Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

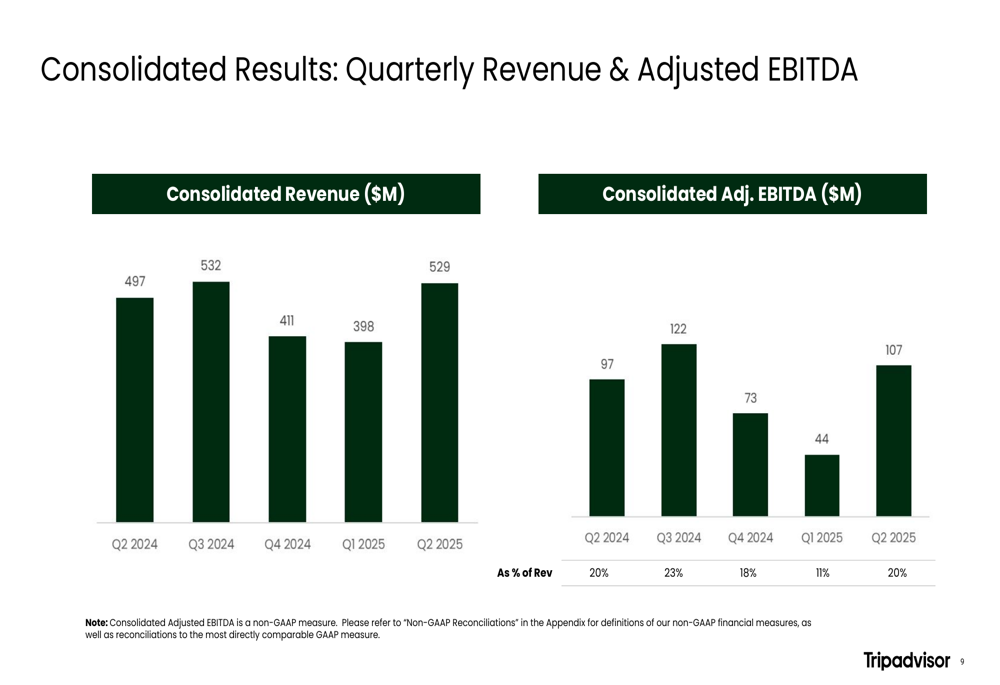

TripAdvisor Inc. (NASDAQ:TRIP) presented its second quarter fiscal year 2025 results on August 7, 2025, showing overall revenue growth of 6.4% year-over-year to $529 million, driven primarily by strong performance in its Viator experiences platform and TheFork restaurant booking service. The company’s shares closed at $16.09, down 2.37% on the day of the presentation.

The company’s consolidated adjusted EBITDA reached $107 million in Q2, representing 20% of revenue and a 10.3% increase from the $97 million reported in the same quarter last year. This performance comes as the global travel market continues its post-pandemic recovery, with the online experiences segment showing particularly strong growth.

Quarterly Performance Highlights

TripAdvisor’s consolidated quarterly revenue showed steady improvement throughout the past five quarters, with Q2 2025 reaching $529 million, up from $497 million in Q2 2024. The adjusted EBITDA margin remained stable at 20% of revenue year-over-year.

As shown in the following chart of quarterly consolidated results:

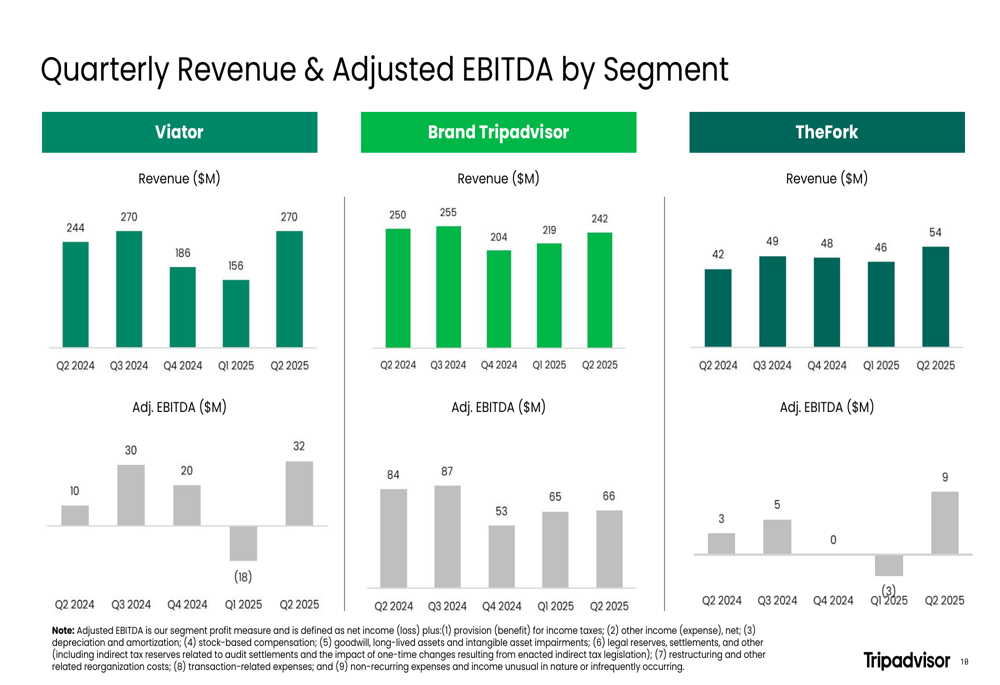

Breaking down performance by segment reveals divergent trends across the company’s three main brands. Viator, the experiences booking platform, continued its strong growth trajectory with revenue reaching $270 million in Q2 2025, an 11% increase from $244 million in Q2 2024. The segment’s adjusted EBITDA more than tripled to $32 million from $10 million a year earlier.

Meanwhile, the core TripAdvisor brand saw revenue decline to $242 million, down 5.1% from $255 million in Q2 2024. TheFork, the company’s restaurant booking platform, delivered the strongest growth rate with revenue increasing 28.6% to $54 million from $42 million in the prior year period.

The segment breakdown is illustrated in this quarterly performance chart:

Segment Analysis

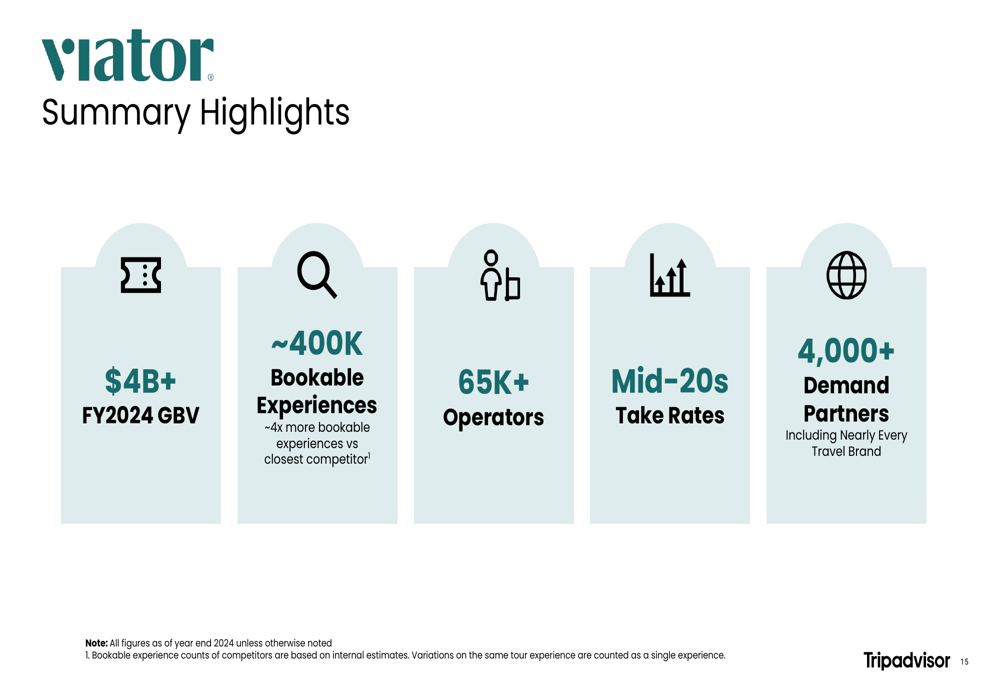

Viator continues to strengthen its position as the leading global online experiences platform, with management highlighting its scale advantages and improving profitability metrics. The platform now offers approximately 400,000 bookable experiences, which the company claims is about four times more than its closest competitor. Viator works with over 65,000 operators and maintains mid-20s take rates while distributing through more than 4,000 demand partners.

