CTAs keep buying Treasuries, gold longs face stop-loss risk: BofA

US Foods Holding Corp (NYSE:USFD) delivered strong second-quarter results for fiscal year 2025, with significant growth in profitability metrics despite modest volume increases. The foodservice distributor’s stock continued its upward momentum, trading at $86.21 in pre-market, up 1.81% following the August 7 presentation.

Quarterly Performance Highlights

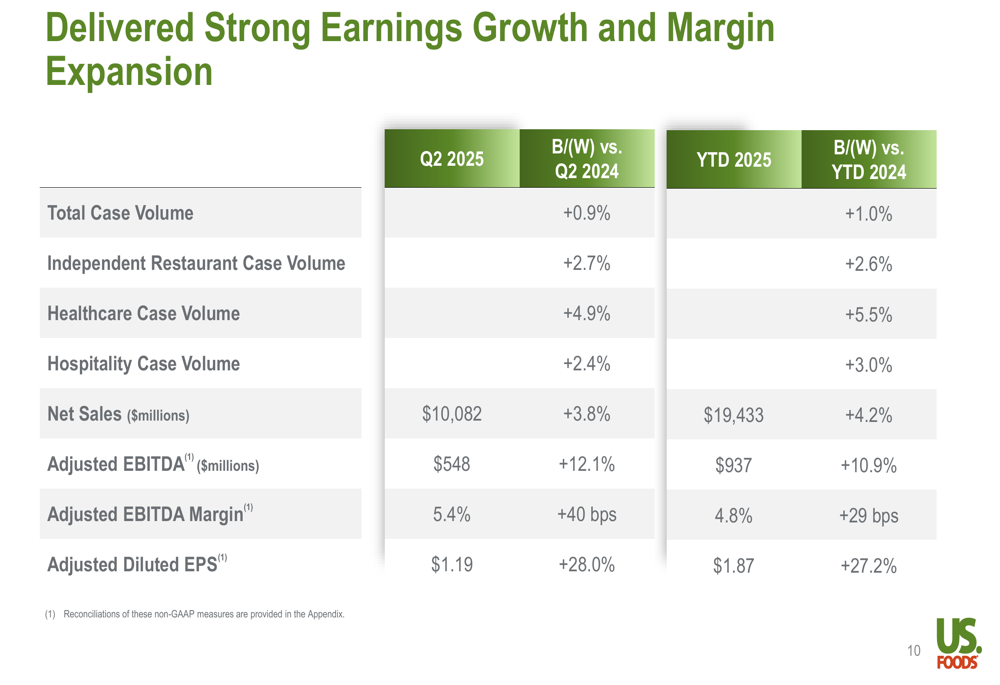

US Foods reported robust financial results for Q2 2025, showing substantial improvements across key metrics compared to the same period last year. The company achieved $10.08 billion in net sales, representing a 3.8% increase year-over-year, while adjusted EBITDA grew by 12.1% to $548 million.

Notably, adjusted diluted EPS surged 28.0% to $1.19, significantly outpacing revenue growth and demonstrating the company’s ability to translate modest top-line expansion into substantial bottom-line results. The adjusted EBITDA margin expanded by 40 basis points to 5.4%, reflecting improved operational efficiency.

As shown in the following detailed performance comparison:

Case volume growth was particularly strong in US Foods’ target customer segments, with healthcare leading at 4.9%, followed by independent restaurants at 2.7% and hospitality at 2.4%. These results represent a continuation of the company’s market share gains in these segments, with the presentation noting 17 consecutive quarters of growth with independent restaurants and 19 quarters with healthcare.

The company has successfully built on its Q1 2025 performance, when it reported adjusted EPS of $0.68 and revenue of $9.4 billion, demonstrating accelerating growth momentum through the first half of the fiscal year.

Strategic Initiatives

US Foods highlighted several strategic initiatives driving its strong performance, organized around four key pillars: Culture, Service, Growth, and Profit. The company has made significant progress in operational efficiency, with its routing transformation initiative now deployed in 65 markets representing approximately 90% of routed miles.

