Five things to watch in markets in the week ahead

Introduction & Market Context

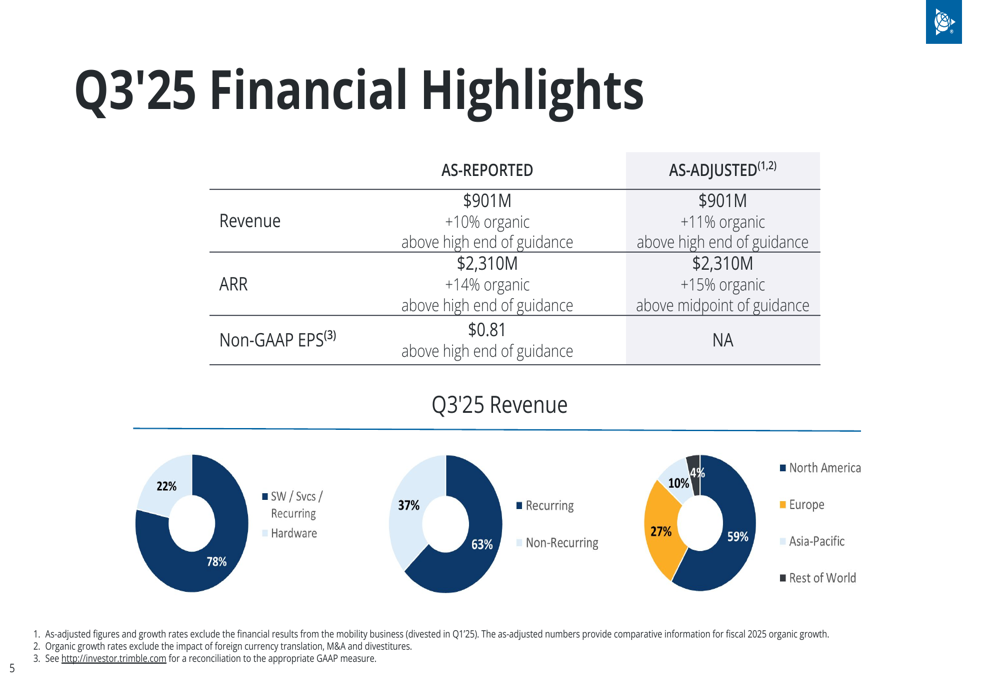

Trimble Inc. (NASDAQ:TRMB) released its third-quarter 2025 results on November 5, showcasing strong organic growth across all business segments. The company reported revenue of $901 million, representing an 11% organic increase year-over-year, while non-GAAP earnings per share reached $0.81, exceeding the high end of previous guidance. Following the announcement, Trimble's stock initially rose 3.44% in premarket trading, though it later retreated to $75.60, down 3.82% from the previous close of $78.60.

The company continues to execute on its "Connect & Scale" strategy, focusing on three key themes for fiscal year 2025: portfolio clarity, business model durability, and operational momentum. These strategic priorities have helped Trimble navigate a complex market environment while expanding margins and growing its recurring revenue base.

Quarterly Performance Highlights

Trimble's third quarter results exceeded expectations across key metrics. Revenue reached $901 million with 11% organic growth, while annual recurring revenue (ARR) grew to $2.31 billion, representing 15% organic growth year-over-year. The company also demonstrated significant margin improvement, with non-GAAP gross margin expanding 90 basis points to 71.2% and adjusted EBITDA margin increasing 160 basis points to 29.9%.

As shown in the following quarterly summary:

The strong performance was driven primarily by robust software and recurring revenue growth, improved revenue mix, and enhanced operating leverage. Recurring revenue now represents 37% of total revenue, highlighting the company's ongoing transition toward a more predictable business model.

Trimble's revenue mix shows a balanced geographic distribution, with North America representing the largest market at 59%, followed by Europe (27%), Asia-Pacific (10%), and other regions (4%). From a product perspective, software, services, and recurring revenue constitute 22% of total revenue, with hardware accounting for the remaining 78%.

