Oracle: Baird initiates with ‘Outperform’, sees it at center of AI boom

Introduction & Market Context

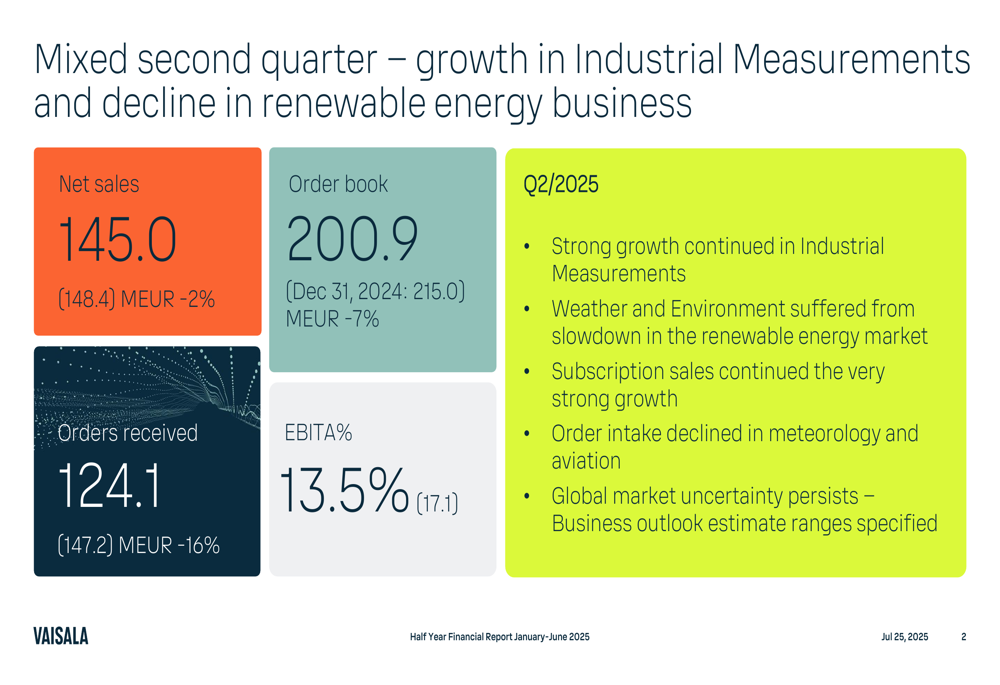

Vaisala Oyj A (HEL:VAIAS) presented its Q2 2025 financial results on July 25, 2025, revealing a mixed performance characterized by strong growth in its Industrial Measurements segment contrasted with significant declines in its Weather and Environment business. The company’s stock fell 6.33% to €46.60 following the presentation, as investors reacted to the company’s narrowed and slightly lowered full-year guidance.

