Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

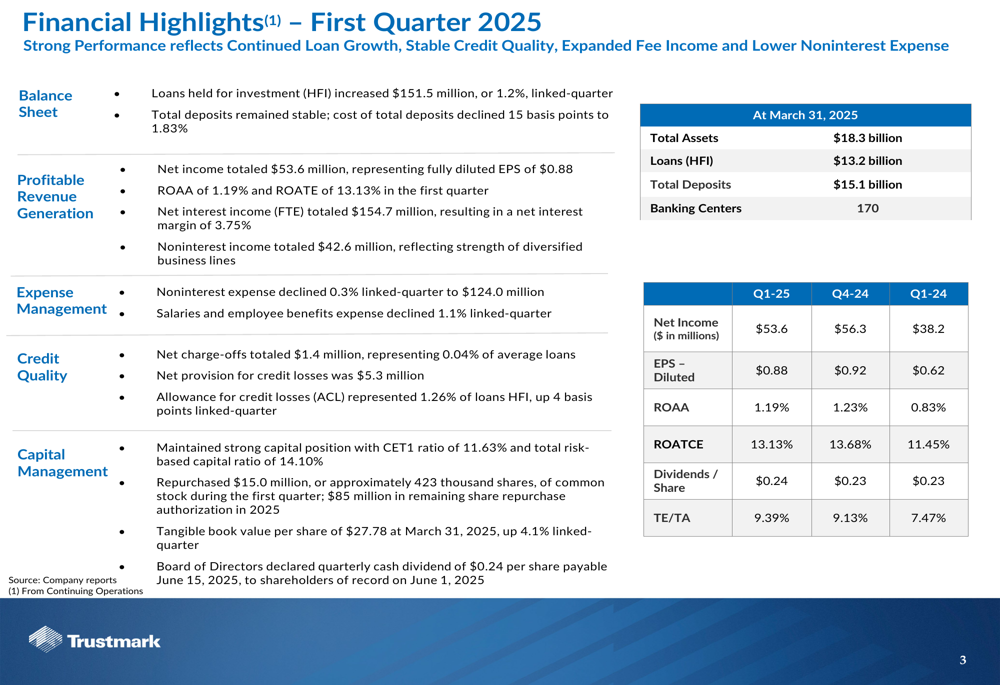

Trustmark Corporation (NASDAQ:TRMK) released its first quarter 2025 financial results on April 22, 2025, showing solid performance with strong year-over-year improvement despite a slight sequential decline. The bank reported earnings per share of $0.88, down from $0.92 in the previous quarter but significantly higher than the $0.62 reported in the same quarter last year. Following the earnings release, Trustmark’s stock closed at $33.80, up 3.33% from the previous close of $32.69.

The company’s performance reflects continued loan growth, stable credit quality, expanded fee income, and lower noninterest expense, positioning Trustmark to continue its capital return program through share repurchases and an increased dividend.

Quarterly Performance Highlights

Trustmark reported net income of $53.6 million for the first quarter of 2025, compared to $56.3 million in the fourth quarter of 2024 and $38.2 million in the first quarter of 2024. This represents a return on average assets (ROAA) of 1.19% and a return on average tangible common equity (ROATCE) of 13.13%.

As shown in the following financial highlights chart, the company demonstrated strong profitability metrics despite the slight sequential decline:

Net interest income on a fully taxable equivalent (FTE) basis totaled $154.7 million, resulting in a net interest margin of 3.75%, down just 1 basis point from the previous quarter. Noninterest income increased to $42.6 million, up $1.6 million from the linked quarter and $3.2 million year-over-year, while noninterest expense declined 0.3% linked-quarter to $124.0 million, demonstrating the company’s focus on expense management.

