Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

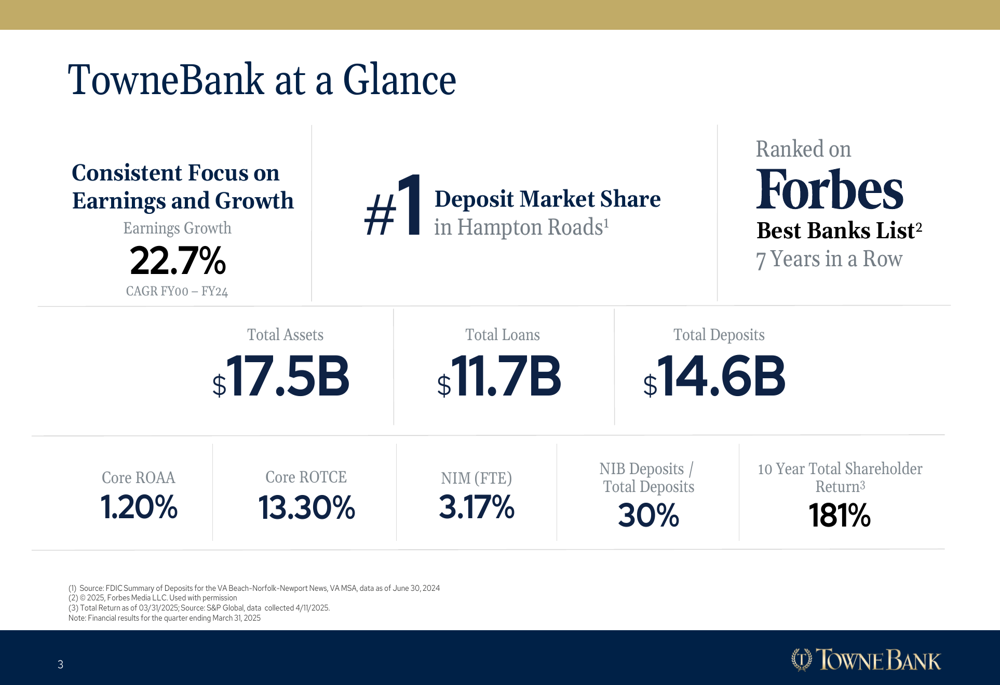

TowneBank (NASDAQ:TOWN) delivered impressive first-quarter 2025 results, with substantial growth in revenue, earnings, and profitability metrics. The bank, which maintains the #1 deposit market share in Hampton Roads and has been ranked on Forbes’ Best Banks List for seven consecutive years, demonstrated the strength of its diversified business model across banking, insurance, mortgage, and resort property management segments.

As shown in the following overview of TowneBank’s key metrics and achievements, the bank reported total assets of $17.5 billion, with strong returns and a healthy net interest margin:

Quarterly Performance Highlights

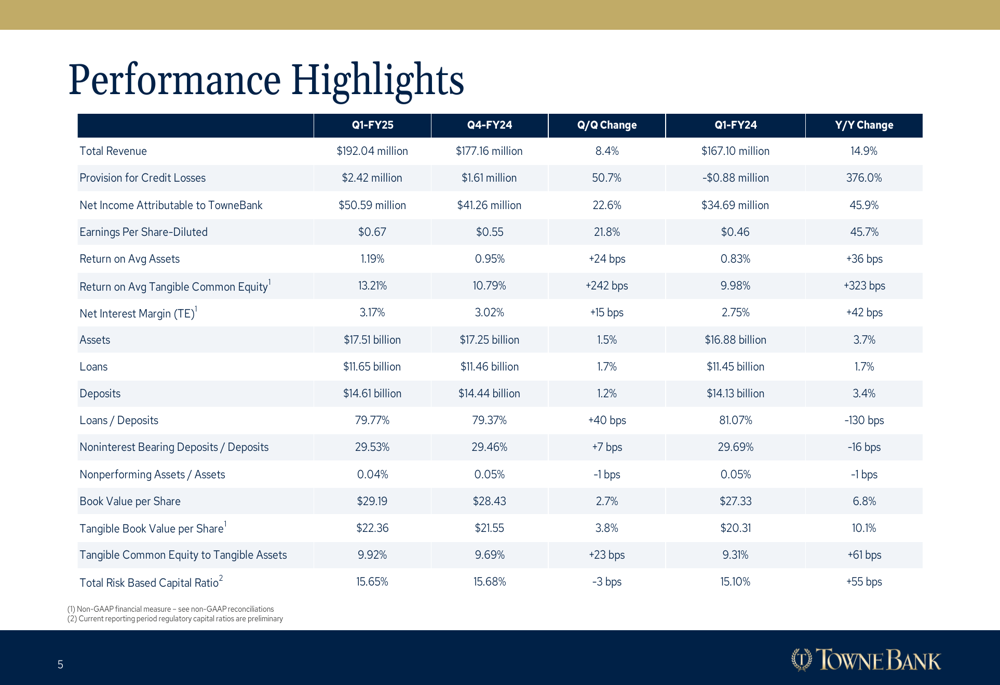

TowneBank reported total revenue of $192.04 million for Q1 2025, representing an 8.4% increase quarter-over-quarter and a 14.9% jump year-over-year. Net income attributable to TowneBank surged to $50.59 million, up 22.6% from the previous quarter and 45.9% compared to the same period last year. This translated to diluted earnings per share of $0.67, a 21.8% increase quarter-over-quarter and 45.7% year-over-year.

The bank’s profitability metrics also showed significant improvement, with return on average assets reaching 1.19% (up 24 basis points quarter-over-quarter and 36 basis points year-over-year) and return on average tangible common equity climbing to 13.21% (up 242 basis points quarter-over-quarter and 323 basis points year-over-year).

The following detailed performance highlights illustrate the bank’s strong financial results across key metrics:

Net interest income increased to $120.48 million, up 2.1% from the previous quarter and 16.7% year-over-year, despite a modest provision for credit losses of $2.42 million. Noninterest income grew substantially to $71.57 million, representing a 21.1% increase quarter-over-quarter and 12.0% year-over-year.

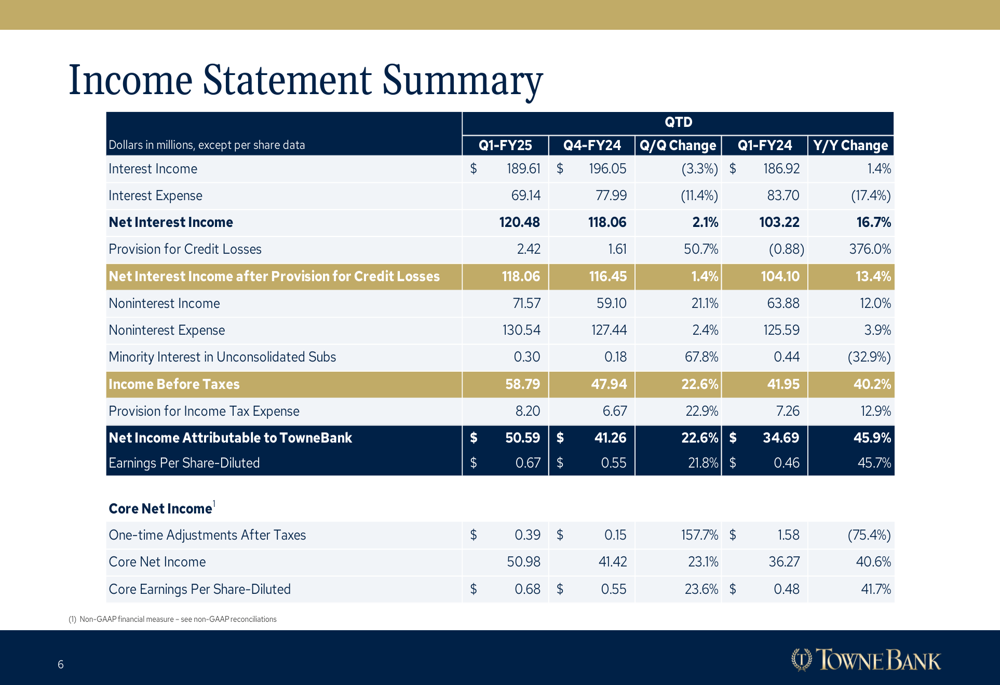

The income statement summary below provides a comprehensive breakdown of TowneBank’s financial performance:

