Park Ha Biological Technology stock rises on upcoming ticker symbol change

U.S. Bancorp (NYSE:USB) delivered strong third-quarter results for 2025, with significant growth in earnings per share and fee revenue, according to its earnings presentation released on October 16. The bank’s stock rose 1.72% in pre-market trading to $47.25, reflecting investor optimism about the results.

Quarterly Performance Highlights

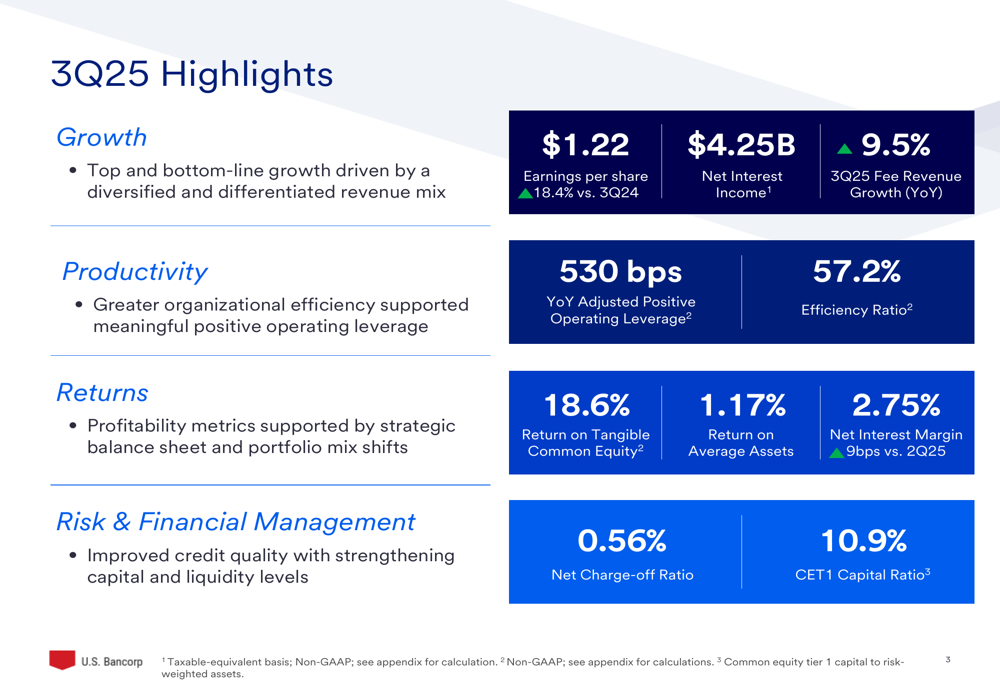

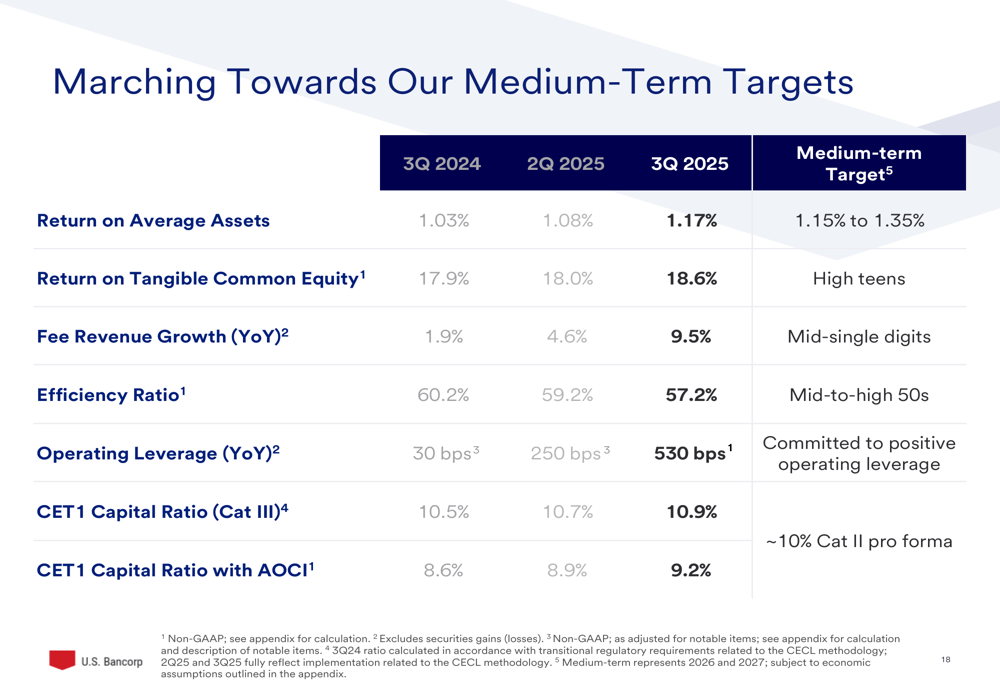

The banking giant reported earnings per share of $1.22, representing an 18.4% increase compared to the third quarter of 2024. This exceeded analysts’ expectations of $1.12 per share, marking an 8.93% positive surprise. The bank achieved a return on tangible common equity of 18.6%, up from 17.9% a year earlier, while return on average assets improved to 1.17% from 1.03% in the same period last year.

