Futures slip, bank earnings ahead, Powell to speak - what’s moving markets

Introduction & Market Context

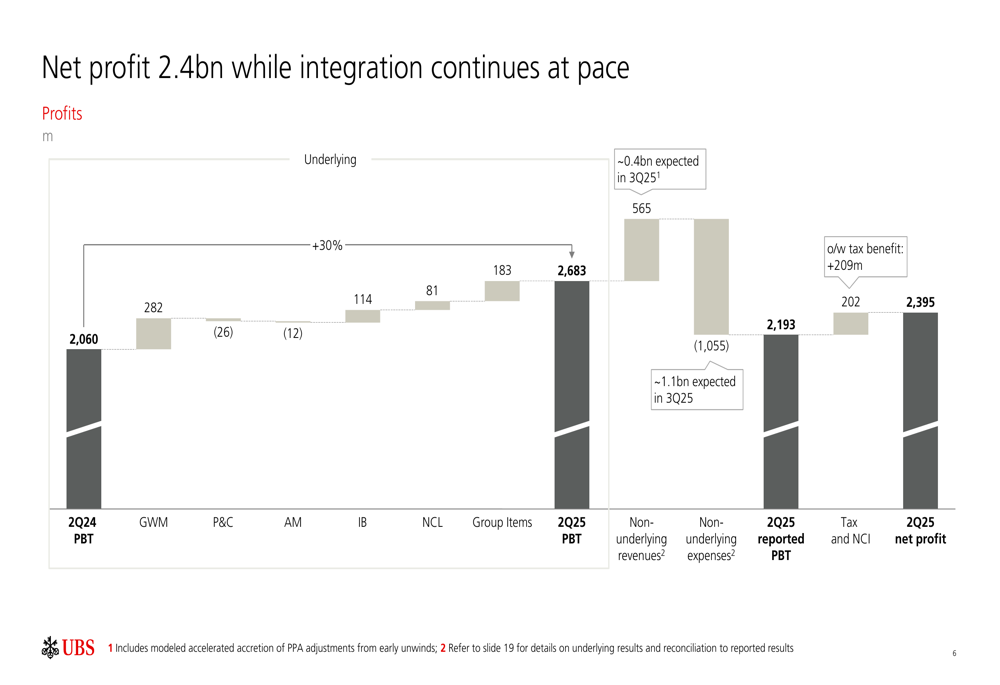

UBS Group AG (NYSE:UBS) (SWX:UBSG) reported a net profit of $2.4 billion for the second quarter of 2025, continuing its positive momentum following the $1.7 billion profit reported in Q1. The results, presented on July 30, 2025, demonstrate the bank’s progress in integrating Credit Suisse operations while maintaining strong performance in its core businesses.

The Swiss banking giant’s stock has shown resilience despite ongoing market volatility, with shares trading near $13.25 in recent sessions. UBS continues to navigate a complex global financial landscape while focusing on integration efforts and strategic growth initiatives.

