European stocks retreat on tech valuation concerns; U.K. economic woes

Introduction & Market Context

Twin Disc Incorporated (NASDAQ:TWIN) presented its first quarter fiscal 2026 results on November 5, 2025, highlighting sales growth across key segments despite missing earnings expectations. The power transmission technology company reported a net loss of $0.04 per share, falling short of the $0.07 per share analysts had forecasted, causing the stock to drop 3.38% to $15.46 in regular trading.

The company's presentation emphasized its increasingly diversified portfolio and strategic positioning in defense markets, while acknowledging challenges including tariff uncertainties and continued, though narrowing, net losses.

Quarterly Performance Highlights

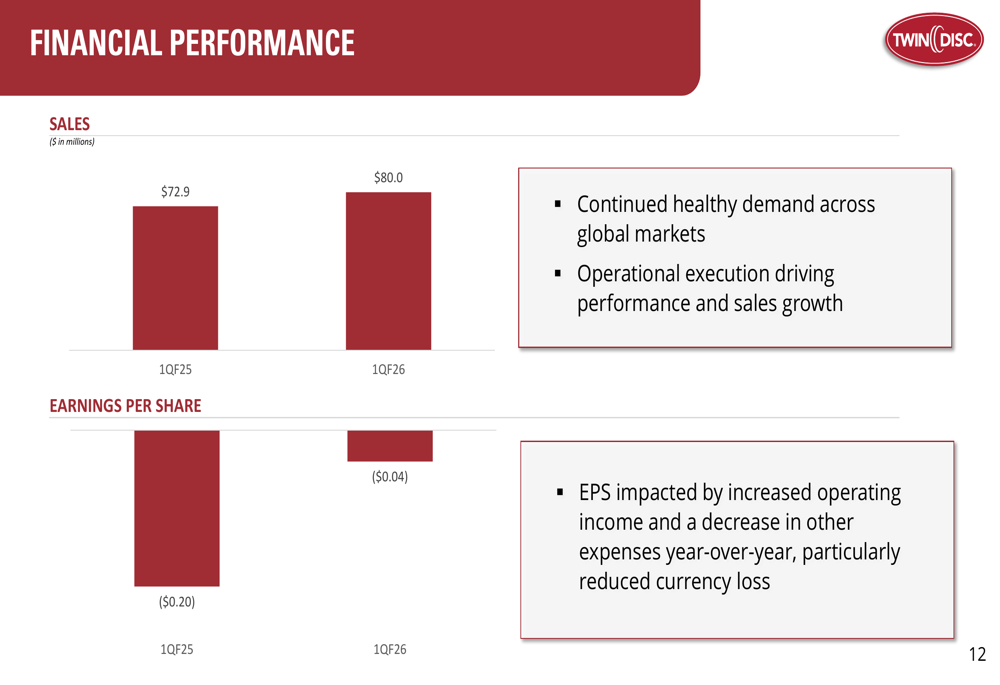

Twin Disc reported Q1 sales of $80.0 million, representing a 9.7% increase year-over-year, in line with market expectations. Organic sales growth was more modest at 1.1%, with the recent Kobelt acquisition contributing significantly to the overall revenue increase.

The company highlighted substantial EBITDA improvement, reporting $4.7 million for the quarter, a 172.3% increase compared to the same period last year. This improvement came despite currency translation losses and stock-based compensation expenses.

As shown in the following financial performance chart:

Despite the improved operational performance, Twin Disc still reported a net loss of $0.04 per share, though this represents a significant improvement from the $0.20 per share loss in the first quarter of fiscal 2025. The company attributed the year-over-year improvement to increased operating income and reduced currency-related losses.

Segment Performance Analysis

The Marine & Propulsion Systems segment emerged as the standout performer, with sales increasing 14.6% compared to the previous year. The company reported record new-unit bookings in the quarter and noted increased demand for autonomous vessels.

The Industrial segment also showed strong growth with sales up 13.2% year-over-year, driven by recovery in demand and order trends. Meanwhile, Land-Based Transmissions sales increased by a more modest 1.6%, with the company noting flat Oil & Gas shipments and a continual decline in China due to tariff uncertainties.

The company's defense business showed particularly promising growth, with defense orders representing approximately 15% of total backlog, a 45% year-over-year increase. The company highlighted a robust defense-related pipeline valued at $50-75 million.

