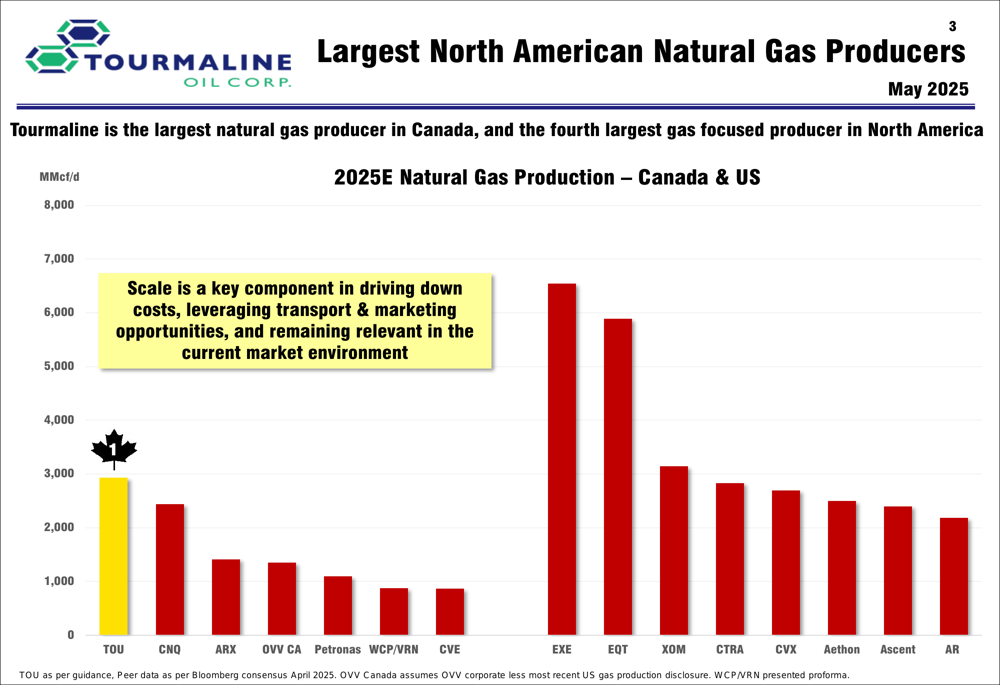

Tourmaline has established itself as a dominant player in the North American natural gas landscape. The presentation highlights its position as the largest natural gas producer in Canada and fourth largest in North America, producing approximately 3,000 MMcf/d.

The following chart illustrates Tourmaline’s competitive positioning among major North American natural gas producers:

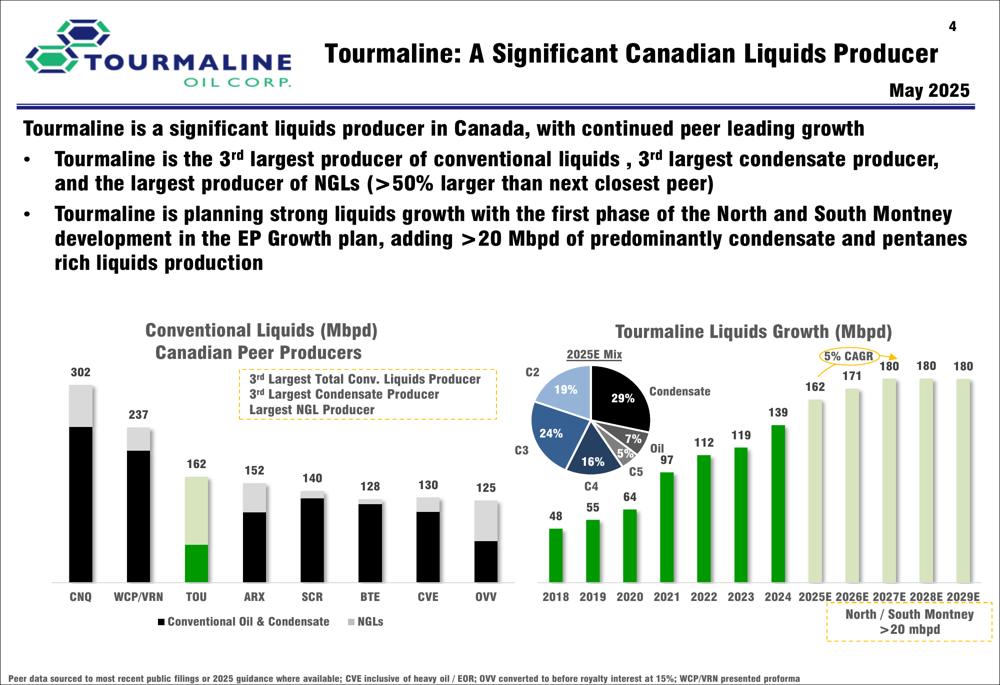

Beyond natural gas, Tourmaline has also developed a significant liquids business, ranking among the top Canadian producers with 162 Mbpd of conventional liquids production. The company projects continued liquids growth, particularly from North and South Montney development, which is expected to add more than 20 Mbpd of condensate and pentanes.

As shown in the following chart comparing Tourmaline’s liquids production to Canadian peers:

The company’s competitive advantage is further strengthened by its extensive midstream assets, which include 33 working interest gas plants (18 of which are 100% owned and operated), with current operated gas processing capacity of 3.2 bcf/day. This vertical integration helps Tourmaline maintain cost control and operational flexibility.

Strategic Initiatives

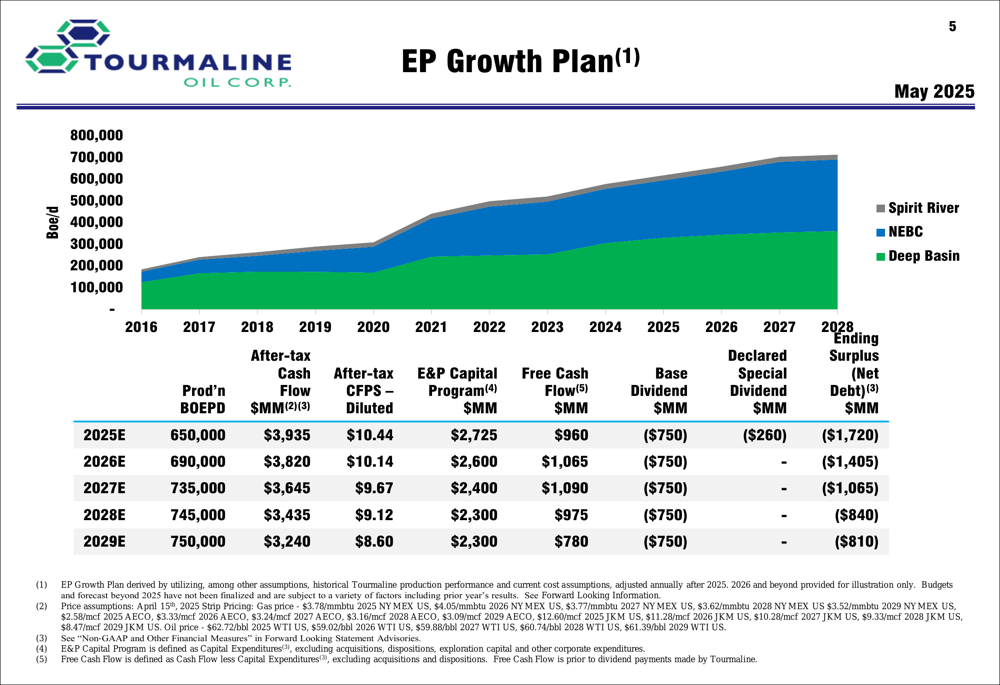

Tourmaline’s strategic focus centers on balanced growth, shareholder returns, and environmental performance improvement. The company has outlined a detailed EP Growth Plan through 2029, projecting production growth from 650,000 boepd in 2025E to 750,000 boepd by 2029E.