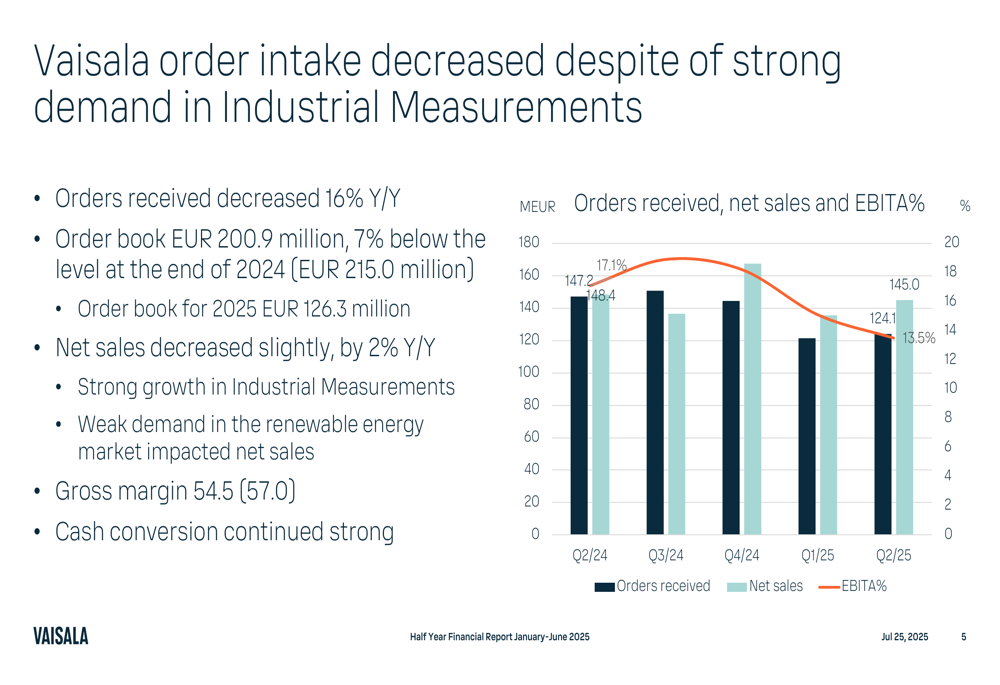

The Finnish measurement technology company reported a 2% year-over-year decline in net sales to €145.0 million, with orders received dropping 16% to €124.1 million. These results mark a notable shift from the company’s robust Q1 2025 performance, which had seen 21% year-over-year revenue growth.

Quarterly Performance Highlights

Vaisala’s Q2 2025 results reflected diverging trends across its business segments. The company achieved an EBITA margin of 13.5%, down from 17.1% in the same period last year, as shown in the financial highlights below.

The company’s order book stood at €200.9 million at the end of Q2, representing a 7% decline from December 31, 2024. Despite the overall decline in orders and sales, Vaisala highlighted the continued strong growth in subscription sales and maintained solid cash flow generation.

A closer look at the company’s order intake and financial performance reveals the extent of the slowdown compared to previous quarters:

Detailed Financial Analysis

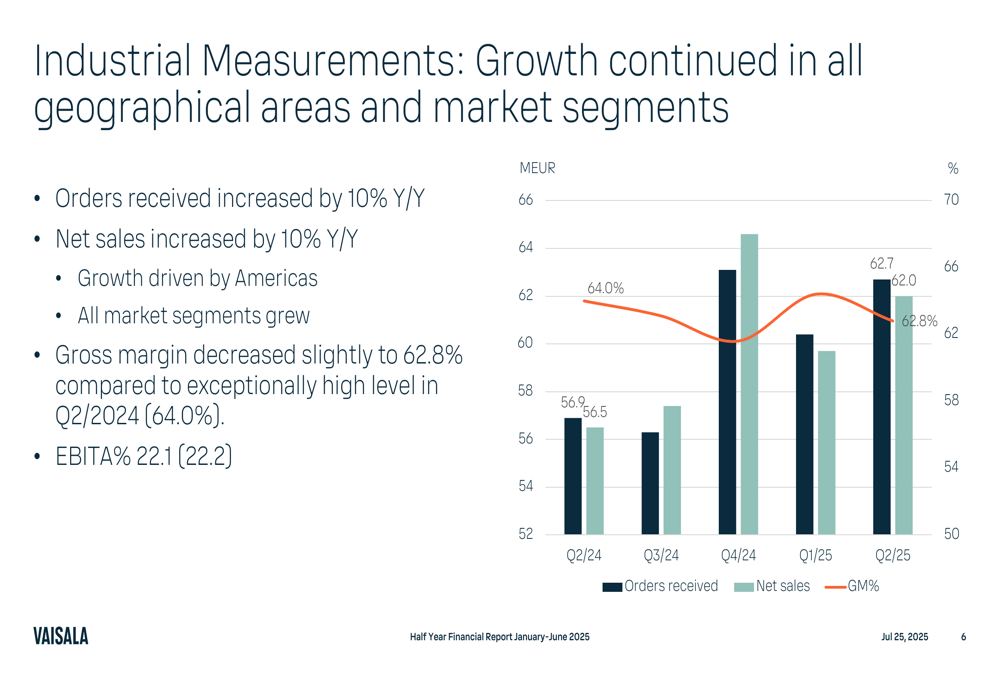

Industrial Measurements Segment

The Industrial Measurements segment emerged as Vaisala’s bright spot in Q2 2025, with both orders received and net sales increasing by 10% year-over-year. Growth was particularly strong in the Americas region, with all market segments contributing positively. However, gross margin in this segment decreased slightly to 62.8% compared to 64.0% in Q2 2024, while EBITA margin remained stable at 22.1%.

