Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

TriplePoint Venture Growth BDC Corp (NYSE:TPVG) presented its second quarter 2025 results on August 6, revealing a mixed performance with missed earnings expectations but robust origination activity. The business development company, which focuses on providing debt financing to venture growth stage companies, reported net investment income (NII) of $0.28 per share, falling short of the $0.2962 forecast. The company’s stock price remained unchanged at $6.90 following the earnings release, trading at a significant discount to its net asset value of $8.65 per share.

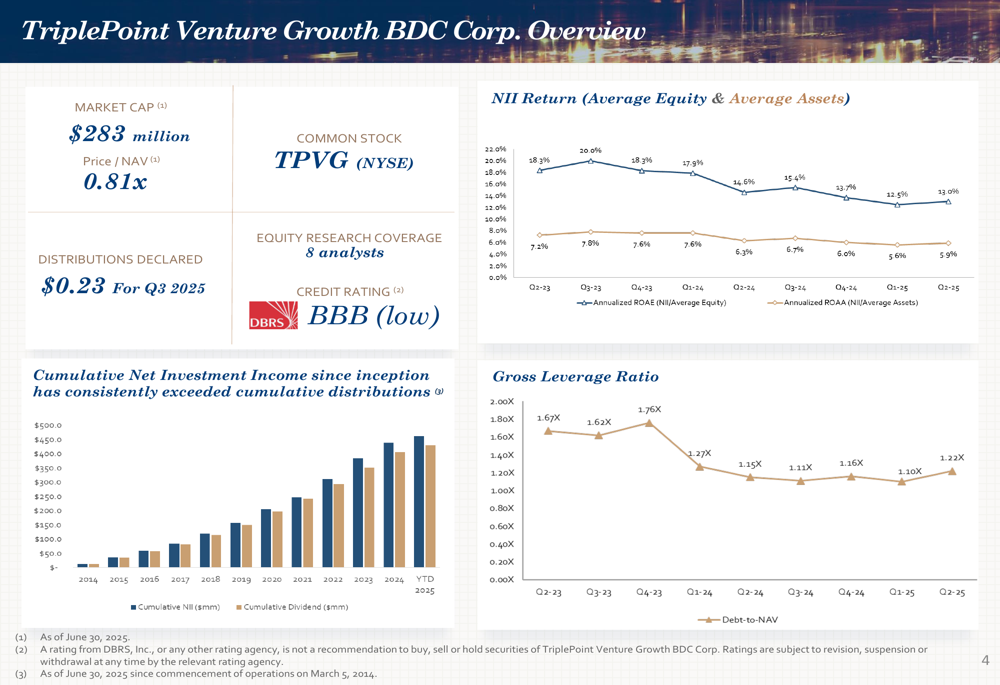

As shown in the following overview of key metrics, TPVG maintained a market capitalization of $283 million with a price-to-NAV ratio of 0.81x, reflecting the ongoing discount at which the stock trades relative to its underlying assets:

Quarterly Performance Highlights

For the second quarter of 2025, TriplePoint Venture Growth reported net investment income of $11.3 million ($0.28 per share) and a net increase in net assets of $13.2 million ($0.33 per share). The company’s net asset value stood at $348.7 million ($8.65 per share) as of June 30, 2025. Notably, the company reduced its quarterly distribution from $0.30 to $0.23 per share for the third quarter of 2025, representing a 13.1% annualized yield based on current share price.

