Nvidia shares pop as analysts dismiss AI bubble concerns

Introduction & Market Context

TransAlta Corporation (TSX:TA) presented its second quarter 2025 results on August 1, showcasing solid financial performance that drove its stock price up 7.65% to $23.49. The Canadian power producer's diverse energy portfolio and strategic initiatives in data centers and energy transition contributed to the positive market reaction, with the stock trading near its 52-week high of $23.75.

The company's presentation highlighted year-over-year improvements in key financial metrics, with particular strength in its hydro segment, while advancing strategic initiatives focused on repurposing legacy generation assets for future growth opportunities.

Quarterly Performance Highlights

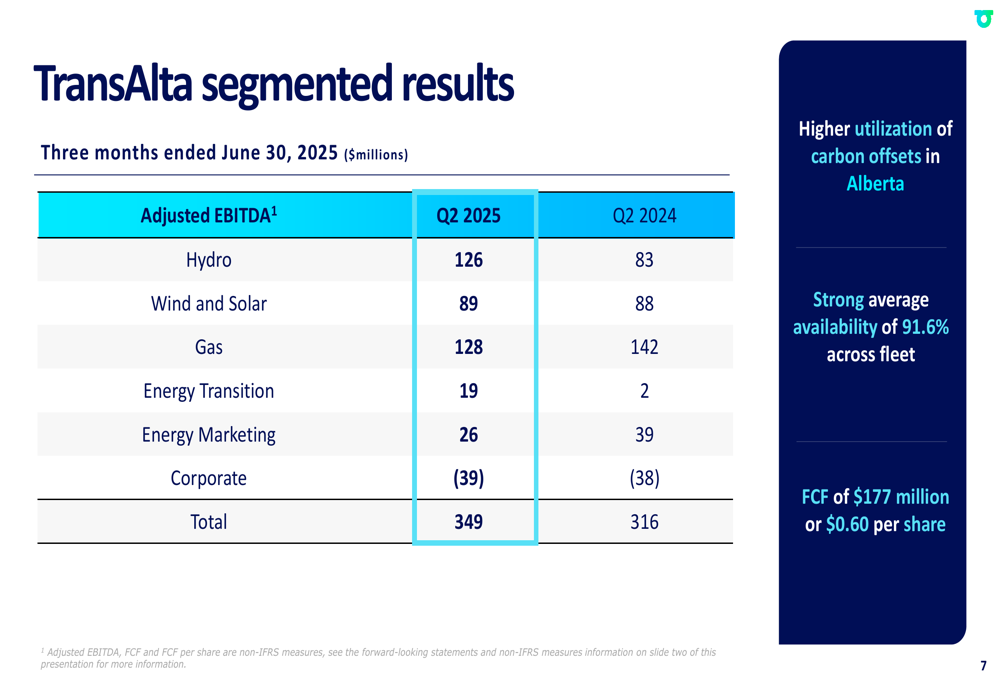

TransAlta reported adjusted EBITDA of $349 million for Q2 2025, representing a 10.4% increase from $316 million in the same period last year. Free cash flow reached $177 million or $0.60 per share, while the company maintained strong fleet availability at 91.6%.

As shown in the detailed segmented results, the hydro business was the standout performer:

The hydro segment saw a substantial year-over-year increase of $43 million, reaching $126 million in Q2 2025 compared to $83 million in Q2 2024. Wind and solar performance remained relatively stable at $89 million (up $1 million), while the gas segment declined by $14 million to $128 million. The energy transition segment showed marked improvement, increasing from $2 million to $19 million.