Loan and Deposit Analysis

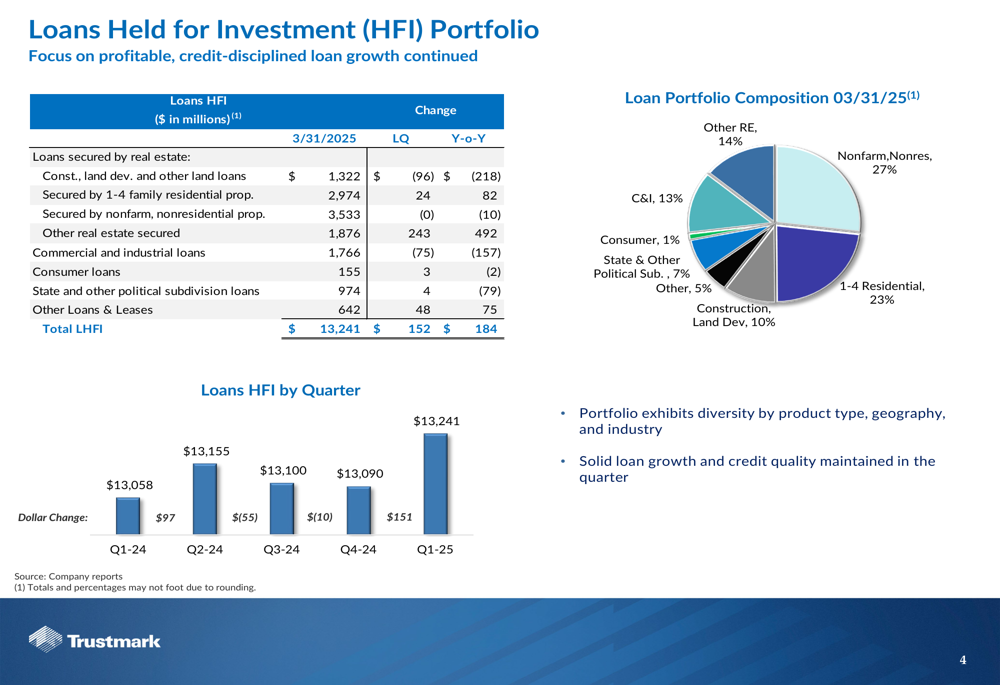

Trustmark’s loans held for investment increased by $151.5 million, or 1.2%, from the previous quarter to $13.2 billion as of March 31, 2025. The loan portfolio remains well-diversified across various categories, with notable growth in other real estate secured loans, which increased by $243 million linked-quarter.

The following chart illustrates the composition and growth trends of Trustmark’s loan portfolio:

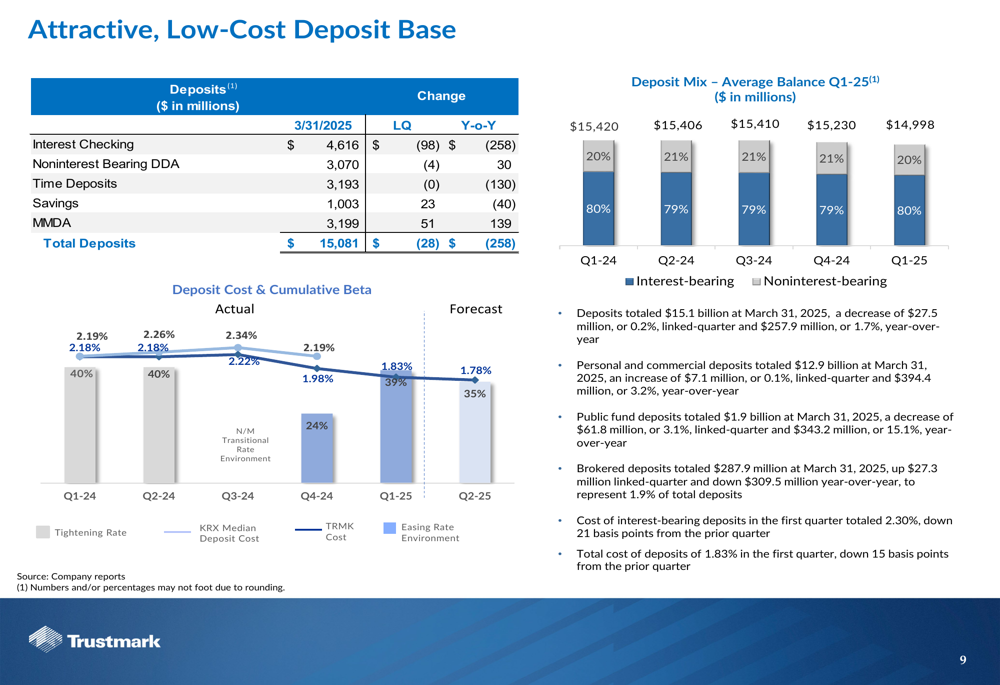

On the funding side, deposits remained stable at $15.1 billion. The company continues to maintain an attractive, low-cost deposit base with the cost of interest-bearing deposits declining to 2.30% in the first quarter, down 21 basis points from the prior quarter. The total cost of deposits decreased to 1.83%, down 15 basis points from the previous quarter.