Detailed Financial Analysis

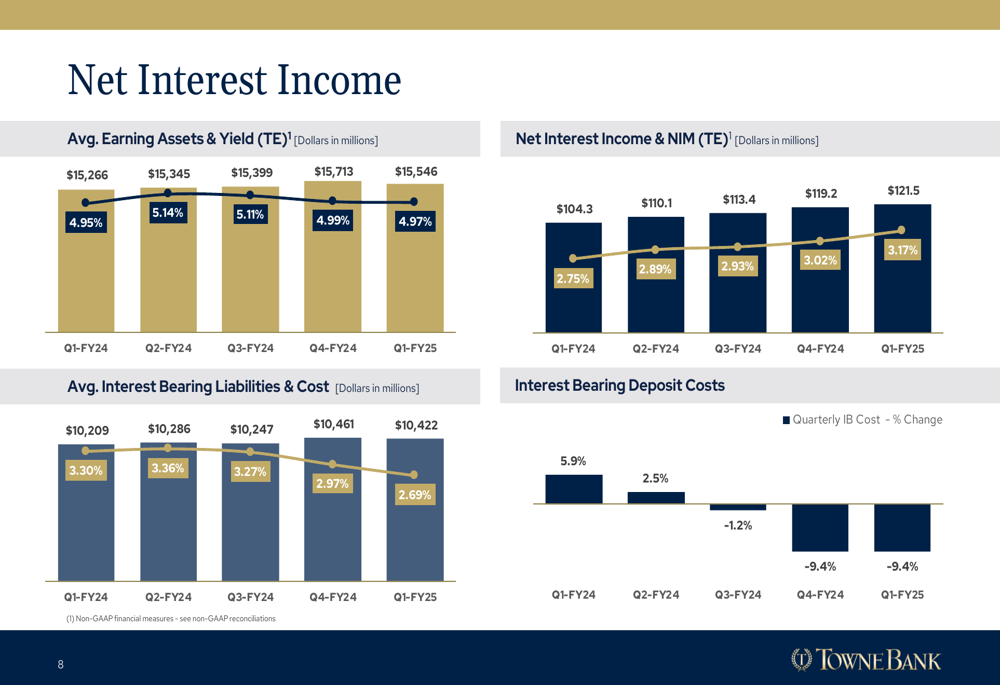

TowneBank’s net interest margin (NIM) continued its upward trajectory, reaching 3.17% in Q1 2025, an increase of 15 basis points from the previous quarter and 42 basis points year-over-year. This expansion was primarily driven by deposit cost reductions, as shown in the following chart:

The bank’s NIM improvement was largely attributed to an 18 basis point contribution from deposits, while the loan portfolio continued to reprice. The sensitivity analysis indicates that TowneBank’s net interest income could increase by up to 10.32% in a rising rate environment of +200 basis points, demonstrating the bank’s favorable positioning for potential rate changes.

TowneBank’s deposit base remained stable with total deposits of $14.61 billion, up 1.2% quarter-over-quarter and 3.4% year-over-year. Notably, the bank has achieved three consecutive quarterly decreases in deposit costs since Q2 2024, with a cumulative 64 basis point reduction in interest-bearing deposit costs. Noninterest-bearing deposits represented approximately 30% of total deposits, providing a low-cost funding source.

The loan portfolio grew to $11.65 billion, up 1.7% both quarter-over-quarter and year-over-year. Commercial real estate loans constituted the largest portion at 50% of the total portfolio, followed by residential 1-4 family loans at 20% and commercial and industrial loans at 11%.

Segment Performance

TowneBank’s diversified business model continued to demonstrate strength across multiple segments. The banking segment showed improved efficiency, with its core efficiency ratio decreasing from 68.84% in FY2024 to 65.55% in Q1 2025.

