BofA sees higher gold prices, likely to hit $5,000/oz in 2026

Introduction & Market Context

Trimble Inc. (NASDAQ:TRMB) released its first quarter 2025 earnings presentation on May 7, highlighting continued strong growth in Annual Recurring Revenue (ARR) that exceeded guidance, despite year-over-year pressure on margins. The positioning technology leader reported progress in its business transformation strategy, including the completed divestiture of its mobility business in February 2025.

The company’s shares reacted positively to the results in premarket trading, rising 2.65% to $65.00, following a 1.2% decline to $63.32 in the previous session.

Q1 2025 Performance Highlights

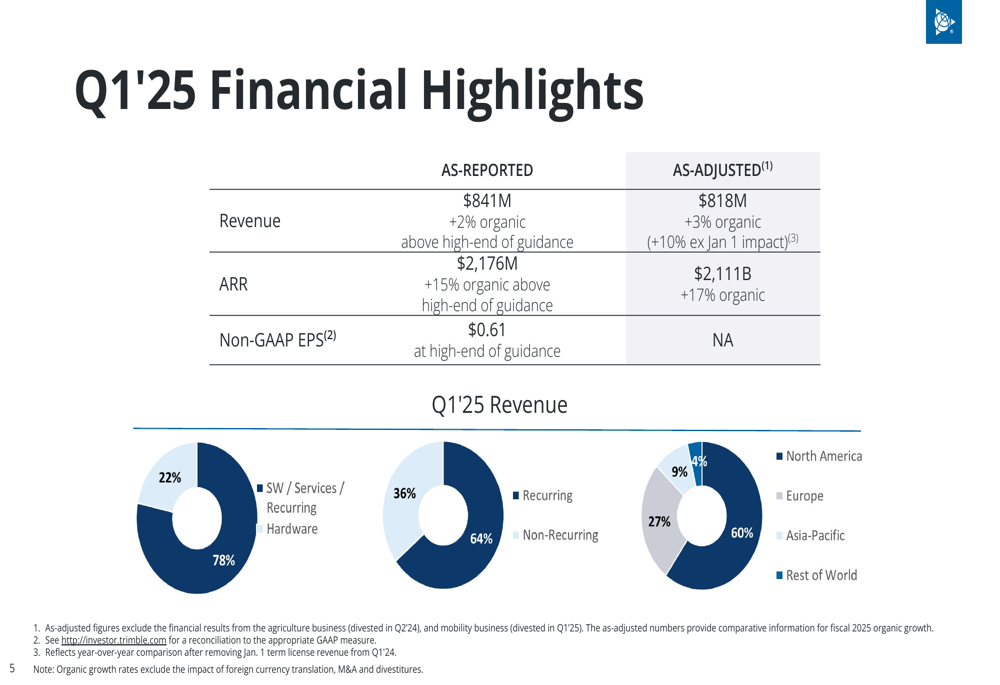

Trimble reported Q1 2025 revenue of $841 million, representing 2% organic growth and exceeding the high end of its guidance. Annual Recurring Revenue (ARR) reached $2.176 billion, growing 15% organically, also above the high end of guidance. Non-GAAP earnings per share came in at $0.61, hitting the high end of the company’s projected range.

As shown in the following financial highlights:

On an as-adjusted basis, which provides a clearer picture of underlying performance, Trimble achieved revenue of $818 million, representing 3% organic growth year-over-year. When excluding the impact of January 1 term license revenue from Q1 2024, organic growth was even stronger at 10%. As-adjusted ARR reached $2.111 billion, growing 17% organically.

