Elastic launches GPU-accelerated inference service for AI workflows

Introduction & Market Context

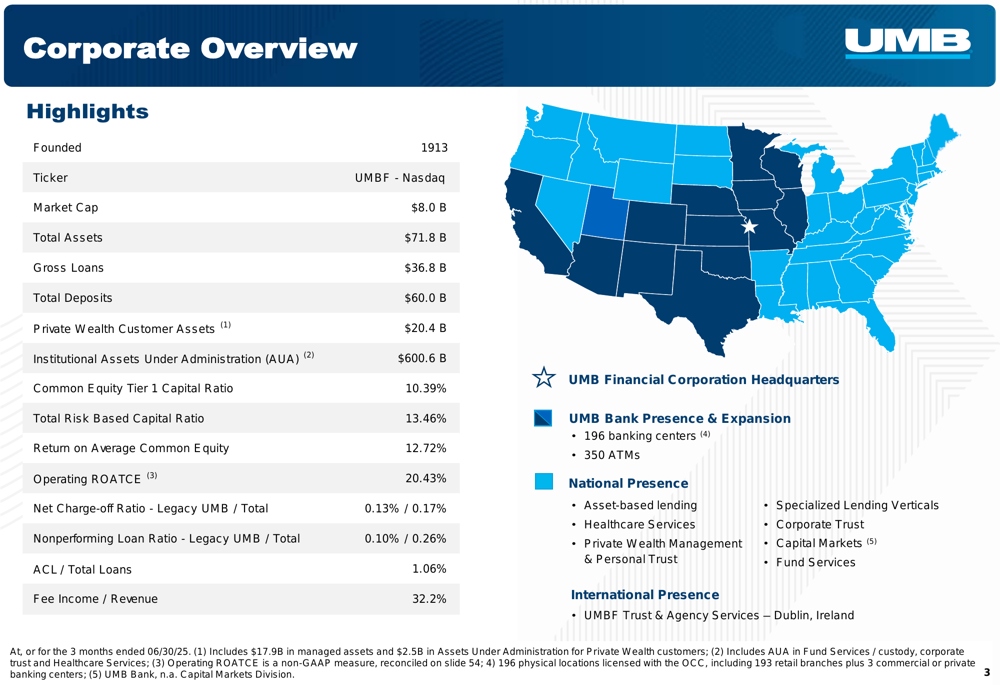

UMB Financial Corporation (NASDAQ:UMBF) presented its second quarter 2025 results on July 29, 2025, revealing substantial growth in revenue and earnings. The Kansas City-based financial services company reported that its total assets have reached $71.8 billion, with a market capitalization of $8.0 billion. UMB’s stock closed at $109.20 on the presentation date, up 0.23% for the day, and has traded between $82.00 and $129.94 over the past 52 weeks.

The Q2 results demonstrate significant improvement from the first quarter, when the company reported earnings per share of $2.58 and revenue of $563.84 million. The integration of Heartland Financial (NASDAQ:HTLF), which was mentioned in the Q1 earnings report, continues to be a key driver of growth for UMB.

As shown in the following corporate overview, UMB has established a strong presence across multiple states with 196 banking centers and 350 ATMs:

Quarterly Performance Highlights

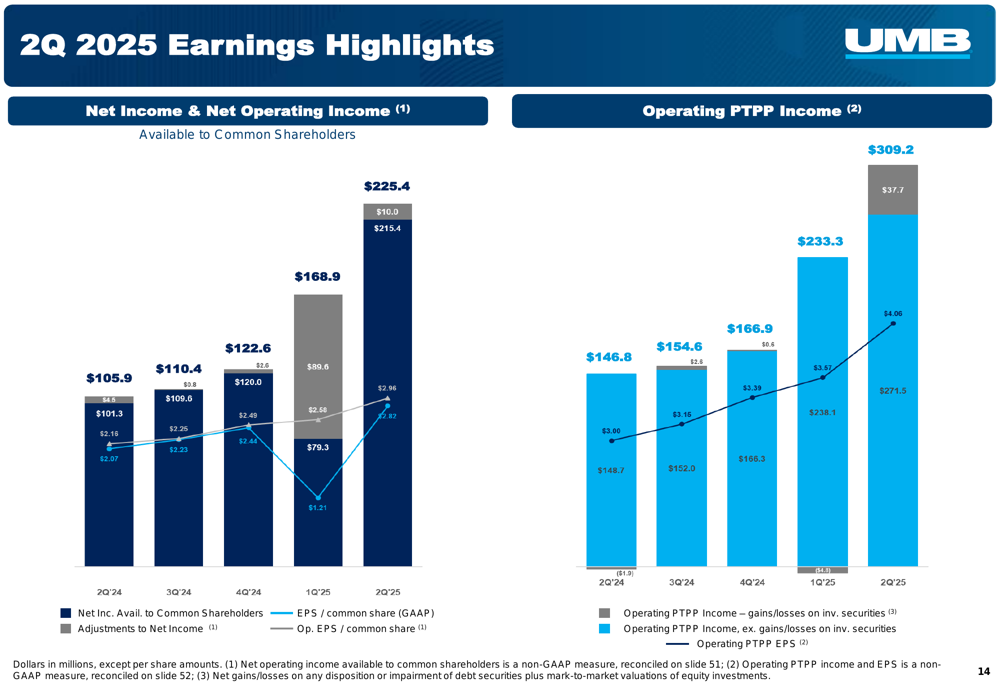

UMB Financial delivered impressive financial results for the second quarter of 2025, with GAAP net income available to common shareholders reaching $215.4 million, or $2.82 per diluted share. On an operating basis, which excludes certain non-recurring items, net income available to common shareholders was $225.4 million, or $2.96 per diluted share.

Total (EPA:TTEF) revenue surged to $689.2 million, representing a substantial increase from the previous quarter’s $563.8 million. This growth was driven by both net interest income and noninterest income components.

The following chart illustrates UMB’s earnings performance, highlighting both GAAP and operating results:

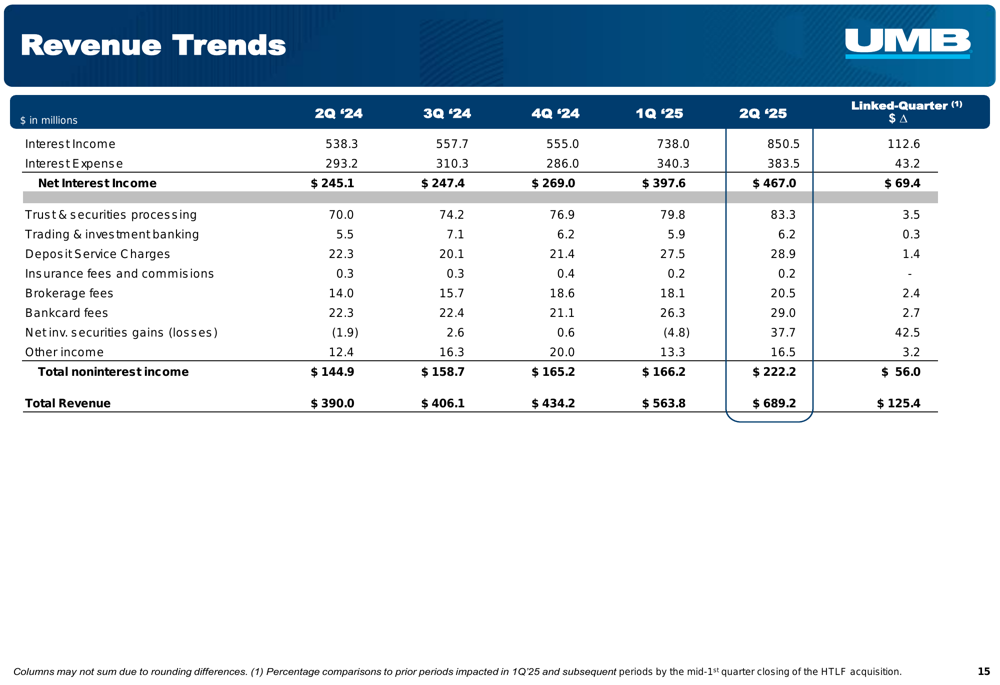

Net interest income for the quarter was $467.0 million, compared to $397.6 million in the first quarter of 2025. Noninterest income contributed $222.2 million to total revenue, including $37.7 million in investment securities gains. The company’s diversified revenue streams continue to be a key strength, with fee income representing 32.2% of total revenue.

