TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

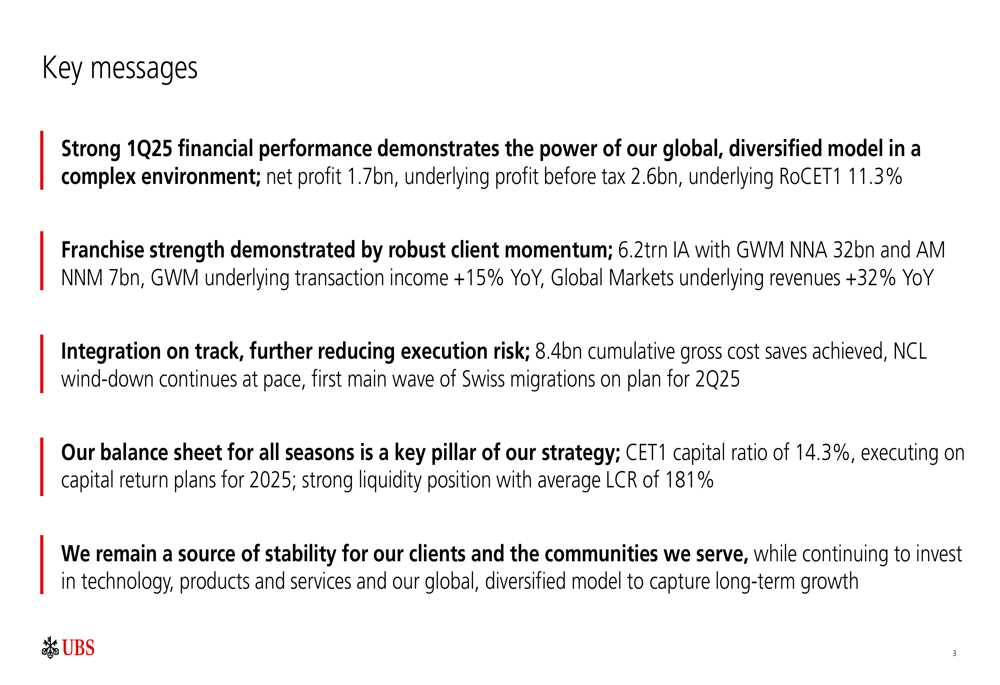

UBS Group AG (NYSE:UBS) (SWX:UBSG) reported a net profit of $1.7 billion for the first quarter of 2025, according to the company’s financial results presentation delivered on April 30. The Swiss banking giant highlighted its continued progress in integrating Credit Suisse operations while maintaining strong performance in key divisions, particularly in wealth management.

The bank reported an underlying profit before tax of $2.6 billion and an underlying return on CET1 capital (RoCET1) of 11.3%, demonstrating resilience amid the ongoing integration process. UBS emphasized that its franchise strength was evident through robust client momentum across divisions.

As shown in the following key performance highlights, UBS maintained stable overall performance while achieving significant progress on cost savings targets:

Quarterly Performance Highlights

UBS’s first quarter results revealed a mixed performance across its business divisions. While the bank’s overall underlying profit before tax remained stable year-over-year at $2.6 billion, core business divisions showed a 15% increase in profit before tax, driven by strong performance in wealth management and investment banking.

The bank’s profitability metrics showed stability, with revenues and operating expenses both essentially flat compared to Q1 2024. However, core revenues increased by 6%, demonstrating the strength of UBS’s primary business lines.

Global Wealth Management emerged as a standout performer, with underlying profit before tax reaching $1.545 billion, representing a 21% increase year-over-year. The division attracted $32 billion in net new assets and $27 billion in net new fee-generating assets, highlighting strong client confidence and business momentum.

In contrast, Personal & Corporate Banking faced headwinds, with profit before tax declining 23% to 597 million CHF, primarily due to lower net interest income. The division also experienced net deposit outflows of 2.9 billion CHF, with inflows in Personal Banking more than offset by outflows in Corporate and Institutional Clients.

The Investment Bank division delivered strong results with profit before tax of $696 million and revenue growth of 24%. Global Markets revenues increased by 32%, while Advisory revenues grew by 17%, driven particularly by strength in the Asia-Pacific region.

