Gold prices dip as December rate cut bets wane; economic data in focus

Introduction & Market Context

Finnish measurement technology company Vaisala Oyj (HEL:VAIAS) reported strong third-quarter 2025 results on October 23, with solid sales growth despite facing headwinds in certain market segments. The company’s stock reacted positively, rising 1.09% to €46.2, continuing its recovery from the 52-week low of €39.7 and moving closer to its high of €54.9.

Vaisala, a global leader in environmental and industrial measurement solutions, continues to navigate a complex market environment with mixed performance across its business segments. The company’s presentation highlighted robust overall growth despite significant challenges in its Weather and Environment division.

Quarterly Performance Highlights

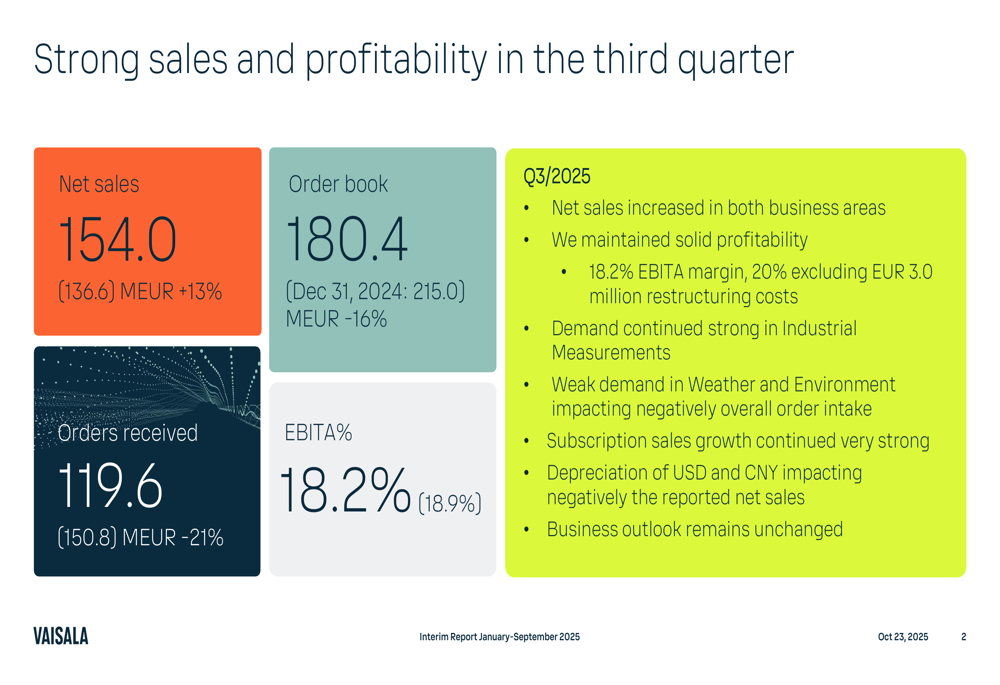

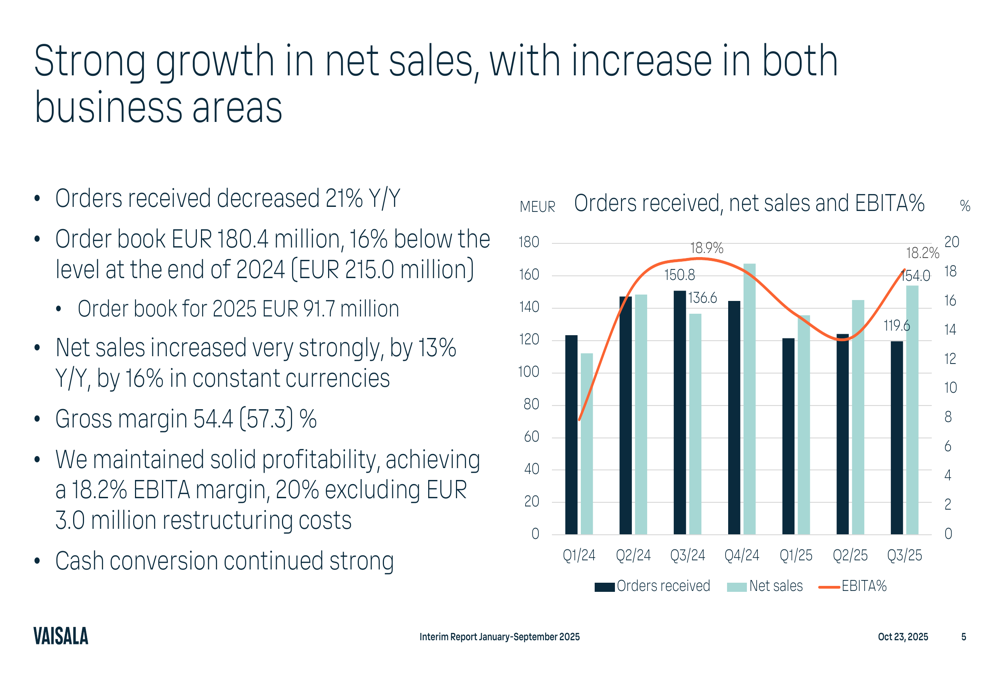

Vaisala reported impressive net sales growth of 13% year-over-year, reaching €154.0 million in Q3 2025. This growth was achieved despite a concerning 21% decline in orders received, which fell to €119.6 million. The company’s order book stood at €180.4 million, representing a 16% decrease from the end of 2024.

As shown in the following key figures summary:

Profitability remained solid with an EBITA margin of 18.2%, or 20% when excluding €3.0 million in restructuring costs. The company’s subscription business emerged as a particular bright spot, with very strong growth continuing throughout the quarter.

CEO Kai Öistämö emphasized the company’s profitability in the earnings call, stating, "We maintained a very solid profitability, 18.2% EBITDA margin." He also highlighted the scalability of the software business, noting, "If software business grows 50% year on year, one should expect that it scales."

The following chart illustrates the company’s performance trajectory over recent quarters, showing the divergence between orders received and net sales:

Segment Analysis

Vaisala’s two main business segments showed markedly different performance patterns in Q3 2025, reflecting varying market conditions across the company’s diverse portfolio.

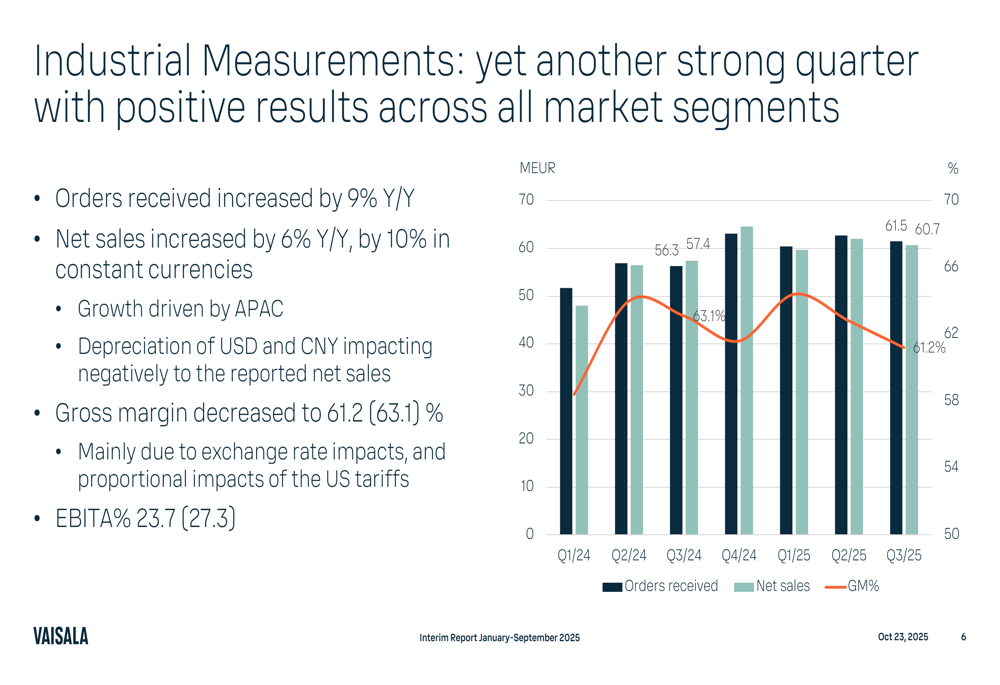

The Industrial Measurements segment delivered solid growth, with orders received increasing by 9% year-over-year and net sales rising by 6% (10% in constant currencies). Growth was primarily driven by the APAC region, though profitability was impacted by exchange rate fluctuations and U.S. tariffs. The segment maintained a strong EBITA margin of 23.7%, though this represented a decline from 27.3% in the prior year period.

