What happens to stocks if AI loses momentum?

Introduction & Market Context

TowneBank (NASDAQ:TOWN) reported mixed second-quarter 2025 results, with strong revenue growth offset by declining net income. The Virginia-based regional bank, which has expanded its footprint across the Mid-Atlantic region, saw its stock trade at $34.49 on August 4, 2025, up 1.39% for the day and within its 52-week range of $29.43 to $38.28.

The bank has maintained its position as the market leader in the Hampton Roads region while continuing to diversify its revenue streams through its insurance, mortgage, and property management businesses. TowneBank has been recognized on Forbes’ Best Banks List for seven consecutive years, underscoring its consistent performance in the competitive regional banking landscape.

Quarterly Performance Highlights

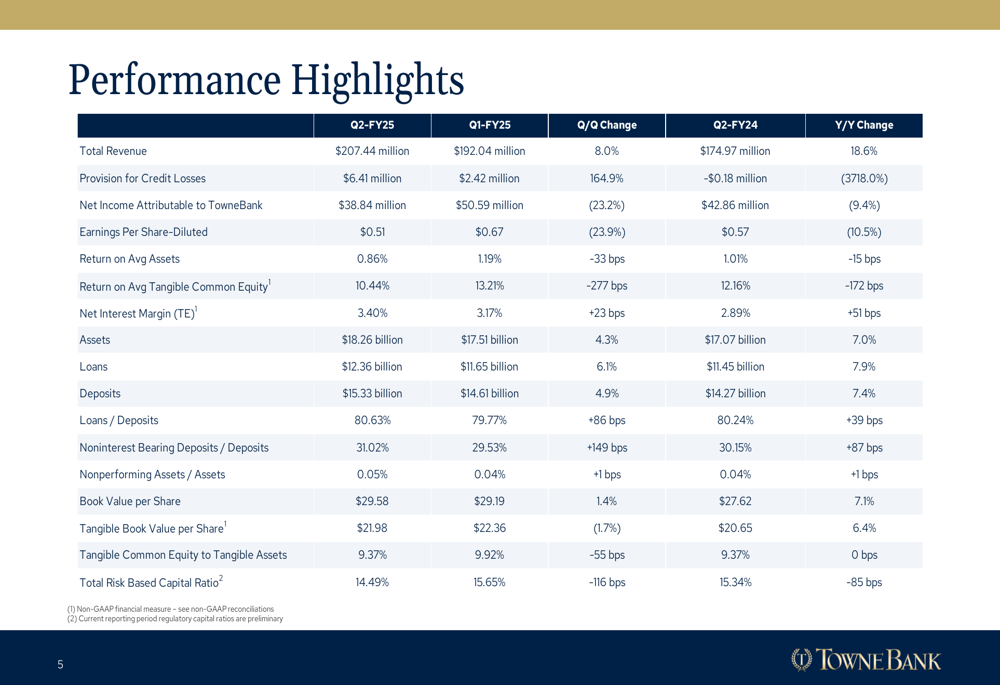

TowneBank reported total revenue of $207.44 million for Q2 2025, representing an impressive 18.6% increase year-over-year and an 8.0% increase quarter-over-quarter. However, net income attributable to TowneBank declined to $38.84 million, down 9.4% from the same quarter last year and 23.2% from the previous quarter. Diluted earnings per share came in at $0.51.

As shown in the following comprehensive performance comparison chart, the bank’s core metrics show mixed results when compared to previous periods:

The bank’s core net income, which excludes non-recurring items, was $61.34 million with core earnings per share of $0.81. Total (EPA:TTEF) assets grew to $18.26 billion, up 7.0% year-over-year, while loans increased to $12.36 billion, up 7.9% from Q2 2024. Deposits rose to $15.33 billion, representing a 7.4% increase year-over-year.

Net interest income showed particularly strong growth, reaching $137.21 million in Q2 2025, up 25.8% year-over-year and 13.9% quarter-over-quarter. The net interest margin (FTE) stood at 3.40%, reflecting the bank’s effective management of its interest-earning assets in the current rate environment.