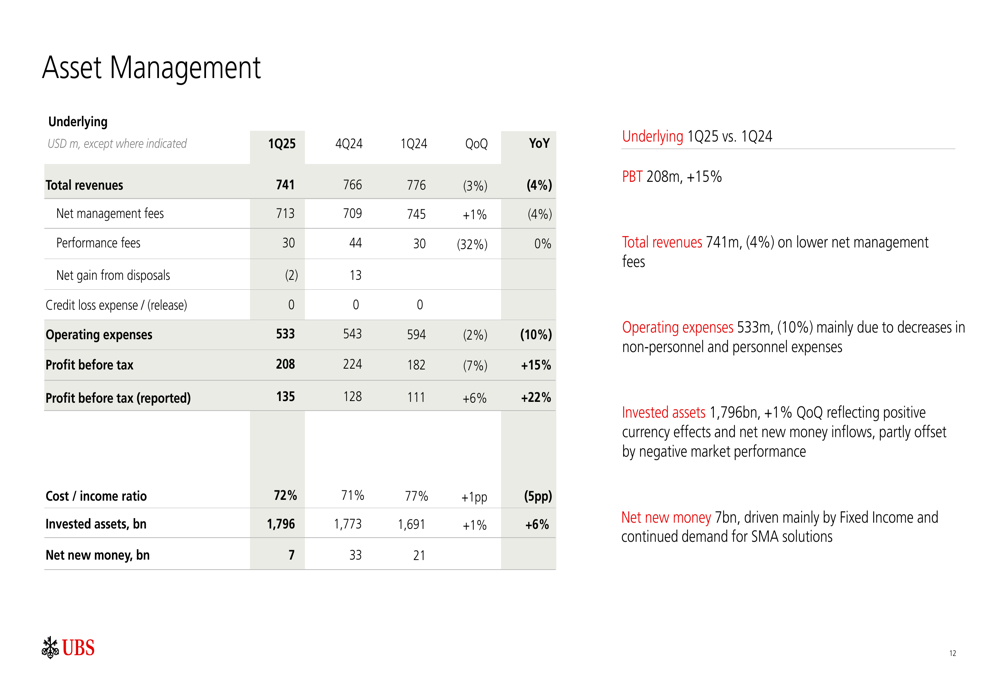

Asset Management also performed well, with profit before tax increasing 15% to $208 million, despite a 4% decline in total revenues due to lower net management fees. The division attracted $7 billion in net new money, driven mainly by Fixed Income and continued demand for separately managed account (SMA) solutions.

Integration Progress

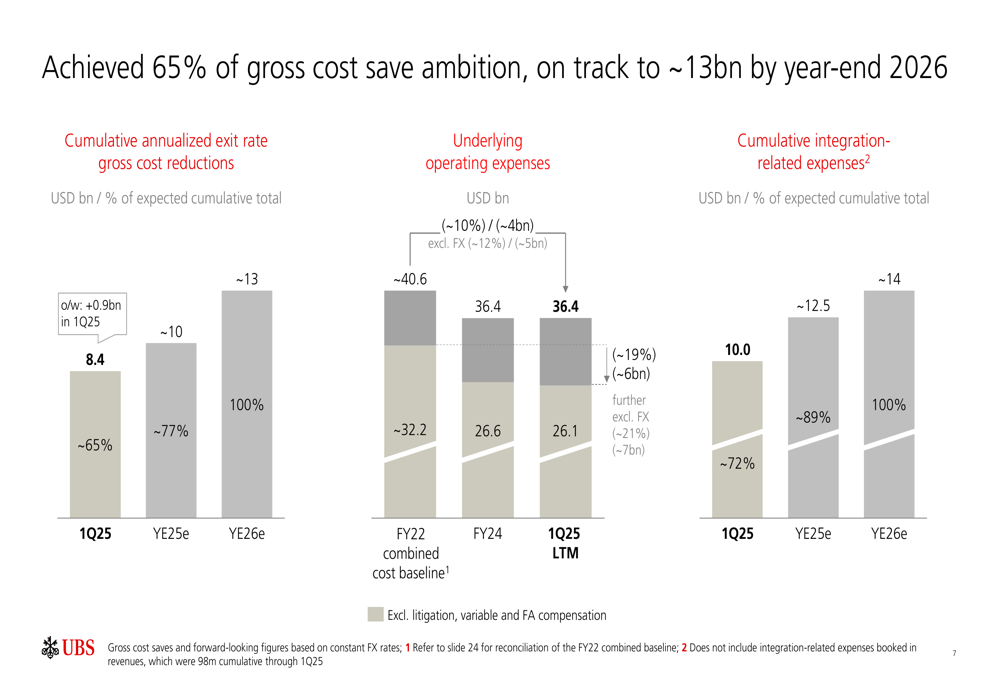

UBS reported significant progress in its integration of Credit Suisse operations, with cumulative gross cost savings reaching $8.4 billion, representing 65% of the expected total by year-end 2026. The bank remains on track to achieve approximately $13 billion in gross cost savings by the end of 2026.