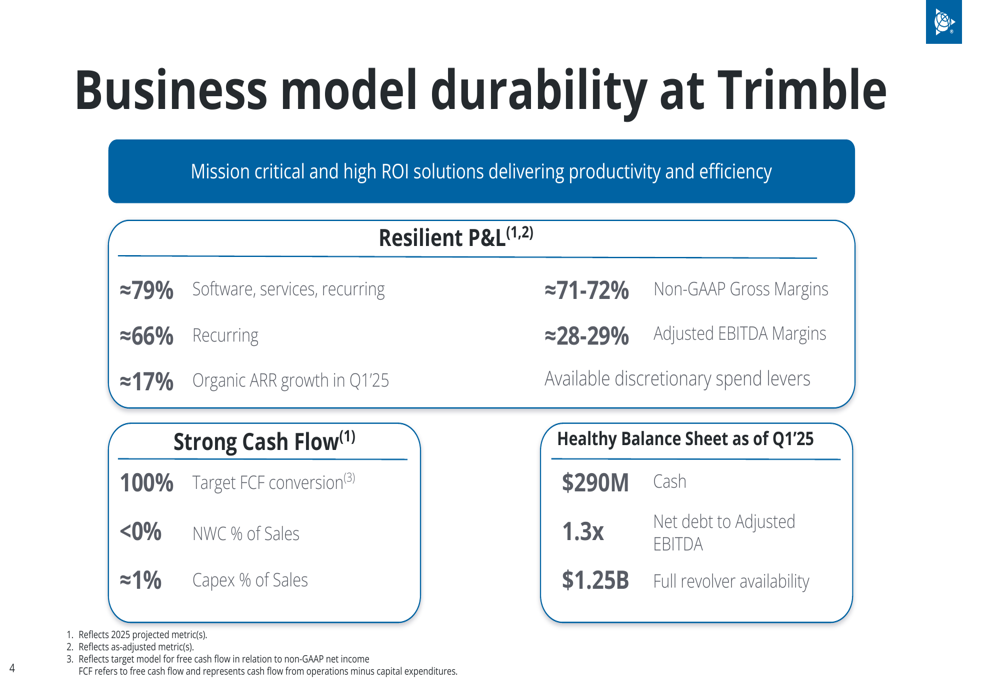

The company’s business model continues to demonstrate durability, with approximately 79% of revenue coming from software, services, and recurring revenue sources. Recurring revenue specifically accounts for about 66% of total revenue, with organic ARR growth reaching 17% in Q1 2025.

Segment Analysis

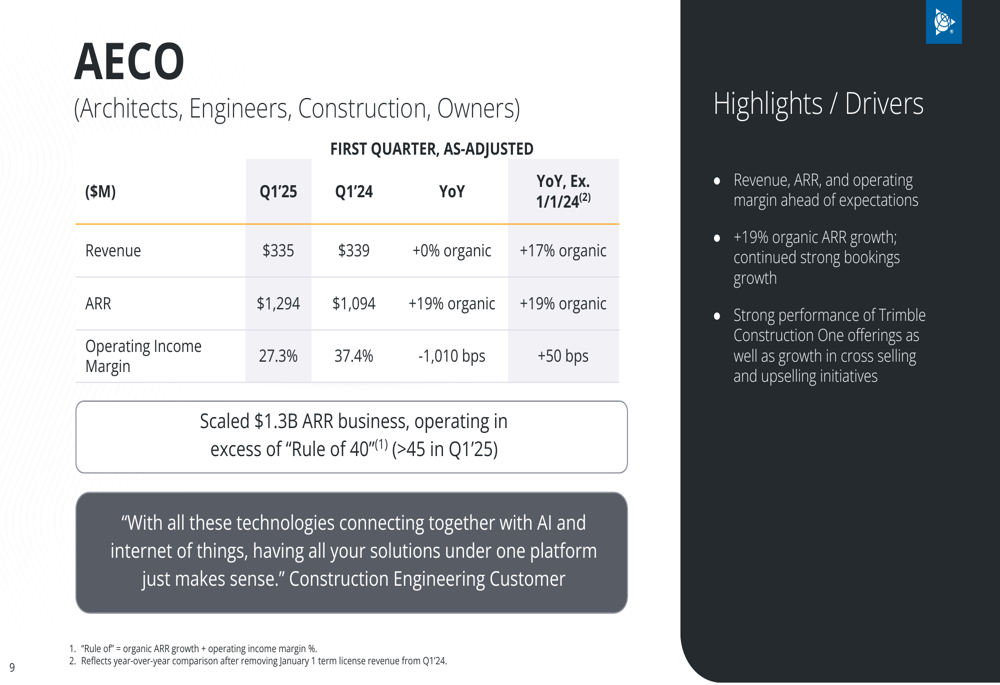

Trimble’s AECO (Architects, Engineers, Construction, Owners) segment showed remarkable ARR growth despite flat revenue performance. On an as-adjusted basis, AECO revenue was $335 million, flat year-over-year organically, but ARR grew 19% organically to $1.294 billion. Operating income margin was 27.3%, down 1,010 basis points year-over-year. However, when removing the impact of January 1 term license revenue from Q1 2024, organic revenue growth was 17% with a 50 basis point improvement in operating margin.