Segment Analysis

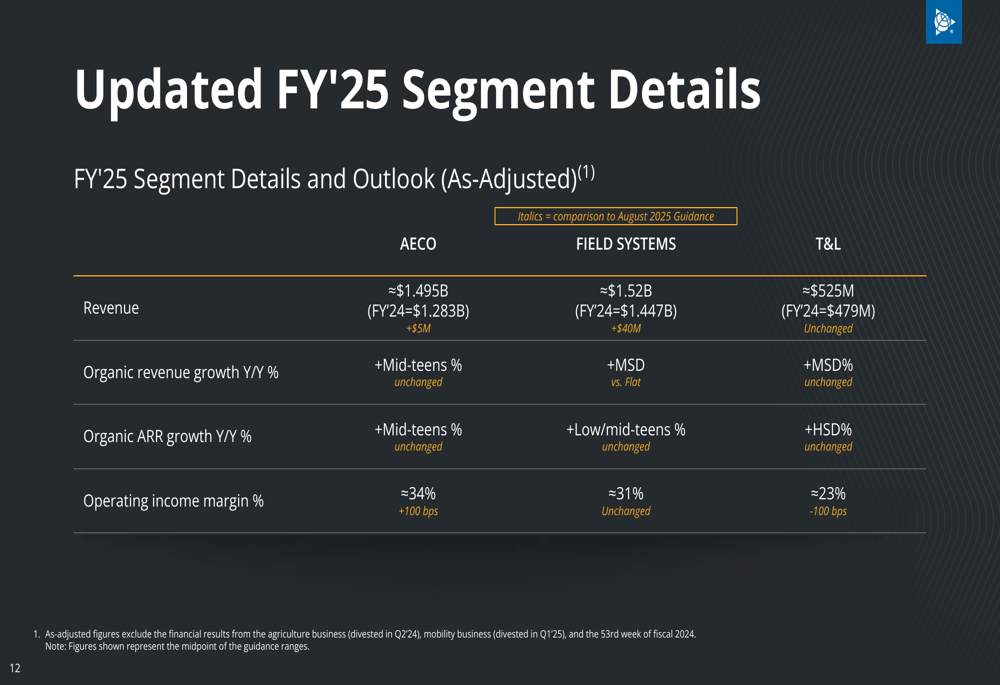

Trimble's business is organized into three main segments, each showing positive organic growth in the third quarter. The AECO (Architects, Engineers, Construction, Owners) segment was the standout performer, with 17% organic revenue growth and a 270 basis point improvement in operating margin.

The AECO segment has scaled to over $1.4 billion in ARR and is operating above the "Rule of 40" (with a combined growth rate and profit margin exceeding 45% in Q3). This performance was driven by increased bookings in Trimble Construction One and cross-sell offerings, resulting in significant margin expansion through revenue growth and gross margin improvement.

The Field Systems segment also delivered solid results, with 8% organic revenue growth and 18% ARR growth. Software, services, and recurring revenue now represent more than 50% of this segment's revenue, highlighting the ongoing business model transformation.