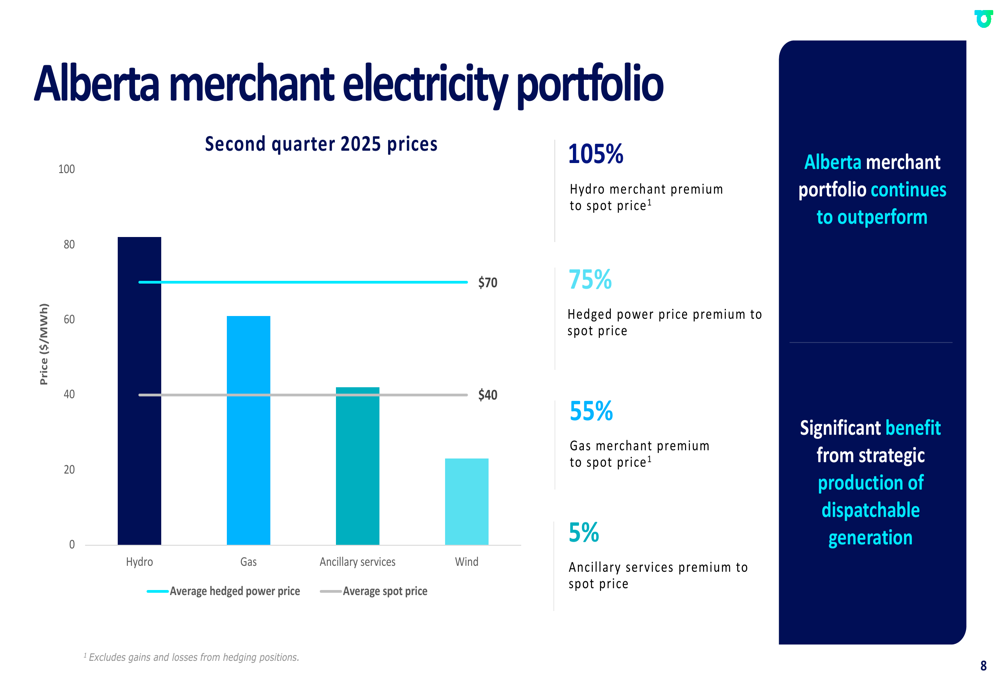

TransAlta's Alberta merchant electricity portfolio continued to outperform spot prices across its generation types, demonstrating the value of the company's strategic positioning and operational flexibility:

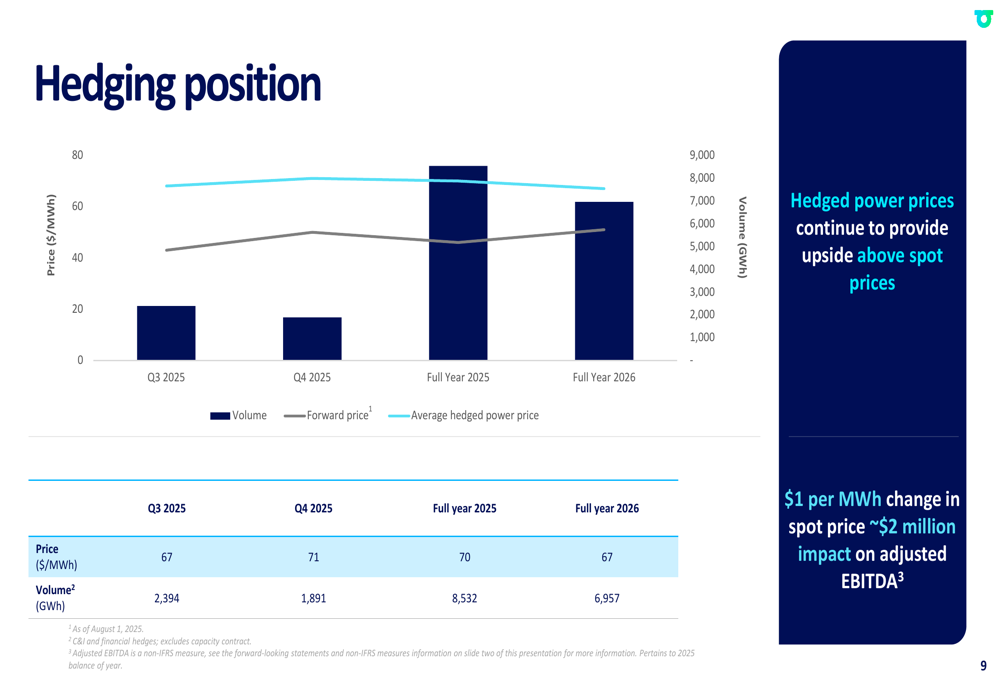

The company's hedging strategy has also positioned it well for the remainder of 2025 and into 2026, with hedged power prices providing upside above spot prices:

Strategic Initiatives

CEO John Kousinioris emphasized two key strategic priorities during the presentation: advancing the Alberta data center project and progressing the Centralia Unit 2 conversion.

The Alberta data center initiative is moving toward a Memorandum of Understanding following the Alberta Electric System Operator's (AESO) phase I large load allocation. The company is engaged in active commercial negotiations with counterparties, with a timeline for contract execution expected by mid-September 2025.

