Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

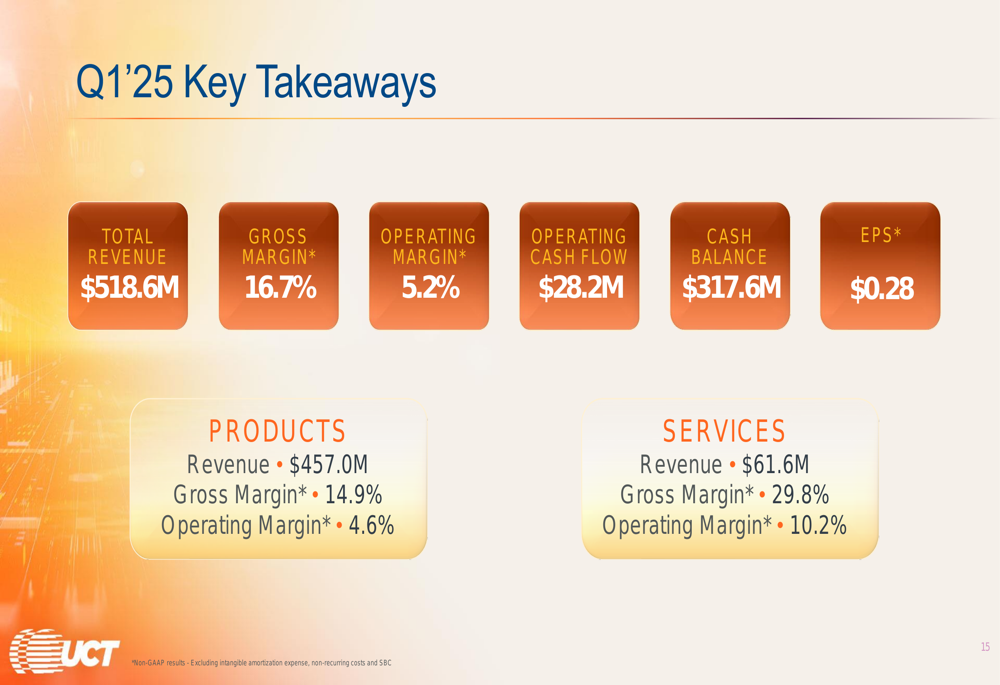

Ultra Clean Holdings Inc (NASDAQ:UCTT) released its Q1 2025 financial results, revealing performance that fell short of market expectations amid ongoing challenges in the semiconductor industry. The company reported revenue of $518.6 million, missing analyst forecasts of $561.33 million, while non-GAAP earnings per share came in at $0.28, below the anticipated $0.31.

Following the announcement, Ultra Clean’s stock dropped 7.94% in after-hours trading to $20.53, reflecting investor concerns about the company’s near-term outlook. The stock has experienced significant volatility over the past year, trading between a 52-week low of $16.66 and a high of $56.47.

Quarterly Performance Highlights

Ultra Clean’s Q1 2025 results showed a decline from the previous quarter, with total revenue falling to $518.6 million from $563.3 million. The company attributed approximately $12 million of this revenue miss to technical issues with two key customers.

As shown in the following detailed financial breakdown:

The company’s Products segment generated $457.0 million in revenue with a non-GAAP gross margin of 14.9% and operating margin of 4.6%. Meanwhile, the Services segment contributed $61.6 million with substantially higher margins – 29.8% gross margin and 10.2% operating margin. Despite the revenue shortfall, Ultra Clean maintained positive operating cash flow of $28.2 million and a healthy cash balance of $317.6 million.

