Street Calls of the Week

Introduction & Market Context

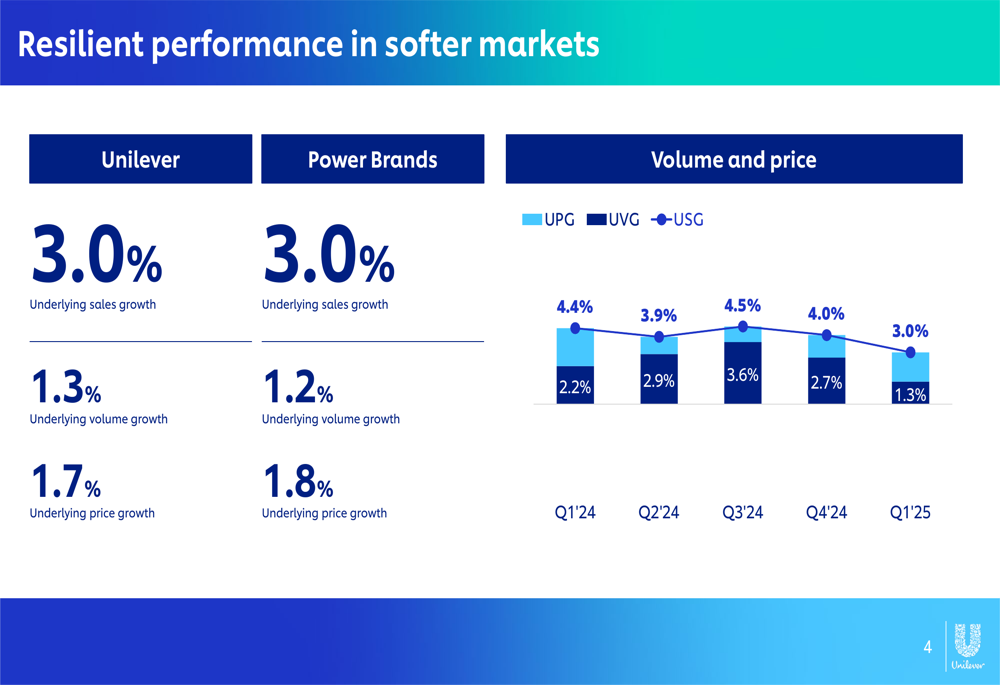

Unilever PLC (LSE:LON:ULVR) reported underlying sales growth of 3.0% in its Q1 2025 trading statement presented on April 24, 2025. The consumer goods giant achieved this growth through a combination of volume growth (1.3%) and price growth (1.7%), demonstrating resilience in what the company described as "softer markets" with heightened macroeconomic uncertainty.

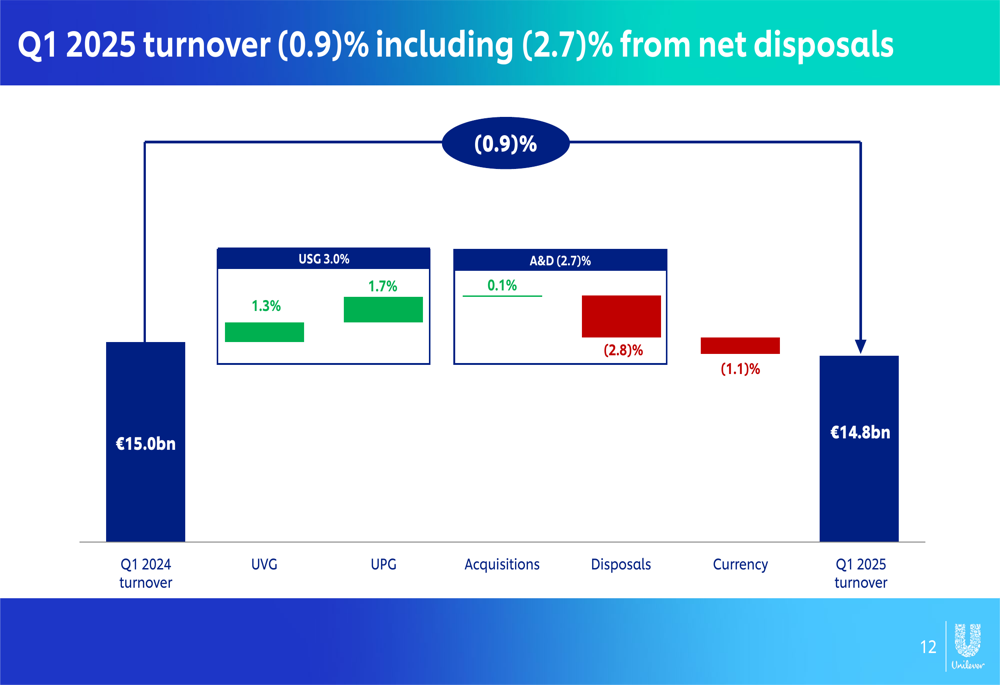

The company’s overall turnover declined by 0.9% to €14.8 billion, primarily due to disposals (-2.8%) and currency effects (-1.1%), while underlying growth and acquisitions made positive contributions.

As shown in the following turnover bridge chart, Unilever’s volume growth has continued to recover while price growth has moderated compared to previous quarters:

Quarterly Performance Highlights

Unilever’s performance showed significant variation across business segments and regions, with Personal Care leading growth at 5.1% while Home Care lagged at just 0.9%. The company emphasized its focus on "Power Brands," which matched the overall company’s underlying sales growth of 3.0%.