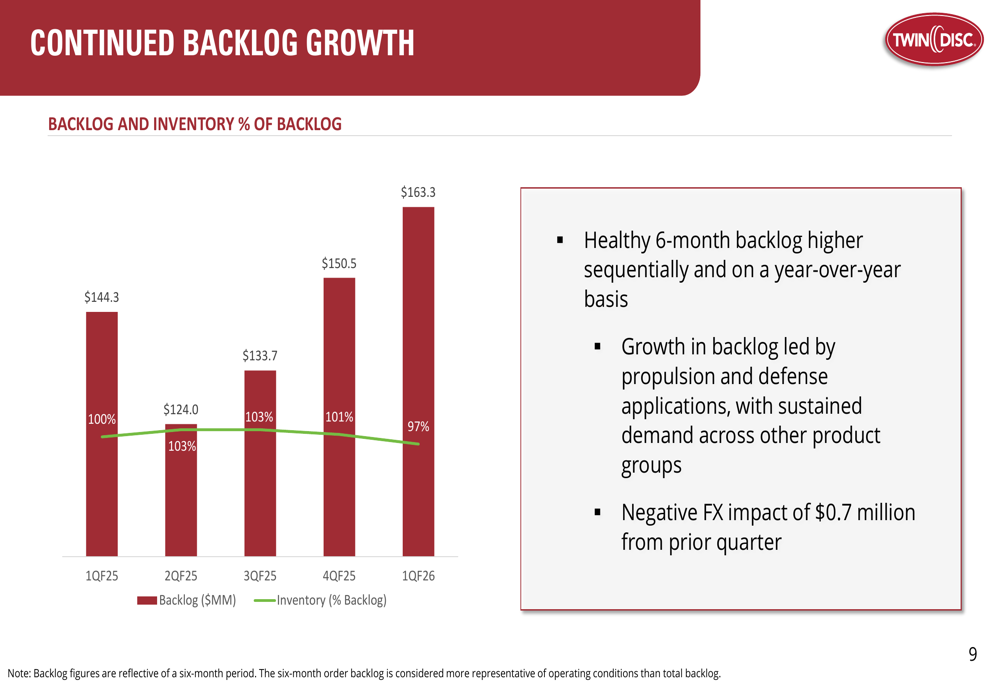

The following chart illustrates the company's continued backlog growth:

The six-month backlog reached $163.3 million, showing sequential growth primarily led by propulsion and defense applications. This healthy backlog provides visibility for future revenue streams despite ongoing market uncertainties.

Balance Sheet and Margin Trends

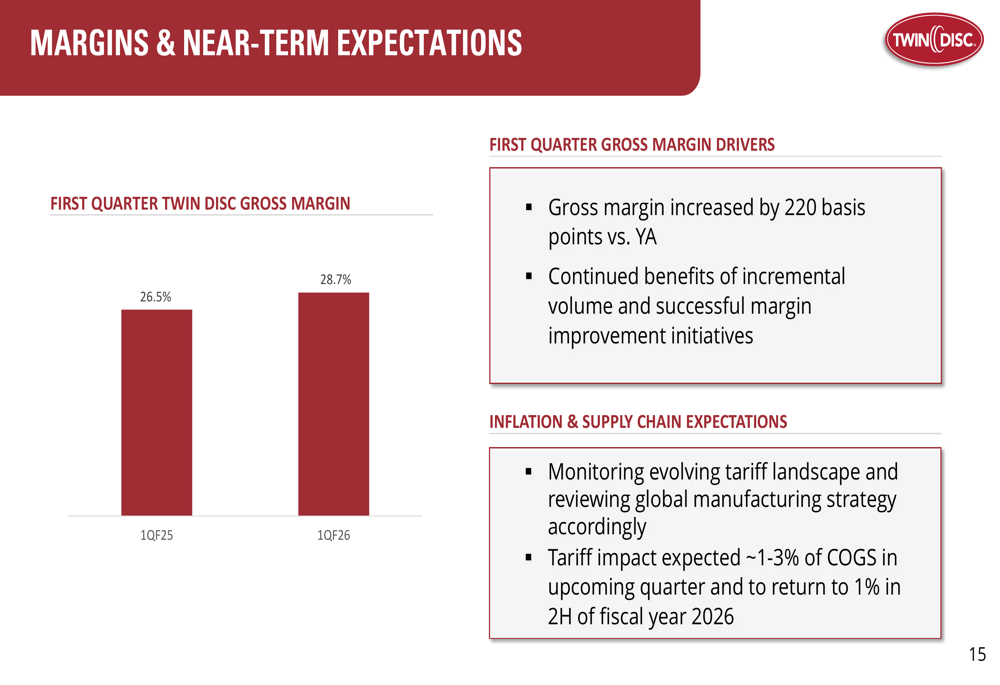

Twin Disc's gross margin improved to 28.7% in Q1 FY2026, up 220 basis points from 26.5% in the prior year period. The company attributed this improvement to incremental volume and successful margin enhancement initiatives.

