Japan PPI inflation slips to 11-mth low in July

Introduction & Market Context

Unicaja Banco SA (BME:UNI) delivered a strong start to 2025, with its first-quarter results showing significant improvement in profitability metrics despite challenges in the interest rate environment. The Spanish bank’s stock has been performing well, with shares trading at €2.108 as of July 28, 2025, up 2.12% and approaching its 52-week high of €2.124.

The bank’s Q1 2025 presentation highlighted substantial progress across key performance indicators, with net profit growth, improved asset quality, and strong capital ratios forming the cornerstone of its financial narrative. These results come amid a favorable Spanish economic backdrop, which has supported lending activity and asset quality metrics.

Quarterly Performance Highlights

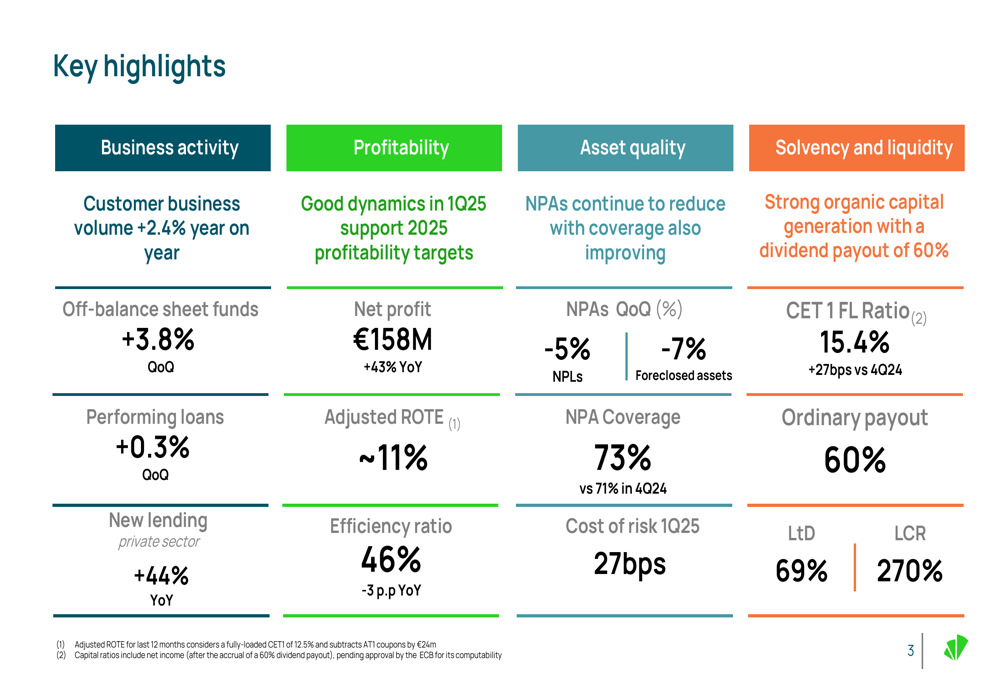

Unicaja Banco reported a significant improvement in its financial performance for Q1 2025, with net profit reaching €158 million, representing a 43% increase compared to the same period last year. This growth was driven by resilient net interest income, improved business activity, and changes in the banking tax accounting.

As shown in the following key highlights from the presentation:

The bank’s adjusted Return on Tangible Equity (ROTE) reached approximately 11%, compared to 6% in Q1 2024, demonstrating a substantial improvement in profitability. The efficiency ratio improved to 46%, down 3 percentage points year-on-year, reflecting better cost management despite a 4.4% increase in operating expenses.

Customer business volumes increased by 2.4% year-on-year, with off-balance sheet funds growing by 3.8% quarter-on-quarter and performing loans increasing by 0.3% quarter-on-quarter. New lending in the private sector showed particularly strong momentum, increasing by 44% year-on-year.

