ION expands ETF trading capabilities with Tradeweb integration

Trinity Industries, Inc. (NYSE:TRN) released its Q2 2025 investor presentation on July 31, 2025, highlighting financial results for the quarter ending June 30. The railcar manufacturer and leasing company reported improved profitability despite revenue challenges, maintaining its full-year guidance on the strength of its leasing business and expectations for improved performance in the second half of the year.

Quarterly Performance Highlights

Trinity reported quarterly earnings per share (EPS) from continuing operations of $0.19, a significant improvement from the $(0.48) loss reported in the same quarter last year. However, revenues declined 40% year-over-year to $506 million, primarily due to lower railcar deliveries in the manufacturing segment.

Cash flow from continuing operations showed substantial improvement at $64 million compared to $(180) million in the prior-year period. The company's last twelve months adjusted return on equity stood at 10.6%.

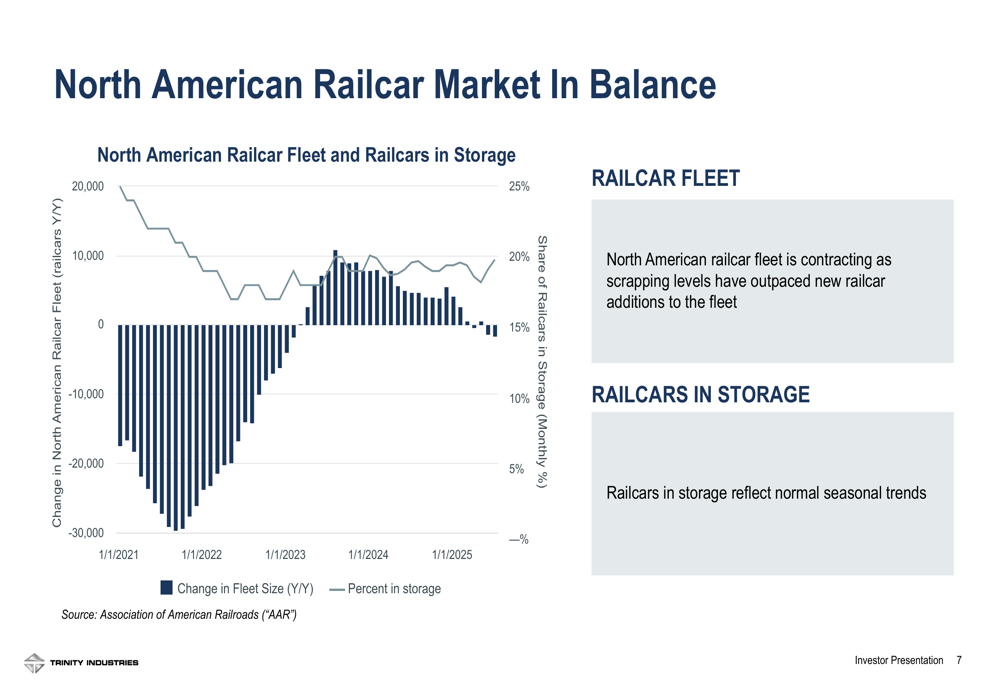

As shown in the following financial results highlights:

The railcar market appears to be stabilizing, with Trinity noting that the North American railcar fleet is contracting as scrapping levels have outpaced new railcar additions. Railcars in storage reflect normal seasonal trends, suggesting a balanced market environment.