"We delivered more than a 2% improvement in cases per mile over prior year and nearly 6% over two years via routing initiatives; best performance in company history," the company noted in its presentation.

The company’s digital ecosystem continues to gain traction, with record e-commerce penetration reaching 78% for independent restaurants and 89% for the total company. This digital leadership has helped US Foods enhance customer loyalty and streamline operations.

US Foods has also expanded its Pronto business, which is now live in 44 markets and has expanded penetration to 15 markets, with plans to reach 20 by year-end. The company expects Pronto to deliver over $900 million in sales this year and has raised its 2027 sales projection for this program to $1.5 billion, up from the previous target of $1 billion.

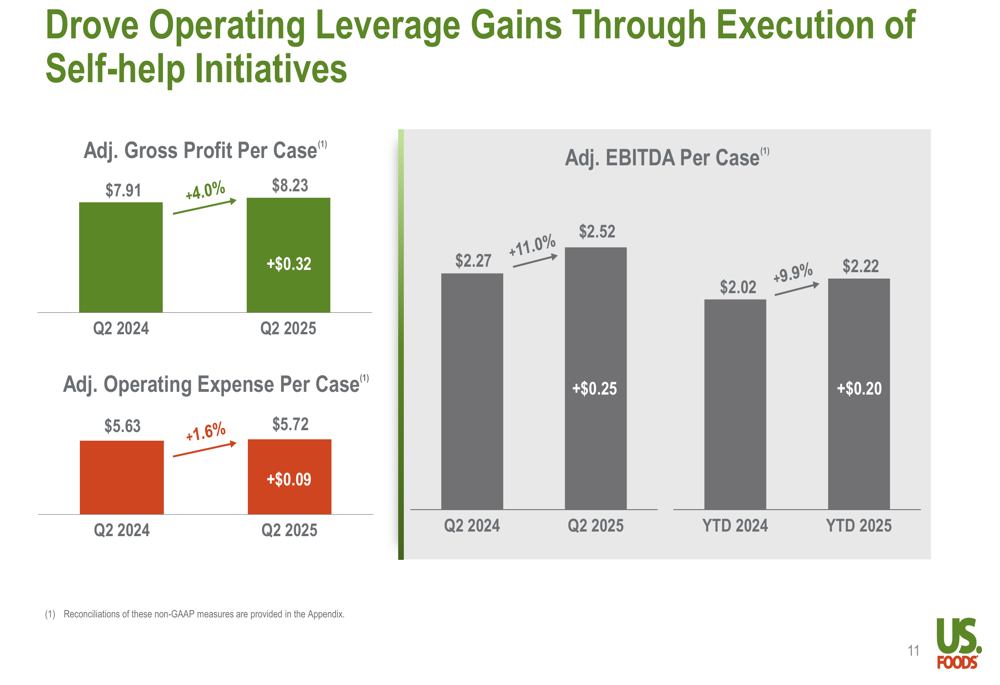

The company’s operational improvements are clearly demonstrated in the following chart showing gains in adjusted gross profit per case and adjusted EBITDA per case:

Detailed Financial Analysis

US Foods has achieved significant operating leverage gains through its self-help initiatives. Adjusted gross profit per case increased by 4.0% to $8.23 in Q2 2025, while adjusted operating expense per case grew at a slower rate of 1.6% to $5.72, resulting in an 11.0% increase in adjusted EBITDA per case to $2.52.