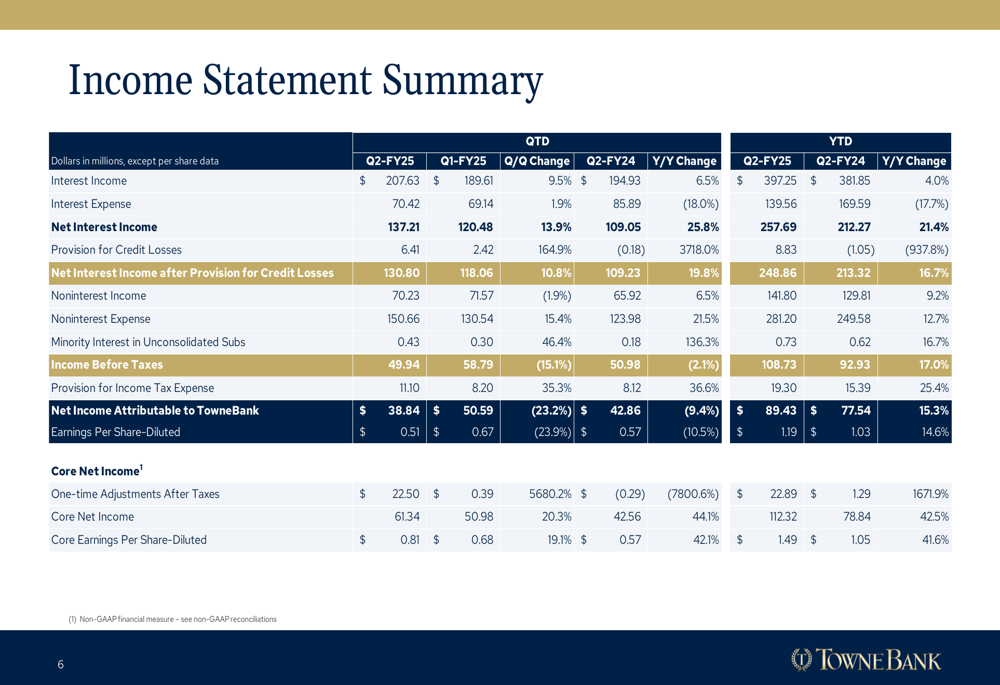

The following income statement summary provides a detailed breakdown of TowneBank’s financial performance:

Segment Performance

TowneBank operates a diversified business model with four key segments: banking, insurance, mortgage, and property management. Each segment contributed differently to the overall performance in Q2 2025.

Insurance

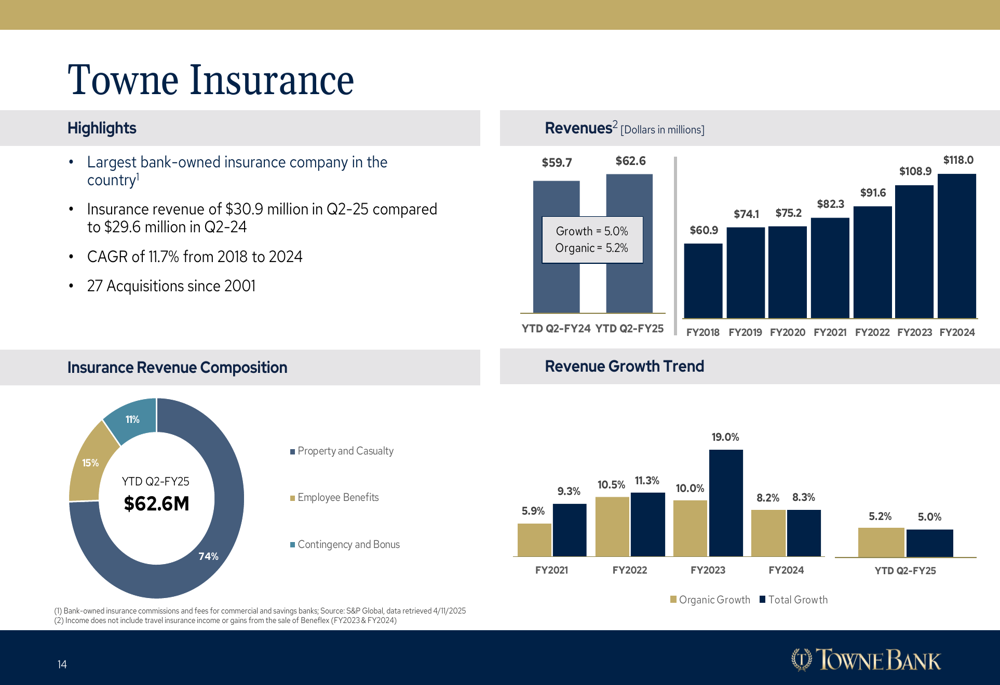

Towne Insurance, which the bank claims is the largest bank-owned insurance company in the country, generated revenue of $30.9 million in Q2 2025, up from $29.6 million in Q2 2024. The insurance division has demonstrated consistent growth with a compound annual growth rate (CAGR) of 11.7% from 2018 to 2024, supported by 27 acquisitions since 2001.

The following chart illustrates the composition and growth of the insurance segment:

Mortgage

TowneBank Mortgage reported mortgage banking income of $14.1 million in Q2 2025, slightly up from $14.0 million in Q2 2024. However, the bank noted that "uncertainty associated with government efficiency initiatives continues to weigh on our Northern Virginia and Maryland markets." The gain on sales and fees as a percentage of loans originated decreased by 5 basis points compared to Q1 2025.