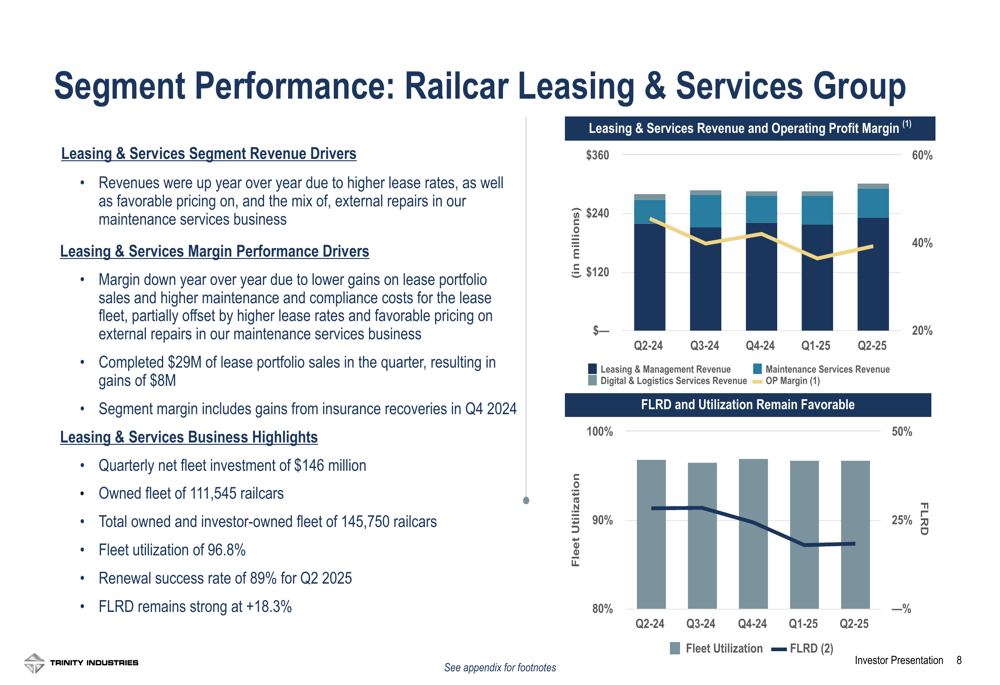

Segment Analysis: Leasing & Rail Products

Trinity's Railcar Leasing & Services Group demonstrated strong performance with fleet utilization of 96.8% and a Future Lease Rate Differential (FLRD) of +18.3%, indicating continued strength in lease rates. The company completed $29 million of lease portfolio sales in the quarter, resulting in gains of $8 million. The owned fleet consists of 111,545 railcars, with an additional 34,205 investor-owned railcars under management.

The following chart illustrates the positive trends in the leasing business:

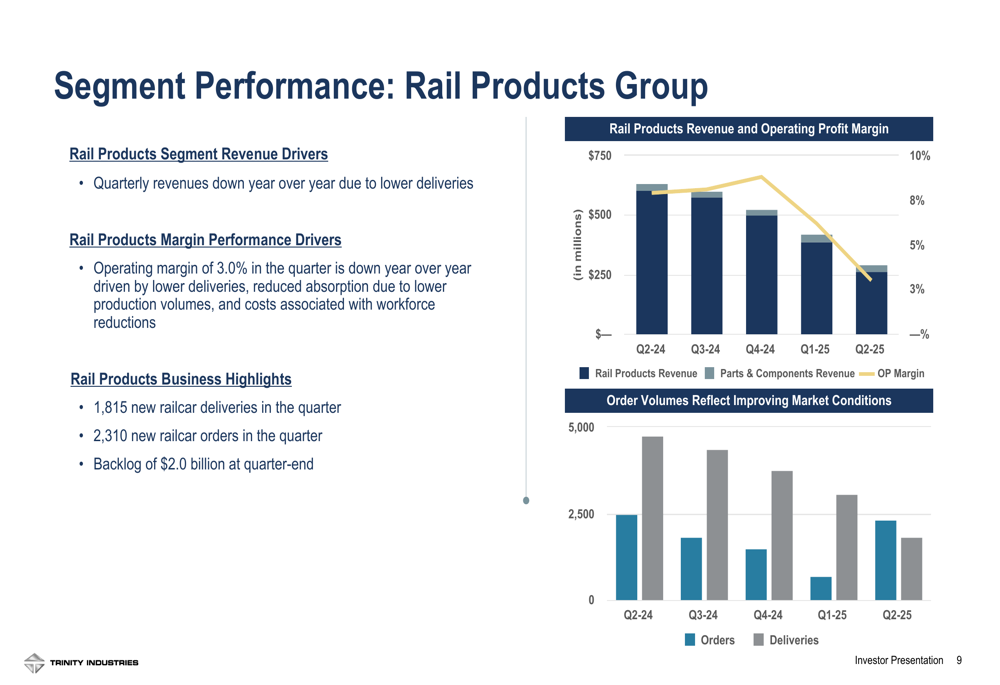

In contrast, the Rail Products Group faced challenges with operating margin declining to 3.0%, driven by lower deliveries, reduced absorption due to lower production volumes, and costs associated with workforce reductions. Despite these challenges, Trinity delivered 1,815 new railcars in the quarter and secured orders for 2,310 units, resulting in a book-to-bill ratio of 1.3x – the first time this metric has exceeded 1.0 in ten quarters.