Detailed Financial Analysis

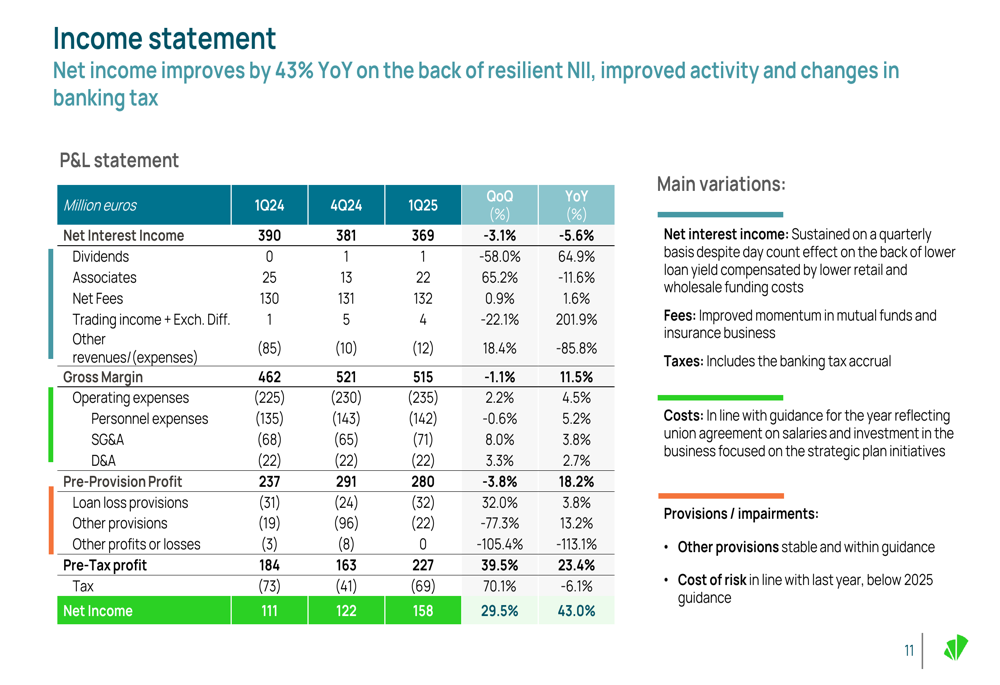

The bank’s income statement reveals the drivers behind the improved profitability, with a resilient net interest income despite the challenging interest rate environment, improved fee income, and better control of operating expenses.

As shown in the comprehensive income statement:

Net interest income (NII) was €369 million in Q1 2025, compared to €390 million in Q1 2024 and €381 million in Q4 2024. The quarter-on-quarter decline was primarily due to lower loan yields, partially offset by lower deposit costs and wholesale funding expenses.

Fee income showed a slight improvement, reaching €132 million in Q1 2025 compared to €130 million in Q1 2024. The bank highlighted a shift in the fee income mix toward higher value-added products for customers, with mutual fund fees increasing from €31 million to €36 million year-on-year.

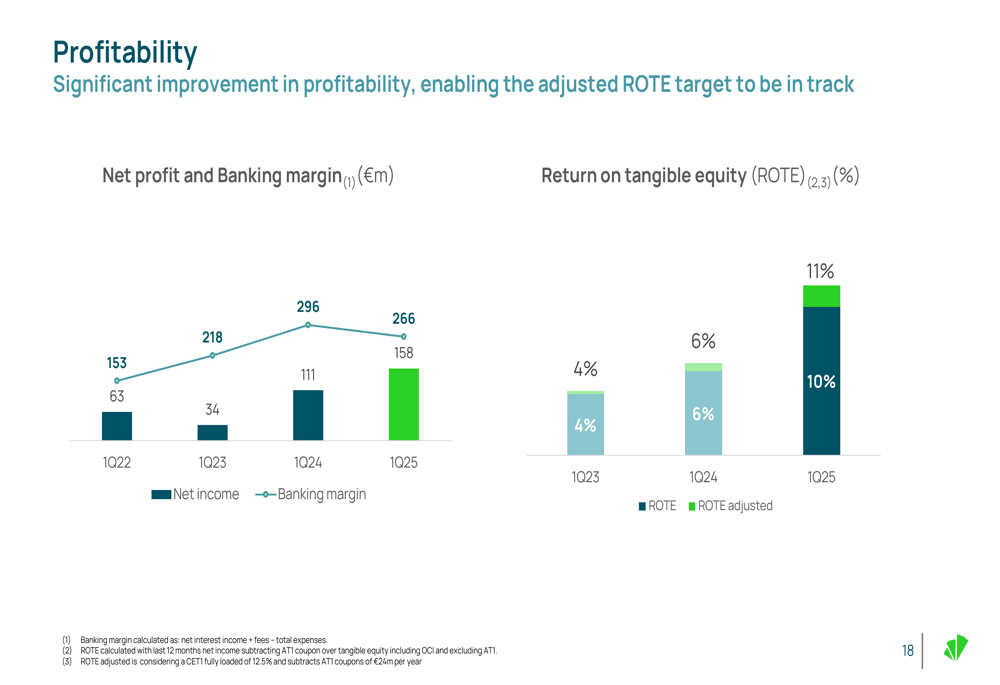

The bank’s profitability metrics showed significant improvement, with the adjusted ROTE reaching approximately 11% in Q1 2025, compared to 10% in Q1 2024.