The detailed revenue breakdown shows consistent growth across multiple categories:

HTLF Acquisition Impact

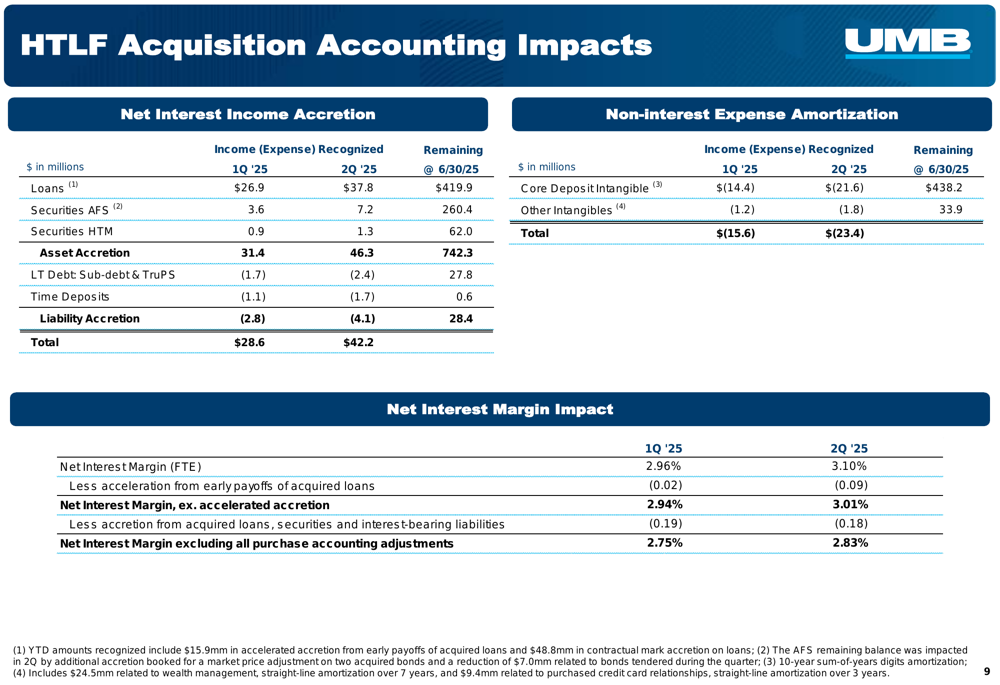

The acquisition of Heartland Financial (HTLF) continues to positively impact UMB’s financial results. The purchase accounting adjustments contributed significantly to net interest income, with loan accretion of $37.8 million, securities accretion of $8.5 million, and liability accretion of -$4.1 million in the second quarter.

The following table details the accounting impacts of the HTLF acquisition on UMB’s financial statements:

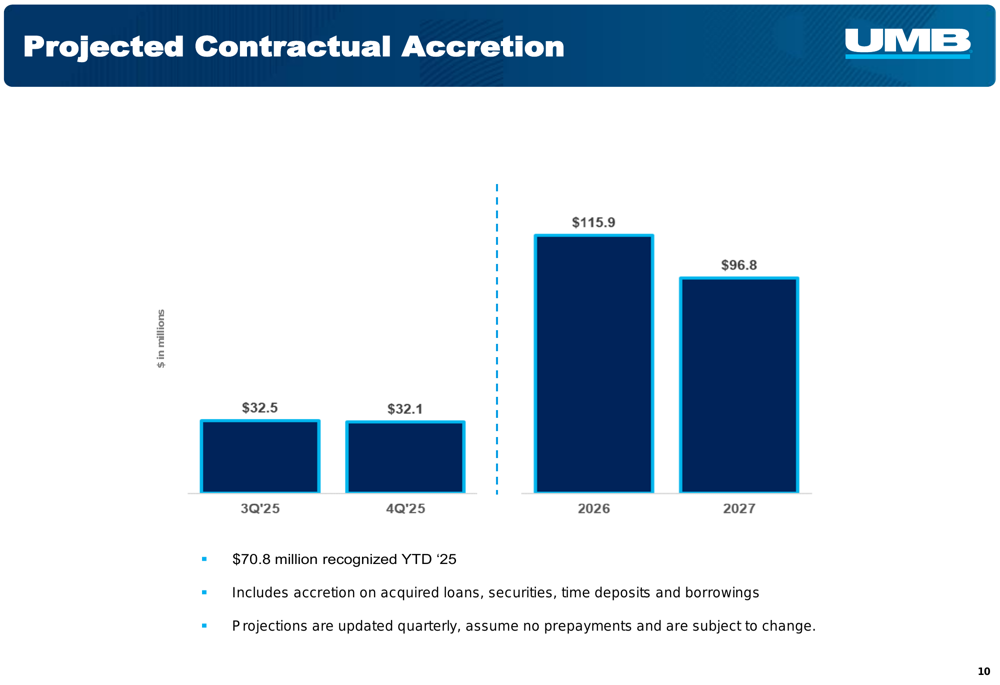

Looking forward, UMB expects to recognize substantial contractual accretion from the acquisition, with projected amounts of $32.5 million in Q3 2025, $32.1 million in Q4 2025, $115.9 million in 2026, and $96.8 million in 2027. These projections assume no prepayments and are subject to change.

