US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

Online learning platform Udemy (NASDAQ:UDMY) reported its first quarter 2025 financial results on April 30, marking the first earnings report under new CEO Hugo Sarrazin. The company’s presentation highlighted revenue exceeding $200 million for the first time, significant margin expansion, and continued strategic shift toward subscription-based revenue and enterprise customers.

Sarrazin, who joined Udemy after serving at UKG from 2021-2025 and spending 26 years at McKinsey & Co., expressed optimism about the company’s position: "As I step in as CEO of Udemy, I am excited because our scale, speed of content delivery and the impact we provide will enable us to both redefine and lead this category."

Quarterly Performance Highlights

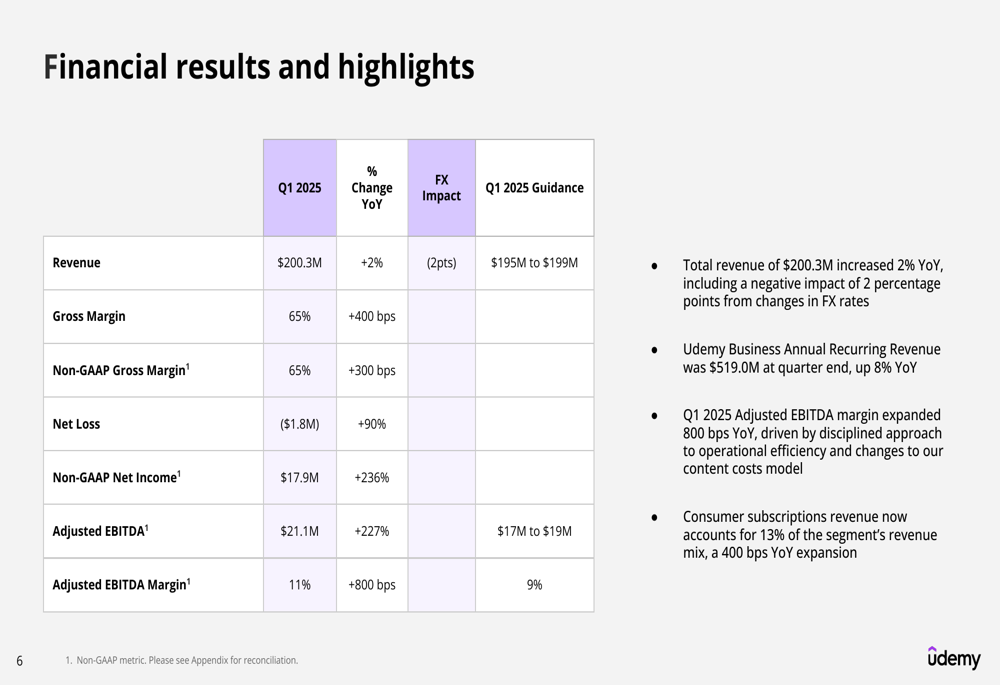

Udemy reported Q1 2025 revenue of $200.3 million, representing 2% year-over-year growth, which included a 2 percentage point negative impact from foreign exchange rates. While revenue growth has slowed compared to previous quarters, the company showed substantial improvement in profitability metrics.

As shown in the following financial results summary:

Gross margin expanded 400 basis points to 65%, while Adjusted EBITDA surged 227% to $21.1 million, representing an 11% margin – an 800 basis point improvement year-over-year. The company’s net loss narrowed significantly to $1.8 million, while non-GAAP net income increased 236% to $17.9 million.