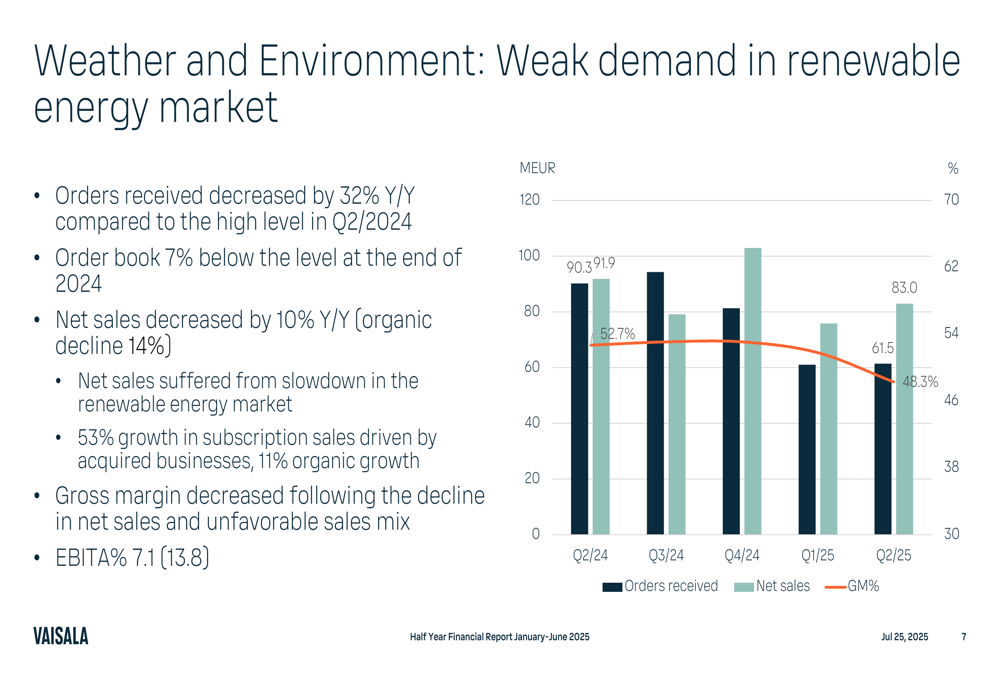

Weather and Environment Segment

In stark contrast, Vaisala’s Weather and Environment segment experienced significant challenges, with orders received plummeting 32% year-over-year and net sales declining 10%. The company attributed this primarily to a slowdown in the renewable energy market. Despite these headwinds, subscription sales in this segment grew by 53%, driven by acquired businesses, with organic growth of 11%.

The segment’s profitability was substantially impacted, with EBITA margin falling to 7.1% from 13.8% in the same period last year. This decline was attributed to lower net sales volume and an unfavorable sales mix.

Cash Flow and Financial Position

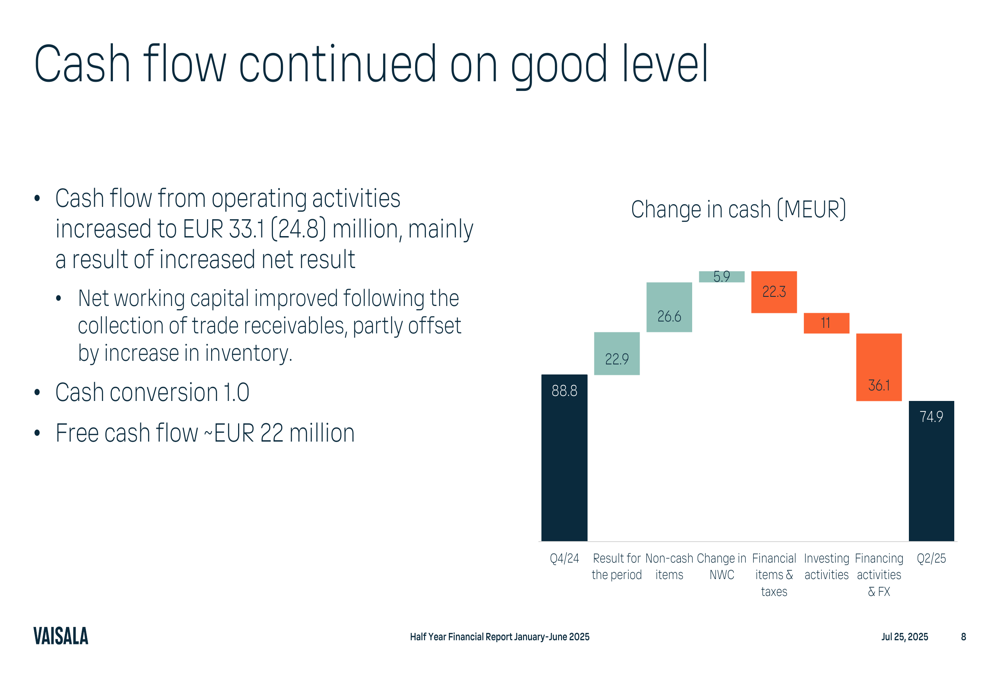

Despite the mixed operational performance, Vaisala maintained strong cash flow generation in Q2. Cash flow from operating activities increased to €33.1 million from €24.8 million in the comparable period, supported by improvements in net working capital.