As shown in the following summary of key performance metrics, U.S. Bancorp demonstrated improvements across multiple financial indicators:

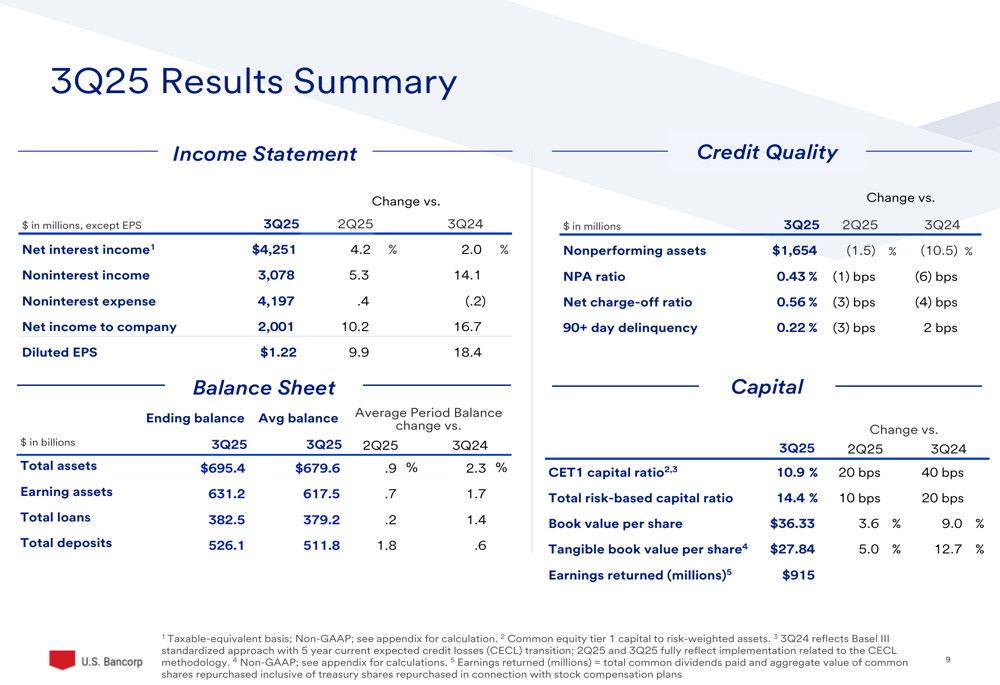

Net interest income reached $4.25 billion, representing a 4.2% increase compared to the previous quarter and a 2.0% increase year-over-year. The bank’s net interest margin expanded to 2.75%, a 9 basis point improvement from the second quarter of 2025, reflecting the bank’s ability to manage its balance sheet effectively in the current interest rate environment.

The efficiency ratio improved to 57.2% from 60.2% a year earlier, demonstrating the bank’s success in controlling expenses while growing revenue. This improvement contributed to a positive operating leverage of 530 basis points year-over-year.

