Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Unibail-Rodamco-Westfield (URW) presented its half-year 2025 results on July 31, highlighting continued operational improvements across its shopping center portfolio despite ongoing market challenges. The company’s presentation emphasized strong retail performance, strategic disposals, and continued deleveraging efforts as it progresses toward its long-term financial targets.

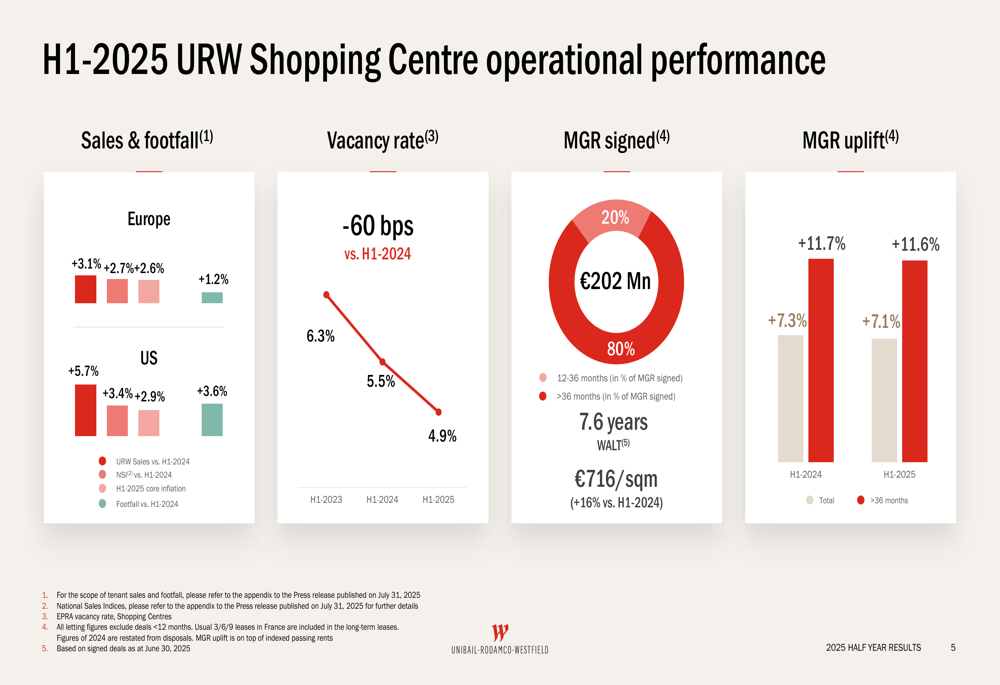

URW reported positive momentum in its core retail business with tenant sales up 3.8% and footfall increasing by 1.6% compared to the same period last year. This performance reflects the company’s focus on premium retail destinations and its ability to attract high-quality tenants despite the evolving retail landscape.

Quarterly Performance Highlights

The company delivered solid operational results across its portfolio, with particularly strong performance in its US assets. Key highlights include a 3.6% increase in like-for-like net rental income and a 4.1% rise in like-for-like EBITDA.

As shown in the following comprehensive overview of H1-2025 performance metrics:

URW’s leasing activity remained robust, with €202 million in minimum guaranteed rent (MGR) signed during the first half of 2025. The company achieved a positive MGR uplift of 7.1%, demonstrating its ability to increase rental rates despite challenging market conditions.

The vacancy rate continued to improve, reaching 4.9% in H1-2025 compared to 5.5% in H1-2024, reflecting the company’s successful leasing efforts and the quality of its assets. This improvement was consistent across most regions, with particularly strong performance in Southern Europe.

The following chart illustrates the company’s shopping center operational performance, showing improvements in key metrics across regions:

Detailed Financial Analysis

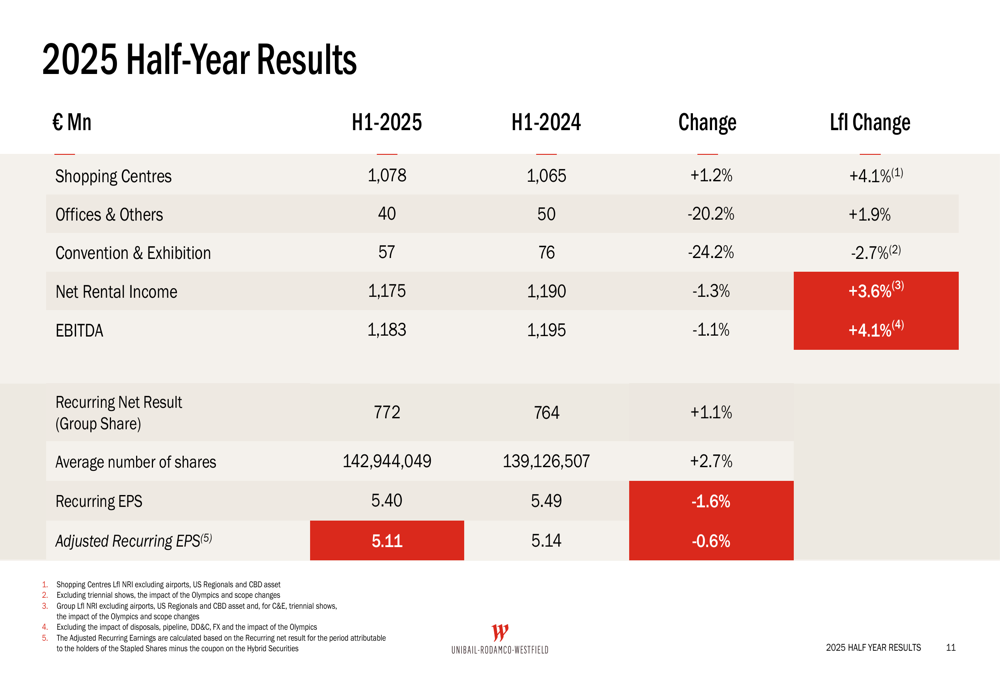

URW’s financial results for H1-2025 show a mixed picture, with some metrics affected by disposals while underlying operational performance remained strong. The company reported a recurring net result (group share) of €772 million, up 1.1% compared to H1-2024.

The following financial overview provides a comprehensive summary of the company’s H1-2025 results:

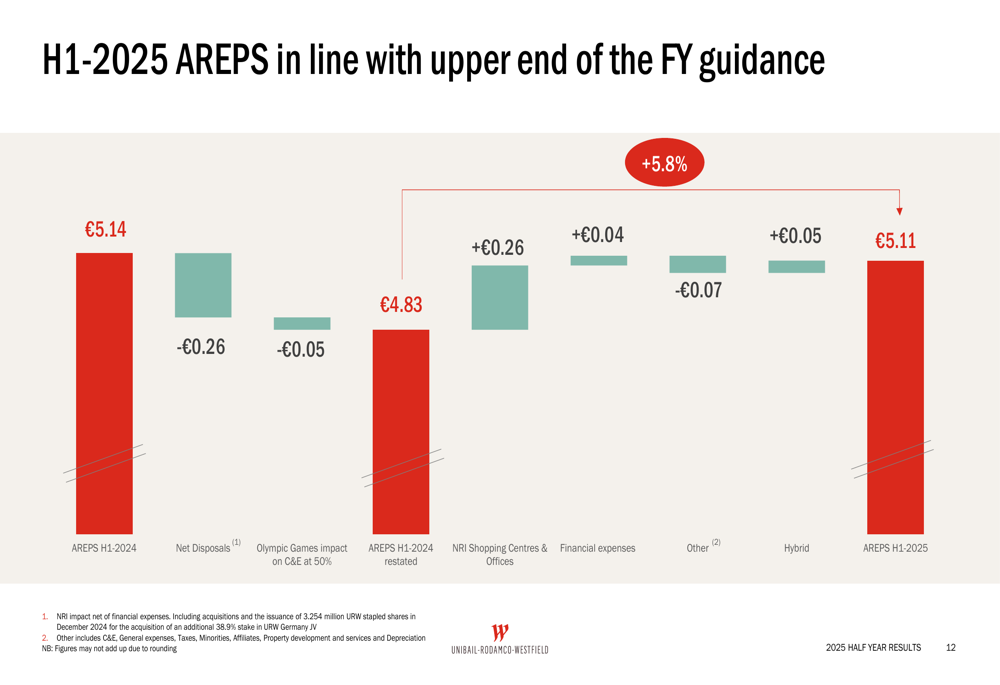

Adjusted Recurring Earnings Per Share (AREPS) was €5.11 in H1-2025, down slightly by 0.6% from €5.14 in H1-2024. However, when adjusting for disposals and the impact of the Olympic Games on the Convention & Exhibition business, AREPS increased by 5.8%, demonstrating the underlying strength of the core business.