The order and delivery trends are illustrated in this chart:

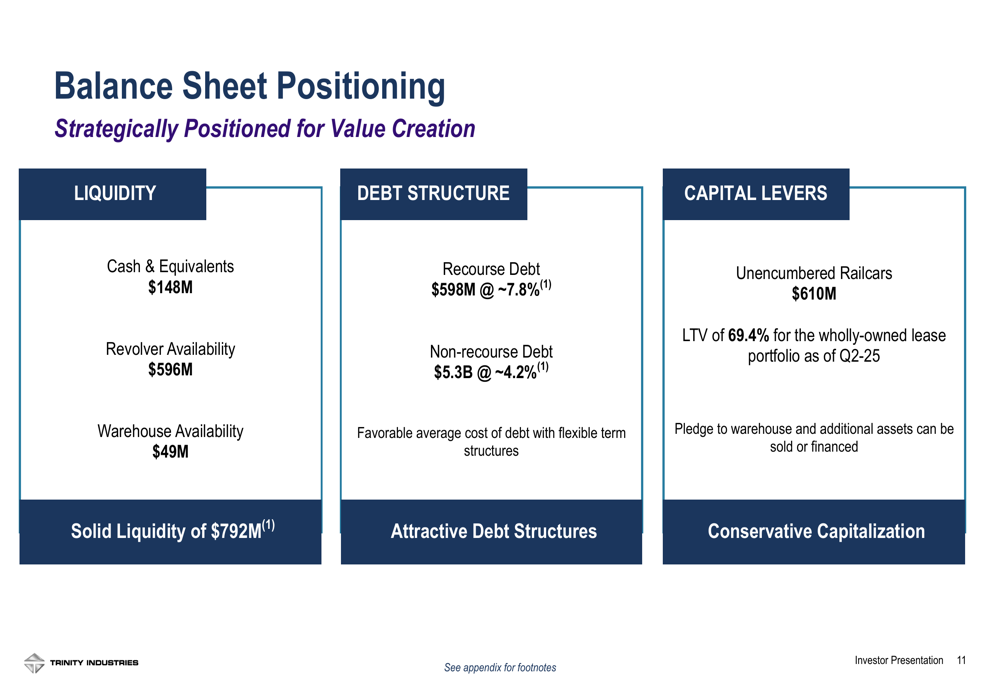

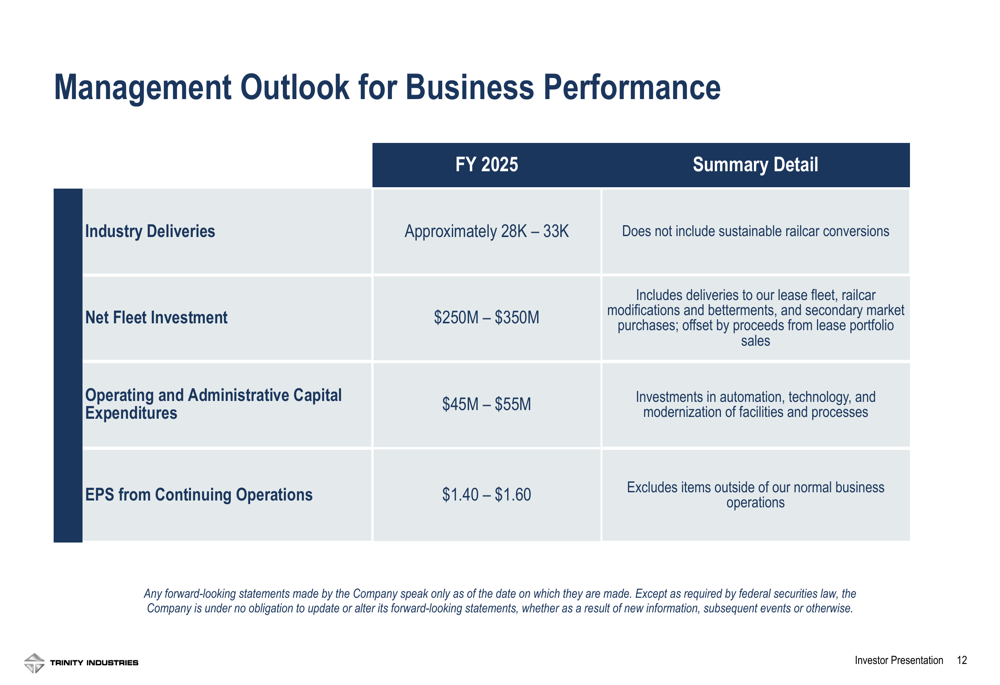

Financial Position and Outlook

Trinity maintains a solid financial position with $792 million in liquidity, including $148 million in cash and equivalents, $596 million in revolver availability, and $49 million in warehouse availability. The company's debt structure consists of $598 million in recourse debt at approximately 7.8% interest and $5.3 billion in non-recourse debt at approximately 4.2%.

