Lumen Technologies hires Sean Alexander as head of Connected Ecosystems

Introduction & Market Context

Valeura Energy Inc . (TSX:VLE) presented its Q2 2025 results and strategic initiatives on August 7, 2025, highlighting solid financial performance and a significant expansion of its Gulf of Thailand operations. The company’s stock closed at C$8.68, down 2.76% on the day of the presentation, reflecting some market hesitation despite the company’s positive developments.

The quarter was marked by stable production and strong cash generation, with the company announcing a strategic farm-in agreement with Thailand’s largest operator, PTTEP, substantially increasing its acreage position in the region. This move aligns with Valeura’s stated strategy of pursuing both organic growth and strategic acquisitions in Southeast Asia.

Q2 2025 Financial Performance Highlights

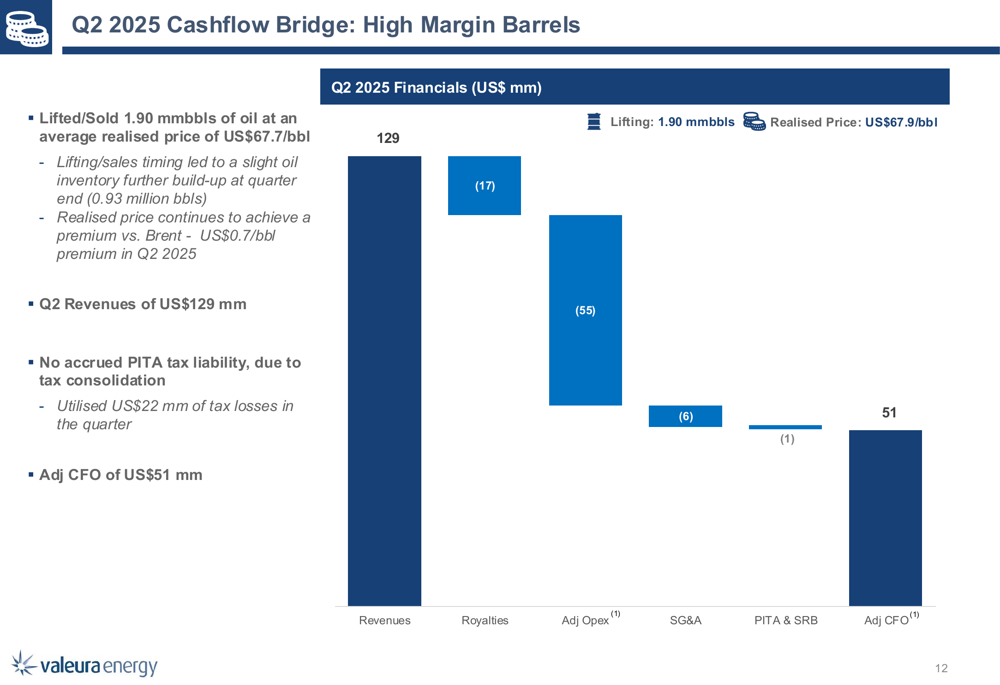

Valeura reported oil production of 21.4 mbbl/d during Q2 2025, generating revenue of US$129 million from 1.90 million barrels sold at an average realized price of US$67.9 per barrel. This represents a decline from the US$79 per barrel realized in Q1 2025, reflecting broader oil market dynamics.

The company delivered adjusted EBITDAX of US$62 million and adjusted cash flow from operations of US$51 million for the quarter. Operating expenses totaled US$55 million, translating to US$28.0 per barrel.

As shown in the following cashflow bridge chart:

Valeura’s balance sheet continued to strengthen, with cash increasing to US$242 million as of June 30, 2025, representing a 65% increase compared to Q2 2024. The company’s book value rose 71% year-over-year to US$542 million, while adjusted working capital improved 81% to US$262 million.

Capital expenditures for the quarter reached US$49 million, including US$11.2 million for the Wassana Redevelopment project. The company also deployed US$4.3 million on share repurchases during the quarter.

