JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

TransUnion (NYSE:TRU) reported strong first-quarter 2025 results on April 24, exceeding guidance across key metrics while maintaining its full-year outlook despite growing economic uncertainties. The credit reporting and analytics company posted 8% organic constant currency revenue growth, marking its sixth consecutive quarter of outperformance.

The company’s shares rose 2.25% to $77.26 following the earnings announcement, continuing the positive momentum seen after its Q4 2024 results when the stock jumped over 6%. TransUnion’s performance comes amid a backdrop of cautious optimism from lenders regarding credit growth, supported by healthy consumer finances but tempered by subdued credit volumes.

"Lenders entered 2025 with cautious optimism for credit growth, supported by healthy consumer finances," noted the company in its presentation, while acknowledging that "new U.S. trade and fiscal policy proposals add uncertainty around levels of inflation, employment, interest rates and economic growth."

Quarterly Performance Highlights

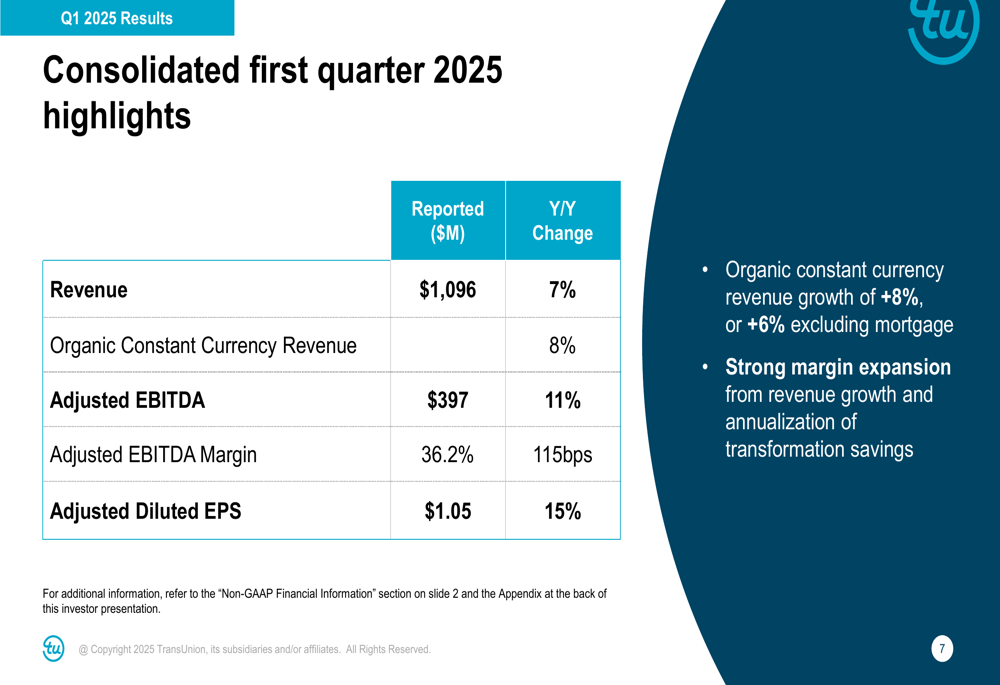

TransUnion delivered impressive financial results for Q1 2025, with revenue reaching $1,096 million, up 7% year-over-year, or 8% on an organic constant currency basis. Excluding mortgage, organic constant currency revenue grew 6%.

The company’s profitability metrics showed even stronger improvement, with Adjusted EBITDA increasing 11% to $397 million and Adjusted EBITDA margin expanding 115 basis points to 36.2%. Adjusted Diluted EPS rose 15% to $1.05.

As shown in the following consolidated financial highlights:

The company attributed its margin expansion to revenue growth and the annualization of transformation savings from its ongoing technology modernization and operating model optimization initiatives.