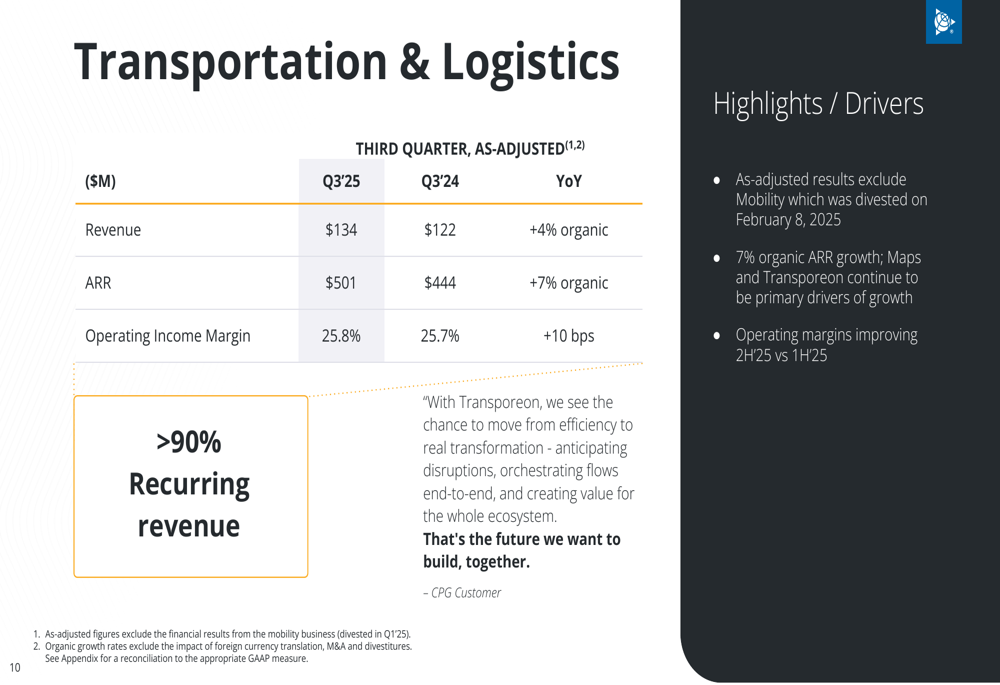

The Transportation & Logistics segment, while growing more modestly at 4% organic revenue growth, maintained strong recurring revenue at over 90% of segment revenue. This segment's performance excludes the Mobility business, which was divested.

Updated Outlook

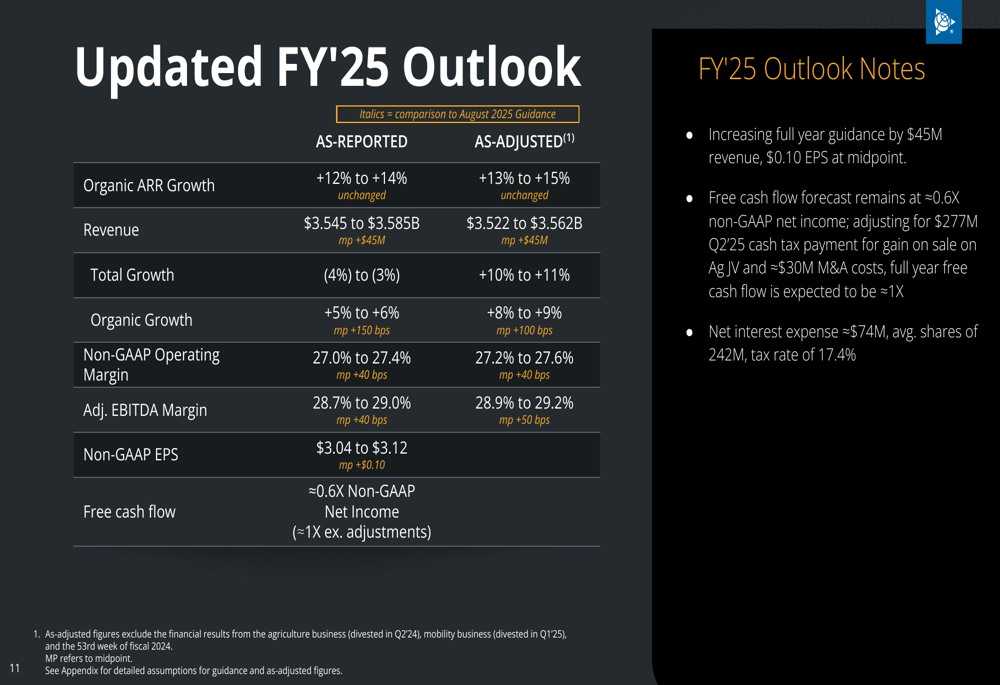

Based on the strong third-quarter performance, Trimble has raised its full-year 2025 guidance. The company now expects revenue between $3.522 billion and $3.562 billion, representing 10-11% total growth and 8-9% organic growth. Organic ARR growth is projected at 13-15%, with non-GAAP EPS between $3.04 and $3.12.