Strategic Farm-in with PTTEP

A centerpiece of the presentation was Valeura’s strategic farm-in agreement with PTTEP, Thailand’s largest oil and gas operator, for blocks G1/65 and G3/65 in the Gulf of Thailand. The deal gives Valeura a 40% non-operated working interest in these blocks, which contain 15 existing oil and gas discoveries.

The company highlighted the low entry costs of US$14.7 million in back costs to June 30, 2025, plus a commitment to carry PTTEP on the cost of additional 3D seismic acquisition capped at US$2.2 million. The agreement dramatically expands Valeura’s acreage from 2,623 km² to 22,757 km².

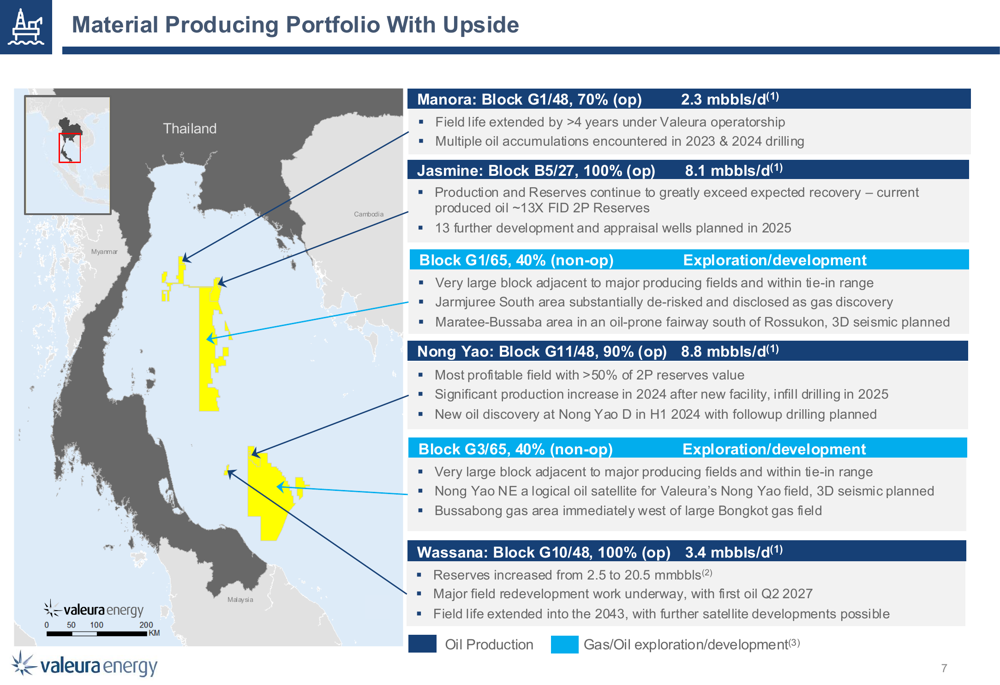

The following map illustrates Valeura’s expanded portfolio in the Gulf of Thailand, showing both existing producing assets and the new farm-in blocks:

The farm-in provides Valeura with both near-term development opportunities and exploration upside. Block G1/65 includes the Jarmjuree South Gas Discovery (NASDAQ:WBD) Area, which is substantially de-risked and positioned for potential near-term development. Block G3/65 features the Bussabong Gas Discovery Area with multiple gas discoveries immediately west of PTTEP’s Bongkot gas field, as well as the Nong Yao North-East Oil Prospect, which could be tied back to Valeura’s existing Nong Yao infrastructure.