The following chart illustrates Tourmaline’s production growth trajectory and financial projections:

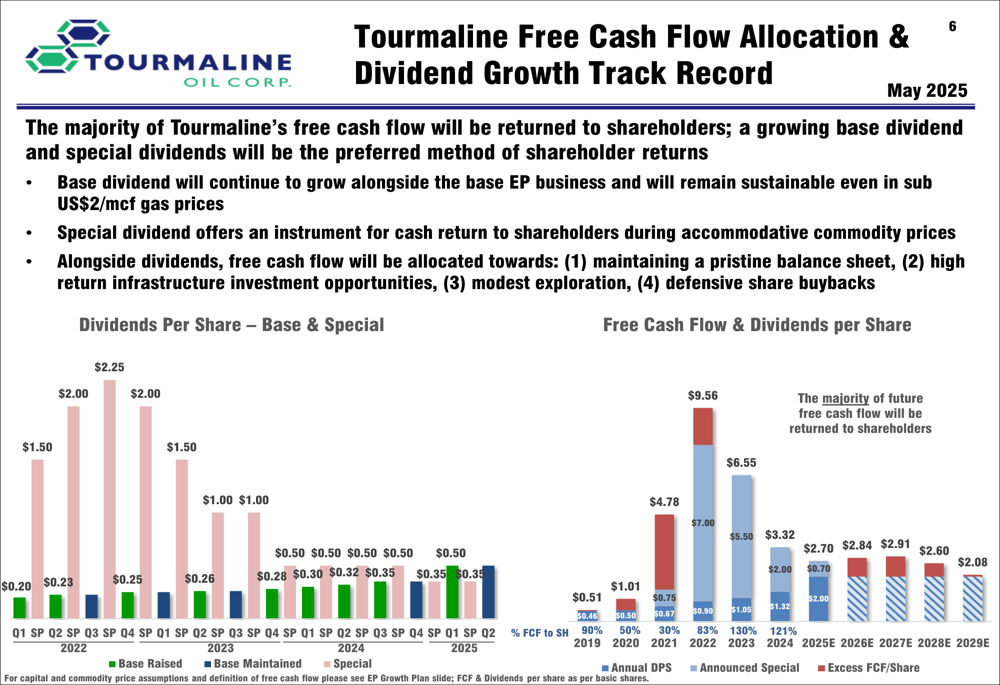

A key component of Tourmaline’s strategy is its approach to free cash flow allocation, with priority given to growing base dividends and special dividends. The company has established a strong track record of dividend growth, as shown in the following chart:

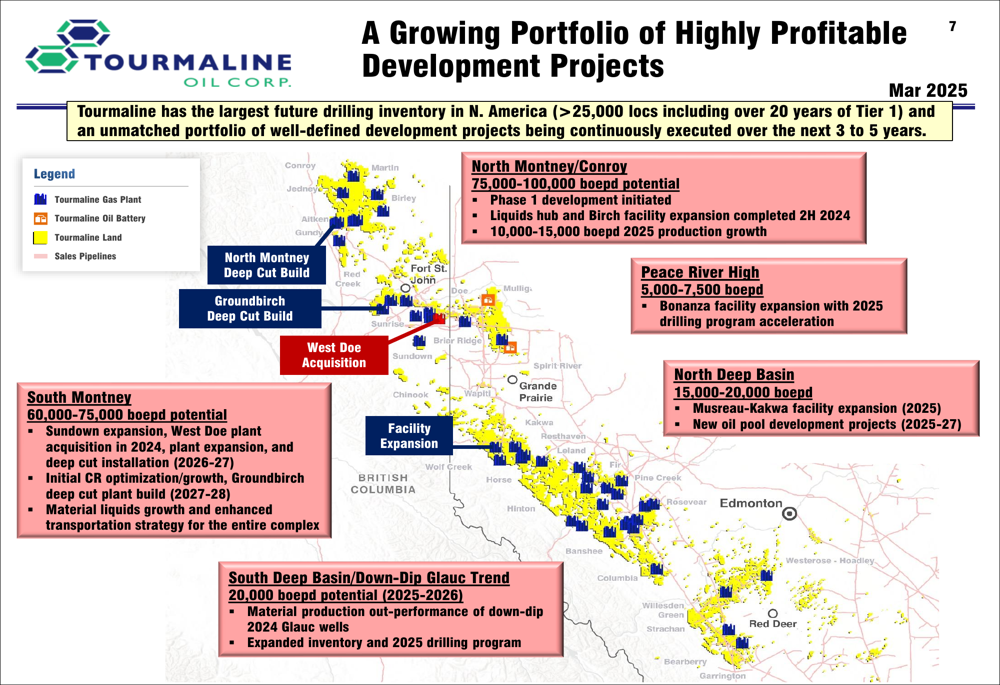

Supporting this growth is Tourmaline’s extensive portfolio of development projects across various regions, including North Montney/Conroy, Peace River High, North Deep Basin, South Montney, and South Deep Basin. The company claims to have the largest future drilling inventory in North America with over 25,000 locations, including more than 20 years of Tier 1 inventory.

As illustrated in this map of Tourmaline’s development projects:

Another strategic focus area is Tourmaline’s growing LNG exposure, which provides access to international pricing. The company has established agreements with Rockies LNG, Trafigura, and Cheniere, with the latter arrangement already delivering since January 2023. This LNG strategy helps diversify Tourmaline’s market exposure beyond North American natural gas prices.

Detailed Financial Analysis

Tourmaline’s financial projections for 2025 include:

- Production: 635,000-665,000 boepd

- Cash Flow: $3,935 million

- Cash Flow Per Share (diluted): $10.44

- E&P Capital Program: $2,600-$2,850 million

- Capital Expenditures: $2,850-$3,100 million

- Free Cash Flow: $960 million

The company emphasizes that its maintenance budget and dividend are fully funded at US$2.00/mcf, providing significant downside protection. At current strip pricing, Tourmaline projects meaningful free cash flow averaging approximately $1 billion per year in its EP Growth plan.

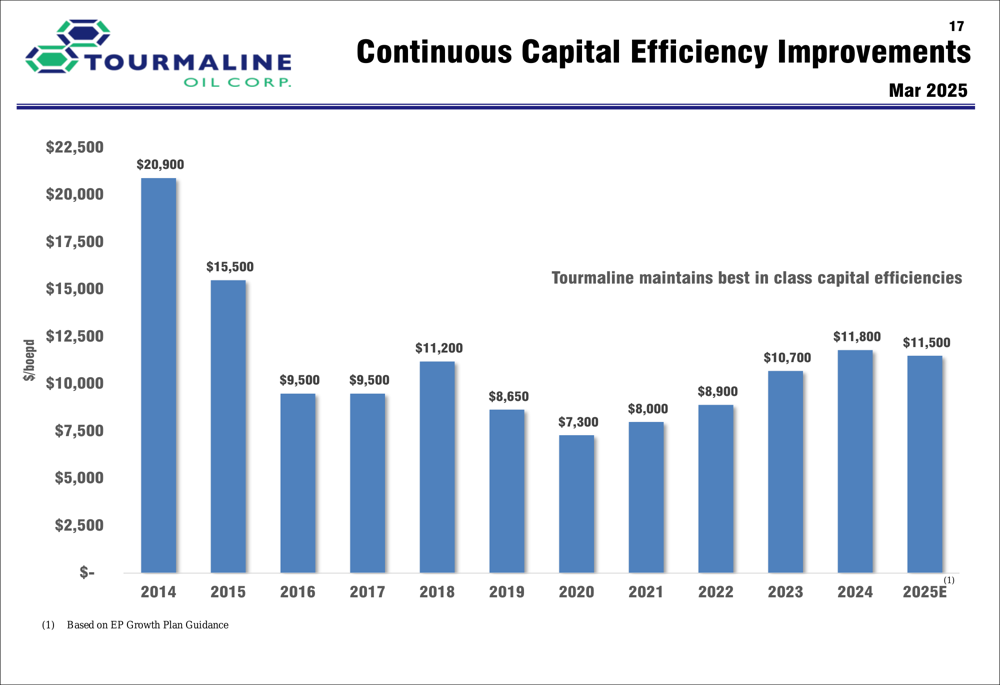

Tourmaline’s capital efficiency has shown improvement over time, though there has been some increase in recent years, as shown in the following chart:

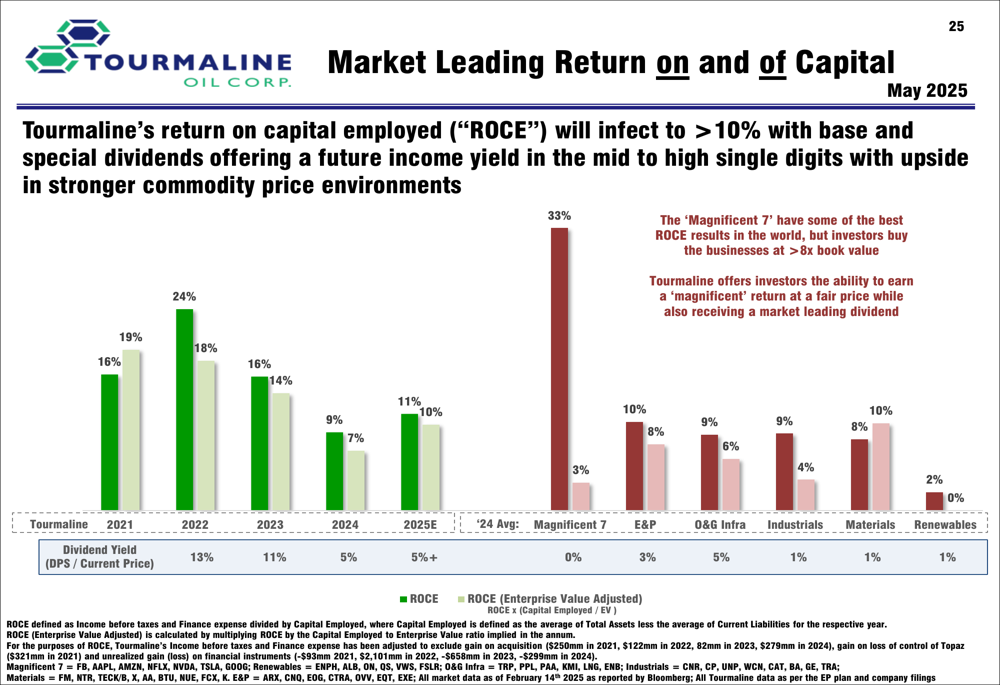

The company highlights its strong return on capital employed (ROCE) compared to other sectors, projecting a yield of over 10% with base and special dividends. Tourmaline positions itself as offering ROCE at a fair price compared to high-growth technology companies that trade at much higher multiples.

As illustrated in this comparative ROCE chart:

Forward-Looking Statements

Tourmaline’s long-term business plan extends from 2026 to 2032, focusing on continued production growth, particularly in NEBC, large project sequencing, and consistent shareholder returns. The company aims to balance yield and growth while maintaining financial discipline.

The company has outlined several key environmental initiatives, targeting continued reduction in CO2 emission intensity and methane intensity. Tourmaline notes it has already achieved a 41% reduction in emissions since 2013 and has received an "A" rating from MSCI for its environmental performance.

Looking ahead, Tourmaline’s guidance suggests the company is well-positioned to benefit from growing natural gas demand, particularly as LNG export capacity increases in North America. The company’s extensive drilling inventory, midstream assets, and improving capital efficiency provide a solid foundation for its growth and shareholder return objectives.

While the presentation naturally emphasizes positive aspects of Tourmaline’s business, the company’s position as Canada’s largest natural gas producer with significant liquids exposure, extensive infrastructure, and focus on shareholder returns appears to support its strategic direction and financial projections.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.