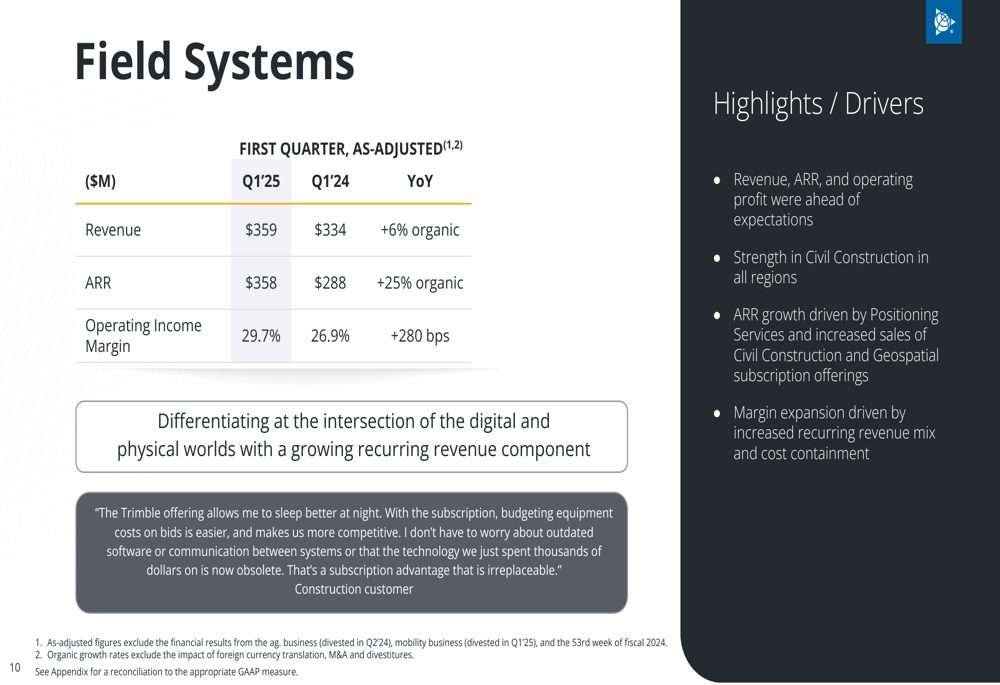

The Field Systems segment delivered the strongest overall performance in the quarter. Revenue reached $359 million, up 6% organically, while ARR grew an impressive 25% organically to $358 million. Operating income margin expanded 280 basis points to 29.7%. The company noted that strength in Civil Construction across all regions drove the segment’s outperformance, with margin expansion resulting from increased recurring revenue mix and cost containment.

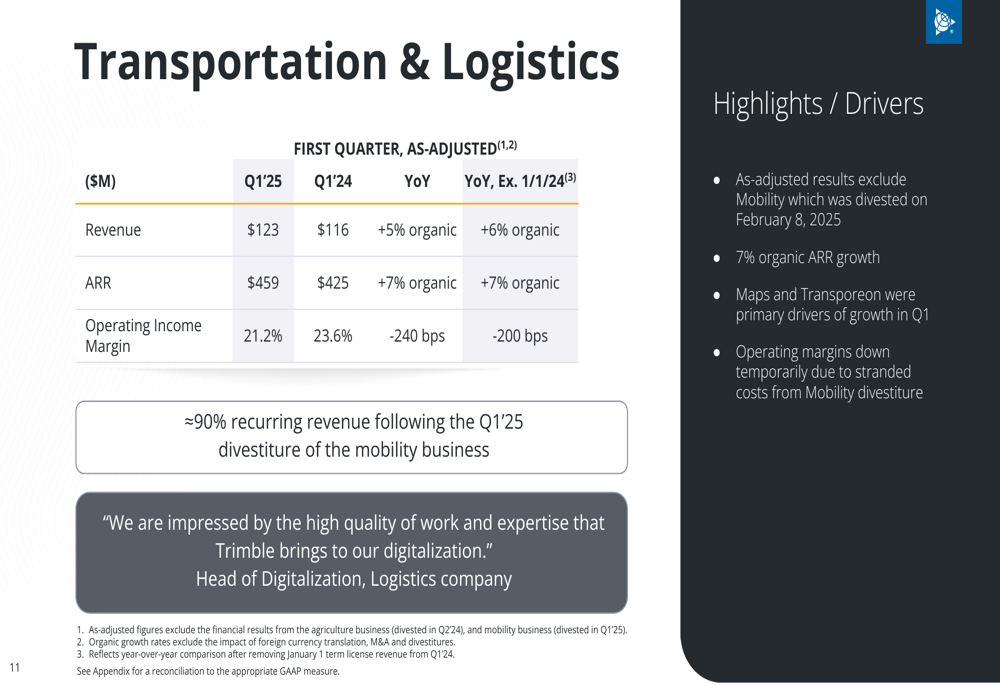

The Transportation & Logistics segment reported $123 million in revenue, up 5% organically, with ARR growing 7% organically to $459 million. Operating income margin declined 240 basis points to 21.2%. This segment underwent significant transformation with the divestiture of the mobility business on February 8, 2025, resulting in approximately 90% recurring revenue for the remaining business. The company noted that operating margins were temporarily down due to stranded costs from the mobility divestiture.