As illustrated in the following profitability chart:

Asset Quality Improvements

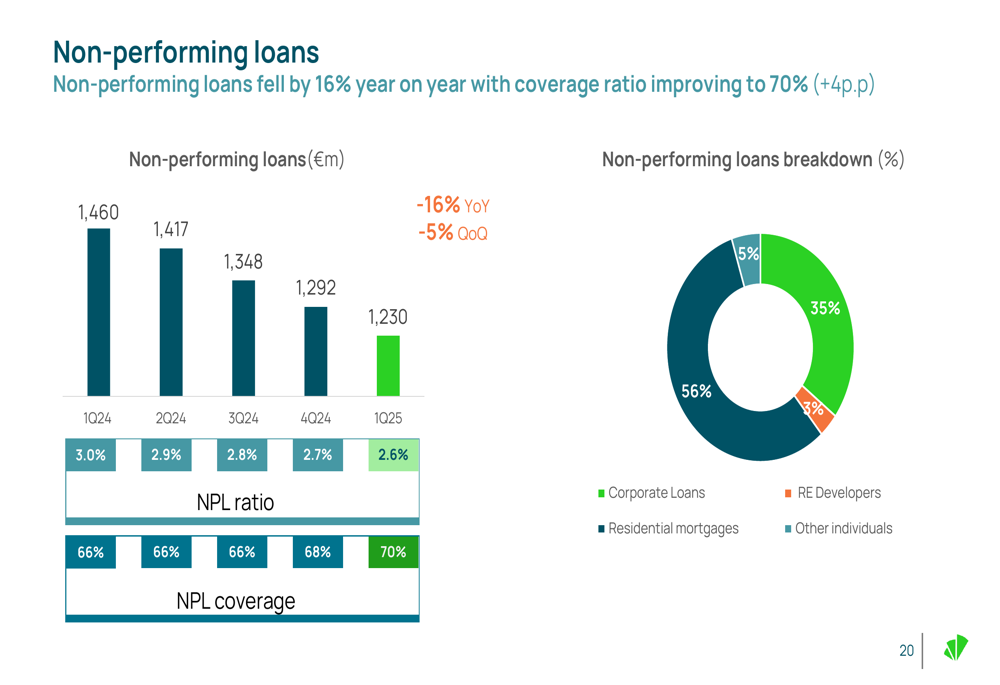

Unicaja Banco made substantial progress in improving its asset quality metrics during the quarter, with non-performing loans (NPLs) decreasing by 16% year-on-year and the NPL ratio improving to 2.6% from 3.0% in Q1 2024.

The following chart illustrates the improvement in non-performing loans:

The NPL coverage ratio improved to 70% in Q1 2025, up from 66% in Q1 2024, providing additional protection against potential loan losses. Total (EPA:TTEF) non-performing assets (NPAs) decreased by 22% year-on-year, with foreclosed assets declining by 30% over the same period.

The cost of risk remained stable at 27 basis points in Q1 2025, in line with the bank’s guidance of approximately 30 basis points for the full year 2025.