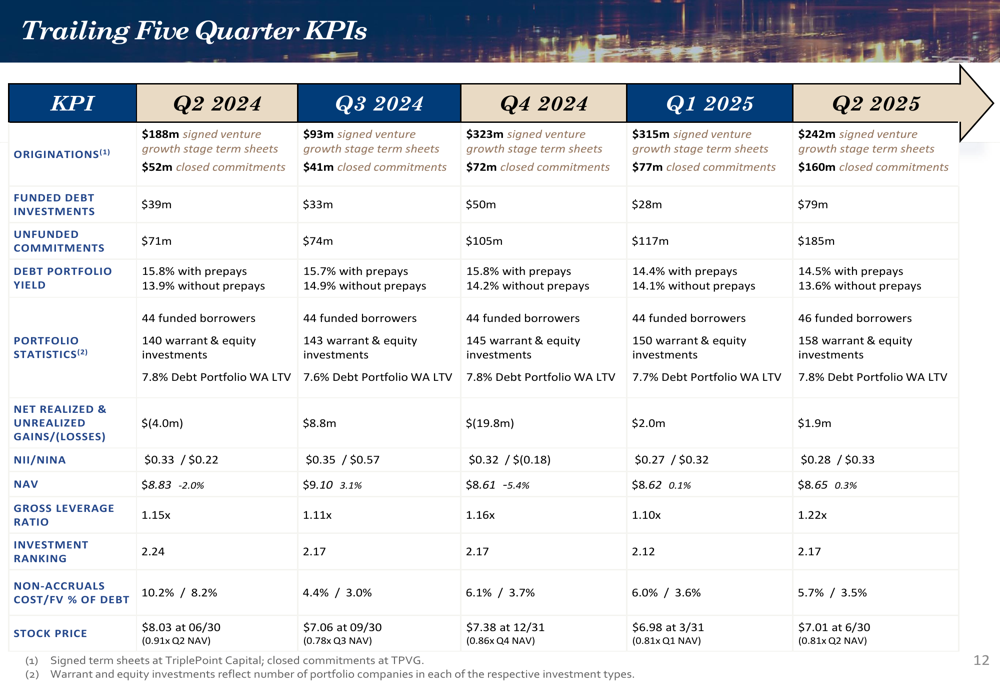

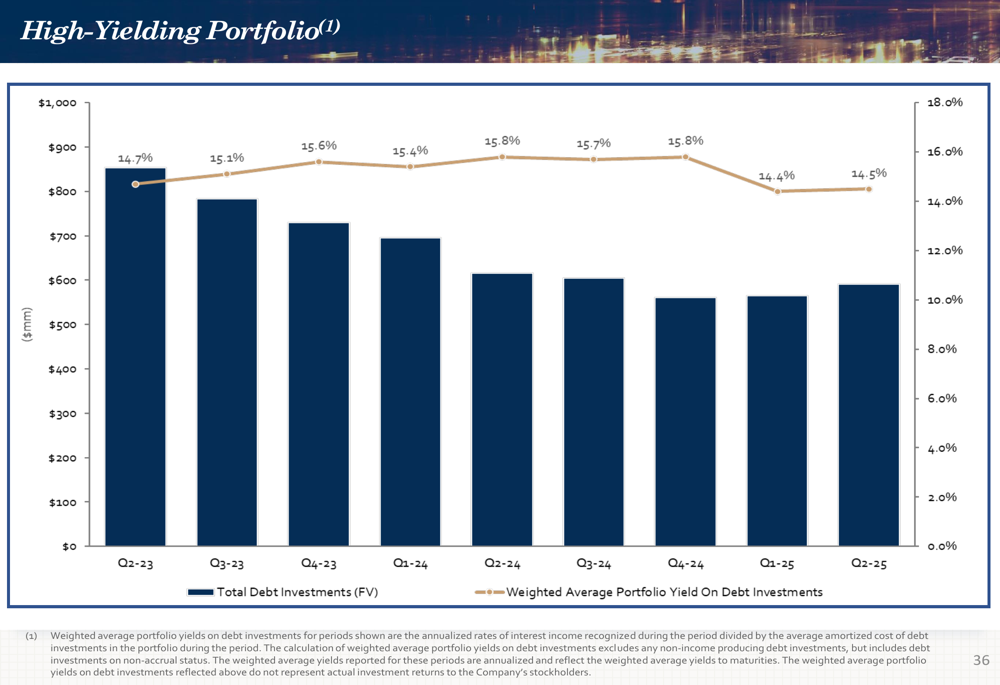

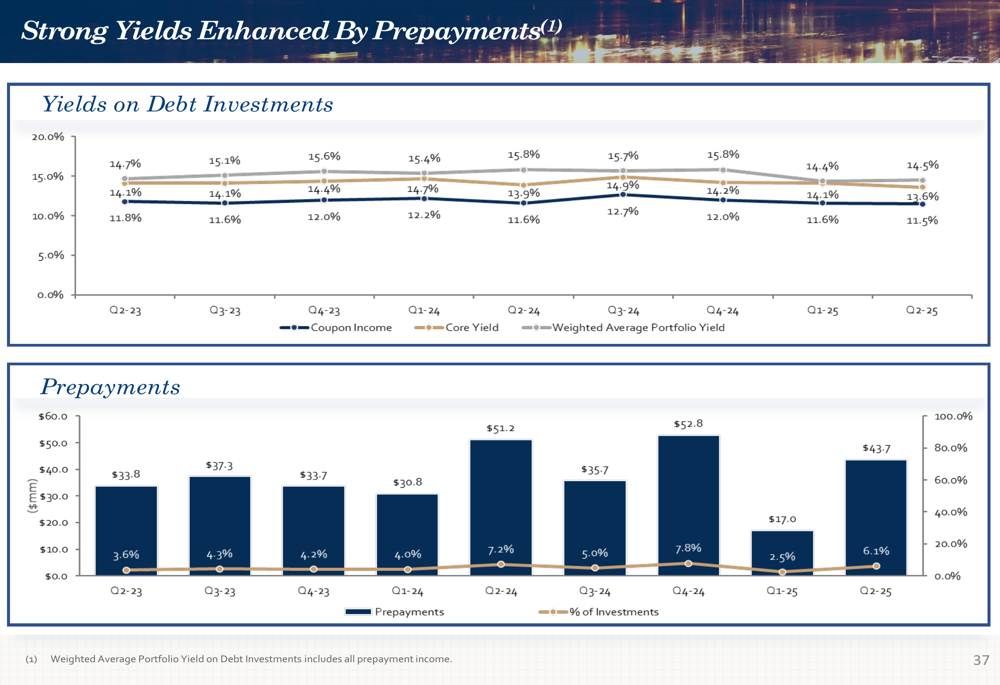

The company’s performance over the past five quarters shows consistent but slightly declining portfolio yields, with Q2 2025 weighted average portfolio yield at 14.5%, down from 15.8% year-over-year according to the earnings call transcript. The following chart illustrates key performance indicators across recent quarters:

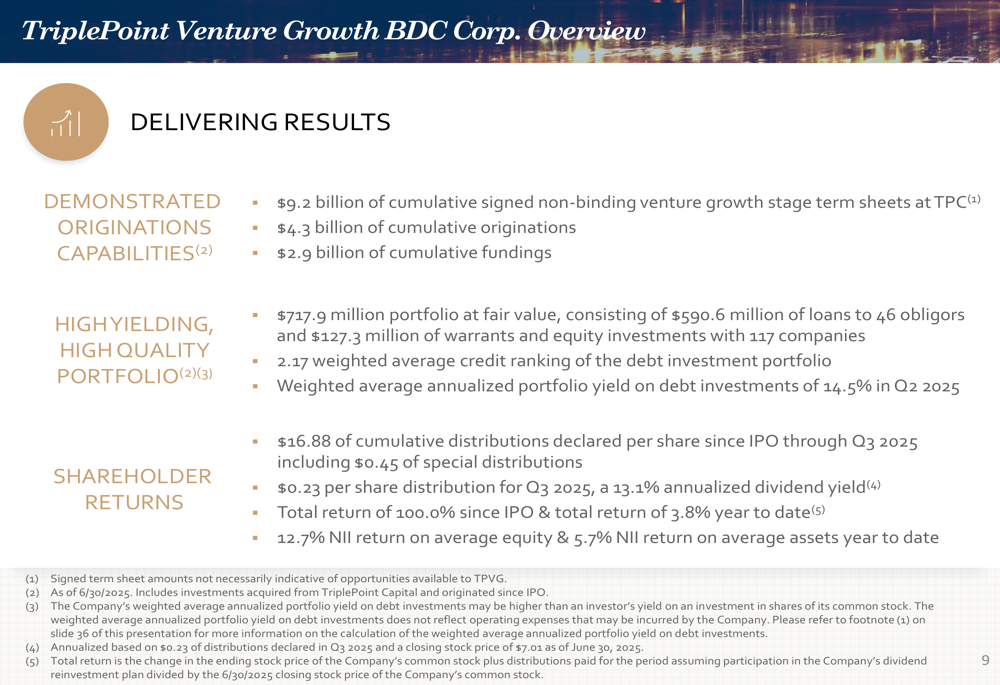

Despite the earnings miss, TriplePoint Venture Growth has demonstrated strong origination capabilities, with $9.2 billion of cumulative signed non-binding venture growth stage term sheets, $4.3 billion of cumulative originations, and $2.9 billion of cumulative fundings. The company’s shareholder returns include $16.88 of cumulative distributions declared per share since IPO through Q3 2025.

The following slide highlights these key results and metrics:

Portfolio and Investment Activity

TriplePoint Venture Growth maintains a high-yielding, high-quality portfolio totaling $717.9 million at fair value as of June 30, 2025. This portfolio consists of loans to 46 obligors and warrants/equity investments in 117 companies. The company’s investment strategy focuses on venture capital-backed companies in technology and other high-growth industries.

As illustrated in the following portfolio breakdown, the debt portfolio accounts for $590.6 million with a weighted average yield of 14.5%, while warrant and direct equity investments contribute $43.9 million and $83.4 million in fair value, respectively:

The company’s warrant and direct equity investments provide potential upside beyond the core lending business. These investments span 106 companies (warrants) and 52 companies (direct equity) with a combined fair value of $89.9 million. The following slide details these investments and their potential for book value appreciation:

During the second quarter, TriplePoint Venture Growth signed term sheets of $241.5 million, closed $160.1 million in debt commitments and $1.1 million in equity commitments, and funded $78.5 million in debt investments. Five portfolio companies raised a total of $216.0 million in equity financing rounds during the quarter, demonstrating continued investor interest in TPVG’s portfolio companies.