Balance Sheet and Cash Flow

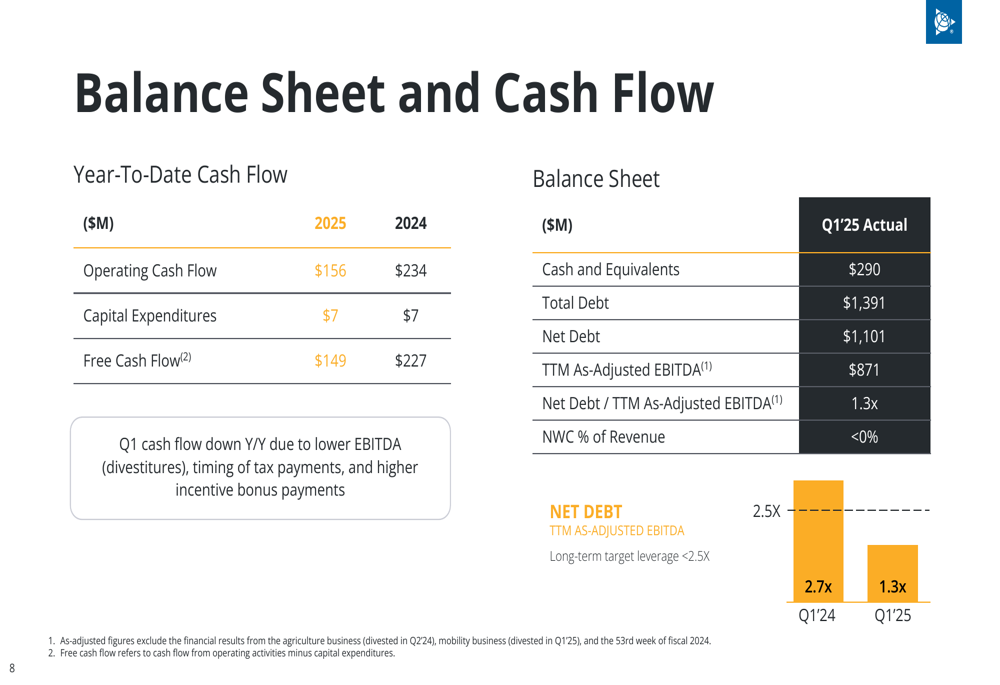

Trimble continues to strengthen its financial position, with net debt to TTM as-adjusted EBITDA improving to 1.3x, down significantly from 2.7x in Q1 2024. Cash and equivalents stood at $290 million, with total debt of $1.391 billion.

Year-to-date operating cash flow was $156 million, compared to $234 million in the same period of 2024. Free cash flow reached $149 million, down from $227 million in the prior year. The company maintains a healthy balance sheet with working capital as a percentage of revenue below zero.

Future Outlook

Trimble maintained its full-year 2025 guidance, projecting as-adjusted ARR growth of 13% to 15% organically. Revenue is expected to be between $3.35 billion and $3.45 billion, representing 4.0% to 7.0% organic growth. Non-GAAP operating margin is projected at 26.3% to 27.3%, with adjusted EBITDA margin between 27.8% and 28.8%.