Property Management

Towne Vacations, the bank’s property management division, generated net income of $15.6 million in Q2 2025, up from $14.3 million in Q2 2024. The division operates in multiple states including North Carolina, South Carolina, Maryland, Tennessee, and Florida. The bank completed the acquisition of a property management business in Northwest Florida, which had its full-quarter impact in Q1 2025. However, the bank noted that the "vacation rental industry continues to be adversely impacted by macro economic uncertainties."

Wealth Management

The wealth management division reported investment commissions income of $3.2 million in Q2 2025, up from $2.6 million in Q2 2024. Assets under management reached $5.9 billion at the end of Q2 2025, reflecting the bank’s growing presence in this segment.

Balance Sheet & Asset Quality

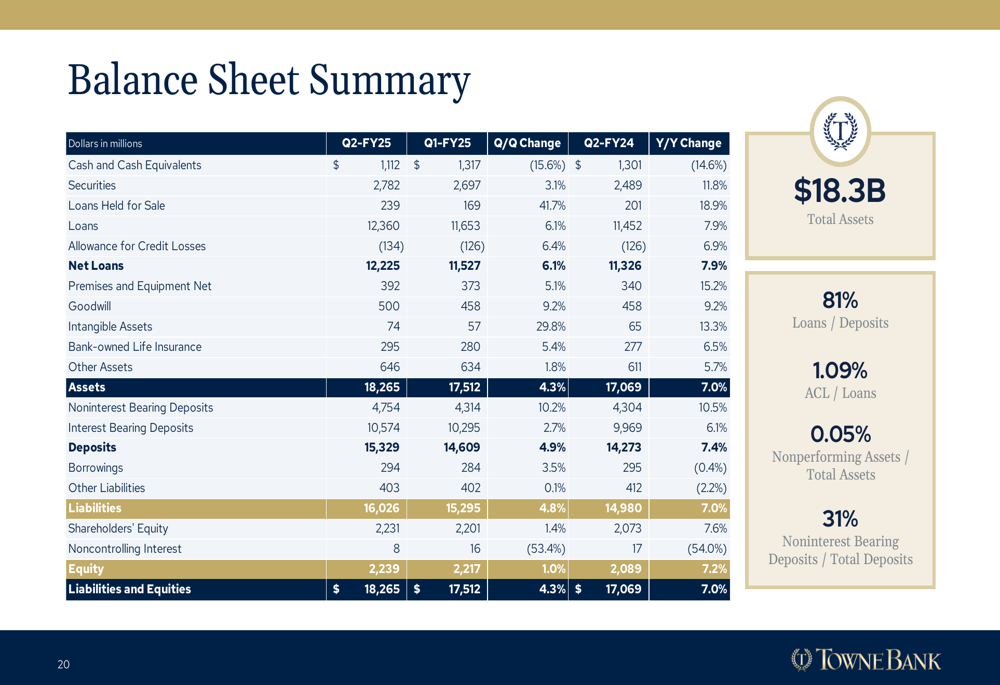

TowneBank’s balance sheet showed solid growth and strong asset quality metrics in Q2 2025. The following balance sheet summary provides a comprehensive overview:

The bank maintained a loan-to-deposit ratio of 80.63%, indicating a conservative lending approach while still supporting growth. Noninterest-bearing deposits represented 31.02% of total deposits, providing a stable and low-cost funding source. The bank reported that it has experienced four consecutive quarterly decreases in deposit costs since Q2 2024, with a cumulative decrease of 71 basis points in interest-bearing deposit costs.

