Figma Shares Indicated To Open $105/$110

Introduction & Market Context

United Internet AG (ETR:UTDI) presented its Q1 2025 financial results on May 12, 2025, revealing a mixed performance across its business segments. The company reported modest revenue growth but flat EBITDA, as strong performance in Business Applications was offset by increased investment costs in its mobile network rollout. Despite these challenges, United Internet upgraded its full-year revenue guidance, signaling confidence in its strategic direction.

The company’s stock has shown resilience in recent months, trading at €21.04 as of May 9, 2025, up 1.25% on the day and continuing a recovery trend after reaching a 52-week low of €14.58.

Quarterly Performance Highlights

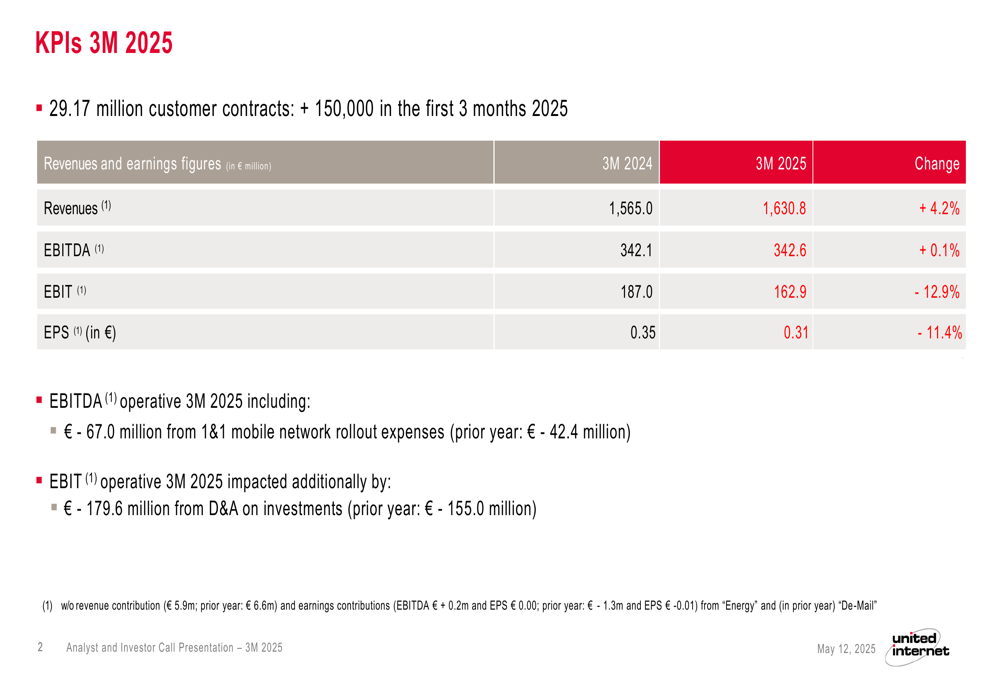

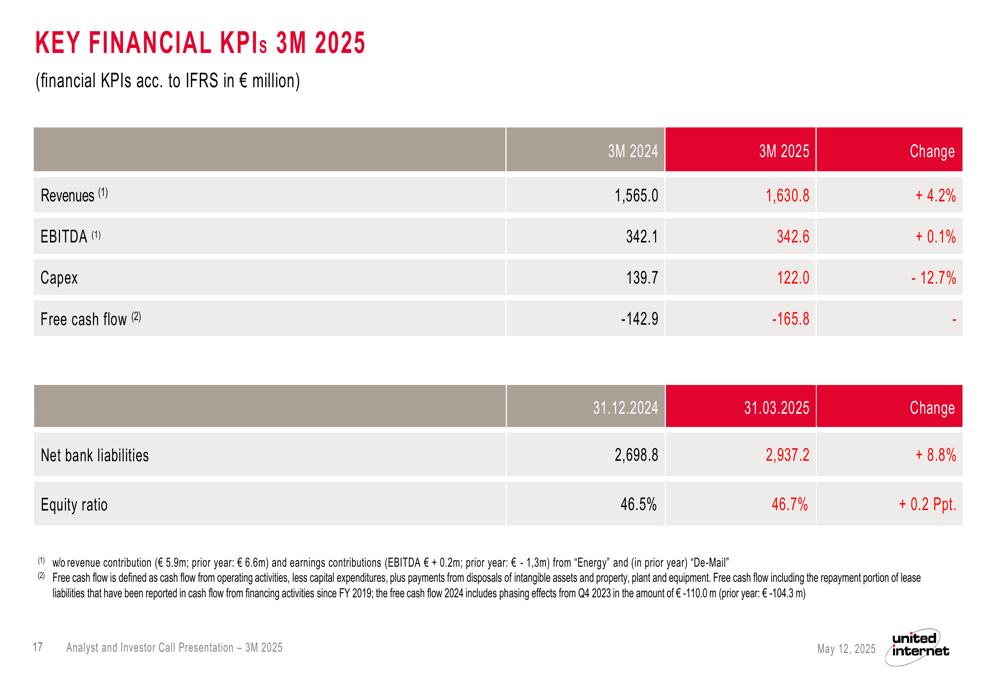

United Internet reported Q1 2025 revenue of €1,630.8 million, representing a 4.2% increase from €1,565.0 million in the same period last year. However, EBITDA