The following chart illustrates UBS’s progress toward its cost savings ambition:

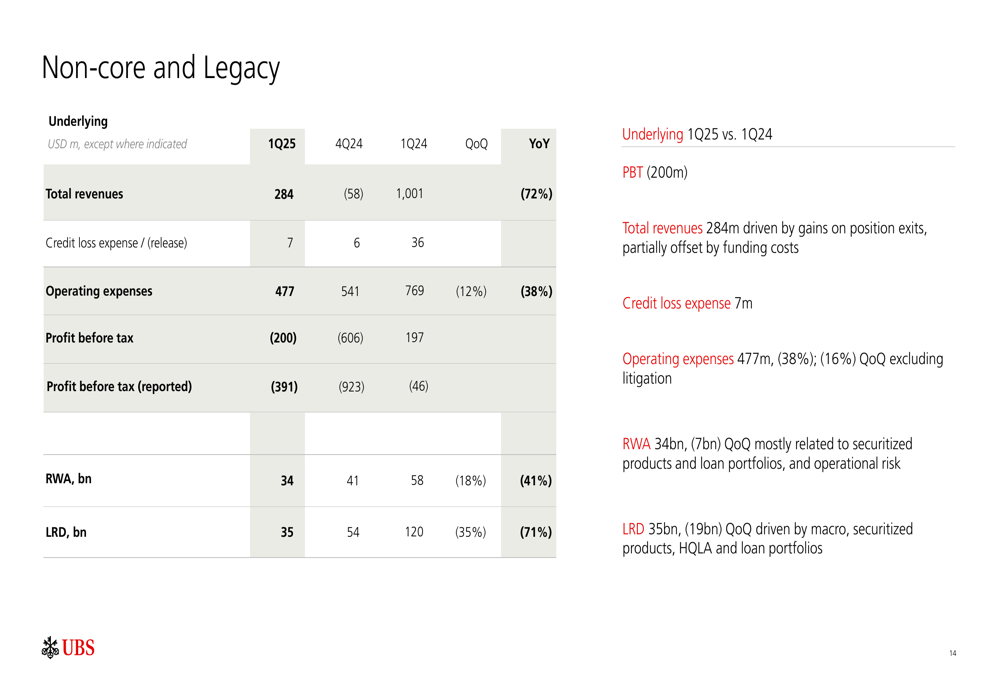

The Non-core and Legacy (NCL) division, which manages the wind-down of non-strategic assets from both UBS and Credit Suisse, reported substantial progress. The bank has closed 74% of NCL books since June 2023 and decommissioned 48% of IT applications in the same period.

Risk-weighted assets (RWA) in the NCL division decreased by $7 billion quarter-over-quarter to $34 billion, primarily related to reductions in securitized products and loan portfolios. UBS has updated its ambition to reduce NCL risk-weighted assets to $24 billion by the end of 2026.