The following image summarizes Viator’s key metrics:

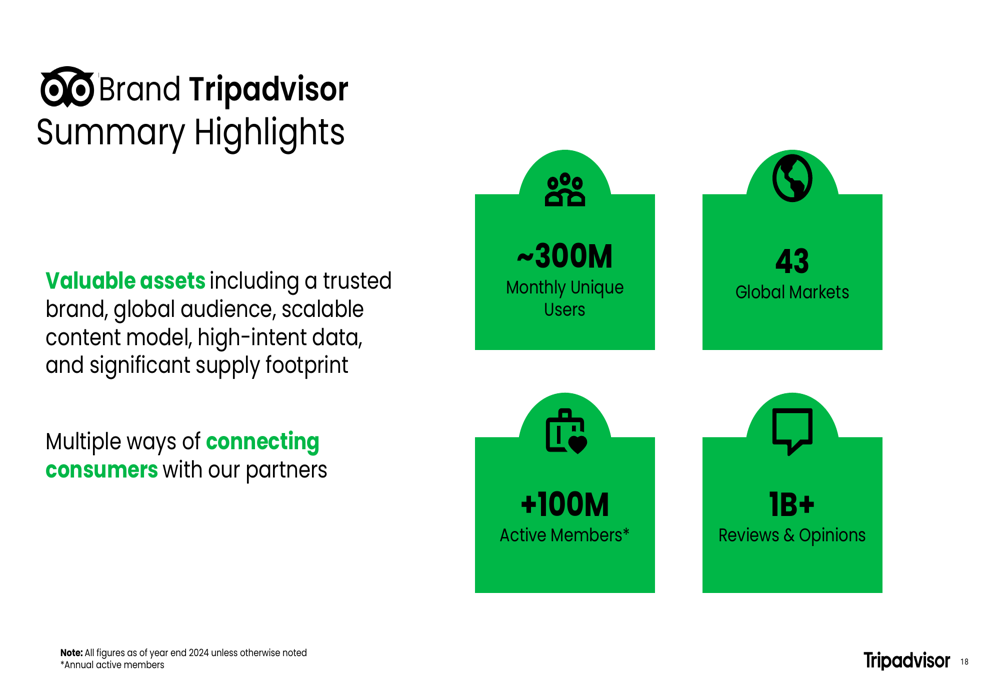

The core TripAdvisor brand, while experiencing revenue decline, maintains its position as a trusted travel guidance platform with approximately 300 million monthly unique users across 43 global markets. The company is shifting from its legacy model to an engagement-led strategy focused on deepening user relationships through improved planning tools and content.

TripAdvisor’s key metrics are highlighted in this summary:

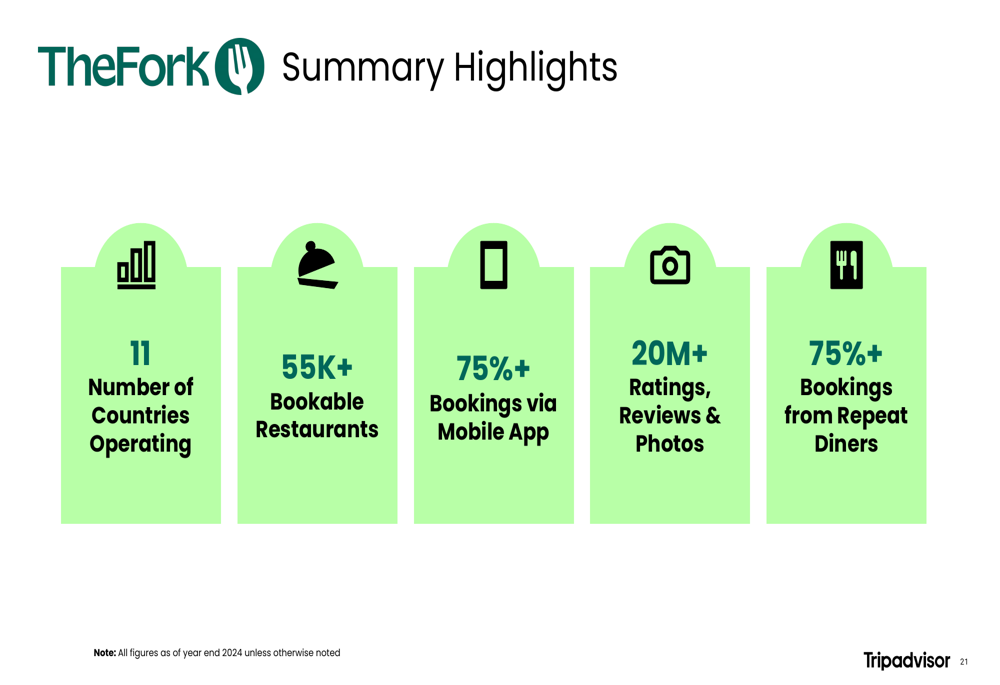

TheFork showed the strongest growth among all segments, with management attributing this to successful reinvestment of cost savings into growth initiatives. Operating in 11 European countries, TheFork now features over 55,000 bookable restaurants and generates 75% of its bookings through its mobile app. The platform benefits from high customer loyalty, with over 75% of bookings coming from repeat diners.

The following image details TheFork’s performance metrics:

Strategic Initiatives

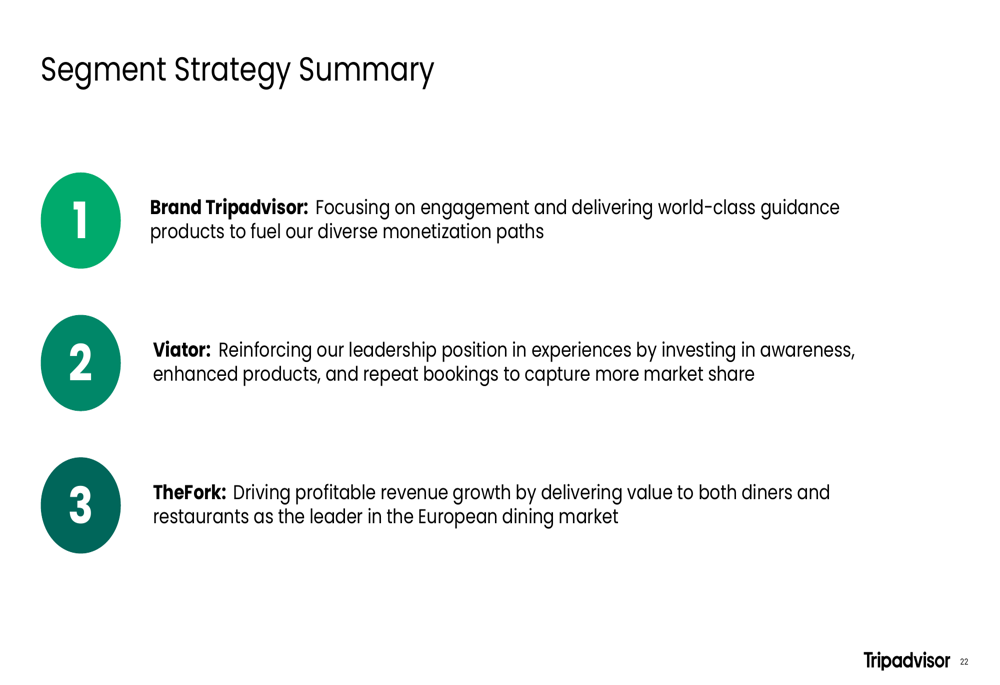

TripAdvisor’s presentation emphasized its strategic positioning across the entire traveler journey through its three complementary brands. The company highlighted how each segment addresses different aspects of travel planning and booking, creating a comprehensive ecosystem.

For Viator, the strategy focuses on balancing scale, growth, profitability, and market share. Management noted that the global tours and experiences market is expected to grow from $253 billion in 2019 to $314 billion in 2026, with online penetration increasing from 16% to 31% during this period. This represents a significant growth opportunity as more bookings shift from offline to online channels.