As shown in the following margin chart:

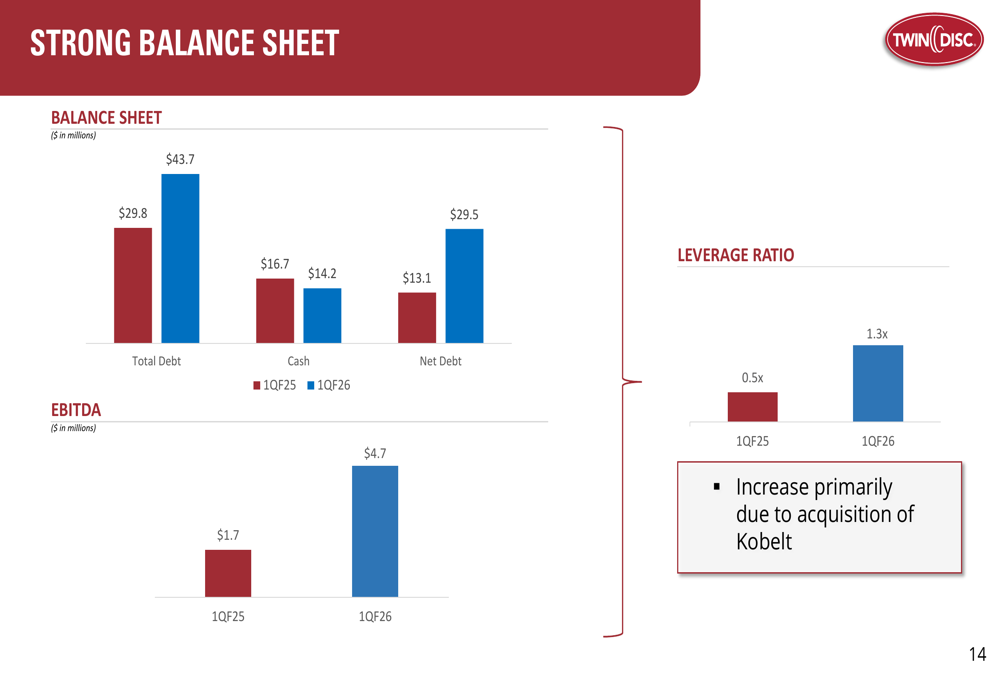

However, the balance sheet reflected increased leverage due to recent acquisition activity. Total debt increased to $43.7 million from $29.8 million, while cash decreased to $14.2 million from $16.7 million. This resulted in net debt of $29.5 million, up from $13.1 million, and an increase in the leverage ratio from 0.5x to 1.3x.

The company noted that the increased debt was primarily due to the acquisition of Kobelt, as illustrated in the following chart:

Looking ahead, Twin Disc is monitoring the evolving tariff landscape, which it expects to impact cost of goods sold by approximately 1-3% in the upcoming quarter before moderating to around 1% in the second half of fiscal 2026.