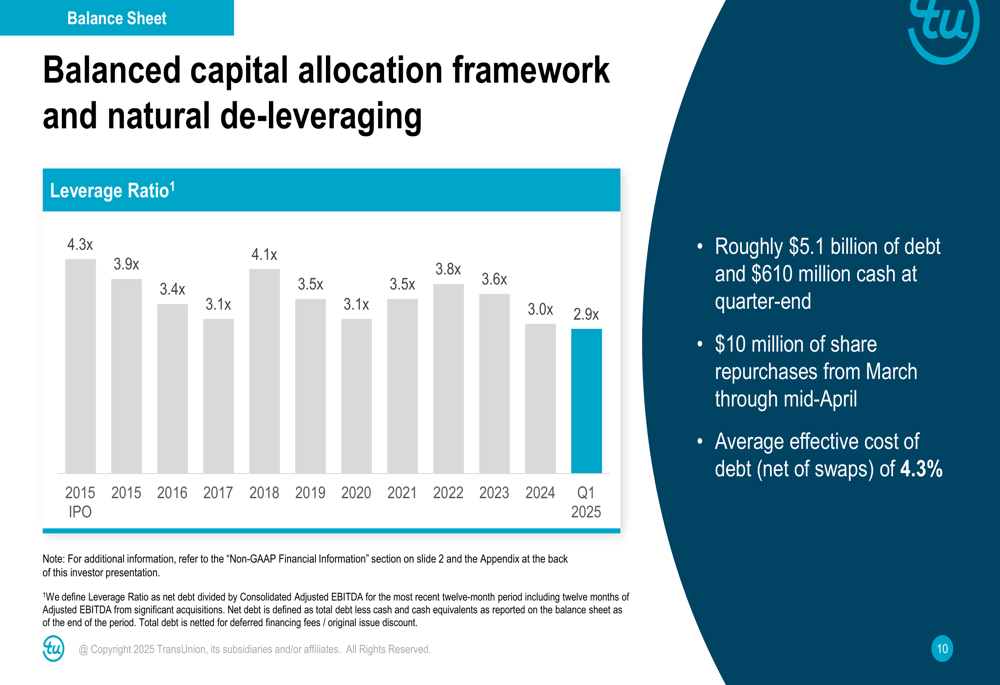

TransUnion also continued its deleveraging efforts, with its leverage ratio decreasing to 2.9x at quarter-end, down from 4.3x in 2015. The company repurchased $10 million in shares from March through mid-April.

Segment Analysis

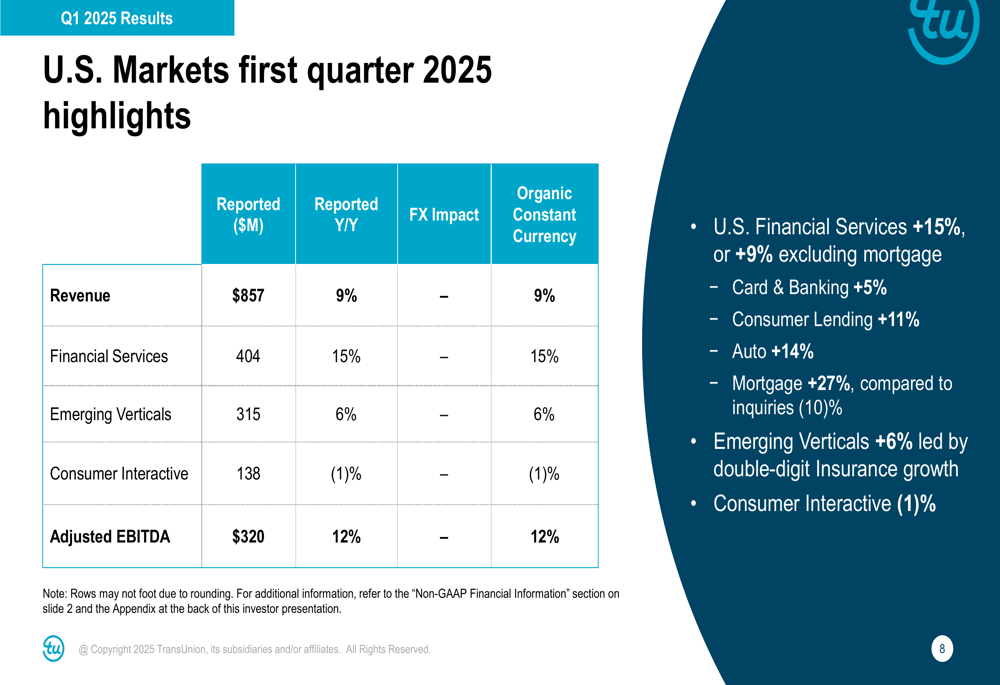

The U.S. Markets segment, which accounts for the largest portion of TransUnion’s business, delivered strong performance with revenue of $857 million, up 9% on an organic constant currency basis. Financial Services was the standout performer, growing 15% to $404 million, driven by significant growth across all subsegments.