Revenue and Fee Income Growth

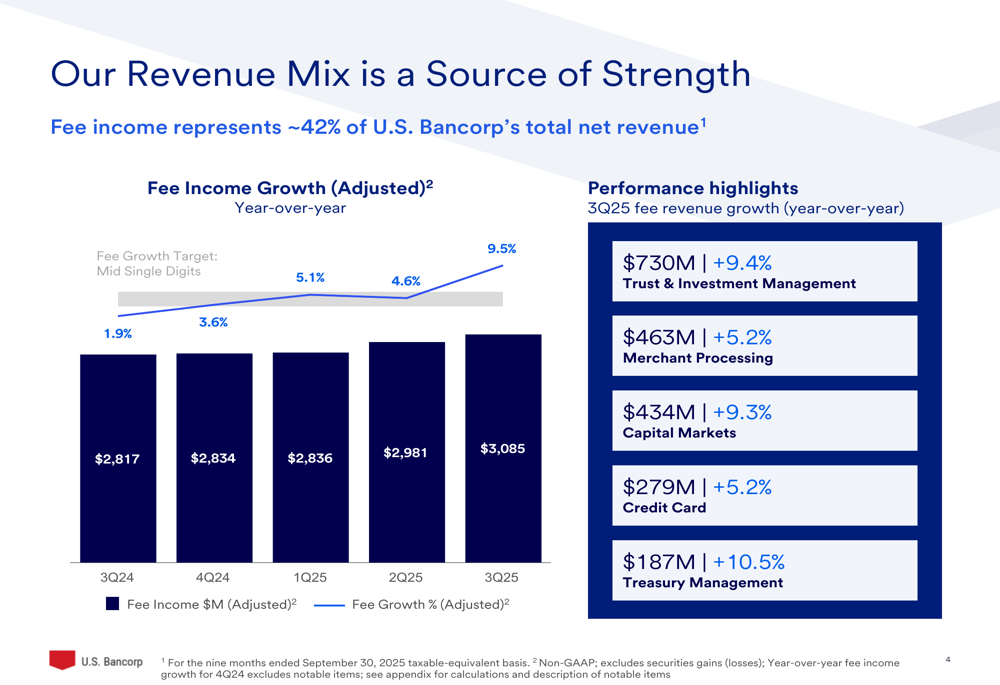

Fee income continues to be a significant driver of U.S. Bancorp’s revenue, representing approximately 42% of total net revenue. The bank reported fee income growth of 9.5% compared to the third quarter of 2024, reaching $3.085 billion.

The following chart illustrates the growth in fee income and the contribution from various business segments:

Trust & Investment Management led the fee growth with a 9.4% year-over-year increase to $730 million, followed by Treasury Management (+10.5% to $187 million) and Capital Markets (+9.3% to $434 million). Merchant Processing and Credit Card businesses also showed solid growth at 5.2% each.

U.S. Bancorp’s payments business showed improved momentum, with merchant processing fee revenue growth accelerating from 3.0% in Q3 2024 to 5.2% in Q3 2025. Similarly, credit card fee revenue growth improved from 4.5% to 5.2% over the same period. Consumer credit card balances grew from $29.0 billion to $30.2 billion, with yields holding steady at 13%.

Strategic Initiatives

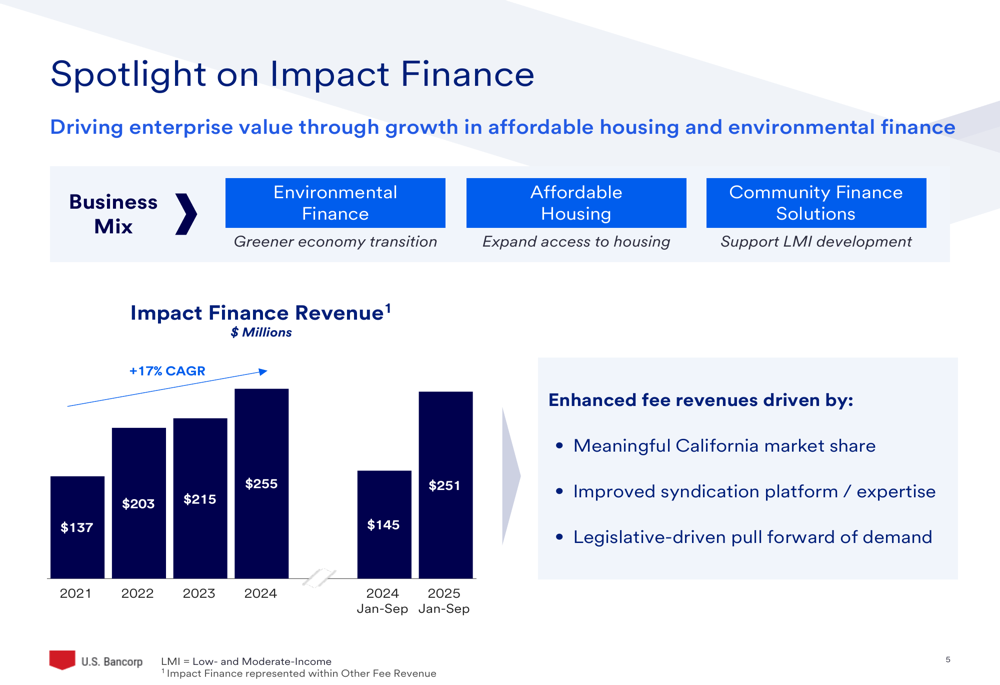

The bank highlighted its focus on Impact Finance as a key growth driver, with revenues in this segment increasing from $137 million in 2021 to $251 million for the first nine months of 2025. This initiative focuses on environmental finance, affordable housing, and community finance solutions.