Balance Sheet and Capital Position

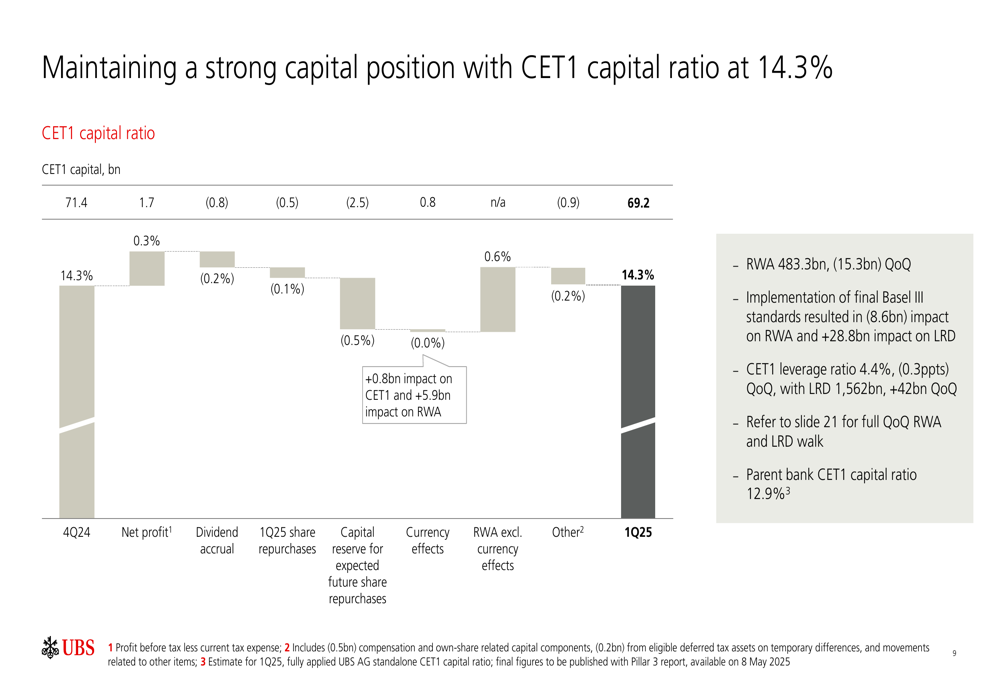

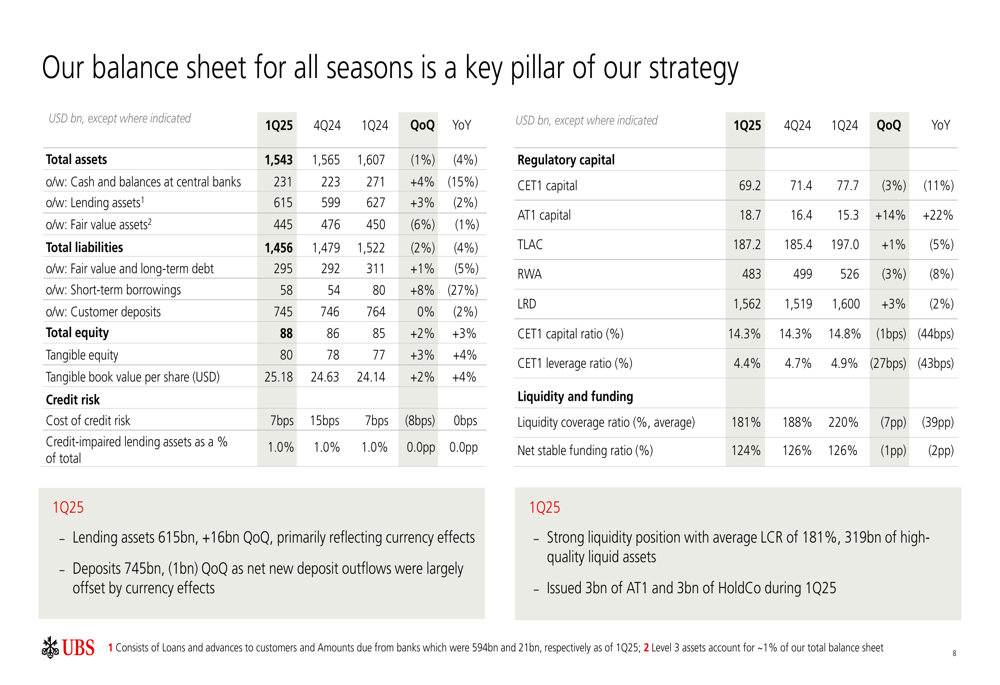

UBS maintained a strong capital position with a CET1 capital ratio of 14.3%, well above its target of approximately 14%. The bank’s liquidity coverage ratio averaged 181%, while its net stable funding ratio stood at 124%, reflecting solid balance sheet fundamentals.

Total (EPA:TTEF) assets decreased slightly to $1.543 trillion in Q1 2025 from $1.565 trillion in Q4 2024. Risk-weighted assets declined by $15.3 billion quarter-over-quarter to $483.3 billion, partly due to the implementation of final Basel III requirements and reductions in credit and counterparty credit risk.

The following chart details the movement in UBS’s CET1 capital during the quarter:

Strategic Outlook

Looking ahead, UBS reaffirmed its financial targets, including an underlying RoCET1 of approximately 15% by the 2026 exit rate and an underlying cost/income ratio below 70% by the same period. The bank’s longer-term ambitions include achieving a reported RoCET1 of approximately 18% by 2028 and growing Global Wealth Management invested assets to more than $5 trillion by 2028.

UBS emphasized its commitment to stability and long-term growth, with integration efforts remaining on track. The bank continues to focus on its core strengths in wealth management while maintaining a diversified business model across investment banking, asset management, and personal and corporate banking.

The presentation highlighted UBS’s strategic priorities of completing the Credit Suisse integration, optimizing its global footprint, and growing its wealth management franchise. With substantial progress on cost savings and strong performance in key divisions, UBS appears well-positioned to achieve its medium and long-term financial targets despite ongoing challenges in certain business areas.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.