The deposit mix and cost trends are illustrated in the following chart:

Credit Quality and Risk Management

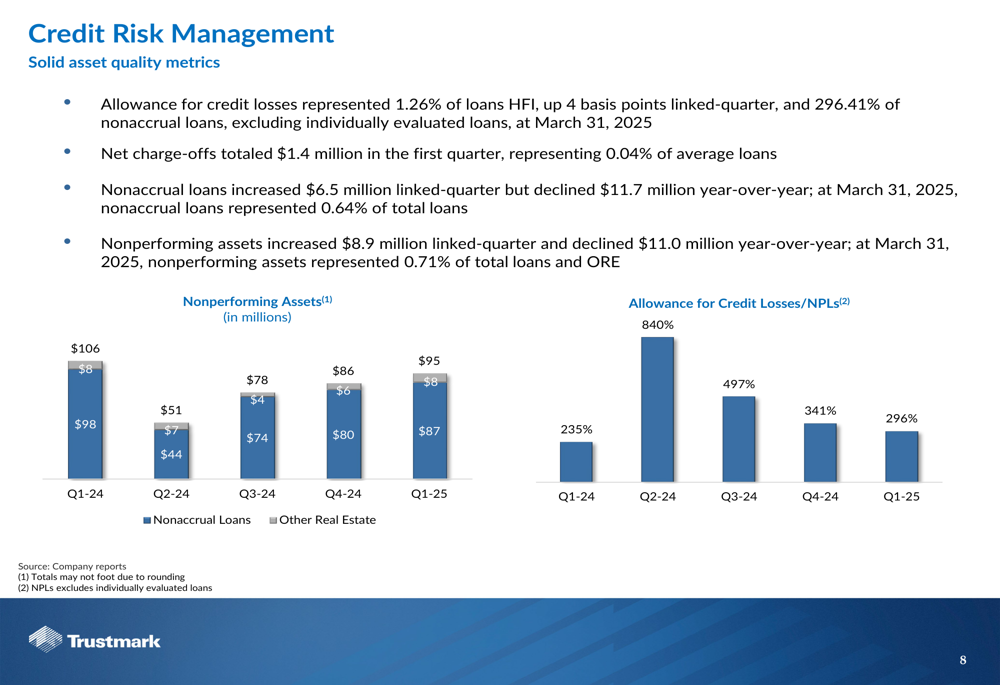

Trustmark maintained solid asset quality in the first quarter of 2025. Net charge-offs totaled $1.4 million, representing just 0.04% of average loans. The allowance for credit losses increased to 1.26% of loans held for investment, up 4 basis points from the previous quarter, and represented 296.41% of nonaccrual loans (excluding individually evaluated loans).

While nonaccrual loans increased $6.5 million linked-quarter, they declined $11.7 million year-over-year. Similarly, nonperforming assets increased $8.9 million from the previous quarter but declined $11.0 million year-over-year.

The following chart provides a detailed view of the company’s credit quality metrics:

The company’s commercial real estate (CRE) portfolio, an area of focus for many investors given industry concerns, is well-diversified with limited exposure to office properties. Office CRE represents just 1.9% of total loans held for investment, with an average loan balance of $1.6 million.