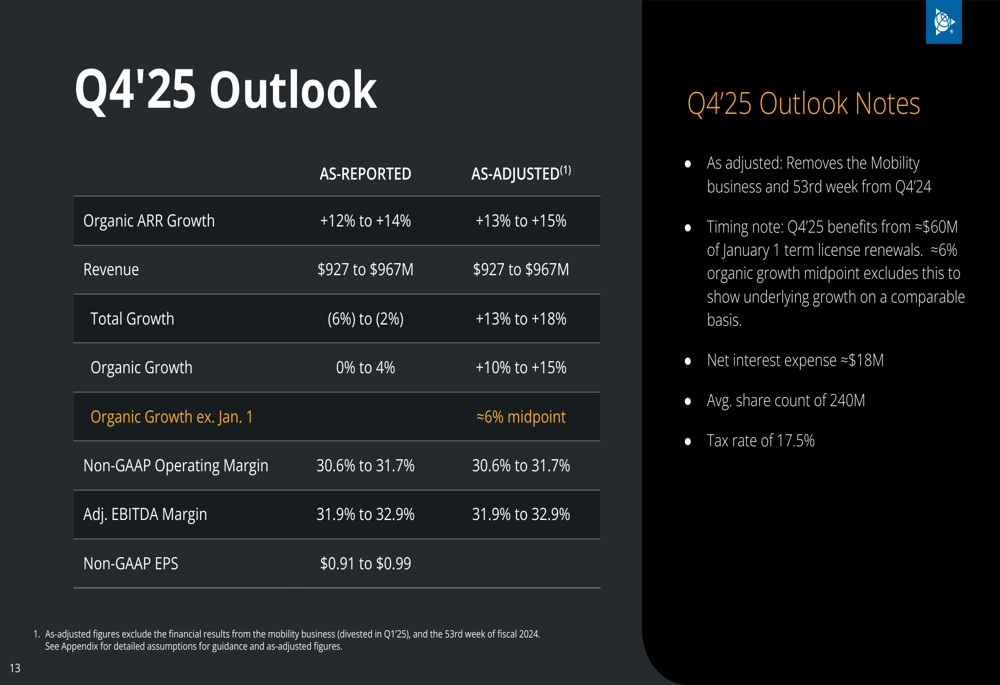

For the fourth quarter of 2025, Trimble projects revenue between $927 million and $967 million, with organic growth of 10-15% and non-GAAP EPS between $0.91 and $0.99.

The updated segment outlook shows continued strength in AECO, with mid-teens organic revenue and ARR growth expected for the full year. The Field Systems segment has seen an improved outlook, with mid-single-digit organic revenue growth now expected versus the previous flat guidance. Transportation & Logistics is projected to maintain mid-single-digit organic revenue growth and high-single-digit ARR growth.

Balance Sheet and Cash Flow Considerations

While Trimble's operational performance remains strong, year-to-date cash flow has declined compared to 2024. Operating cash flow reached $226 million (versus $416 million in 2024), with free cash flow at $206 million (compared to $389 million). The company noted that these figures include a $277 million cash tax payment related to the gain on sale from the Agriculture divestiture.

Trimble maintains a solid balance sheet with $233 million in cash and equivalents, total debt of $1.392 billion, and net debt of $1.159 billion. The company's net debt to trailing twelve-month adjusted EBITDA ratio stands at 1.2x, indicating a manageable leverage position.

In its forward guidance, Trimble indicated a shift in its full-year cash flow expectations, now projecting free cash flow at 0.6x non-GAAP net income. Despite this adjustment, the company's overall financial position remains strong, with improving margins and robust organic growth providing a foundation for continued investment in strategic initiatives.

The third-quarter results and raised guidance reflect Trimble's successful execution of its business strategy, with particular strength in the AECO segment and continued progress in transforming its business model toward higher-margin, recurring revenue streams. While challenges remain in certain areas, particularly cash flow, the company's overall trajectory appears positive as it moves toward the close of fiscal year 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.