As shown in the following chart of projected contractual accretion:

Balance Sheet and Credit Quality

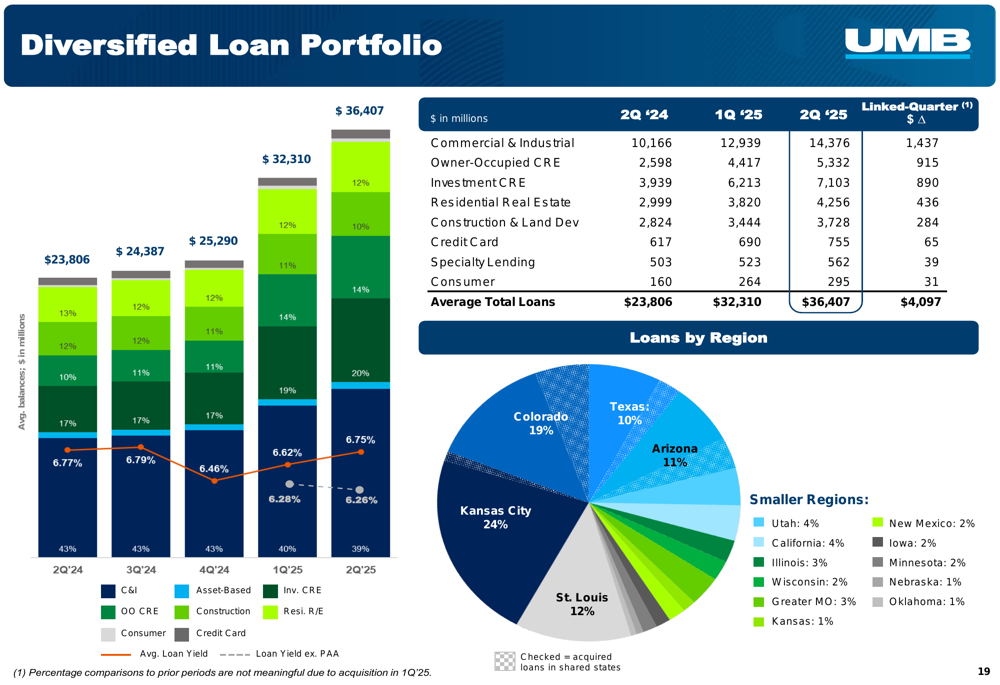

UMB’s balance sheet continued to strengthen in the second quarter, with average loans reaching $36.4 billion and end-of-period loans at $36.8 billion. Average total deposits were $55.6 billion, with end-of-period deposits of $60.0 billion.

The company’s loan portfolio remains well-diversified across industries and geographies, providing resilience against sector-specific downturns:

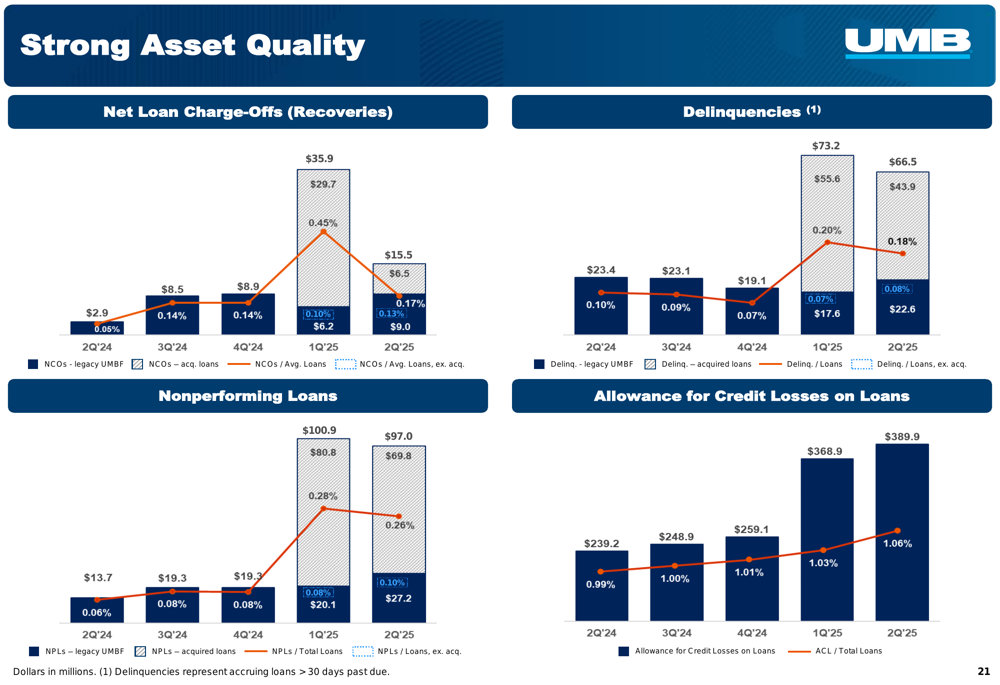

Asset quality metrics remain strong, with net charge-offs to average loans at 0.17% and nonperforming loans to total loans at 0.26%. The allowance for credit losses to total loans stood at 1.06%, reflecting the company’s prudent risk management approach.

The following chart illustrates UMB’s consistently strong asset quality metrics:

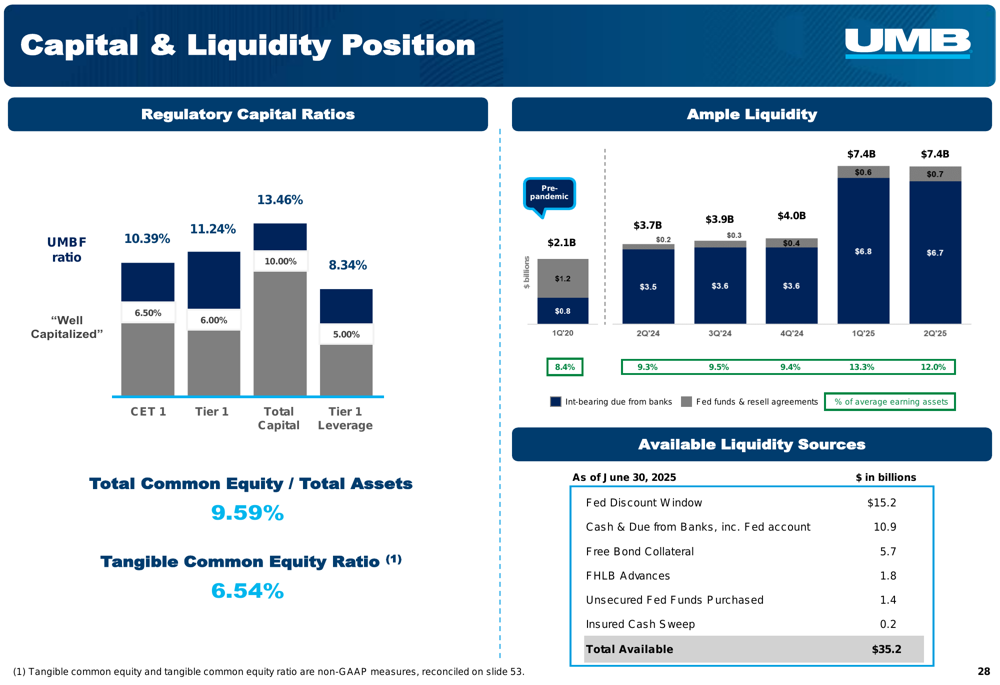

UMB maintains a solid capital position, with a Common Equity Tier 1 Capital Ratio of 10.39% and a Total Risk-Based Capital Ratio of 13.46%. The company’s available liquidity sources total $26.1 billion, providing ample flexibility to support continued growth.

The capital and liquidity position is detailed in the following slide:

Business Segment Performance

UMB’s diversified business model continues to drive performance across multiple segments. Commercial Banking, which includes middle market, investment real estate, and various lending verticals, represents a significant portion of the company’s loan portfolio. Commercial and Industrial (C&I) loans account for 40.1% of total loans, while Commercial Real Estate comprises another substantial portion.