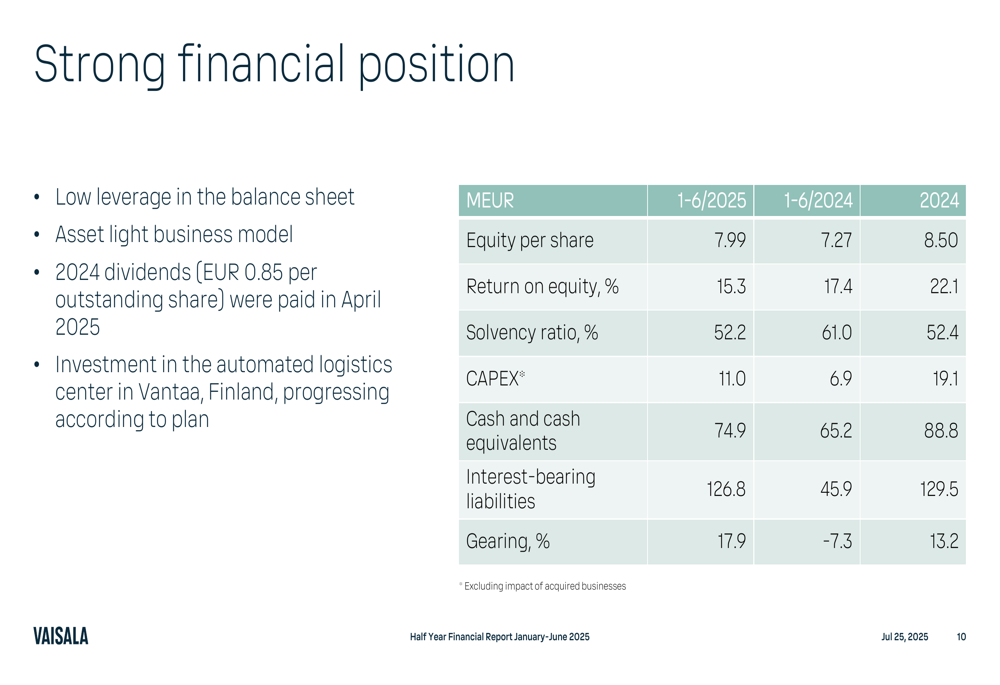

The company’s financial position remains solid, with a solvency ratio of 52.2% and gearing at 17.9%. Capital expenditures for the first half of 2025 totaled €11.0 million, up from €6.9 million in the same period last year, reflecting ongoing investments including the automated logistics center in Vantaa, Finland.