Meanwhile, the Centralia Unit 2 conversion project is advancing toward a definitive agreement expected in the second half of 2025, which would secure a long-term contract for 100% of the facility's capacity with potential for future expansion.

"We delivered exceptional results during the second quarter," Kousinioris stated in the earnings call. He expressed confidence that Alberta would develop a framework supporting the company's data center ambitions, which represent a significant growth opportunity for TransAlta's legacy generation assets.

Forward-Looking Statements

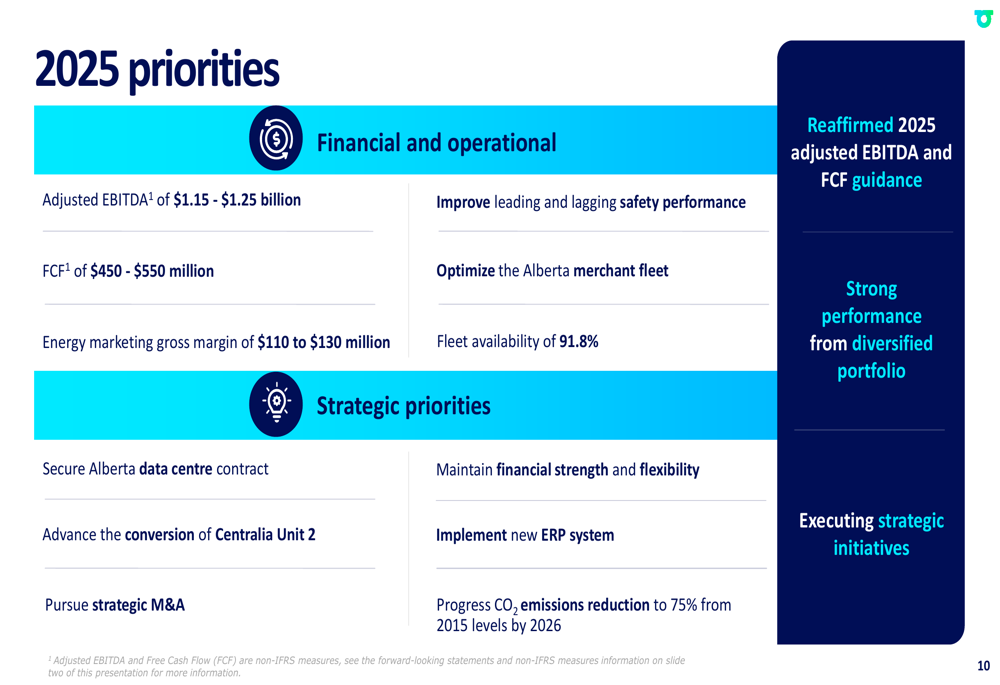

TransAlta reaffirmed its 2025 financial guidance, projecting adjusted EBITDA of $1.15-1.25 billion and free cash flow of $450-550 million. The company also outlined its operational targets, including energy marketing gross margin of $110-130 million and fleet availability of 91.8%.

Strategic priorities for the remainder of 2025 include:

The company continues to balance financial performance with its energy transition goals, targeting a 75% reduction in CO2 emissions from 2015 levels by 2026.

Competitive Industry Position

TransAlta positions itself as a clean electricity leader with a diversified and increasingly contracted portfolio. The company highlighted its value proposition, emphasizing its role as a safe and reliable operator with high-potential legacy energy campuses that provide unique redevelopment opportunities.

The company's capital allocation strategy includes share repurchases, with 1.9 million shares bought back year-to-date at an average cost of $12.42, significantly below the current trading price. This reflects management's confidence in the company's intrinsic value and future prospects.

Conclusion

TransAlta's Q2 2025 results demonstrate the company's ability to generate strong financial performance while advancing its strategic transition toward lower-carbon operations and new growth opportunities. The 10% year-over-year increase in adjusted EBITDA, driven primarily by hydro operations, highlights the value of the company's diverse generation portfolio.

As TransAlta progresses with its data center initiatives and Centralia conversion project, investors will be watching closely for definitive agreements that could further validate the company's strategy of repurposing legacy assets. With the stock trading near its 52-week high following the results announcement, market sentiment appears to support management's strategic direction and execution capabilities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.