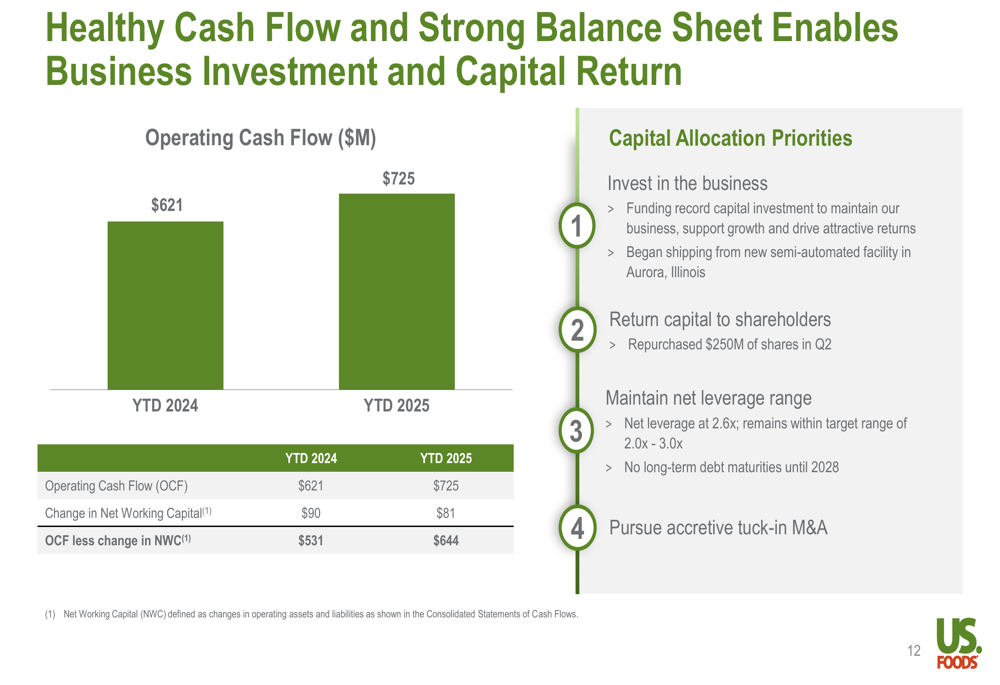

The company’s cash flow generation has also strengthened, with year-to-date operating cash flow of $725 million, up from $621 million in the same period last year. This robust cash flow has enabled US Foods to pursue its capital allocation priorities, including significant investments in its business and returning capital to shareholders.

As illustrated in the cash flow and capital allocation summary:

US Foods repurchased $250 million of shares in Q2 2025, while maintaining a healthy balance sheet with net leverage at 2.6x, within its target range of 2.0x to 3.0x. The company has no long-term debt maturities until 2028, providing financial flexibility for future growth initiatives.

On the operational front, US Foods has delivered more than $50 million in year-to-date cost of goods savings through strategic vendor management and is on track to exceed its 2027 plan commitment of $260 million. The company has also grown private label penetration by more than 80 basis points to over 53% with core independent restaurants, enhancing margins.