As illustrated in the following chart, Impact Finance has shown consistent growth over the past several years:

U.S. Bancorp is also making strategic shifts in its deposit mix, with consumer deposits growing from 50.5% of total deposits in Q3 2023 to 52.4% in Q3 2025, representing an increase of $5 billion or 2%. This shift reflects the bank’s focus on growing its consumer franchise through interconnected products, pricing analytics, marketing promotions, and distribution strategies.

The bank’s self-funding organic growth strategy balances savings initiatives with strategic reinvestments. This approach has contributed to the improvement in efficiency ratio from 61.1% in Q4 2023 to 57.2% in Q3 2025, while operating leverage improved from negative 470 basis points to positive 530 basis points over the same period.

Capital Position and Credit Quality

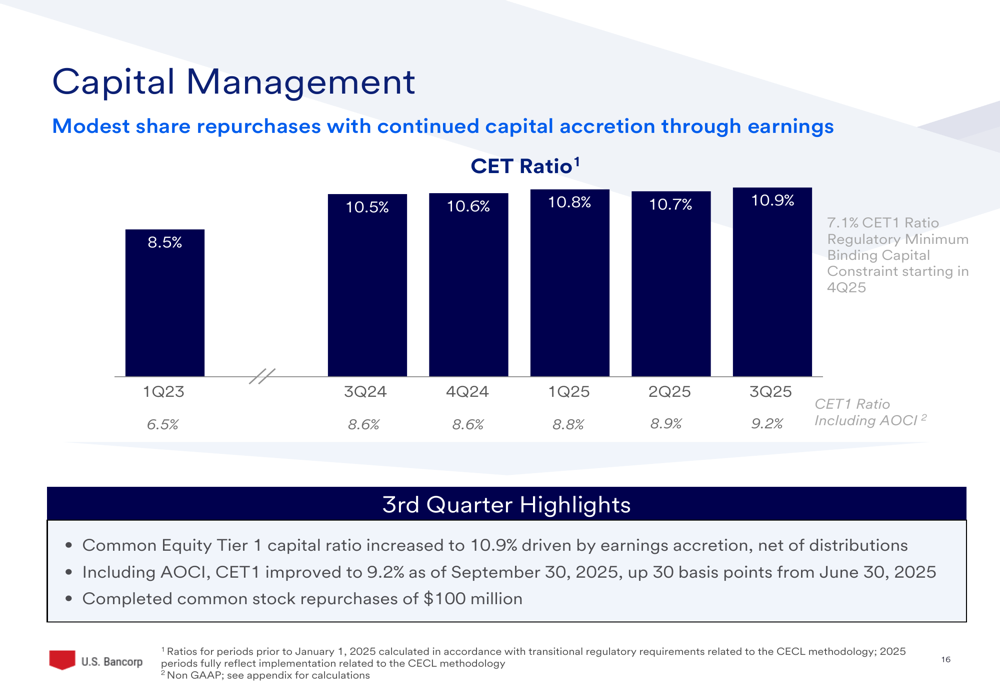

U.S. Bancorp maintained a strong capital position, with a Common Equity Tier 1 (CET1) capital ratio of 10.9%, well above regulatory requirements. This represents a significant improvement from earlier periods, providing the bank with flexibility for growth and capital returns to shareholders.

The following chart shows the progression of the CET1 ratio over time:

Credit quality remained stable, with a net charge-off ratio of 0.56%. Nonperforming assets decreased by 1.5% compared to the previous quarter and by 10.5% year-over-year to $1,654 million.

Forward-Looking Statements

Looking ahead, U.S. Bancorp provided guidance for the fourth quarter of 2025 and outlined medium-term targets that reflect confidence in its growth strategy. For Q4 2025, the bank expects net interest income to remain stable compared to Q3 levels.

The bank’s medium-term targets include:

These targets reflect U.S. Bancorp’s confidence in its ability to generate sustainable growth and returns. The bank aims to achieve a return on average assets of 1.15% to 1.35%, a return on tangible common equity in the high teens, and mid-single-digit fee revenue growth.

During the earnings call, CEO Gunjan Kedia emphasized the bank’s focus on organic growth, stating, "We are generating organic growth through distinctive interconnected solutions." CFO John Stern expressed confidence in reaching a 3% net interest margin by 2027.

U.S. Bancorp’s comprehensive results summary provides a detailed breakdown of its financial performance:

With its strong financial performance, strategic focus on fee income growth, and clear medium-term targets, U.S. Bancorp appears well-positioned to continue delivering value to shareholders while navigating the evolving banking landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.