remained essentially flat at €342.6 million, up just 0.1% year-over-year, while EBIT declined by 12.9% to €162.9 million. Earnings per share also fell by 11.4% to €0.31.

As shown in the following comprehensive overview of key performance indicators:

The company’s customer base continued to grow, reaching 29.17 million contracts, an increase of 150,000 in the first quarter of 2025. However, this growth was uneven across segments, with Consumer Access experiencing a decline of 40,000 contracts while Business Applications added 110,000 new contracts.

Segment Analysis

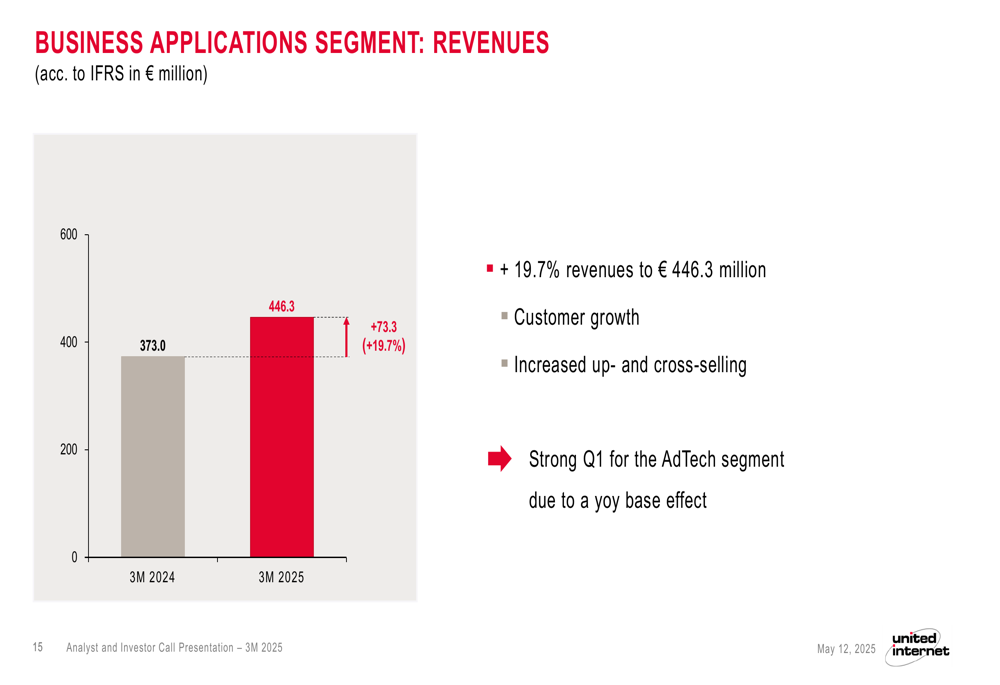

The Business Applications segment emerged as the standout performer in Q1 2025, with revenues surging 19.7% to €446.3 million. This growth was driven by customer acquisition, increased up-selling and cross-selling, and a strong performance in the AdTech segment due to a year-over-year base effect.

The segment’s impressive revenue growth is illustrated in this chart:

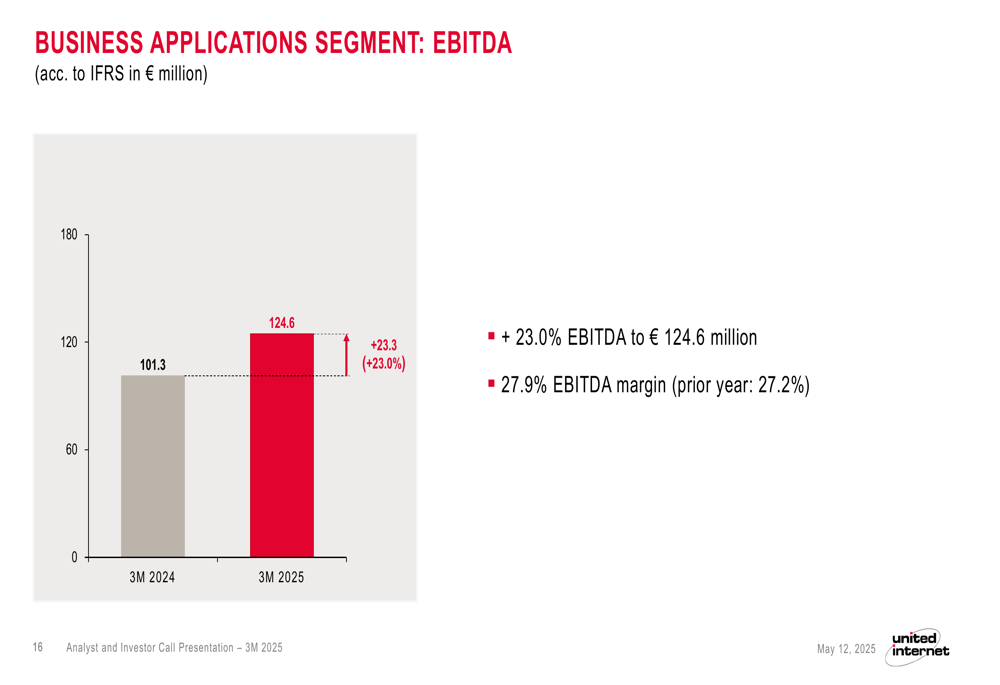

This robust revenue performance translated into strong EBITDA growth of 23.0% to €124.6 million, with an improved EBITDA margin of 27.9% compared to 27.2% in the prior year:

In contrast, the Consumer Access segment faced challenges, with revenues declining by 0.6% to €1,018.5 million. While service revenues remained stable at €821.9 million, other revenues (particularly low-margin smartphones) decreased by 2.9% to €196.6 million.