The following chart breaks down the components contributing to the change in AREPS:

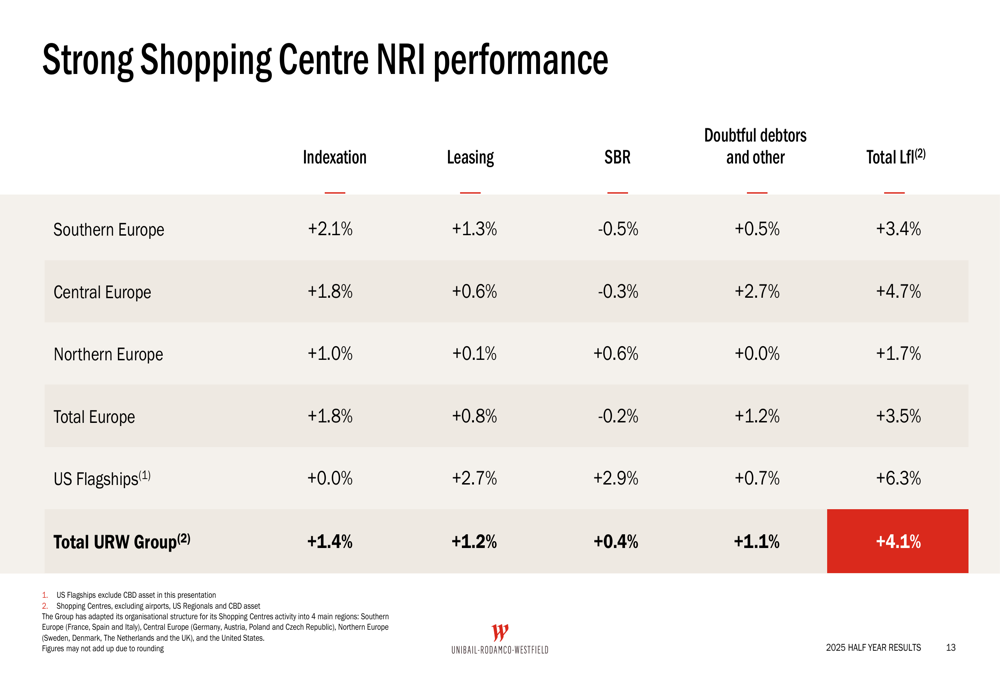

Regional performance varied, with US Flagships showing particularly strong results. Like-for-like NRI growth in the US reached 6.3%, driven by strong leasing activity (+2.7%) and higher sales-based rent (+2.9%). European shopping centers delivered a 3.5% like-for-like NRI growth, with Central Europe leading at 4.7%.

The following detailed breakdown illustrates the strong shopping center NRI performance by region:

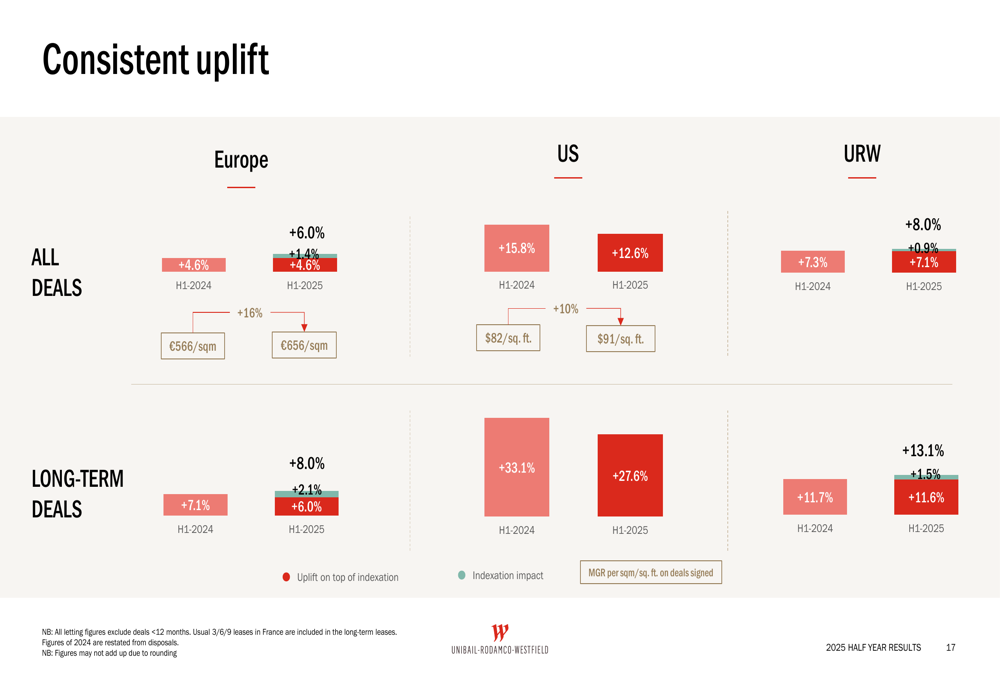

URW’s leasing activity continued to generate consistent rent uplifts across its portfolio. In H1-2025, the company achieved an 8.0% MGR uplift on all deals, with long-term deals delivering an 11.6% uplift. The US portfolio showed particularly strong performance with a 12.6% uplift on all deals and 27.6% on long-term deals.

As shown in the following chart of MGR performance:

Strategic Initiatives

URW continued to make progress on its deleveraging strategy, completing or securing €1.6 billion in disposals during H1-2025. These included the sale of a 15% stake in Westfield Forum des Halles in France, Bonaire in Spain, Stadshart Zoetermeer in the Netherlands, and an 80% stake in Trinity Tower in France. The company also secured agreements for the disposal of Pullman Paris Montparnasse and its US Airport business, subject to customary conditions.

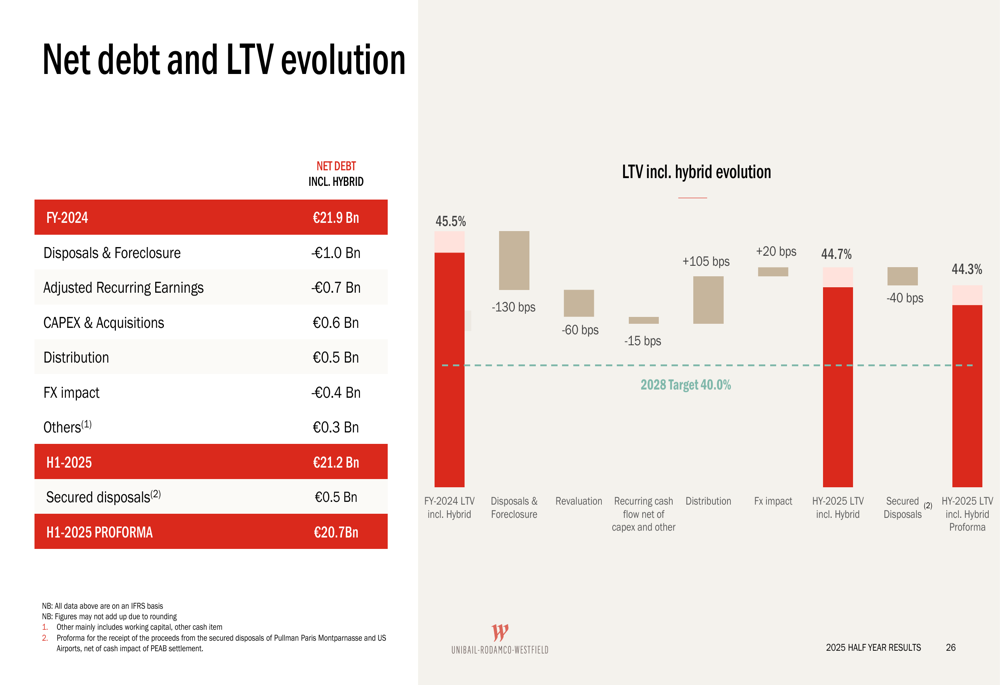

The company’s net debt decreased to €21.2 billion as of June 30, 2025, down from €21.9 billion at the end of 2024. This reduction, combined with improved operational performance, led to a decrease in the IFRS Loan-to-Value ratio from 45.5% at FY-2024 to 44.7% at H1-2025.