Half-Year Performance

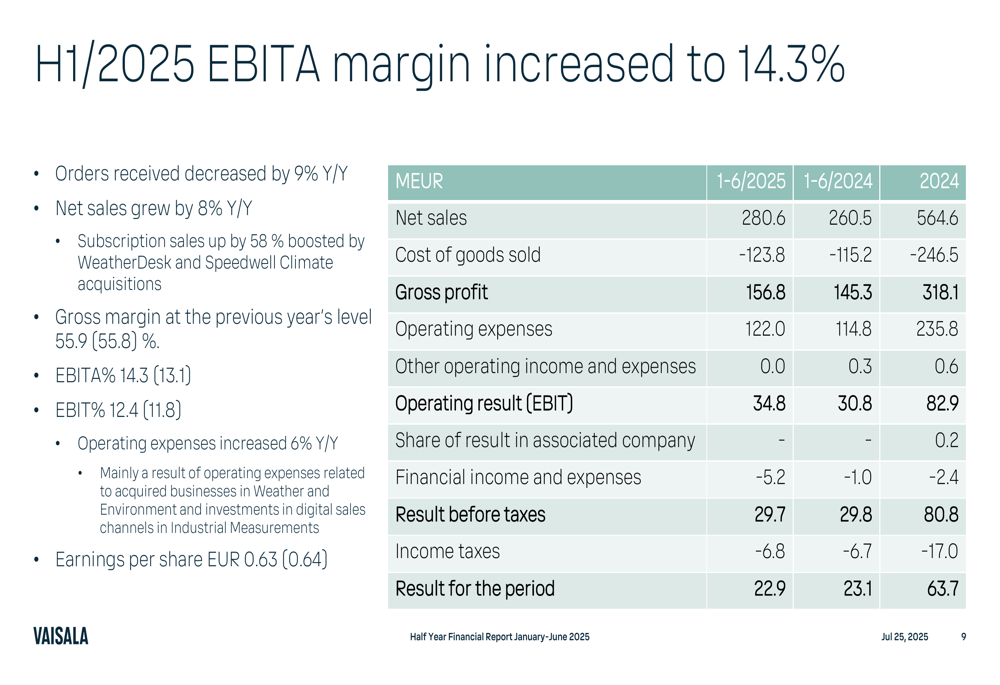

For the first half of 2025, Vaisala reported 8% growth in net sales year-over-year, despite a 9% decline in orders received. Subscription sales were particularly strong, increasing by 58%. The company’s EBITA margin improved to 14.3% from 13.1% in H1 2024, while earnings per share remained relatively stable at €0.63 compared to €0.64 in the prior year period.

Forward-Looking Statements

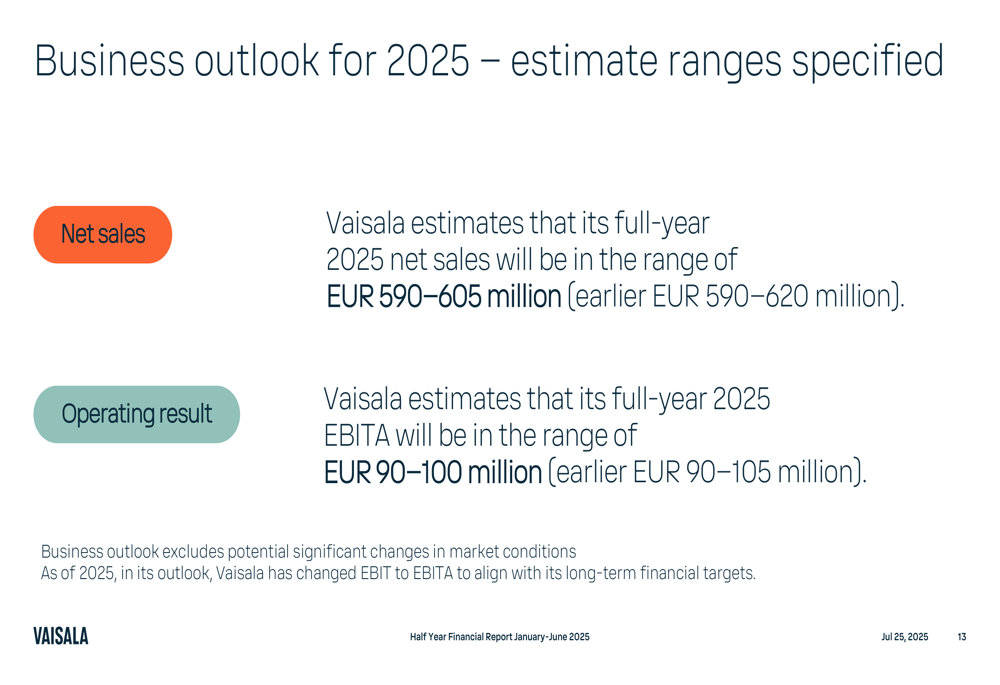

In light of the challenging market conditions, particularly in the renewable energy sector, Vaisala revised its business outlook for 2025. The company now expects full-year net sales to be in the range of €590-605 million, down from the previous estimate of €590-620 million. Similarly, the EBITA forecast was adjusted to €90-100 million from the earlier projection of €90-105 million.

The company’s market outlook categorizes its various sectors into three groups: growth markets (Industrial, Life science, Power), stable markets (Roads), and declining markets (Renewable energy, Meteorology, Aviation). This segmentation highlights the challenges Vaisala faces in its Weather and Environment business, which is heavily exposed to the currently declining renewable energy and meteorology markets.

Strategic Initiatives

Despite near-term challenges, Vaisala continues to focus on its strategic priorities, which include growth in industrial measurements, expansion in energy transition, driving profitability, and simplifying and scaling operations. The company’s vision centers on "Taking every measure for the planet," with megatrends such as energy transition, AI and process optimization, and health and wellbeing guiding its long-term strategy.

The contrast between Vaisala’s Q1 and Q2 2025 performance underscores the volatility in its markets, particularly in renewable energy. While the Industrial Measurements segment continues to deliver strong growth, the significant challenges in the Weather and Environment segment are likely to persist in the near term, as reflected in the company’s revised guidance. Investors will be watching closely to see if the company can navigate these headwinds while continuing to advance its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.