Business Segment Analysis

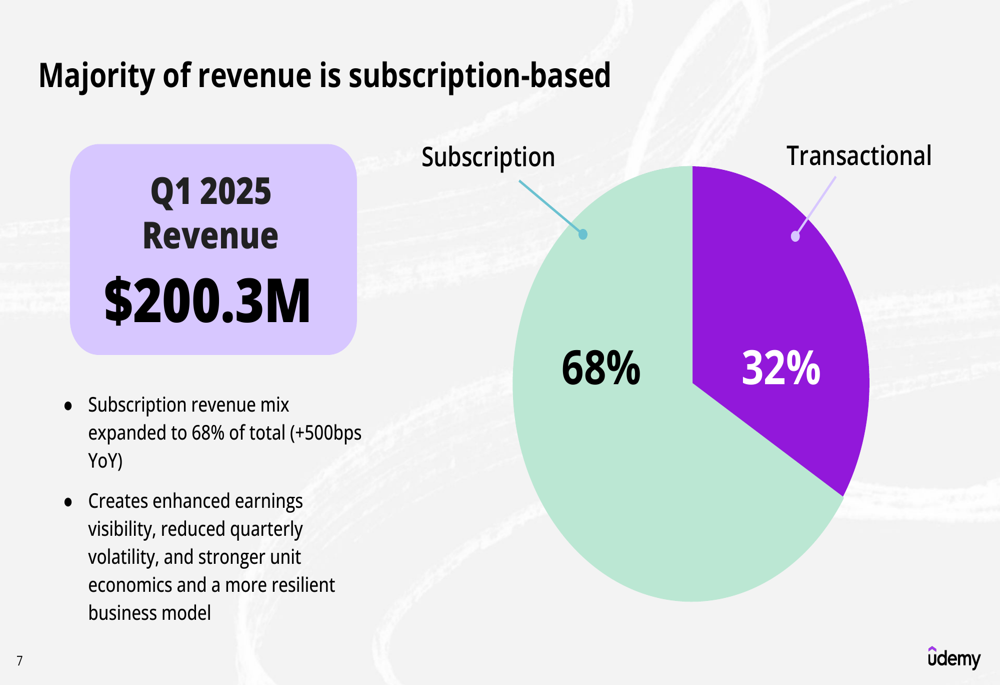

Udemy’s business model continues to shift toward subscription-based revenue, which now represents 68% of total revenue, up 500 basis points year-over-year. This transition is creating enhanced earnings visibility and stronger unit economics, according to the company.

The following chart illustrates this revenue composition:

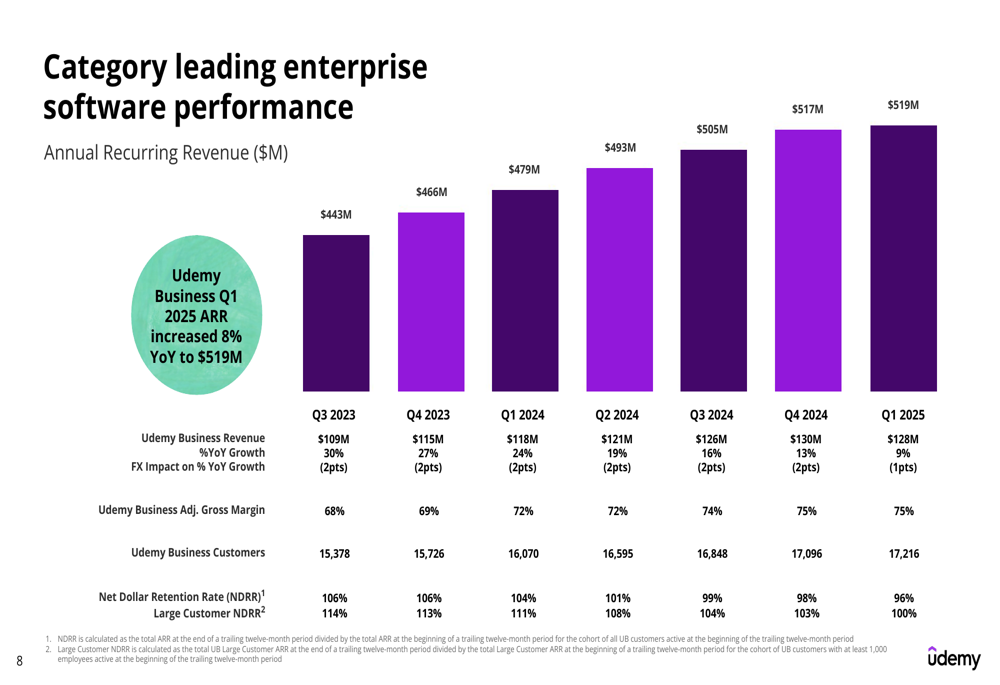

In the enterprise segment, Udemy Business Annual Recurring Revenue (ARR) reached $519.0 million, an 8% increase year-over-year. The company added 120 net new enterprise customers in Q1, bringing the total to 17,216, up 7% from the previous year. Large customers (those with 500+ employees) grew 9% year-over-year to 5,701.