The segment’s performance is visualized in the following chart:

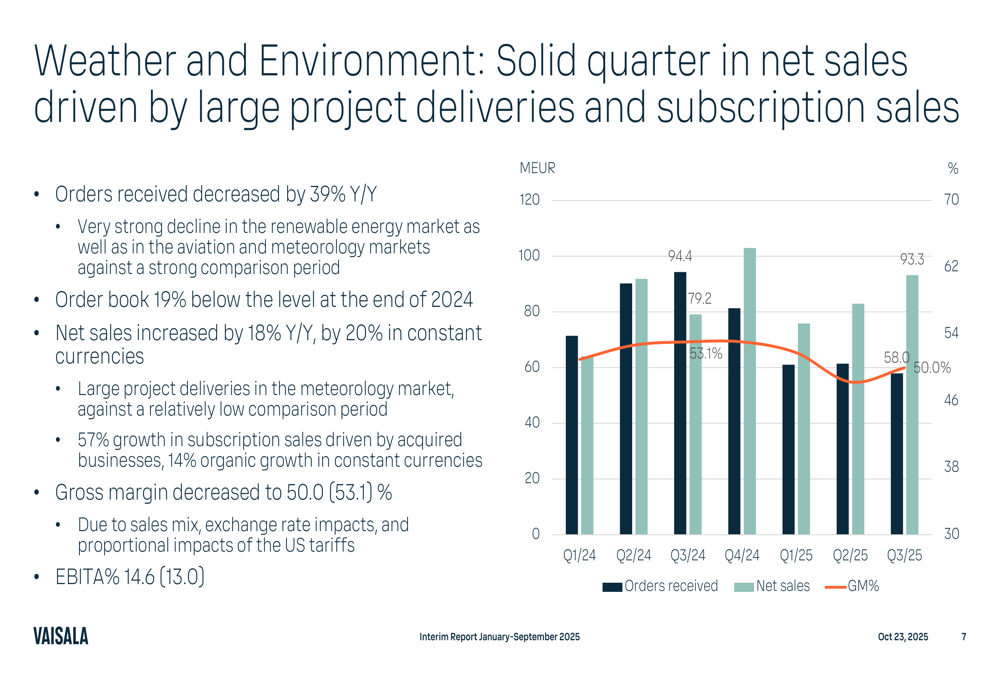

In contrast, the Weather and Environment segment faced significant challenges, with orders received plummeting by 39% year-over-year. The company attributed this decline to weakness in the renewable energy market as well as in aviation and meteorology markets. Despite these headwinds, the segment’s net sales increased by 18% year-over-year (20% in constant currencies), driven by large project deliveries in the meteorology market.

A notable bright spot in this segment was the 57% growth in subscription sales, boosted by the WeatherDesk and Speedwell Climate acquisitions. Organic subscription growth reached 14% in constant currencies, highlighting the success of Vaisala’s digital transformation initiatives.

The following chart details the Weather and Environment segment’s performance:

Financial Position and Cash Flow

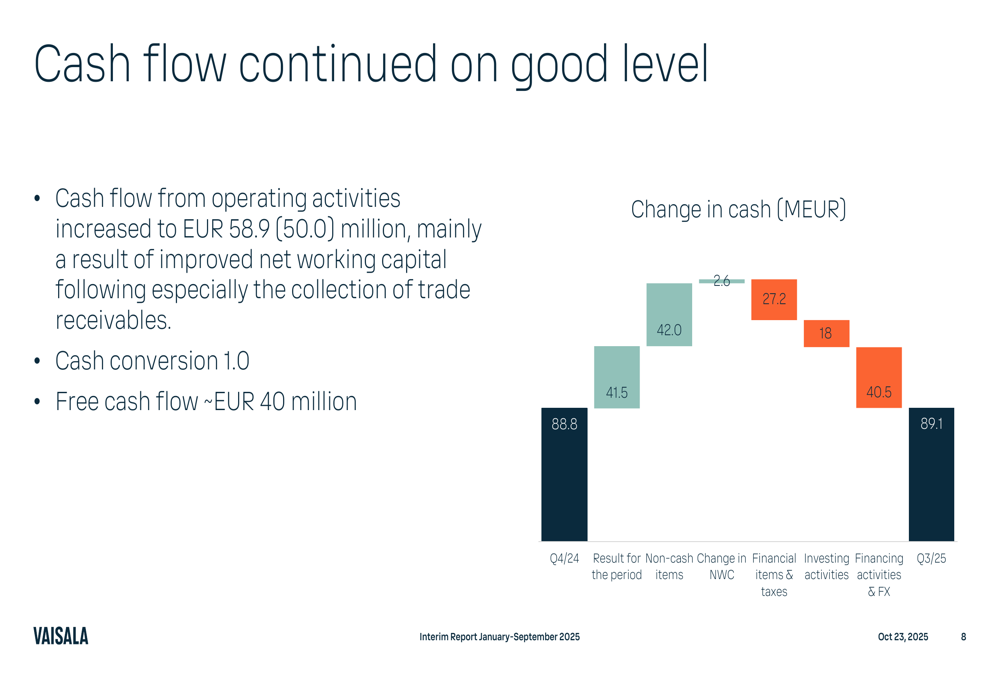

Vaisala maintained a strong financial position in Q3 2025, with cash flow from operating activities increasing to €58.9 million from €50.0 million in the prior year period. This improvement was primarily driven by better working capital management, particularly in the collection of trade receivables. Cash conversion remained strong at 1.0, with free cash flow reaching approximately €40 million.

The company’s cash flow development is illustrated in the following waterfall chart:

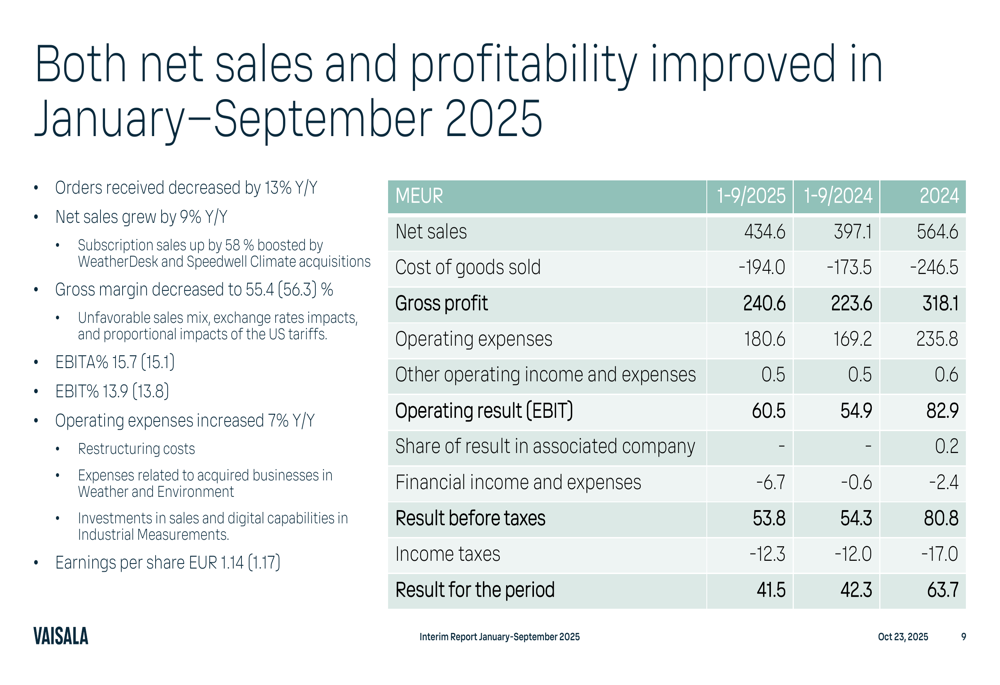

The income statement for the first nine months of 2025 shows net sales of €434.6 million, up 9% from €397.1 million in the same period of 2024. Gross profit increased to €240.6 million from €223.6 million, though gross margin decreased slightly to 55.4% from 56.3%. Operating result (EBIT) improved to €60.5 million from €54.9 million.