Particularly notable was the 27% growth in mortgage revenue, which outperformed the broader mortgage market where inquiries declined 10%. Other Financial Services subsegments also showed robust growth, with Auto up 14%, Consumer Lending up 11%, and Card & Banking up 5%.

The detailed breakdown of U.S. Markets performance is illustrated below:

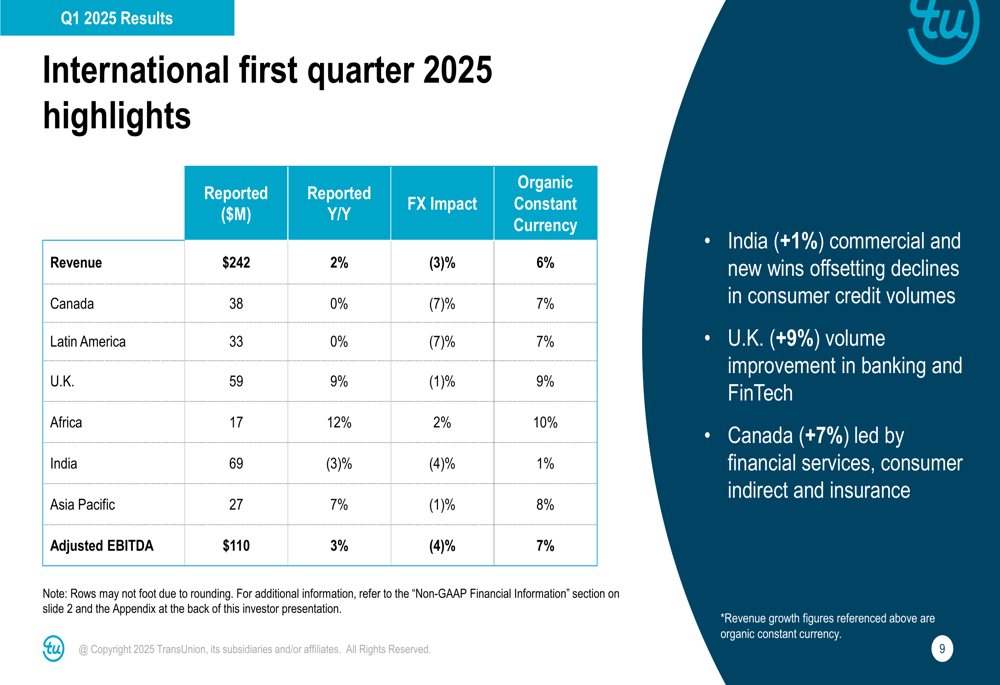

TransUnion’s International segment generated $242 million in revenue, up 6% on an organic constant currency basis. Most regions showed strong performance with high-single-digit growth, including the U.K. (+9%), Africa (+10%), Canada (+7%), Latin America (+7%), and Asia Pacific (+8%). India posted modest 1% growth, which the company noted was "as anticipated" with commercial and new wins offsetting declines in consumer credit volumes.

The following chart details the International segment’s performance:

Strategic Initiatives and Technology Transformation

TransUnion highlighted progress on several strategic initiatives during the quarter. The company is transitioning over 90 U.S. credit customers to its new OneTru platform and launched OneTru Assist, an AI-powered tool designed to enhance developer productivity.

The company also completed the acquisition of Monevo and plans to launch a freemium solution by the end of Q2 2025, which aligns with the freemium credit management platform launched with Credit Sesame mentioned in the Q4 2024 earnings report.

TransUnion strengthened its leadership team with the appointments of Tiffani Chambers as Chief Operations Officer and Mohamed Abdelsadek as Chief Global Solutions Officer, positioning the company to better execute on its global operating model and accelerate innovation.