The following chart shows the ARR progression and key enterprise metrics:

However, the presentation revealed declining Net Dollar Retention Rates (NDRR), with overall NDRR at 96% (down from 104% a year earlier) and Large Customer NDRR at 100% (down from 111%). This suggests challenges in expanding usage within existing customer accounts.

The consumer marketplace remains a significant part of Udemy’s ecosystem with 79 million learners, 250,000 total courses, and 85,000 instructors. Consumer segment revenue declined to $72.6 million from $79.2 million a year earlier, but adjusted gross margin improved to 56%. Notably, consumer subscriptions now account for 13% of the segment’s revenue, up from 9% a year ago.

Strategic Initiatives

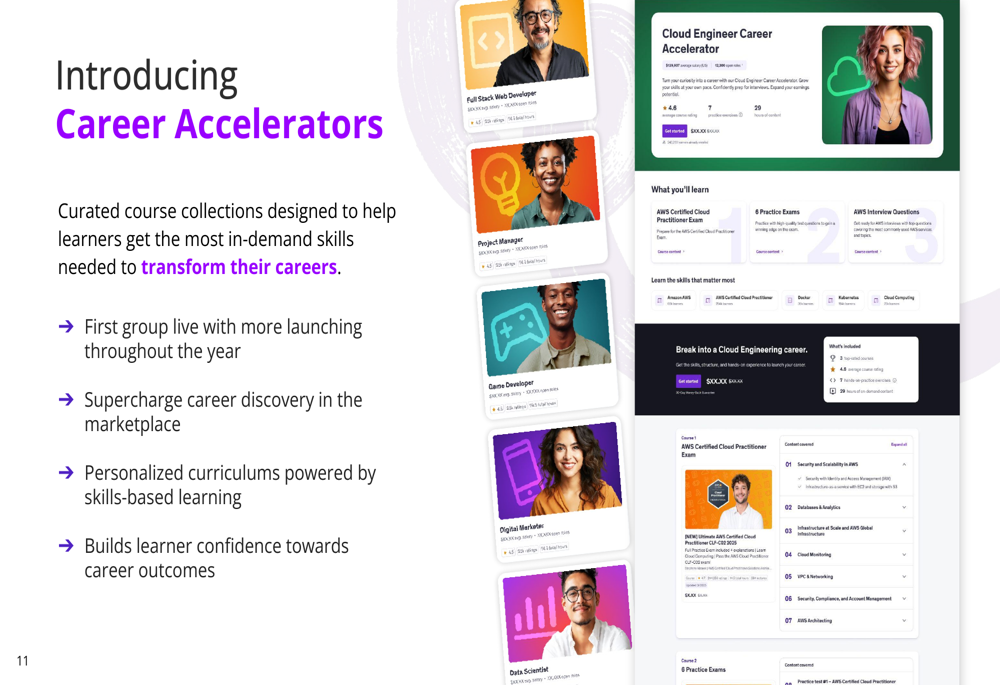

Udemy is focusing on AI innovation to drive growth and differentiation. The company introduced Career Accelerators, which are curated course collections designed to help learners acquire in-demand skills for career transformation.