Vaisala maintains a strong balance sheet with relatively low leverage, reflecting its asset-light business model. The company paid dividends of €0.85 per outstanding share in April 2025 and completed construction of a new automated logistics center in Vantaa, Finland during Q3. Additionally, Vaisala announced the acquisition of Quanterra Systems Ltd, a company specializing in atmospheric monitoring of CO2 fluxes, in September.

Business Outlook and Guidance

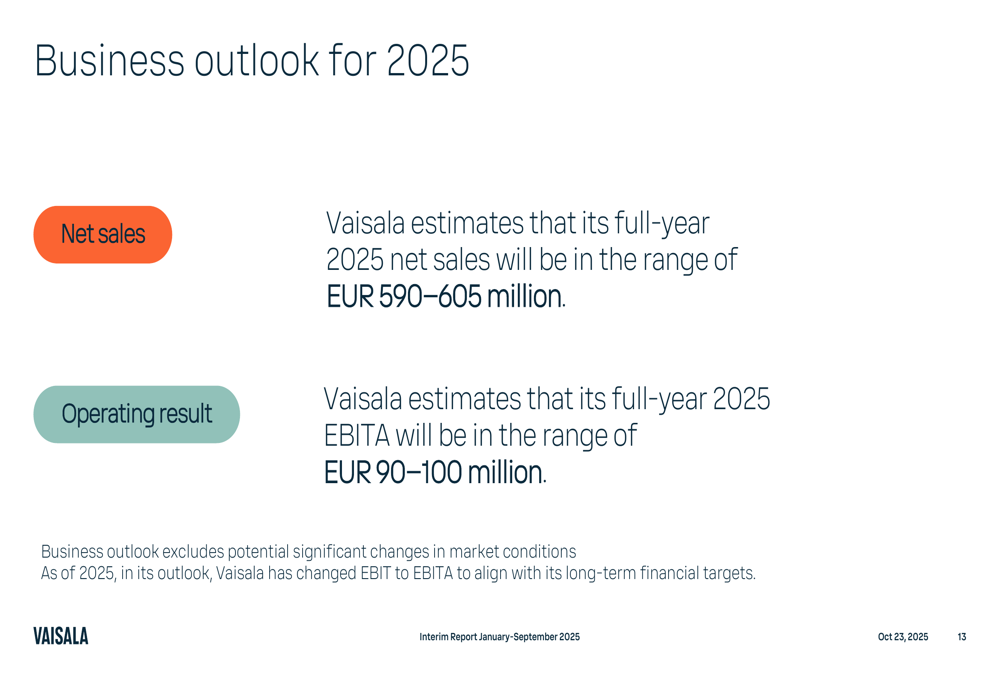

Vaisala maintained its full-year 2025 guidance, expecting net sales between €590-605 million and EBITA in the range of €90-100 million. This outlook excludes potential significant changes in market conditions.

The company’s market outlook for 2025 indicates growth in Industrial, Life science, and Power segments, while Roads are expected to remain stable. In contrast, Renewable energy, Meteorology, and Aviation markets are projected to decline, presenting ongoing challenges for the Weather and Environment business segment.

Vaisala continues to innovate across its portfolio, with recent product launches including the Vaisala Circular service for probe recalibration, Xweather hail forecasts for solar panel protection, and the WindCube 2.1 XP wind lidar with enhanced accuracy and performance.

While Vaisala has demonstrated resilience with strong sales growth and solid profitability in Q3 2025, the significant decline in orders received, particularly in the Weather and Environment segment, raises concerns about future growth potential. However, the company’s strong subscription business performance and continued innovation provide positive indicators for long-term success as Vaisala navigates a complex and evolving market landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.