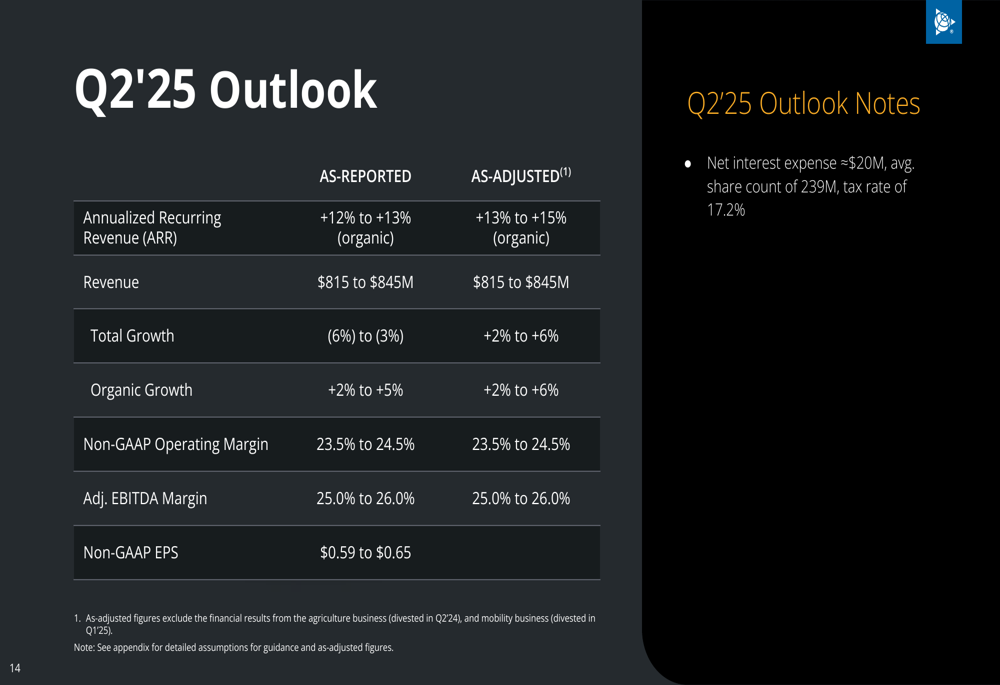

For the second quarter of 2025, Trimble expects as-adjusted ARR to increase 13% to 15% organically, with revenue between $815 million and $845 million, representing 2% to 6% organic growth. Non-GAAP EPS is projected to be between $0.59 and $0.65.

The company noted that operating margins are expected to increase in the second half of 2025, reflecting continued recurring revenue growth. However, free cash flow forecast was revised to approximately 0.5 times non-GAAP net income.

Strategic Initiatives

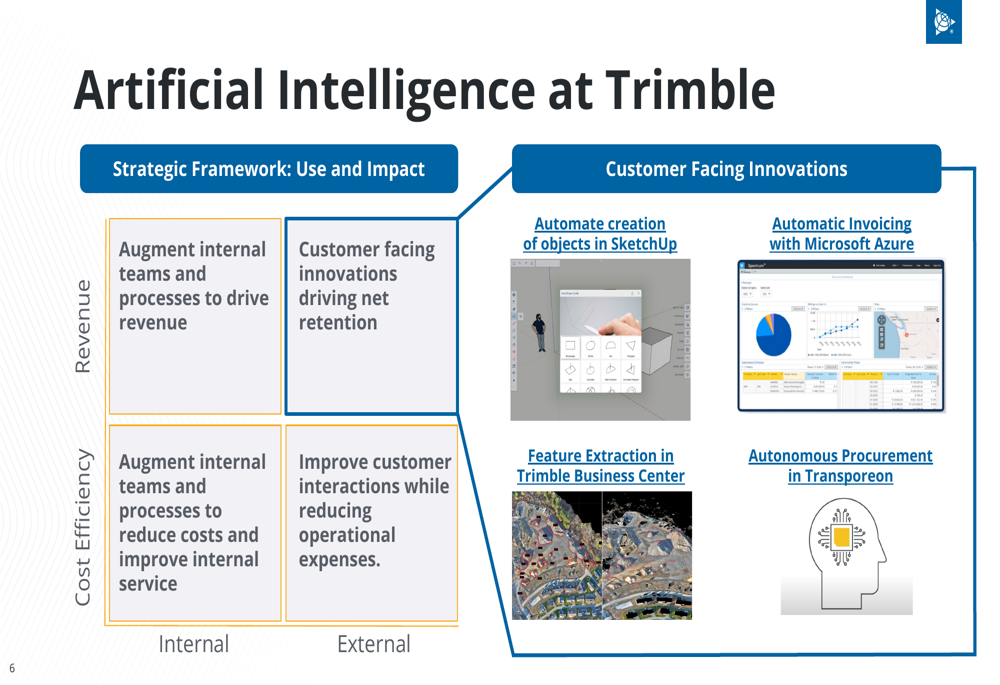

Trimble continues to advance its artificial intelligence strategy across the business. The company outlined a framework for AI implementation that focuses on both revenue generation and cost efficiency. Customer-facing innovations include automating the creation of objects in SketchUp, automatic invoicing with Microsoft (NASDAQ:MSFT) Azure, feature extraction in Trimble Business Center, and autonomous procurement in Transporeon.

This strategic focus on AI aligns with Trimble’s broader Connect and Scale strategy and its shift toward software and recurring revenue. The company’s Q1 results reflect this ongoing transformation, with software, services, and recurring revenue now comprising approximately 79% of total revenue.

In the previous quarter’s earnings call, CEO Rob Painter had highlighted the company’s portfolio shift toward software and recurring revenue, noting that it provides greater visibility into future performance. The Q1 2025 results demonstrate continued progress on this strategic path, with strong ARR growth across all segments despite some temporary margin pressure from the mobility business divestiture.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.