As shown in the following interface preview:

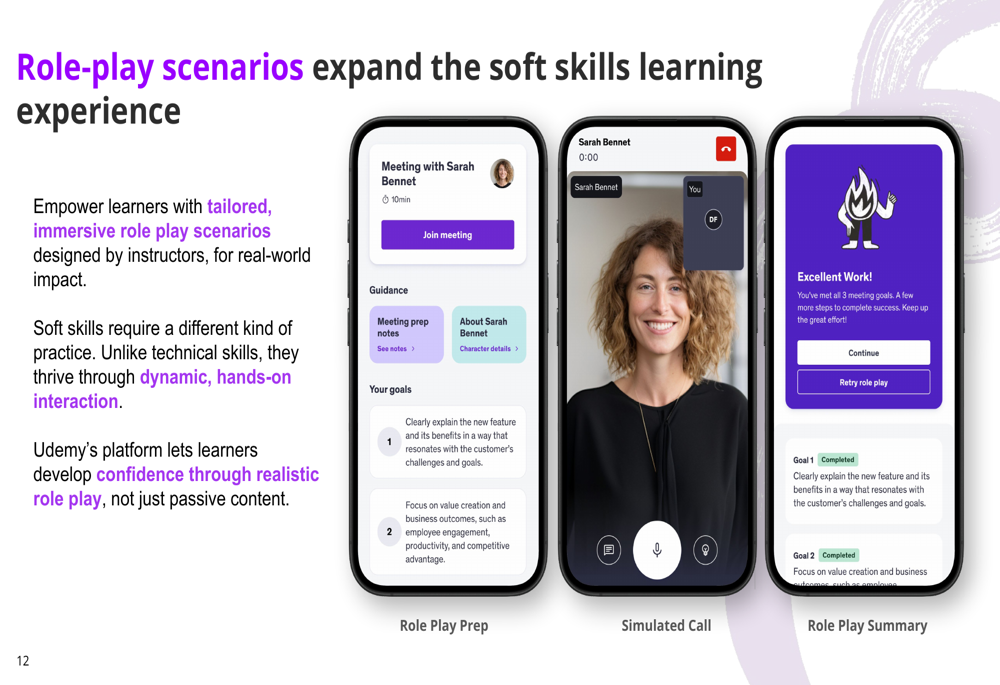

Additionally, Udemy is launching AI-driven role-play scenarios to enhance soft skills learning through immersive, hands-on interaction:

The company outlined several key initiatives to drive revenue growth, including reallocating resources toward large enterprises, positioning Udemy as the AI reskilling platform, emphasizing subscriptions across both consumer and enterprise segments, expanding indirect channels, and pursuing strategic growth opportunities.