The core TripAdvisor brand is undergoing a strategic shift toward an engagement-led approach, focusing on delivering world-class guidance products to fuel diverse monetization paths. This represents a departure from its traditional advertising-heavy model as the company works to better leverage its massive user base and content library.

TheFork’s strategy centers on driving profitable revenue growth in the European dining market by delivering value to both diners and restaurants. The segment is focused on growing its restaurant base, reaching more travelers, and improving profitability through value-added products and services.

The company’s segment strategy is summarized in this overview:

Financial Position

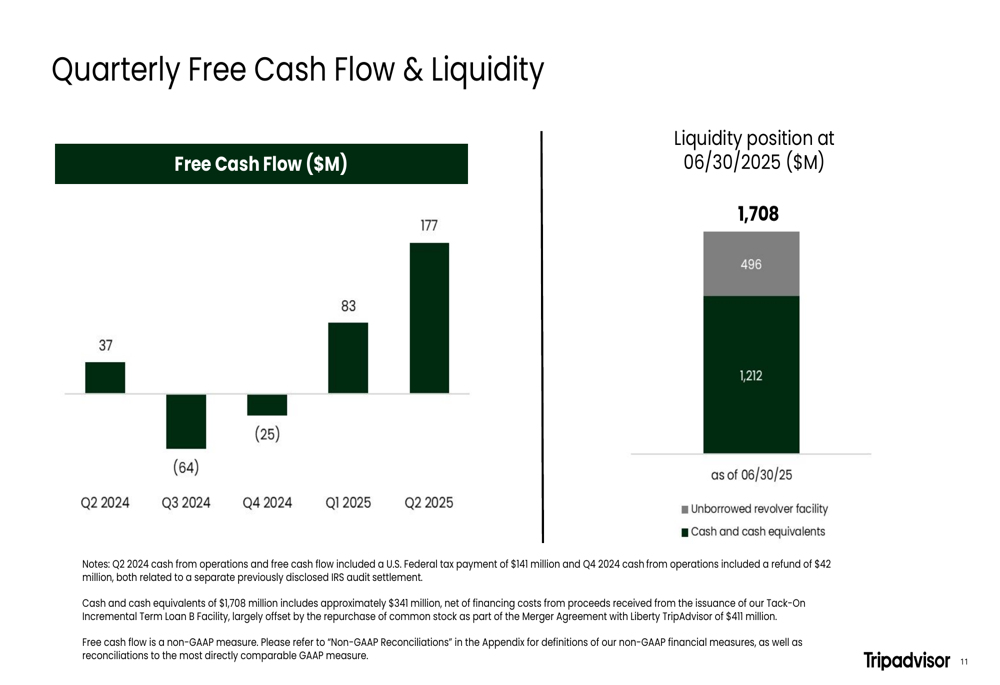

TripAdvisor reported substantial improvement in its free cash flow, which reached $177 million in Q2 2025, a dramatic increase from $37 million in Q2 2024. The company noted that the prior year’s Q2 cash flow was impacted by a $141 million U.S. Federal tax payment related to an IRS audit settlement.

As of June 30, 2025, TripAdvisor maintained a strong liquidity position of $1.71 billion, consisting of $1.21 billion in cash and cash equivalents and $496 million in unborrowed revolver facility.

The following chart illustrates the company’s quarterly free cash flow and liquidity position:

Forward-Looking Statements

While the presentation did not provide specific forward guidance, management emphasized their focus on balancing growth and profitability across all three segments. For Viator, the company highlighted investments in building market share today to establish a long-term profitable business, noting that increasing rates of repeat bookers and higher subsequent order values should drive improving profitability over time.

The TripAdvisor core brand is expected to continue its transition to an engagement-led strategy, which may impact near-term revenue but is designed to create more sustainable growth opportunities. For TheFork, management expects to maintain strong growth while improving profitability through operational efficiencies and strategic focus on core European markets.

Overall, TripAdvisor’s Q2 2025 presentation painted a picture of a company with divergent segment performance but solid overall financial results, strong cash generation, and clear strategic direction for each of its three main brands.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.