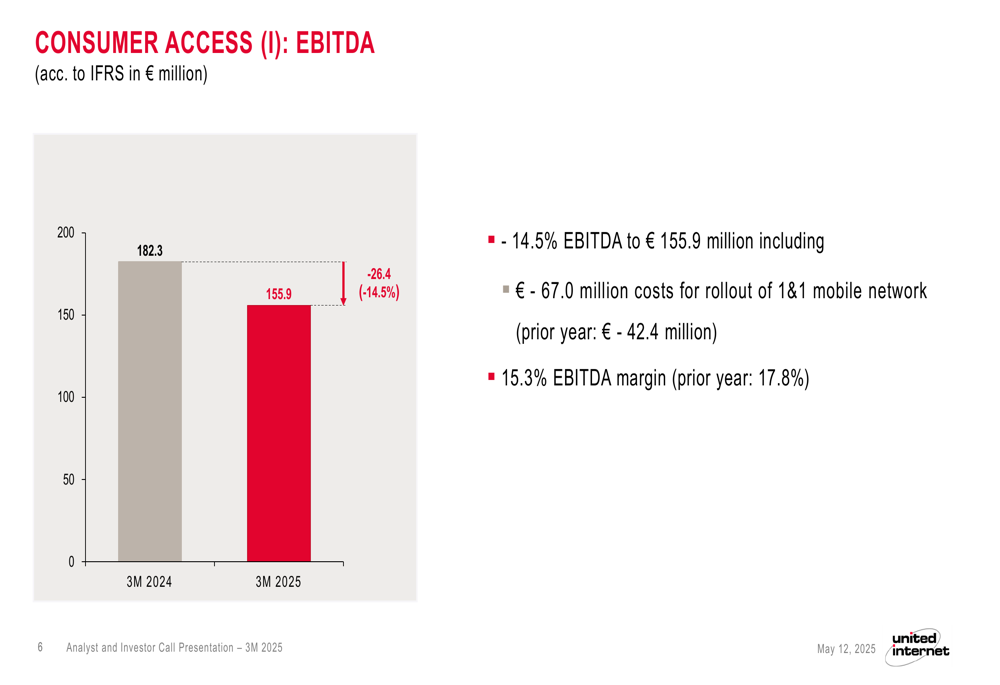

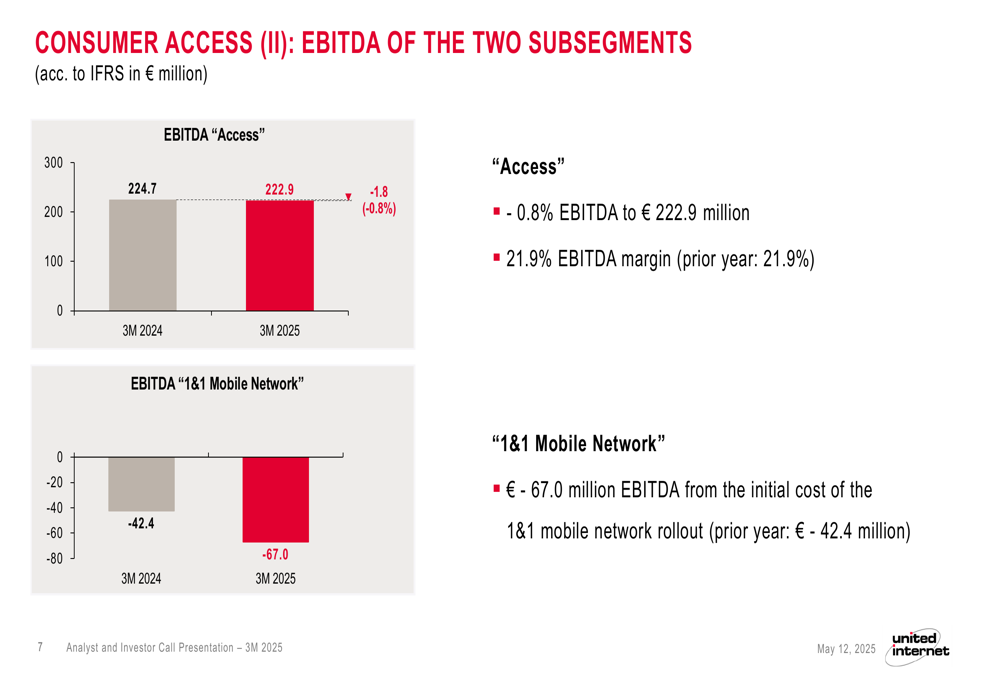

More significantly, the segment’s EBITDA fell by 14.5% to €155.9 million, primarily due to increased costs associated with the 1&1 mobile network rollout:

A deeper analysis of the Consumer Access segment reveals that while the core "Access" business maintained relatively stable EBITDA (€222.9 million, down just 0.8%), the 1&1 Mobile Network subsegment reported negative EBITDA of -€67.0 million, compared to -€42.4 million in the prior year:

Financial Position

United Internet’s capital expenditure (Capex) decreased by 12.7% to €122.0 million in Q1 2025. However, free cash flow remained negative at -€165.8 million, compared to -€142.9 million in the same period last year. Net bank liabilities increased by 8.8% to €2,937.2 million as of March 31, 2025, while the equity ratio slightly improved to 46.7%.

The following table summarizes these key financial metrics:

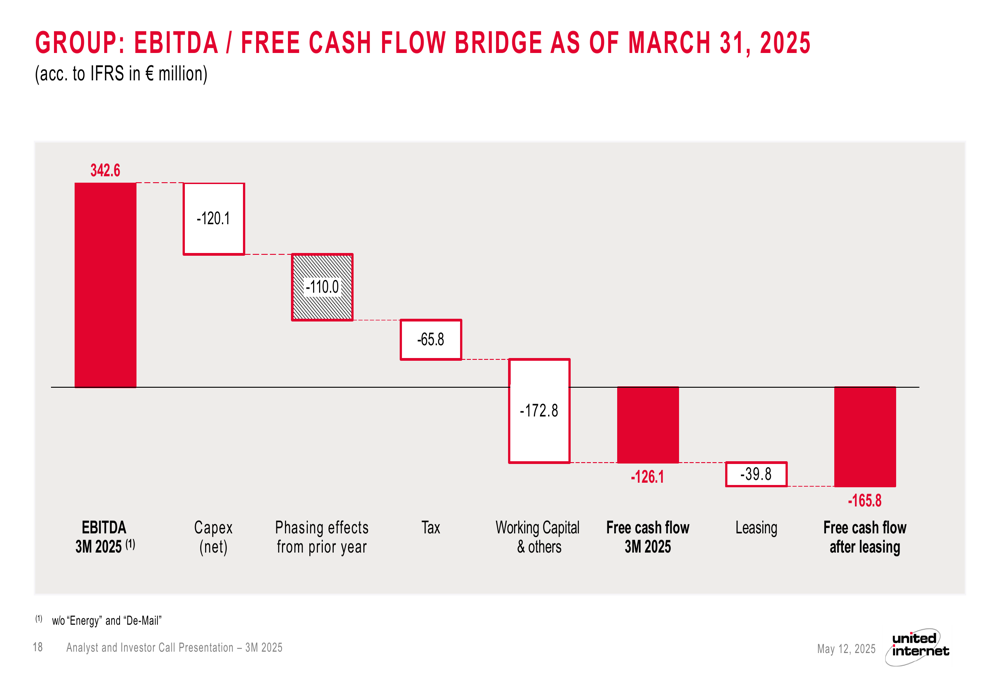

The company provided a detailed bridge from EBITDA to free cash flow, highlighting the various factors impacting cash generation:

Working capital changes and phasing effects from the prior year were significant drags on cash flow, contributing -€172.8 million and -€110.0 million respectively. These factors, combined with capital expenditures and tax payments, resulted in the negative free cash flow position.

Forward-Looking Statements

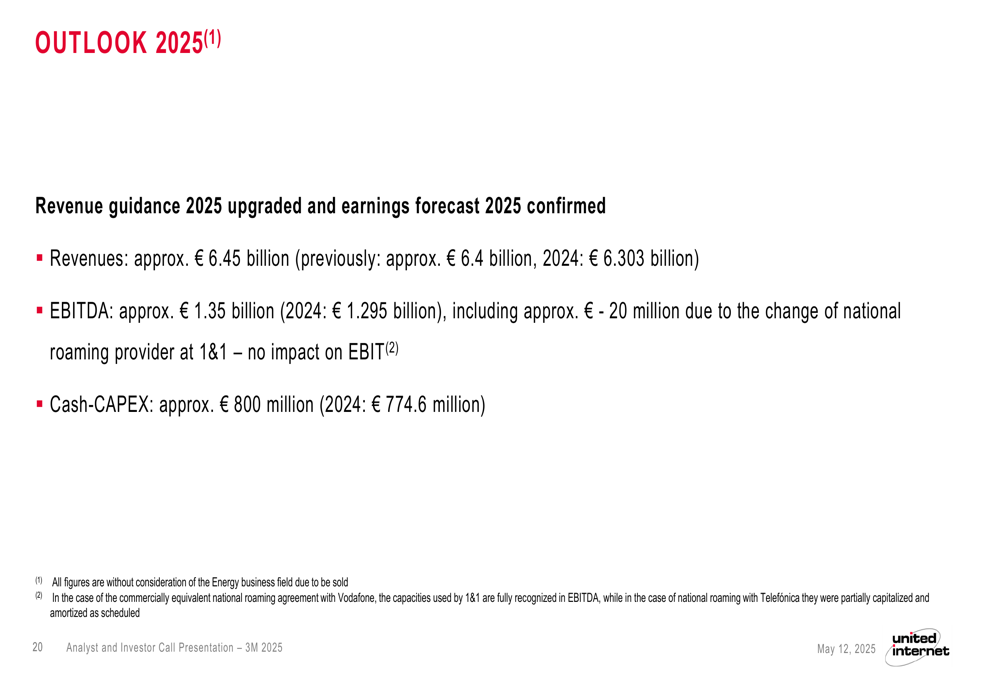

Despite the mixed Q1 results, United Internet upgraded its revenue guidance for 2025 to approximately €6.45 billion, up from the previous forecast of €6.4 billion. The company maintained its EBITDA guidance at approximately €1.35 billion, which includes an expected €20 million impact from changing national roaming providers at 1&1.

The detailed outlook is presented here:

The company plans to invest approximately €800 million in capital expenditures during 2025, slightly higher than the €774.6 million spent in 2024. This continued investment underscores United Internet’s commitment to expanding its network infrastructure and digital capabilities.

Strategic Initiatives

United Internet’s strategic focus remains on expanding its digital solutions portfolio and network infrastructure. The ongoing rollout of the 1&1 mobile network represents a significant investment that is currently weighing on profitability but is positioned as a long-term growth driver.

The company is also experiencing strong momentum in its Business Applications segment, with customer growth both domestically and internationally. As of March 31, 2025, this segment had 9.70 million customer contracts, with 5.03 million abroad and 4.67 million in Germany.

Conclusion

United Internet’s Q1 2025 results present a nuanced picture for investors. While overall revenue growth is positive and the Business Applications segment is performing exceptionally well, the costs associated with the 1&1 mobile network rollout continue to pressure profitability. The upgraded revenue guidance suggests management confidence in the company’s trajectory, but investors will likely focus on whether the significant investments in network infrastructure will deliver the expected returns in the medium to long term.

With a stable equity ratio and clear strategic direction, United Internet appears positioned to navigate the current investment phase, though the widening negative free cash flow and increasing net bank liabilities bear monitoring in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.