The following chart illustrates the evolution of the company’s net debt and LTV ratio:

URW also made significant progress in its financing activities, successfully refinancing $1.2 billion of US assets through CMBS at a 5.3% coupon, representing approximately 190 basis points of tightening compared to previous rates (5.3% vs. 7.2%). This refinancing included $925 million for Westfield Century City at a 5.27% 5-year CMBS and $275 million for Westfield Galleria at Roseville at a 5.59% 5-year CMBS.

The company continued to make progress on its environmental transition objectives, achieving an 85% reduction in GHG emissions (Scopes 1 & 2) against its 2030 target of 90%, and a 37% reduction in energy intensity against its 2030 target of 50%.

Forward-Looking Statements

Based on the strong H1-2025 performance, URW expects its full-year 2025 AREPS to be at the upper end of its guidance range of €9.30 to €9.50. The company remains focused on its strategic priorities, including enhancing the value of its core assets, reducing debt, and expanding its Westfield brand through licensing agreements.

URW launched its Westfield brand licensing business in May 2025, signing a partnership with Cenomi Centers in Saudi Arabia. Under this agreement, up to eight flagship centers will be Westfield-branded, with three centers expected to be rebranded by H2-2026 in Dammam, Jeddah, and Riyadh.

The company also highlighted the successful opening of Westfield Hamburg-Überseequartier in April 2025, which has attracted approximately 4 million visits since its opening. The retail portion of the project is 95% let, with 83% already open, featuring 170 units including over 40 food and dining concepts.

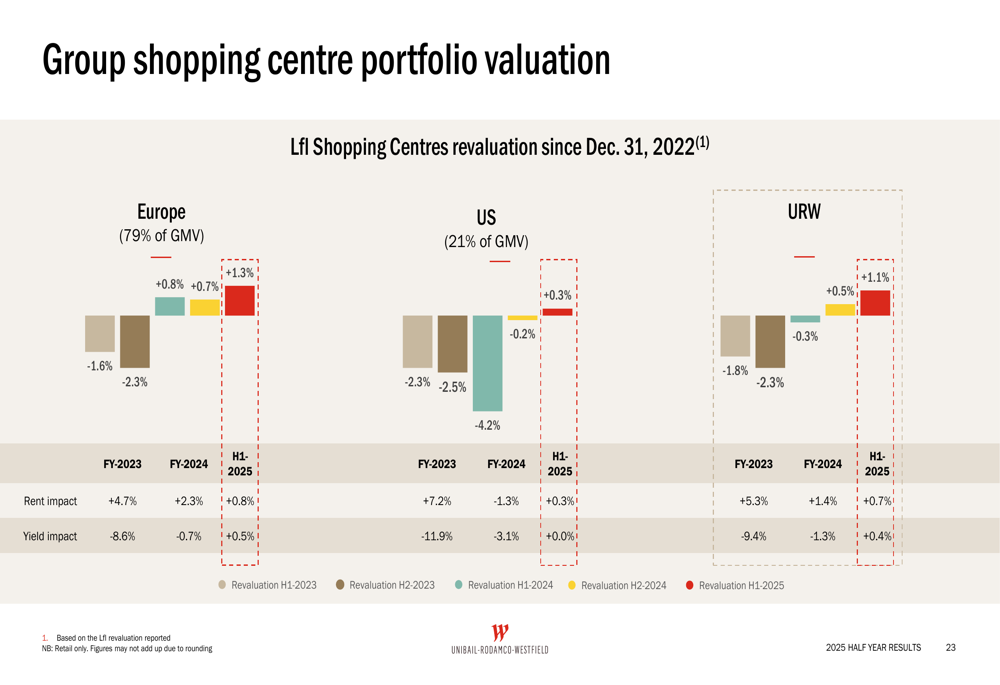

URW’s portfolio valuation increased by 1.2% in H1-2025, indicating market confidence in the quality of its assets despite challenging market conditions. The company’s shopping center portfolio valuation is supported by continued cash flow growth, with a net initial yield of 5.4% in Europe and 5.1% in US Flagships.

The following chart shows the evolution of the group’s shopping center portfolio valuation:

URW continues to make progress toward its long-term financial targets, with its IFRS Net Debt to EBITDA ratio improving to 9.2x from 9.5x at the end of 2024. The company aims to reduce this ratio to 9.0x by the end of 2025 and to 8.0x by 2028.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.