Forward-Looking Statements

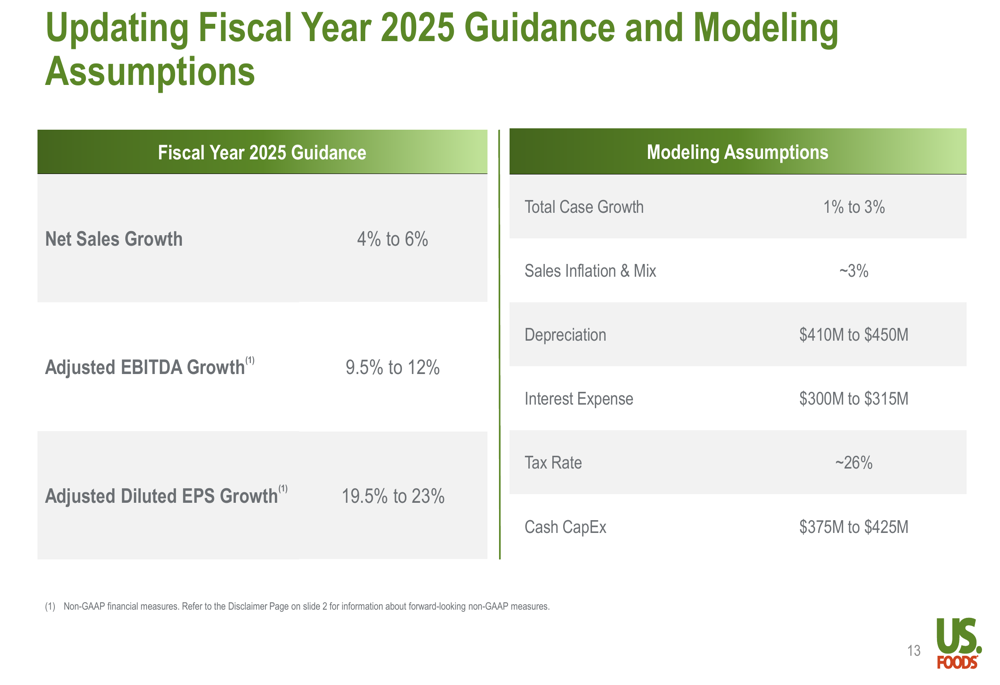

Based on its strong first-half performance, US Foods has provided an updated fiscal year 2025 guidance, projecting continued robust growth across key metrics:

The company expects net sales growth of 4% to 6% for the full year, with adjusted EBITDA growth of 9.5% to 12% and adjusted diluted EPS growth of 19.5% to 23%. These projections are supported by anticipated total case growth of 1% to 3% and sales inflation and mix of approximately 3%.

Looking beyond 2025, US Foods outlined its long-term financial targets, including approximately 5% net sales CAGR, 10% adjusted EBITDA CAGR, more than 20 basis points of annual adjusted EBITDA margin expansion, and approximately 20% adjusted diluted EPS CAGR.

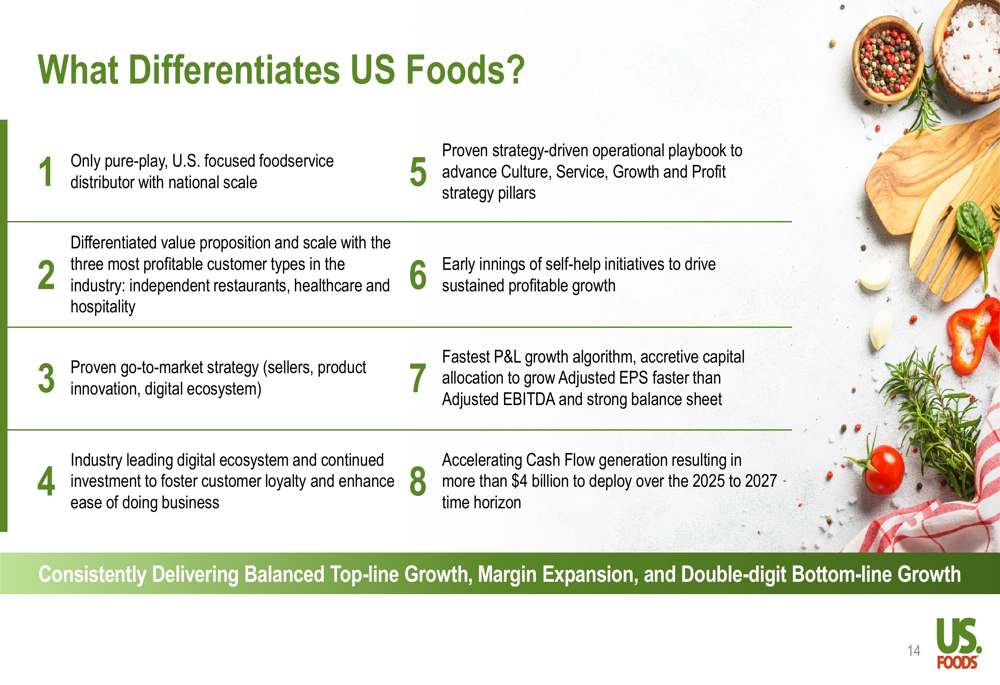

The company highlighted its key differentiators that position it for continued success in the foodservice distribution industry:

US Foods emphasized its status as "the only pure-play, U.S. focused foodservice distributor with national scale" and its "differentiated value proposition and scale with the three most profitable customer types in the industry: independent restaurants, healthcare and hospitality."

The company also noted that it is in the "early innings of self-help initiatives to drive sustained profitable growth" and expects "accelerating cash flow generation resulting in more than $4 billion to deploy over the 2025 to 2027 time horizon."

With its strong Q2 2025 performance, strategic initiatives gaining traction, and positive outlook, US Foods appears well-positioned to continue its growth trajectory and deliver value to shareholders in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.