Quarterly Performance Highlights

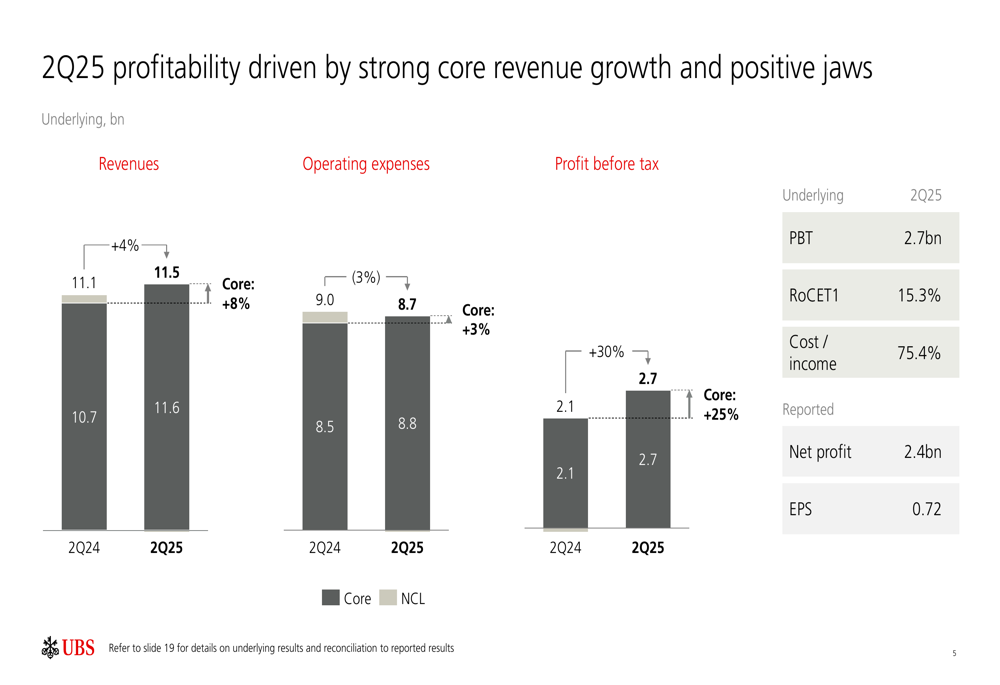

UBS delivered solid financial results in Q2 2025, with underlying profit before tax reaching $2.7 billion and an underlying return on CET1 capital (RoCET1) of 15.3%. For the first half of 2025, the bank reported a net profit of $4.1 billion and underlying profit before tax of $5.3 billion, with a half-year RoCET1 of 13.3%.

As shown in the following profitability overview, the bank achieved core revenue growth of 8% year-over-year, while keeping operating expenses under control with just a 3% increase in core expenses:

The $2.4 billion net profit for Q2 2025 represents a significant improvement from the previous year, driven by strong performance in Global Wealth Management and the Investment Bank. The following breakdown illustrates the key contributors to this profit growth:

Business Division Performance

Global Wealth Management emerged as a standout performer, with profit before tax increasing by 24% year-over-year to $1.44 billion. The division benefited from an 8% increase in recurring net fee income and an impressive 11% growth in transaction-based income. Invested assets grew to $4.51 trillion, up 12% year-over-year and 7% quarter-over-quarter.

The Investment Bank also delivered strong results, with profit before tax rising 28% year-over-year to $526 million. Global Markets was particularly robust, with revenues increasing 26% compared to the same period last year. Within this segment, all three business lines showed strong performance: Execution Services (+24% YoY), Derivatives & Solutions (+25% YoY), and Financing (+27% YoY).

In contrast, Personal & Corporate Banking faced challenges, with profit before tax declining 14% year-over-year to CHF 557 million. This was primarily due to an 11% decrease in net interest income. Asset Management reported a modest 5% year-over-year decline in profit before tax to $216 million, despite a 36% increase in performance fees.

Integration Progress and Cost Savings

UBS continues to make significant progress in integrating Credit Suisse operations, with approximately one-third of Swiss-booked client accounts successfully transferred onto UBS systems. The bank aims to migrate the remaining accounts by the end of Q1 2026.

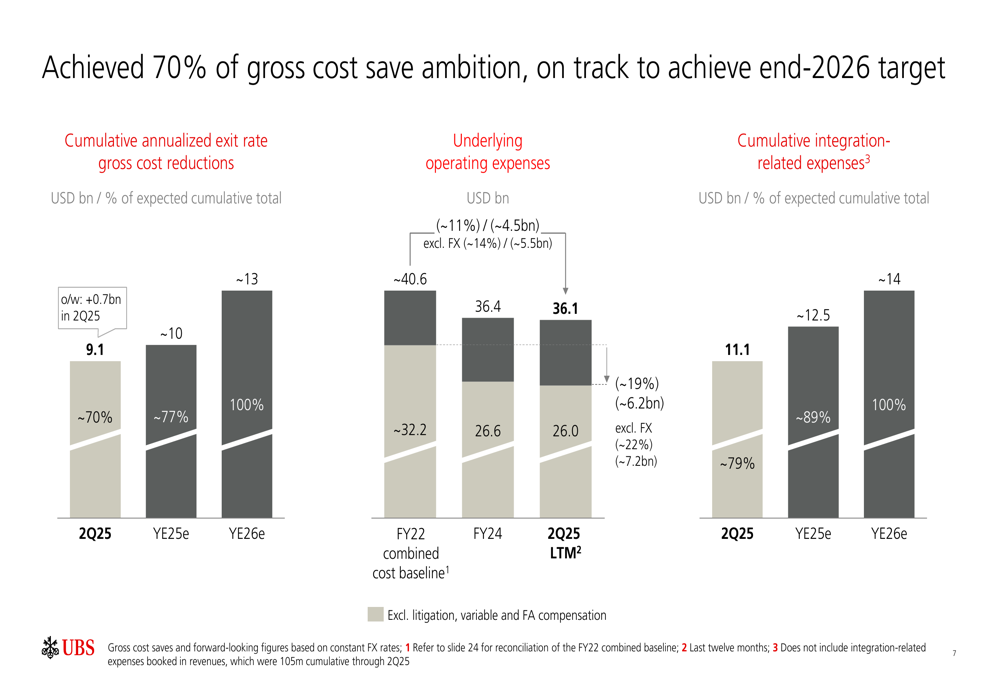

The following chart illustrates UBS’s impressive progress on cost reduction, having achieved $9.1 billion in cumulative annualized gross cost savings, representing approximately 70% of the expected total:

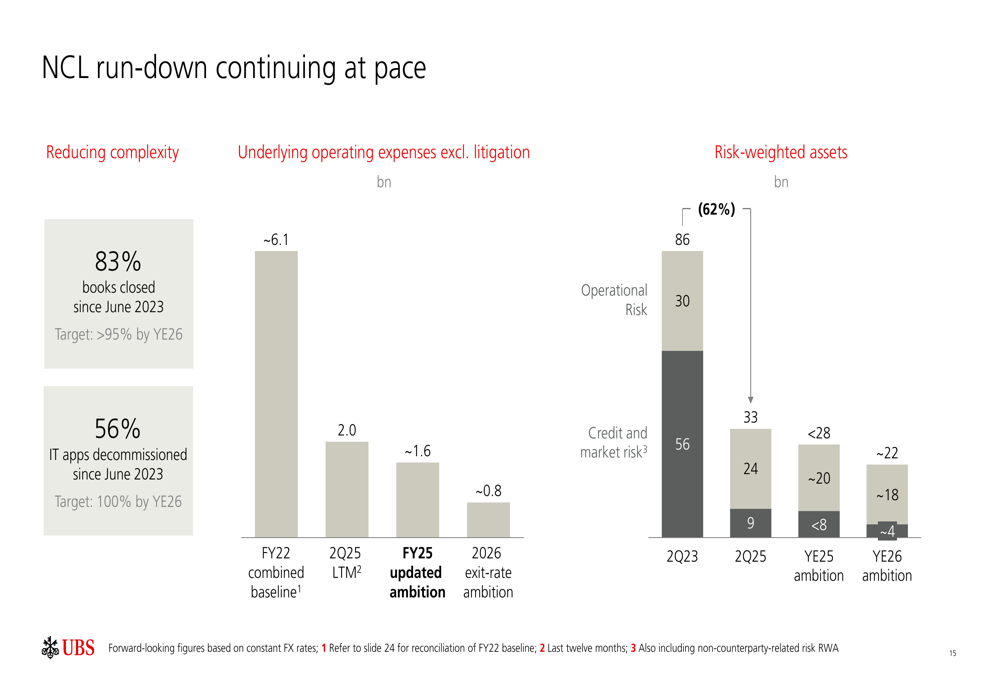

The bank has also made substantial progress in running down its Non-Core and Legacy (NCL) portfolio, with 83% of books closed since June 2023 and 56% of IT applications decommissioned. Risk-weighted assets in the NCL division have been reduced from $86 billion in Q2 2023 to $30 billion in Q2 2025, with a target of approximately $12 billion by year-end 2026.

The following slide demonstrates the progress in NCL run-down and the ambitious targets for further reduction:

Capital Position and Regulatory Concerns

UBS maintained a strong capital position in Q2 2025, with a CET1 capital ratio of 14.4%, up 10 basis points from the previous quarter. The bank’s tangible book value per share increased to $25.95, representing growth of 3% quarter-over-quarter and 9% year-over-year.

The following chart shows the components contributing to the bank’s strong capital position:

However, UBS expressed concerns about proposed Swiss regulatory changes that would significantly increase capital requirements. The bank argues that these proposals would make it an outlier compared to global peers, potentially affecting its competitiveness in international markets.

As illustrated in the following slide, the proposed minimum CET1 ratio requirement of approximately 17% for UBS would be substantially higher than the peer average of 10.9%:

Forward-Looking Statements

UBS remains on track to meet its 2026 exit rate targets, including an underlying return on CET1 capital of approximately 15% and a cost/income ratio of 70%. The bank has made steady progress toward these goals, with the first half of 2025 showing an underlying return on CET1 capital of 13% and a cost/income ratio of 76%.

The following chart illustrates the bank’s progress toward its 2026 targets:

Looking ahead, UBS will continue to focus on completing the Credit Suisse integration, enhancing its global capabilities, and investing in infrastructure and AI technologies. The bank also remains actively engaged in discussions regarding future regulations in Switzerland, advocating for a framework that allows it to compete effectively on the global stage.

With $6.6 trillion in invested assets (up 8% quarter-over-quarter) and strong client momentum across key businesses, UBS appears well-positioned to navigate the challenges and opportunities ahead while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.