The following chart shows the company’s portfolio yield over time, highlighting the relatively stable performance despite market fluctuations:

Strategic Initiatives and Outlook

TriplePoint Venture Growth continues to focus on its core strategy of providing customized debt financing to venture growth stage companies. The company targets returns of 10-18% from interest and fees, with additional upside through equity kickers in the form of warrants. This approach allows portfolio companies to finance growth while minimizing equity dilution.

According to the earnings call, the company is particularly focused on opportunities in the artificial intelligence sector, with CEO Jim Labe emphasizing that "AI is providing a renaissance and macro tailwind to the broader technology sector with the potential to surpass the impact of the internet, cloud computing or the mobile revolution."

Looking ahead, TriplePoint Venture Growth targets Q3 funding between $25 million and $50 million, with potential for exceeding this range in Q4. The company anticipates portfolio growth to become more evident in 2026 and plans to refinance $200 million of fixed-rate notes in Q1 2026.

Financial Position and Dividend

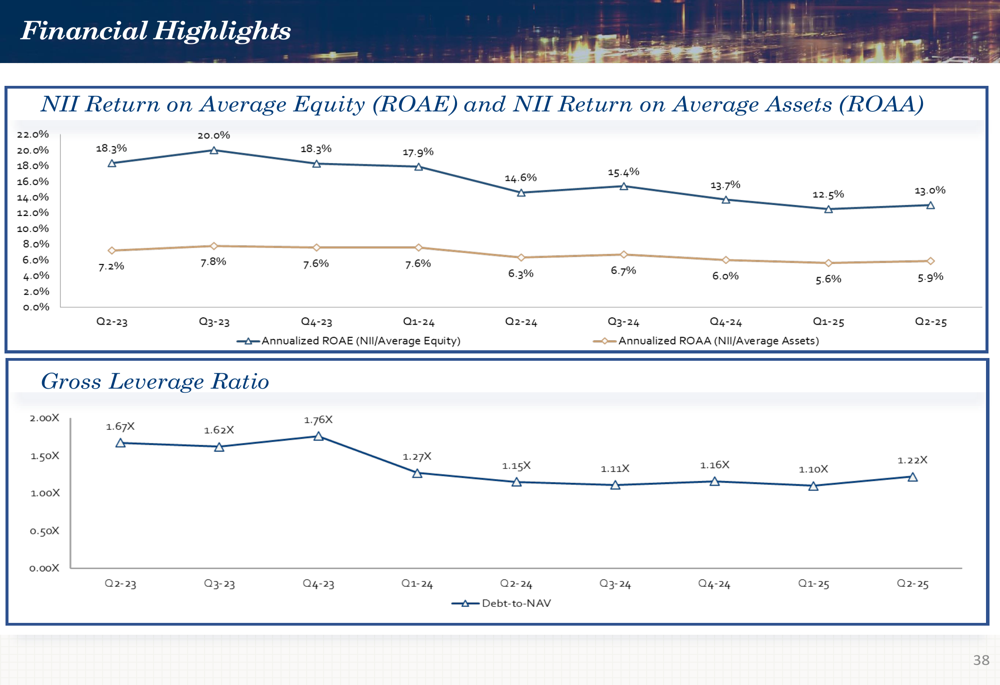

TriplePoint Venture Growth ended the second quarter with a gross leverage ratio of 1.22x and a net leverage ratio of 1.04x. The company maintained strong liquidity of $312.5 million, including $62.5 million in cash equivalents, against $184.7 million of unfunded commitments.

The following chart illustrates the company’s NII return on average equity (ROAE), NII return on average assets (ROAA), and gross leverage ratio over recent quarters:

In a notable development, the company’s adviser waived the quarterly income incentive fee for the remainder of 2025, reflecting alignment with shareholder interests during a challenging period. Additionally, TriplePoint Capital announced a share purchase program of up to $14 million, signaling confidence in the company’s valuation.

The reduction in quarterly distribution from $0.30 to $0.23 per share represents a significant change for income-focused investors. However, the company maintains estimated spillover income of $42.0 million ($1.04 per share), providing some cushion for future distributions.

As shown in the following chart, the company’s strong yields have been enhanced by prepayments, though these have fluctuated over recent quarters:

While TriplePoint Venture Growth faces challenges including missed earnings expectations and a reduced dividend, its strong origination pipeline, high-yielding portfolio, and solid liquidity position provide a foundation for potential recovery. Investors will be watching closely to see if the company can translate its robust origination activity into improved financial performance in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.