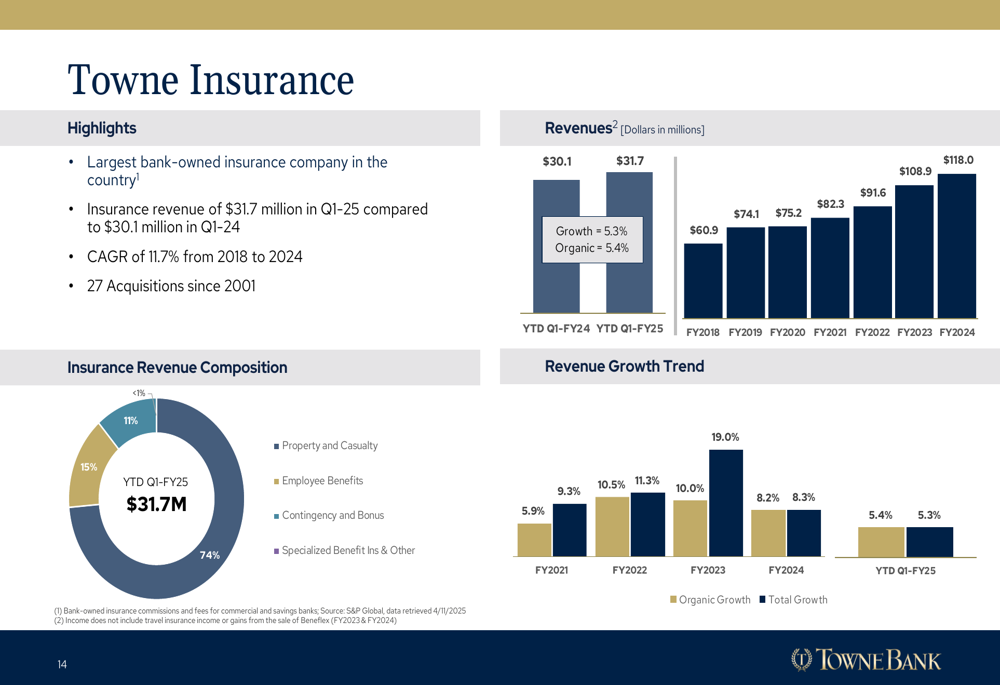

Towne Insurance, which the company notes is the largest bank-owned insurance company in the country, generated revenue of $31.7 million in Q1 2025, up from $30.1 million in Q1 2024. The insurance segment has achieved a compound annual growth rate of 11.7% from 2018 to 2024, supported by 27 acquisitions since 2001.

As illustrated in the following chart, Towne Insurance’s revenue is primarily derived from property and casualty insurance (74%), with additional contributions from employee benefits (15%) and contingency and bonus revenue (11%):

The resort property management segment, Towne Vacations, reported strong performance with property management income of $19.5 million in Q1 2025, up from $16.8 million in Q1 2024, representing a 16.1% year-over-year increase. This segment’s efficiency ratio improved dramatically from 81.70% in FY2024 to 61.34% in Q1 2025.

In contrast, the mortgage segment faced challenges, with its efficiency ratio increasing from 89.70% in FY2024 to 104.21% in Q1 2025, indicating that expenses exceeded revenue. Mortgage banking income was $10.6 million in Q1 2025, slightly down from $10.8 million in Q1 2024, as gain on sales and fees as a percentage of loans originated decreased by 7 basis points compared to Q4 2024.