Wassana Redevelopment Progress

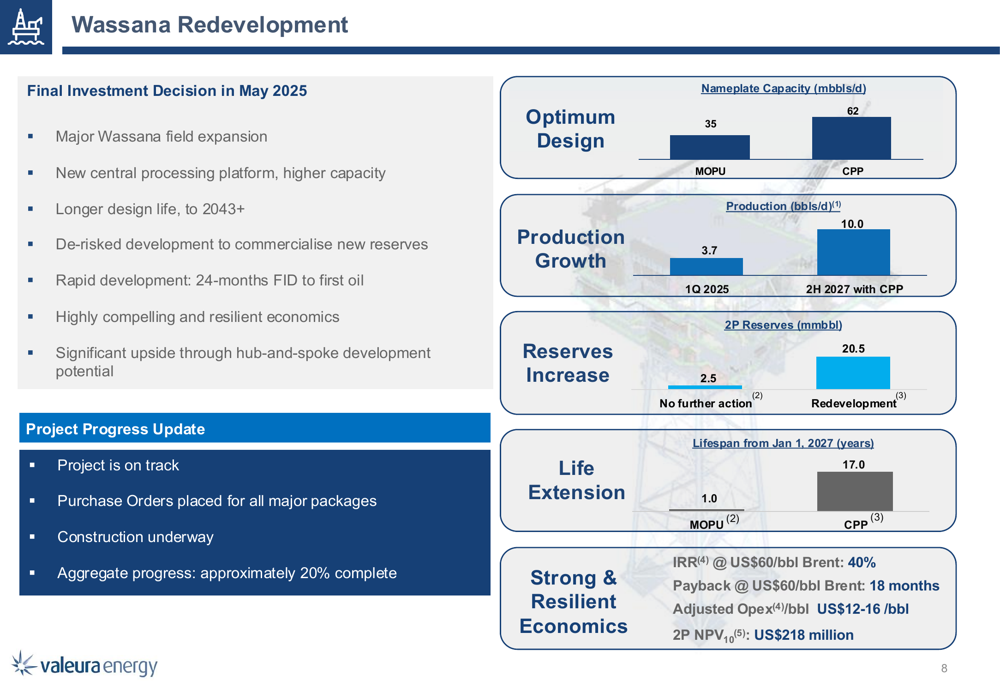

Valeura provided an update on its Wassana Redevelopment project, which reached Final Investment Decision (FID) in May 2025. The project aims to significantly expand the Wassana field with a new central processing platform, extending field life to 2043 and beyond.

The redevelopment is expected to increase 2P reserves from 2.5 million barrels to 20.5 million barrels and boost production from current levels of 3.7 mbbl/d to approximately 10 mbbl/d by the second half of 2027.

The following chart details the project’s economics and progress:

The company reported that construction is underway with approximately 20% of the work completed. The project offers compelling economics with an IRR of 40% at US$60/bbl Brent, an 18-month payback period, and a 2P NPV10 of US$218 million.

2025 Guidance and Outlook

Valeura reaffirmed its 2025 guidance, projecting full-year production of 23.0-25.5 mbbl/d, compared to 22.6 mbbl/d achieved in H1 2025. The company expects operating expenses of US$215-245 million and capital expenditures of US$175-195 million for the year.

Free cash flow guidance remains at US$80-195 million, based on Brent oil prices between US$65-85 per barrel. The company noted that this guidance will be updated following the closing of the G1/65 and G3/65 farm-in agreement.