The company’s technology modernization efforts continue to progress, with expected benefits including $200 million in free cash flow improvement by 2026 and approximately $95 million in run-rate operating expense savings by the end of 2024.

Forward-Looking Statements and Guidance

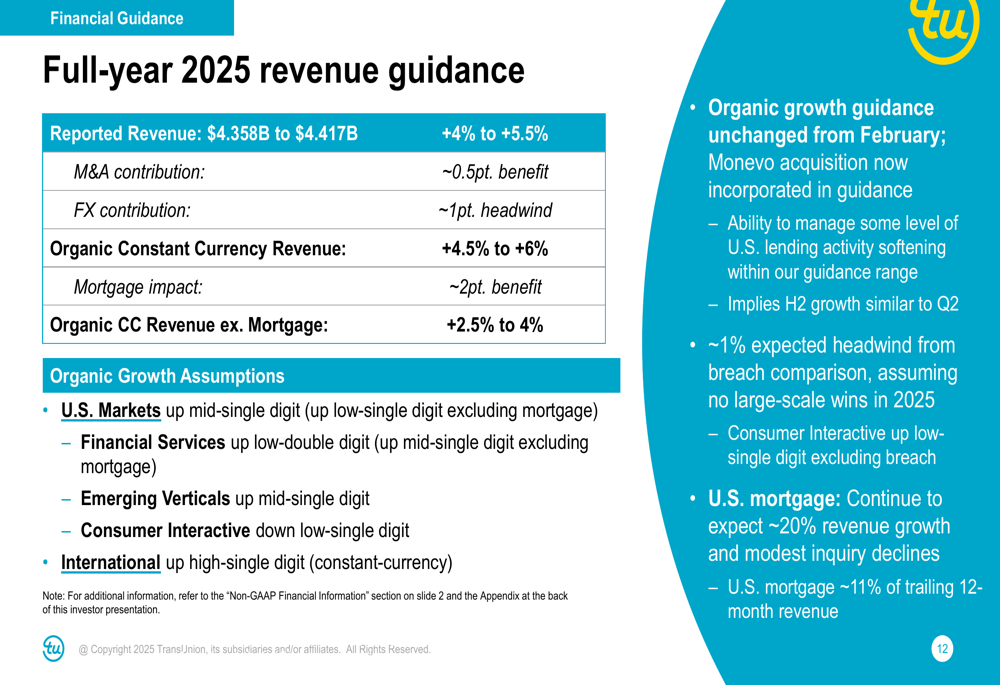

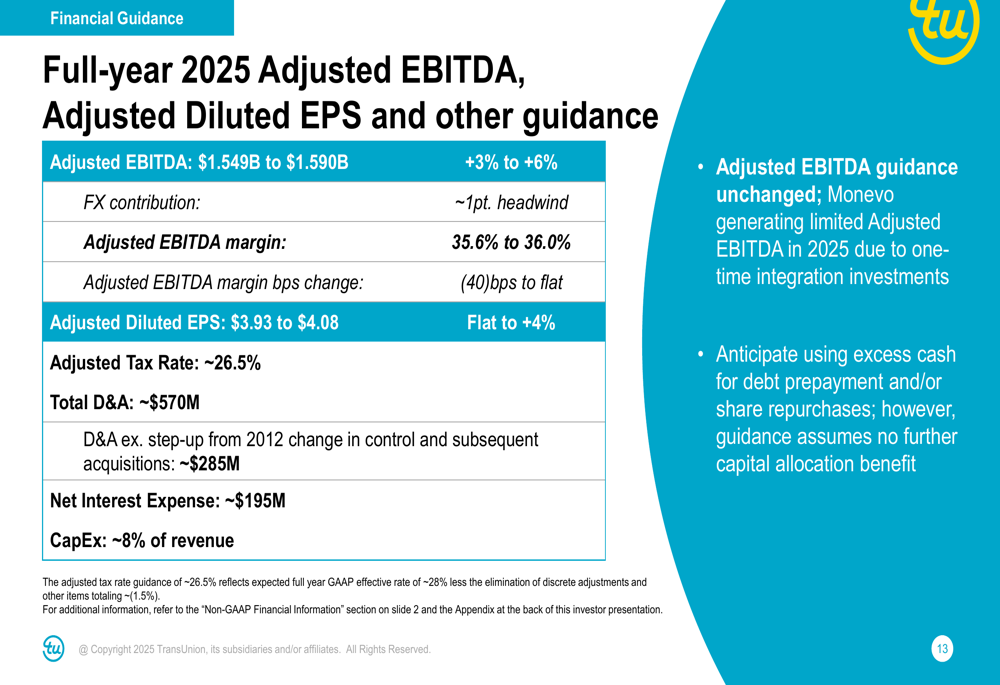

Despite exceeding Q1 expectations, TransUnion maintained its full-year 2025 organic constant currency revenue growth guidance of 4.5% to 6% and Adjusted Diluted EPS guidance of $3.93 to $4.08 (flat to +4%). The company cited increased market uncertainty as a reason for its conservative approach.

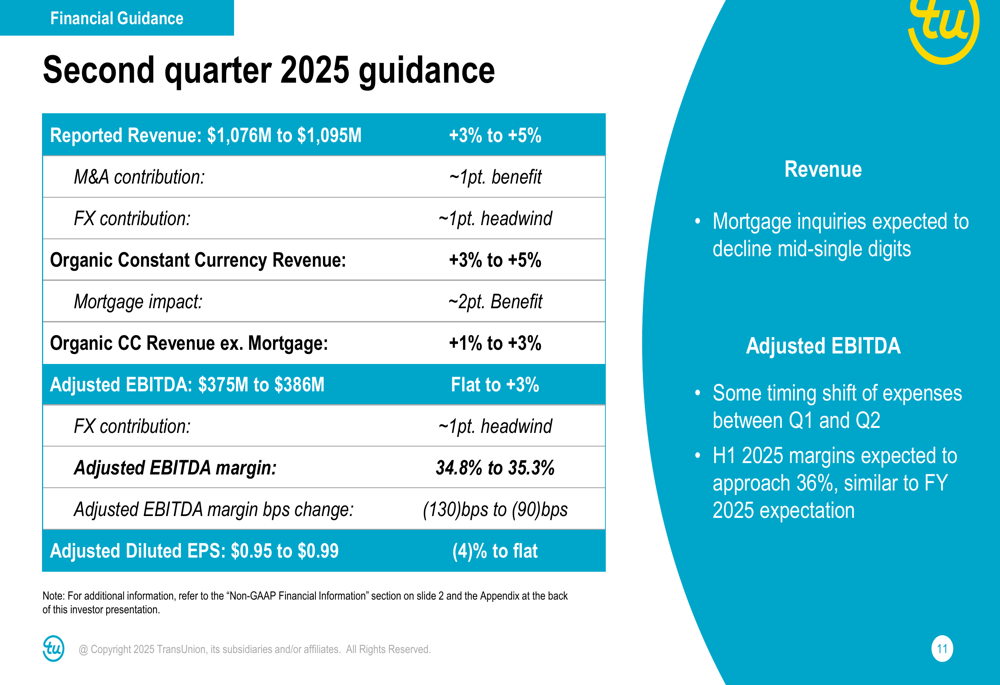

For the second quarter of 2025, TransUnion expects:

The full-year 2025 revenue guidance remains unchanged from February, with the Monevo acquisition now incorporated:

Similarly, the company maintained its Adjusted EBITDA and EPS guidance for the full year:

TransUnion emphasized its portfolio resilience in the face of economic uncertainty, noting its track record of through-cycle revenue growth, including 3% growth during the COVID-impacted 2020 and 3% growth during the rate-hike cycle of 2022-2023. The company highlighted its diversification across solutions, verticals, and geographies, with U.S. Financial Services now accounting for approximately one-third of revenue compared to about 60% in 2007.

"TransUnion grew through varying economic environments over the last decade, compounding revenue at high-single digits organically," the company stated in its presentation, underscoring its ability to navigate challenging market conditions.

The company’s first quarter performance continues the positive momentum seen in Q4 2024, when it reported 9% revenue growth and exceeded expectations. With its diversified portfolio and ongoing transformation initiatives, TransUnion appears well-positioned to maintain its growth trajectory despite market uncertainties in 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.