Balance Sheet and Asset Quality

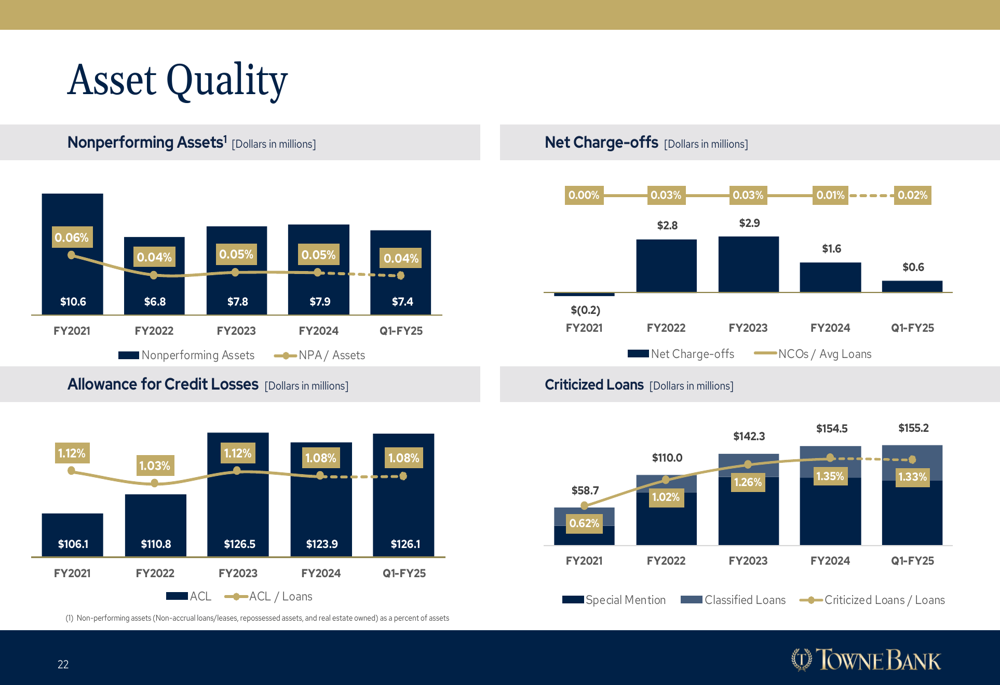

TowneBank maintained strong asset quality metrics, with nonperforming assets representing just 0.04% of total assets, down 1 basis point both quarter-over-quarter and year-over-year. The allowance for credit losses stood at 1.08% of loans, reflecting the bank’s conservative approach to credit risk management.

The following chart illustrates TowneBank’s consistently strong asset quality metrics:

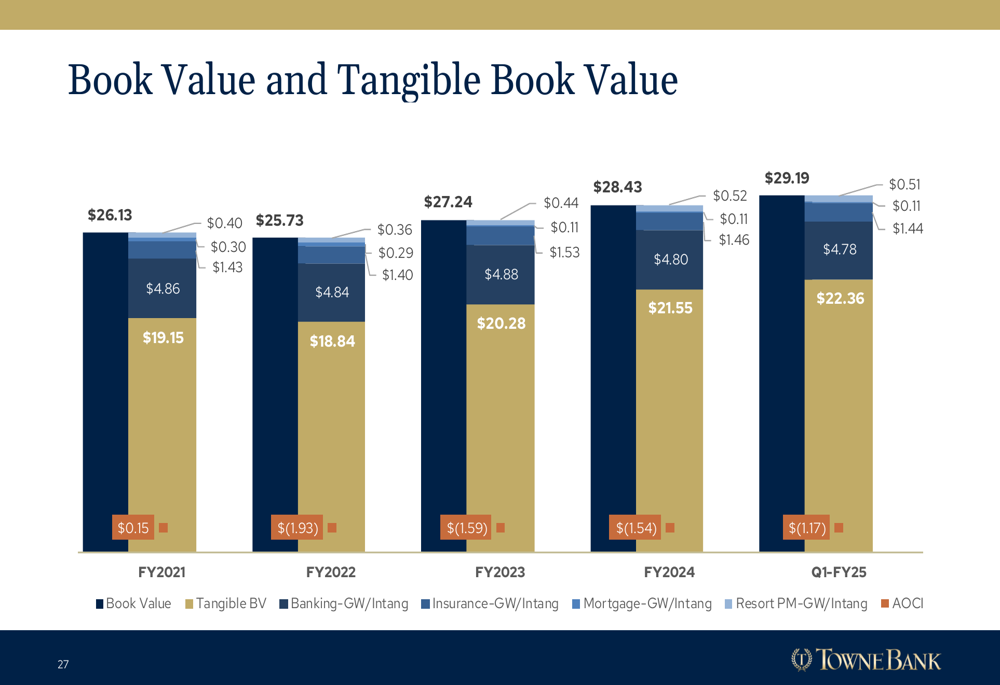

The bank’s capital position remained robust, with a total risk-based capital ratio of 15.65%, well above regulatory requirements. Tangible book value per share increased to $22.36, up 3.8% quarter-over-quarter and 10.1% year-over-year, demonstrating continued shareholder value creation.