The following chart illustrates Unilever’s resilient performance metrics for Q1 2025:

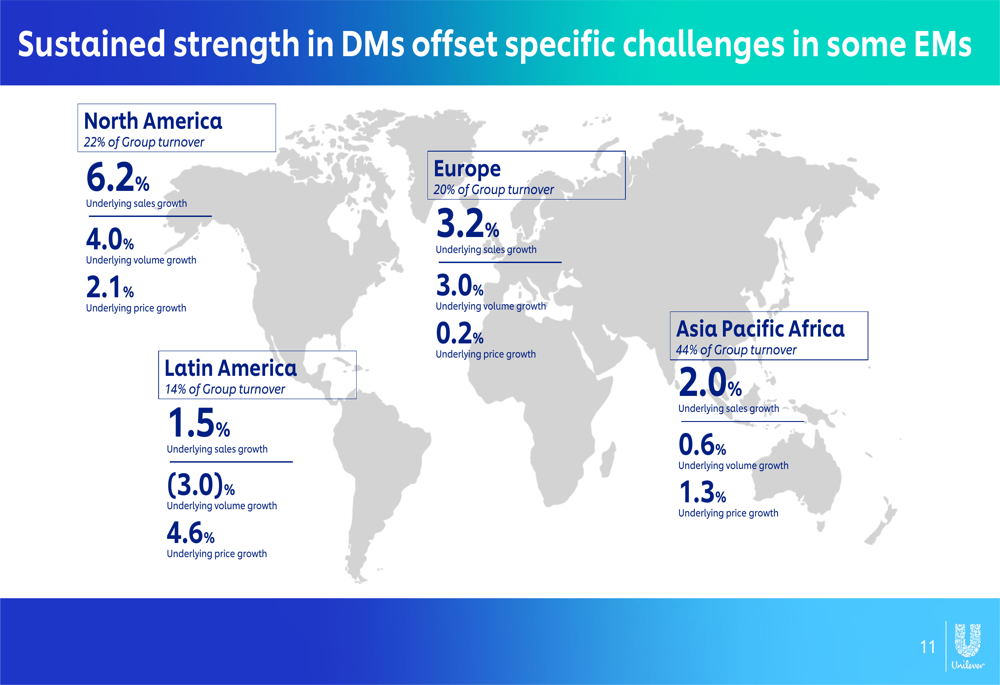

Regional performance revealed North America as the standout performer with 6.2% underlying sales growth, driven by strong volume growth of 4.0%. Europe followed with 3.2% growth, while Latin America struggled with a 3.0% volume decline despite price growth of 4.6%.

The company’s global performance by region is visualized in this map:

Segment and Regional Analysis

Beauty & Wellbeing delivered 4.1% underlying sales growth with 2.5% volume growth. Strong performance from Dove led the way in Core Skin Care and Hair Care, while Wellbeing products like Liquid IV and Nutrafol achieved double-digit growth. However, Prestige Beauty declined due to market slowdowns in the US and China.

Personal Care emerged as the strongest segment with 5.1% underlying sales growth. Dove continued its success with high-single-digit growth driven by premium innovations. The company also highlighted its acquisition of Wild, which further enhances its Personal Care portfolio.

Home Care was the weakest performer with just 0.9% underlying sales growth, facing challenges in Latin America. The company noted it was "navigating challenging macroeconomic conditions" in the region, though Europe outperformed markets driven by Persil and Comfort innovations.

Foods achieved 1.6% underlying sales growth despite a 1.1% volume decline. Knorr and Hellmann’s performed well in retail, supported by innovations enabling higher pricing. However, Unilever Food Solutions was flat as China lapped double-digit growth from the previous year, and India Foods was impacted by weak Horlicks performance.

Ice Cream delivered solid 4.0% underlying sales growth with 1.8% volume growth. Magnum grew mid-single digit with its new Utopia range, while Ben & Jerry’s also grew mid-single digit, supported by a new larger shareable size and new Sundae flavors.

Ice Cream Separation Update

Unilever confirmed that the planned separation of its Ice Cream business remains on track to complete by the end of 2025. The separation will be executed as a demerger with listings in Amsterdam, London, and New York.

The company provided this timeline for the separation:

- Operational separation of the business by July 1, 2025

- Ice Cream business to be reported as a discontinued operation from Q4

- Capital Markets Day scheduled for September 9, 2025

This strategic move will allow Unilever to focus on its core businesses while enabling the Ice Cream division to pursue its own growth strategy independently.

Financial Outlook and Guidance

Unilever reconfirmed its full-year 2025 financial outlook, projecting underlying sales growth within its target range of 3-5% and modest improvement in underlying operating margin. The company noted that margins in the first and second half of the year will be more balanced than in 2024.

As shown in the financial outlook slide:

Additional financial guidance for 2025 includes:

- Capital expenditure above 3% of turnover

- Restructuring costs around 1.4% of turnover

- Net finance costs around 3% on average net debt

- Underlying effective tax rate around 26%

- Leverage of approximately 2x net debt to underlying EBITDA

- Currency impact on full-year results expected to be around -3% to -5% on turnover and approximately -20 basis points on underlying operating margin

Risks and Opportunities

Unilever identified several factors providing confidence in its outlook, including its resilient and diversified portfolio, strong innovation pipeline, stepped-up execution, limited direct tariff exposure, and targeted actions in challenged markets.

However, the company also acknowledged significant risks, including potential macroeconomic deterioration, worsening consumer sentiment, and heightened commodity cost and foreign exchange volatility.

The following slide outlines these factors:

The company’s unwavering priority remains driving growth, with continued investment behind its strongest growth opportunities. Quality of innovation is driving outperformance in developed markets, while targeted and decisive action is being taken in select emerging markets facing challenges.

With its diverse portfolio and strategic focus on Power Brands, Unilever appears positioned to navigate market volatility, though macroeconomic headwinds and regional challenges, particularly in Latin America and parts of Asia, remain areas to watch in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.