Forward-Looking Statements

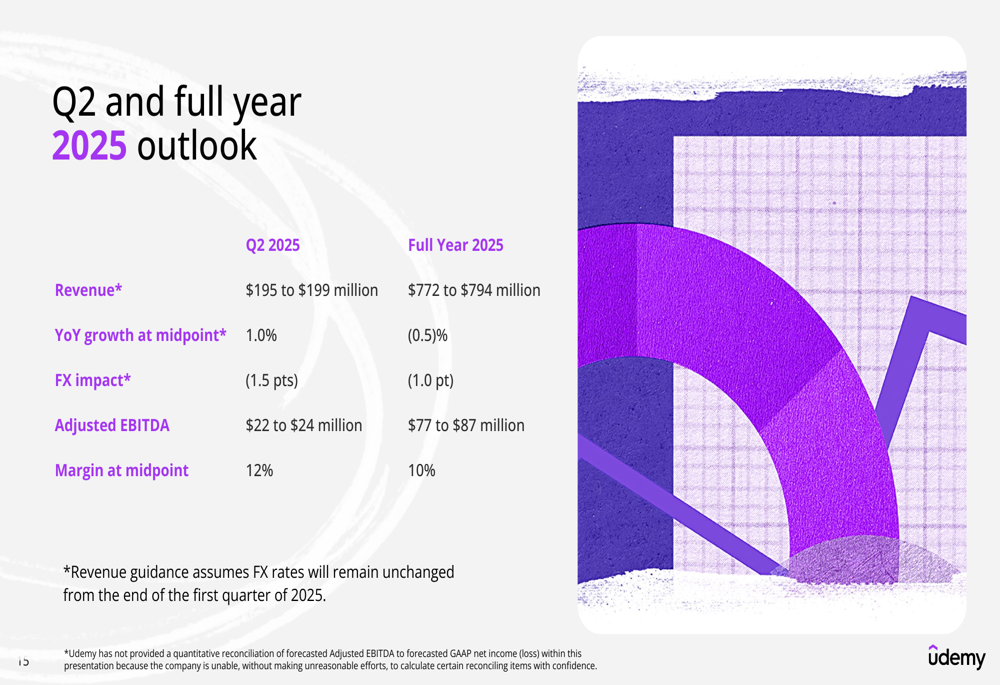

For Q2 2025, Udemy expects revenue between $195 million and $199 million, representing approximately 1% year-over-year growth at the midpoint, with a 1.5 percentage point negative impact from foreign exchange. Adjusted EBITDA is projected to be between $22 million and $24 million, representing a 12% margin at the midpoint.

The full-year 2025 outlook projects revenue between $772 million and $794 million, representing a slight year-over-year decline of 0.5% at the midpoint, with a 1 percentage point negative impact from foreign exchange. Adjusted EBITDA is expected to be between $77 million and $87 million, representing a 10% margin at the midpoint.

This guidance is presented in the following chart:

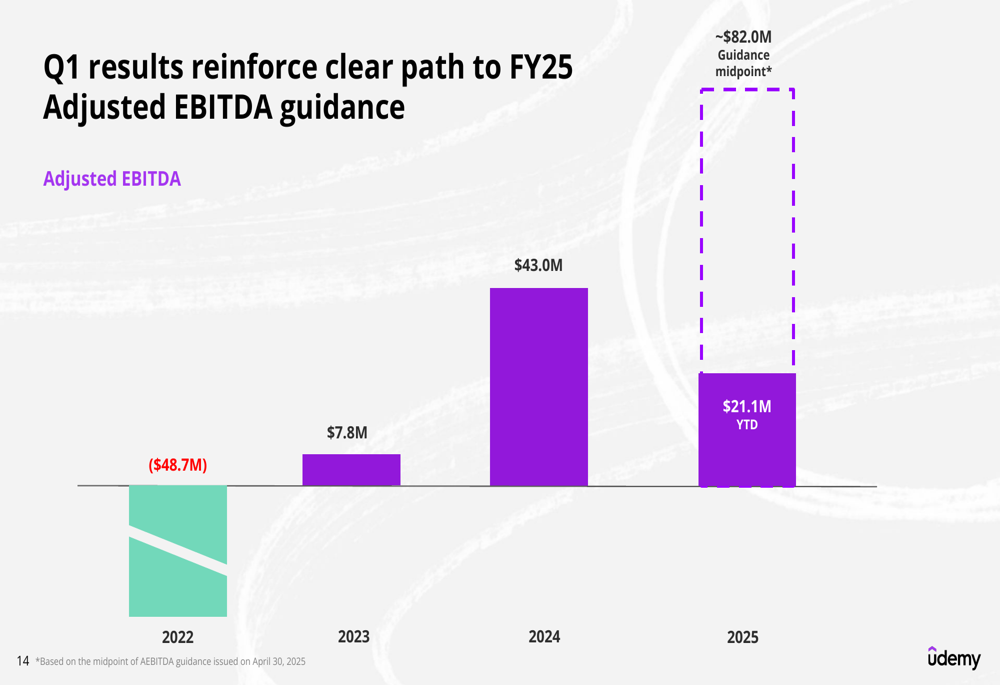

Despite the modest revenue outlook, Udemy remains on track to achieve its long-term profitability goals, as illustrated by the clear progression in Adjusted EBITDA:

Conclusion

Udemy’s Q1 2025 presentation reveals a company in transition, balancing slowing topline growth with significant improvements in profitability. The strategic shift toward subscription revenue and enterprise customers, particularly large enterprises, appears to be yielding margin benefits while creating a more predictable business model.

However, declining net dollar retention rates and modest revenue growth projections suggest challenges ahead in an increasingly competitive online learning market. The company is betting on AI innovations and new product offerings to differentiate its platform and drive future growth.

With a strong cash position and improving profitability metrics, Udemy appears focused on sustainable growth and long-term value creation under its new CEO’s leadership. Investors will likely be watching closely to see if the company’s strategic initiatives can reaccelerate growth while maintaining the positive profitability trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.