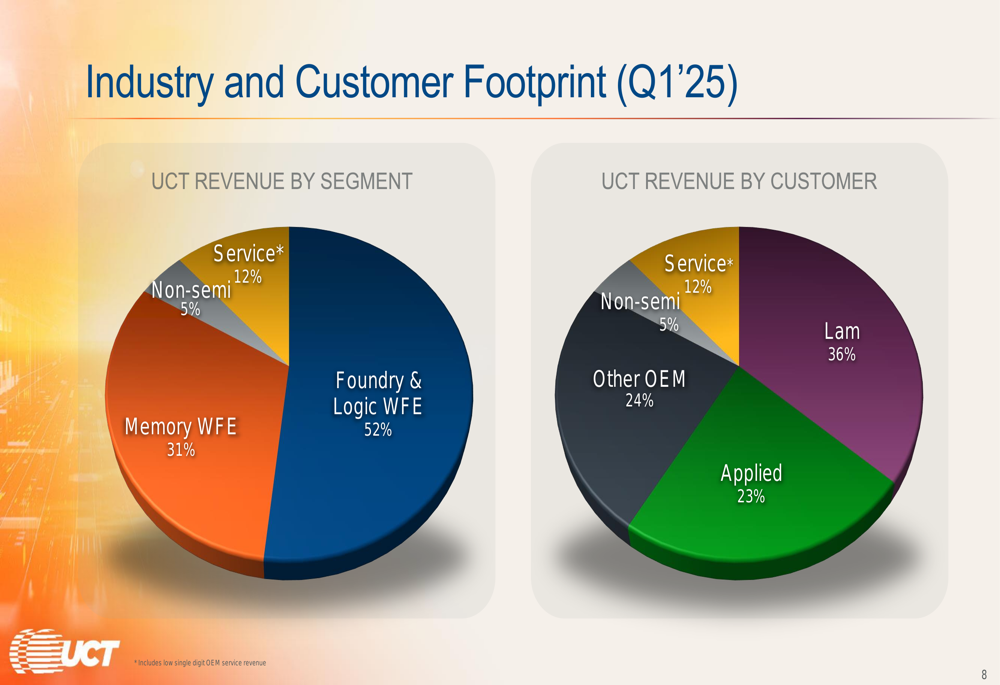

Ultra Clean’s revenue remains heavily concentrated among major semiconductor equipment manufacturers, with Lam Research (NASDAQ:LRCX) and Applied Materials (NASDAQ:AMAT) accounting for 59% of total revenue. The company’s end market exposure is primarily in foundry and logic wafer fabrication equipment (WFE), which represents 52% of revenue, followed by memory WFE at 31%.

The following chart illustrates the company’s revenue breakdown by segment and customer:

Strategic Initiatives

Despite current headwinds, Ultra Clean continues to execute its long-term growth strategy through strategic acquisitions, product innovation, and global expansion. Since 2015, the company has completed several acquisitions to diversify its offerings and accelerate revenue growth.

The company’s acquisition-driven growth strategy is illustrated in this comprehensive timeline:

These strategic acquisitions have enabled Ultra Clean to expand its total addressable market (TAM) and improve margins. The company estimates its 2025 TAM at $25-30 billion for products and $1.4-1.8 billion for services, within a total wafer fabrication equipment market of $95-100 billion.

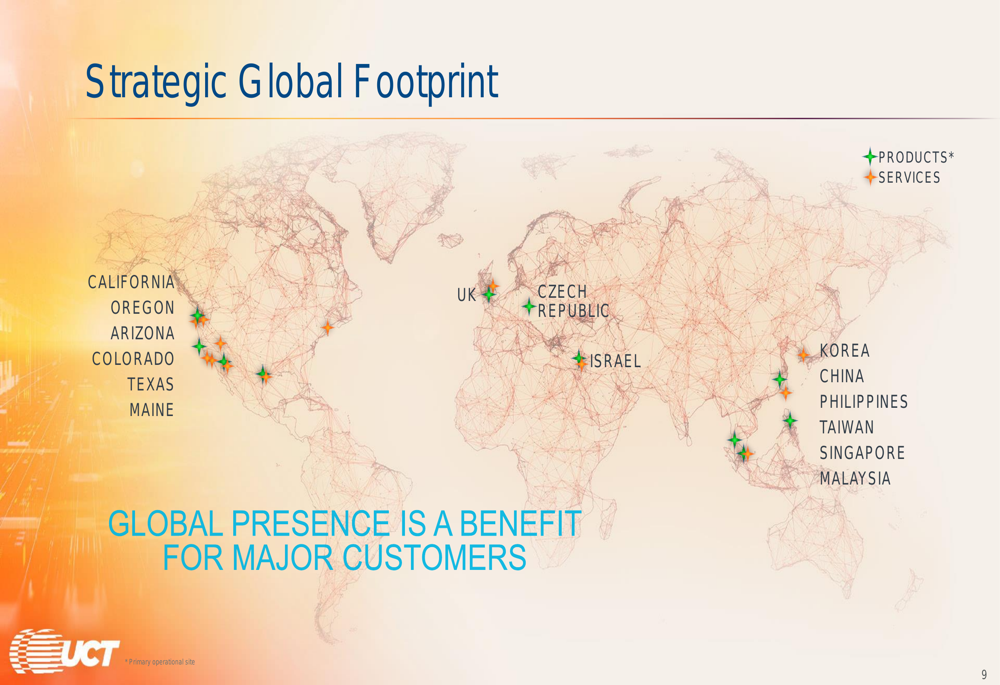

Ultra Clean’s global footprint represents a competitive advantage, with facilities strategically located across North America, Europe, the Middle East, and Asia to serve major customers worldwide:

Interim CEO Clarence Granger emphasized the company’s focus on cost reduction and scalability during the earnings call, stating, "We are now going to look at all of our business systems and cost structures and scale them to our current volumes." The company is also accelerating the ramp-up of its Arizona fab in partnership with a major chipmaker, which management expects to contribute to future growth.

Industry Outlook

Ultra Clean’s presentation provided insights into current semiconductor end market conditions, highlighting both challenges and opportunities across different segments:

In the foundry segment, investments continue to support long-term demand, particularly for advanced packaging and gate-all-around (GAA) technologies that enable AI applications. Logic spending is occurring across a wider base as current shortages ease, while memory markets show signs of improvement driven by AI demand, particularly for high-bandwidth memory (HBM).

The company’s total available market remains substantial, with the 2025 total chip market estimated at $780 billion:

Forward-Looking Statements

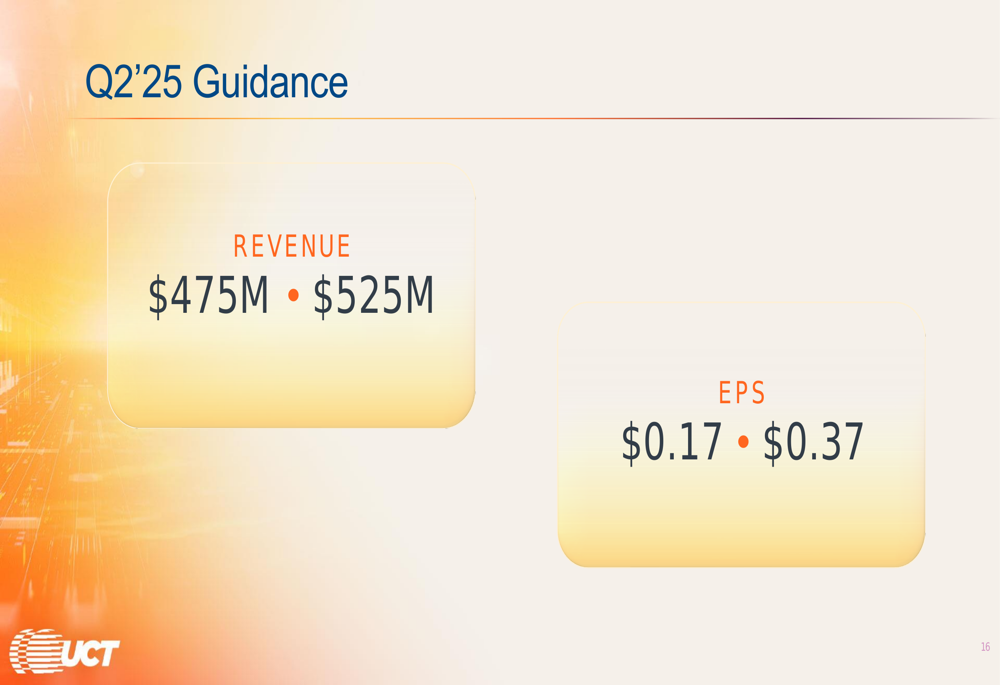

For the second quarter of 2025, Ultra Clean provided revenue guidance of $475-525 million and non-GAAP EPS guidance of $0.17-0.37:

This wide guidance range reflects ongoing market uncertainties and geopolitical factors affecting the semiconductor industry. Management anticipates a slight revenue increase in Q2 with further improvements expected in the latter half of the year.

However, several risks could impact future performance, including geopolitical uncertainties affecting supply chains, potential flat or declining semiconductor industry growth in 2025, tariff impacts on international operations, and the ongoing CEO search, which is expected to conclude in approximately four months.

Despite these challenges, Ultra Clean remains focused on its long-term growth strategy, with Granger expressing optimism about the company’s strategic initiatives: "We expect all these initiatives will gain momentum once economies of scale kick in commensurate with a market recovery."

As Ultra Clean navigates the current semiconductor industry headwinds, investors will be closely monitoring whether the company’s cost reduction measures and strategic initiatives can drive improved performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.