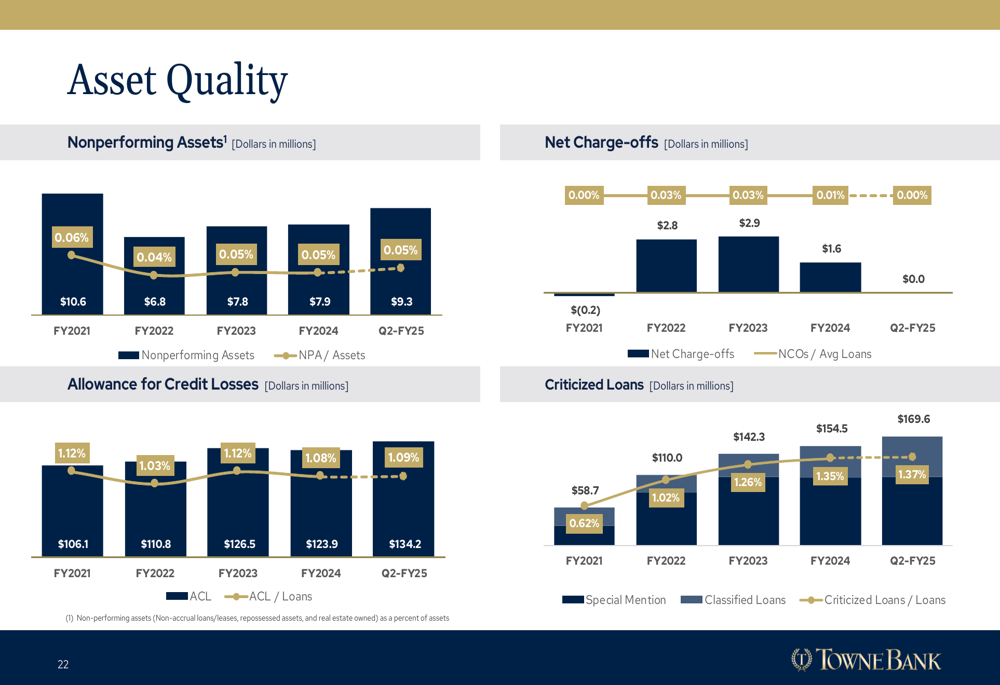

Asset quality remained exceptional, with nonperforming assets at just 0.05% of total assets. The allowance for credit losses stood at 1.09% of total loans. The following chart illustrates the bank’s consistently strong asset quality metrics:

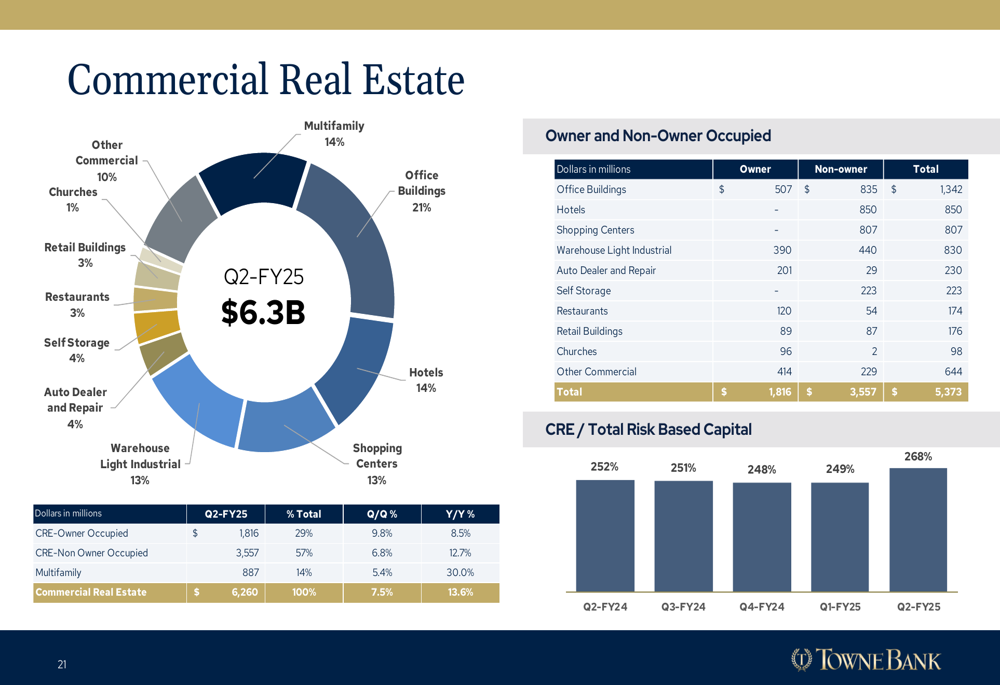

TowneBank’s commercial real estate (CRE) portfolio, a key component of its loan book, is well-diversified across various property types. The following breakdown shows the composition of the CRE portfolio:

The bank maintains strong capital ratios, with a total risk-based capital ratio of 14.49%, well above regulatory requirements for well-capitalized institutions.

Forward Outlook

For fiscal year 2025, TowneBank provided the following guidance:

- Targeting annualized core loan growth in the mid-single digits

- Anticipating stable credit quality in the near term with potential for incremental reserve build due to M&A and loan growth

- Net interest income expected to range between $545-555 million

- Noninterest income projected at $265-270 million

- Noninterest expense estimated at $525-535 million

The bank’s diversified business model, strong deposit franchise, and exceptional asset quality position it well to navigate the current economic environment. However, challenges remain, including pressure on the mortgage and vacation rental businesses due to macroeconomic uncertainties.

TowneBank’s consistent focus on earnings and growth has resulted in an earnings growth CAGR of 22.7% from FY2000 to FY2024, and a 10-year total shareholder return of 178% as of June 30, 2025. The bank’s strategy of combining traditional banking services with complementary businesses in insurance, mortgage, property management, and wealth management provides multiple revenue streams and growth opportunities, even as it faces headwinds in certain segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.