Strategic Initiatives and Outlook

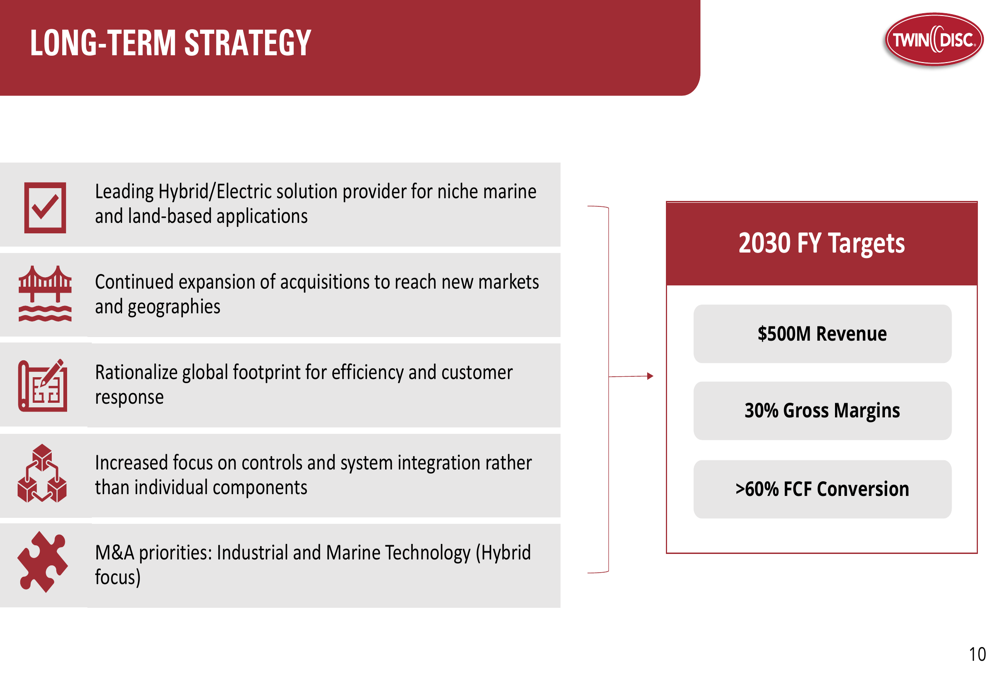

Twin Disc outlined its long-term strategy focused on becoming a leading provider of hybrid/electric solutions for niche marine and land-based applications. The company also emphasized continued expansion through acquisitions to reach new markets and geographies, with a particular focus on industrial and marine technology with a hybrid focus.

As illustrated in the company's long-term strategy slide:

The company has set ambitious 2030 fiscal year targets, including $500 million in revenue, 30% gross margins, and greater than 60% free cash flow conversion. These targets represent significant growth from current levels and reflect management's confidence in the company's strategic direction.

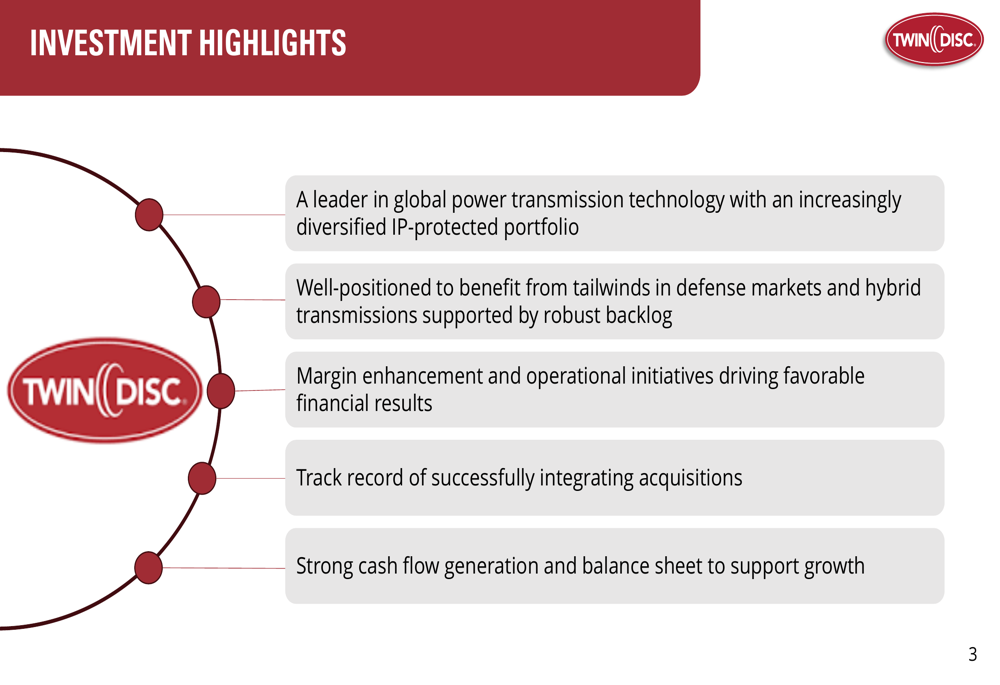

Twin Disc highlighted several key investment points that support its growth trajectory:

Despite the positive long-term outlook, investors appear to be focusing on the near-term earnings miss and increased debt levels. The company's ability to navigate tariff challenges while continuing to improve margins and integrate acquisitions successfully will be critical to achieving its ambitious targets and restoring investor confidence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.