Capital Position and Shareholder Returns

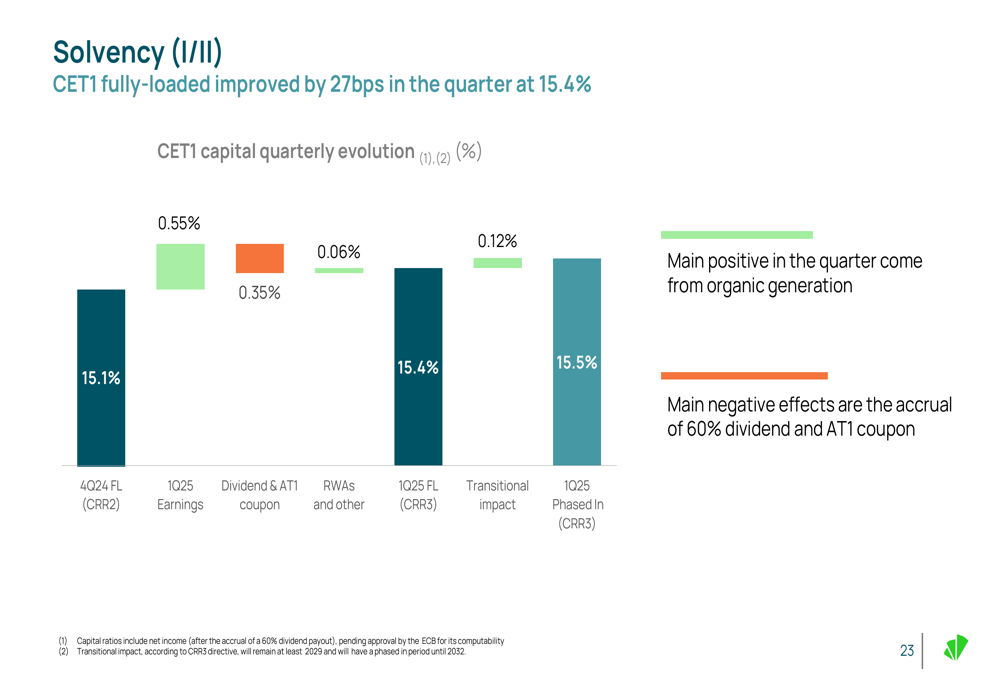

Unicaja Banco maintained a strong capital position, with its CET1 fully-loaded ratio improving by 27 basis points in the quarter to 15.4%. This improvement was primarily driven by organic capital generation through earnings, partially offset by dividend accrual and AT1 coupon payments.

The following chart shows the evolution of the bank’s CET1 ratio:

The bank’s strong capital position supports its increased shareholder remuneration, with an ordinary payout ratio of 60%. Unicaja Banco also maintains excellent liquidity metrics, with a loan-to-deposit ratio of 69% and a liquidity coverage ratio (LCR) of 270%.

Forward-Looking Statements

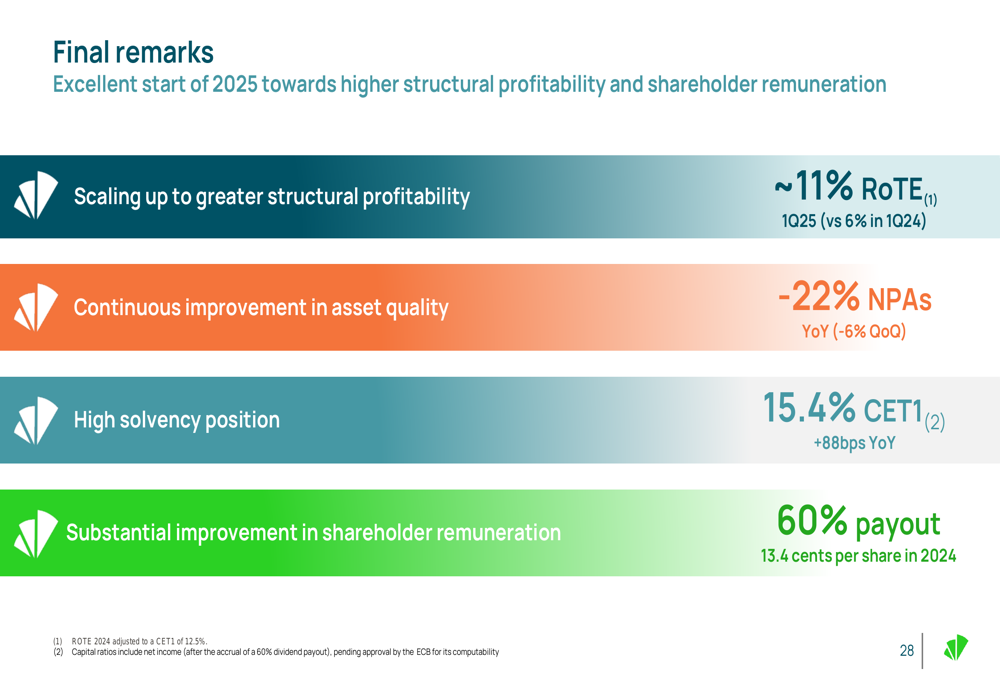

Unicaja Banco reiterated its guidance for 2025, targeting net interest income of more than €1,400 million, flat fee income, cost growth of approximately 5%, and a cost of risk of around 30 basis points. The bank aims to achieve a ROTE of 12.5% for the full year.

As summarized in the final remarks of the presentation:

The bank’s strategic focus remains on scaling up structural profitability, continuing to improve asset quality, maintaining a strong solvency position, and enhancing shareholder remuneration. Unicaja Banco also highlighted its commitment to ESG initiatives, with green bonds avoiding 81,000 tons of CO2 in 2024 (a 48% increase versus 2023) and 30% of new lending to corporates in Q1 2025 being sustainable.

Looking ahead, Unicaja Banco is well-positioned to continue its positive trajectory, with a strong capital position, improving asset quality, and a clear strategic focus on enhancing profitability and shareholder returns. The bank’s performance in Q1 2025 represents an excellent start toward achieving its full-year targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.