Capital Management and Shareholder Returns

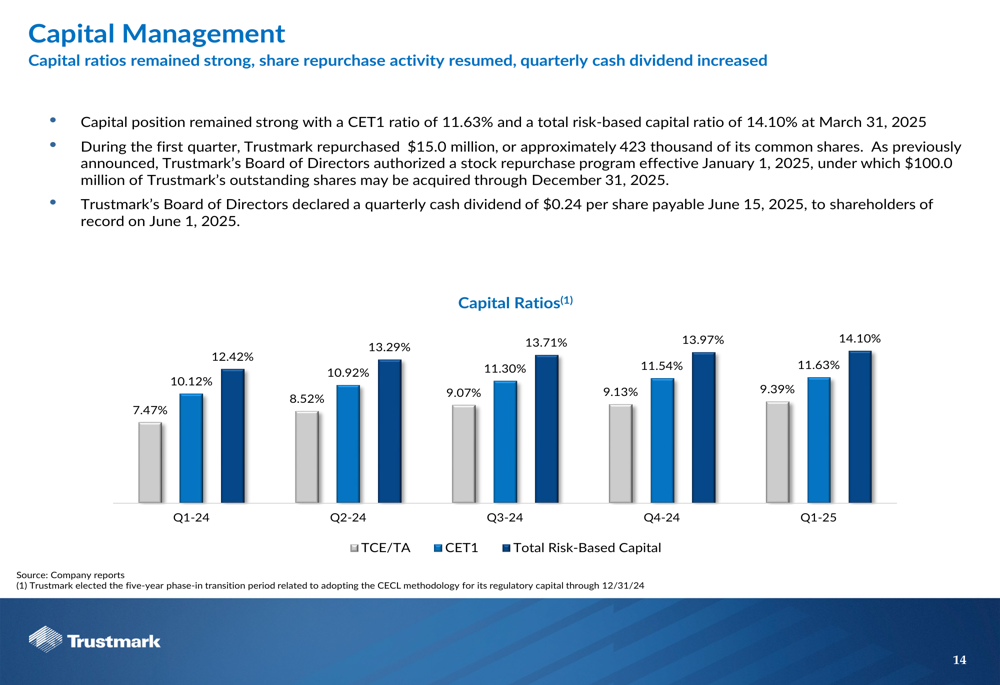

Trustmark’s capital position remained strong with a Common Equity Tier 1 (CET1) ratio of 11.63% and a total risk-based capital ratio of 14.10% as of March 31, 2025. This solid capital foundation has enabled the company to enhance shareholder returns through both share repurchases and dividend increases.

During the first quarter, Trustmark repurchased $15.0 million, or approximately 423,000 shares of its common stock. Additionally, the Board of Directors declared a quarterly cash dividend of $0.24 per share, an increase from the previous $0.23 per share.

The following chart illustrates the company’s strengthening capital position over the past five quarters:

Forward-Looking Statements

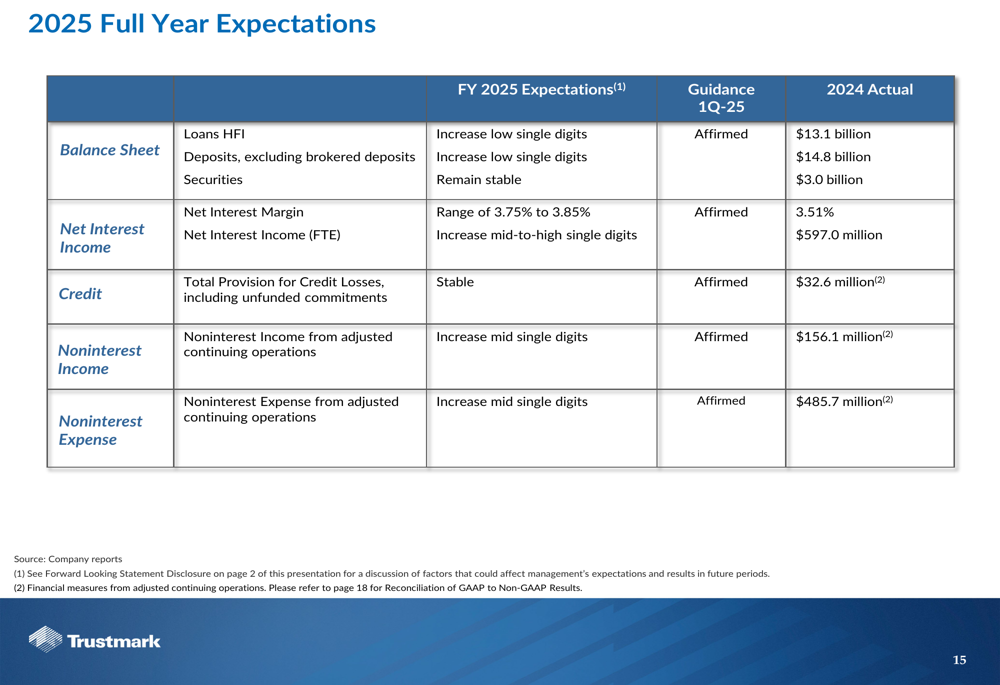

Looking ahead to the full year 2025, Trustmark provided guidance across several key metrics. The company expects loans held for investment and deposits (excluding brokered deposits) to increase in the low single digits. The net interest margin is projected to range between 3.75% and 3.85%, with net interest income expected to increase in the mid-to-high single digits.

Both noninterest income and noninterest expense from adjusted continuing operations are expected to increase in the mid-single digits. The company anticipates that the provision for credit losses, including unfunded commitments, will remain stable compared to 2024.

The following chart summarizes Trustmark’s full-year 2025 expectations:

Trustmark continues to focus on its strategic priorities to enhance shareholder value, including efficiency, growth, innovation, risk management, and culture. The company’s diversified business model and strong capital position provide a solid foundation for navigating the evolving economic environment while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.