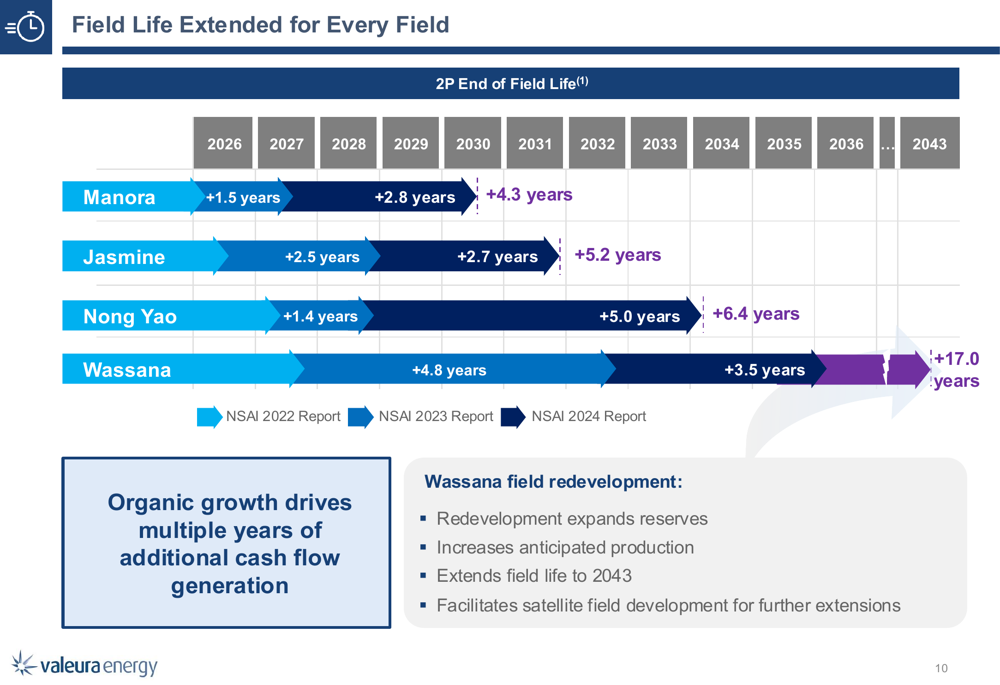

As illustrated in the following chart, Valeura has successfully extended the life of all its fields:

Valuation and Market Position

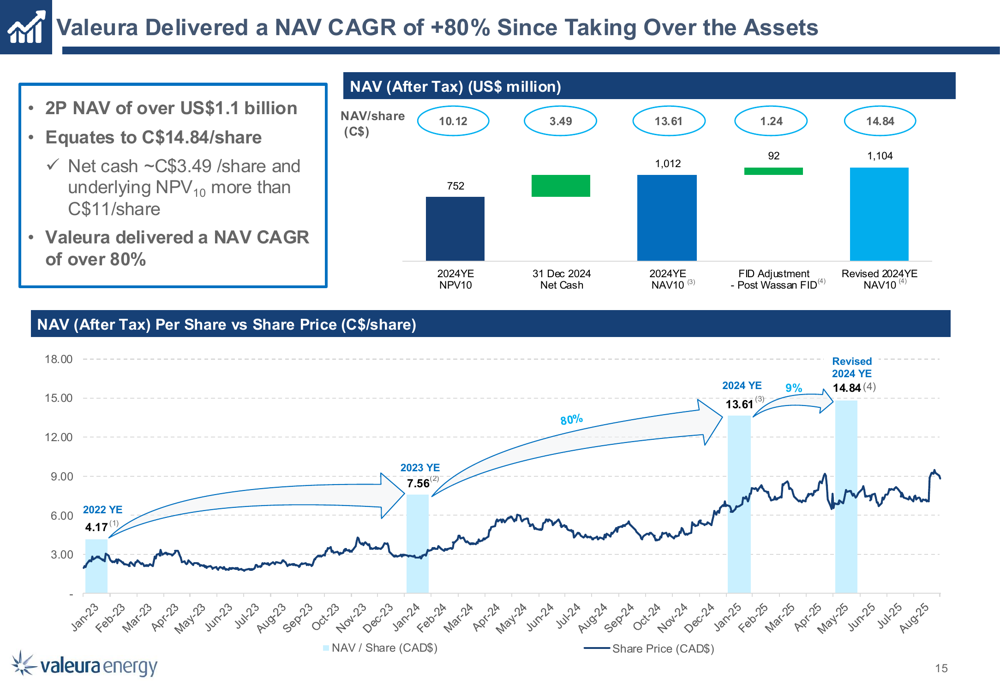

Valeura emphasized that its current market valuation does not reflect the company’s intrinsic value. Management highlighted that the company’s 2P NAV exceeds US$1.1 billion, equivalent to C$14.84 per share, compared to the current share price of C$8.67.

The company also presented comparative valuation metrics showing that it trades at a discount to peers across multiple metrics, including EV/2025E CFO (1.4x vs. peers’ median of 2.3x) and EV/2025E EBITDA (1.6x vs. peers’ median of 3.5x).

The following chart illustrates Valeura’s NAV growth trajectory:

Management pointed to a NAV CAGR of over 80% since taking over its current assets, demonstrating the company’s ability to create value through operational improvements and strategic initiatives.

In conclusion, Valeura’s Q2 2025 presentation showcased solid financial performance, strategic expansion through the PTTEP farm-in agreement, and progress on the Wassana Redevelopment project. While the market appears to be discounting the company’s shares relative to peers and NAV, management remains focused on executing its growth strategy in the Gulf of Thailand.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.