TowneBank’s shareholder returns have significantly outpaced its peers, with a 10-year total shareholder return of 181% compared to the peer average of 93%. The bank maintained its quarterly dividend at $0.25 per share in Q1 2025.

As shown in the following chart, TowneBank has consistently created shareholder value through increasing book value and tangible book value per share:

Forward-Looking Statements

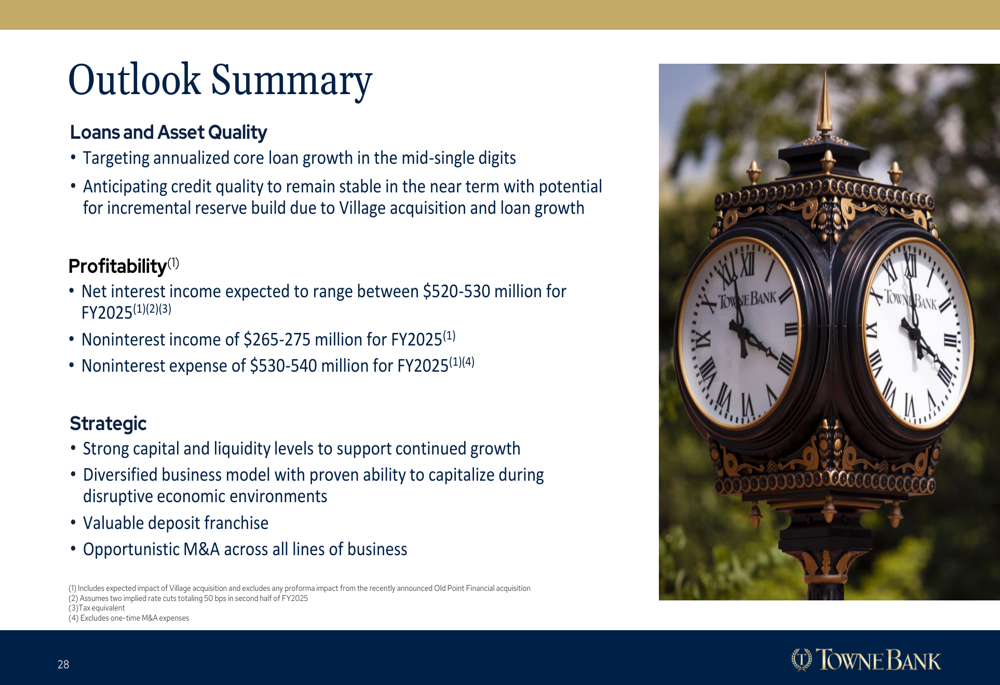

Looking ahead, TowneBank provided guidance for fiscal year 2025, targeting mid-single-digit annualized core loan growth with stable credit quality. The bank expects net interest income to range between $520-530 million, noninterest income of $265-275 million, and noninterest expense of $530-540 million for FY2025.

The outlook summary below highlights TowneBank’s expectations for the remainder of 2025:

Management emphasized the bank’s strong capital and liquidity levels, diversified business model, and valuable deposit franchise as key strengths. The bank also indicated it would pursue opportunistic mergers and acquisitions as part of its strategic initiatives.

TowneBank’s stock (NASDAQ:TOWN) closed at $34.56 on June 2, 2025, down 0.78% for the day. The stock has traded between $25.70 and $38.28 over the past 52 weeks, reflecting the overall market volatility but demonstrating resilience supported by the bank’s strong financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.