The balance sheet positioning is detailed in the following slide:

Management has maintained its 2025 EPS guidance in the range of $1.40 to $1.60, indicating confidence in improved performance in the second half of the year. The company expects industry-wide railcar deliveries of approximately 28,000-33,000 units, excluding sustainable railcar conversions. Trinity projects net fleet investment of $250-$350 million and operating and administrative capital expenditures of $45-$55 million.

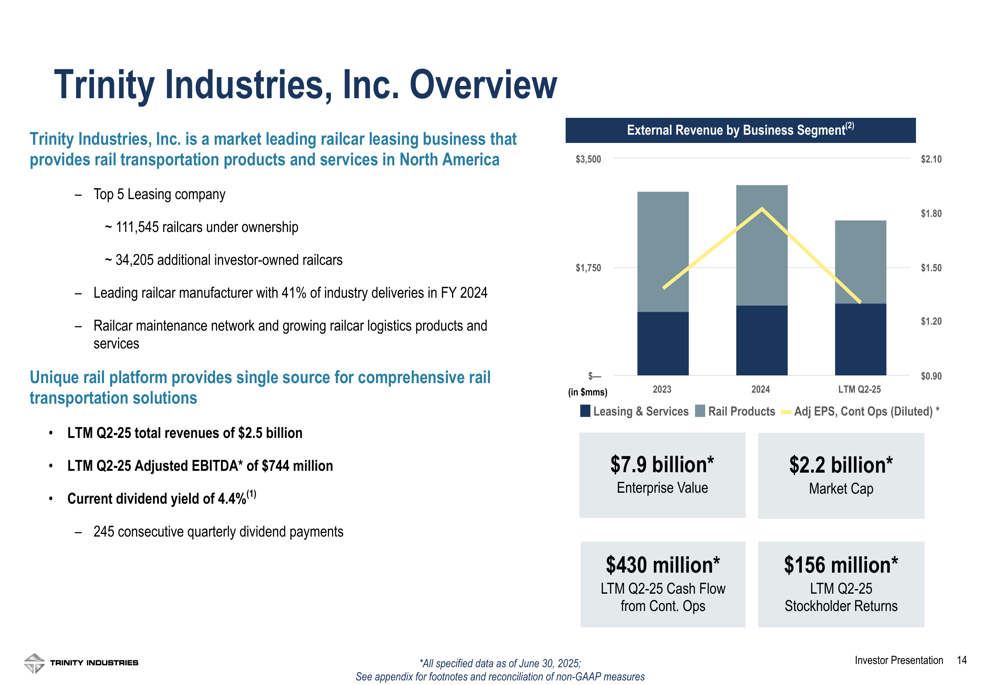

Strategic Initiatives and Company Overview

Trinity positions itself as a comprehensive rail transportation solutions provider, ranking among the top 5 leasing companies in the industry. The company delivered 41% of industry railcars in FY 2024, demonstrating its significant market position. With an enterprise value of $7.9 billion and market capitalization of $2.2 billion, Trinity continues to deliver shareholder returns, maintaining a 4.4% dividend yield and 245 consecutive quarterly dividend payments.

The company overview highlights Trinity's scale and market position:

Trinity's CEO Gene Savage expressed optimism during the earnings call, stating, "We believe the second quarter was the bottom of that cycle," while CFO Eric Marketo emphasized the company's resilience "against a backdrop of low industrial growth and macroeconomic uncertainty."

While Trinity faces challenges including industry railcar fleet contraction, macroeconomic pressures, and the impact of workforce reductions, the company's diversified business model with both manufacturing and leasing segments provides some insulation against market volatility. The improving book-to-bill ratio suggests potential recovery in the manufacturing segment, which could complement the already strong performance in leasing.

Trinity's stock closed at $27.59 on the most recent trading day, reflecting a 1.88% increase. Year-to-date, the stock has declined 17.4%, though it maintains strong dividend credentials with 55 consecutive years of dividend payments and 15 years of consecutive increases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.