Personal Banking services, including retail banking, private banking, mortgage, and community development, have shown strong growth with deposits up 78% and loans up 31%. The segment achieved a Net Promoter Score of 76.1, indicating high customer satisfaction.

Private Wealth Management reported $17.9 billion in managed assets (AUM) and $2.5 billion in non-managed assets. Institutional Banking services, including Fund Services and Institutional Custody, continue to expand with 78 new accounts and custody assets under administration growing 10.4% year-over-year.

The Payments division reported strong performance in credit and debit card products, with Q2 2025 card spend reaching $5.6 billion, up 19.1% year-over-year. UMB now ranks 22nd in U.S. credit card purchase volume.

Long-Term Performance Trends

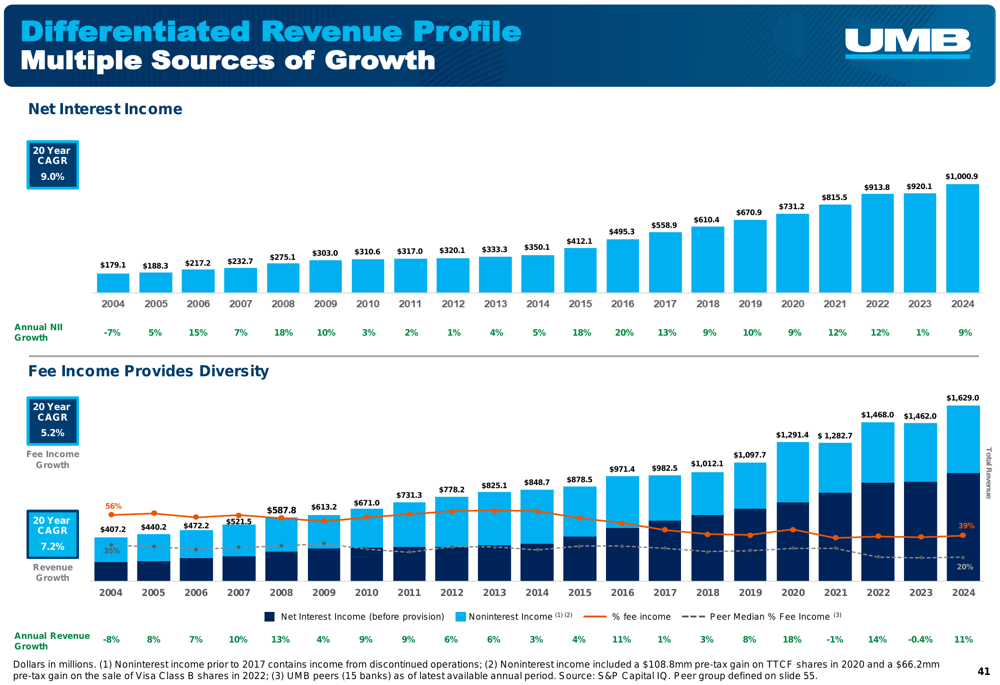

UMB’s long-term performance trends demonstrate consistent growth across key metrics. The company has achieved a 20-year compound annual growth rate (CAGR) of 9.0% for total revenue and 5.2% for fee income. Loan and deposit growth have been equally impressive, with 20-year CAGRs of 11.4% and 10.3%, respectively.

The company’s differentiated revenue profile, combining net interest income and noninterest income, has provided stability and growth over time:

UMB has also maintained a consistent dividend growth track record, with annual dividends declared for 2025 at $1.60 per share, representing a 1.9% increase from 2024.

Forward Outlook

UMB Financial appears well-positioned for continued growth, supported by its diversified business model, strong capital position, and the ongoing benefits from the HTLF acquisition. The company’s investment thesis emphasizes its diverse deposit base, track record of strong loan growth, flexible balance sheet, differentiated revenue profile, and time-tested underwriting philosophy.

Management highlighted that 51% of deposit accounts have been with the bank for more than 10 years, accounting for approximately 46% of deposit balances. This stability in core deposits provides a solid foundation for future growth.

While specific forward guidance was limited in the presentation, the projected contractual accretion from the HTLF acquisition suggests continued positive impact on earnings through 2027. The company’s strong capital and liquidity position also provides flexibility to pursue additional growth opportunities, whether organic or through further acquisitions.

As UMB continues to integrate the Heartland acquisition and leverage its diversified business model, investors will be watching closely to see if the company can maintain its momentum in the second half of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.