ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Varonis Systems (NASDAQ:VRNS) presented its Q2 2025 results on July 29, showcasing continued momentum in its data security business despite headwinds from its ongoing transition to a software-as-a-service (SaaS) model. The company’s stock closed at $54.41 and gained nearly 1% in aftermarket trading, reflecting investor confidence in its strategic direction.

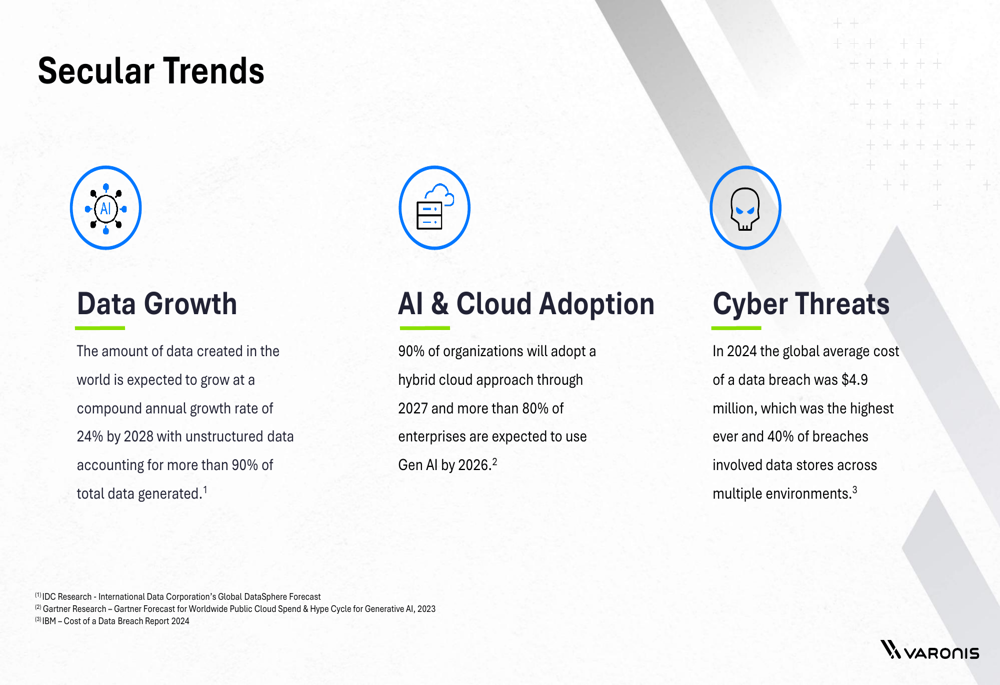

As a data security leader established in 2005, Varonis positions itself as "fighting a different battle than conventional cybersecurity companies" by focusing on a data-centric approach to security. This strategy appears well-aligned with key market trends, including rapid data growth, accelerating cloud and AI adoption, and evolving regulatory requirements.

As shown in the following slide highlighting secular trends driving demand:

The company cites data expected to grow at a 24% compound annual growth rate by 2028, with 90% of organizations adopting hybrid cloud by 2027 and over 80% using generative AI by 2026. Meanwhile, the global average cost of a data breach in 2024 reached $4.9 million, underscoring the critical need for robust data security solutions.

Quarterly Performance Highlights

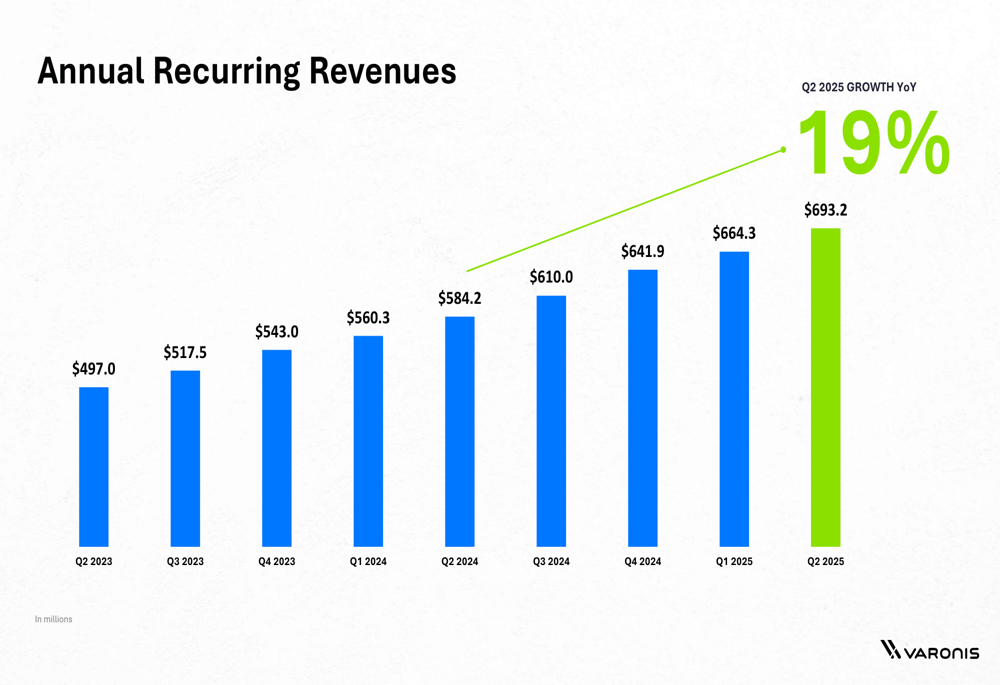

Varonis reported annual recurring revenue (ARR) of $693.2 million for Q2 2025, representing a 19% year-over-year increase from $584.2 million in Q2 2024. This growth trajectory has remained consistent over recent quarters, as illustrated in the company’s ARR chart:

The company’s SaaS transition continues to gain momentum, with SaaS ARR now constituting approximately 69% of total ARR, up significantly from 61% reported in Q1 2025. This acceleration indicates the company is making substantial progress toward its strategic goal of completing the SaaS transition by the end of 2025.

Year-to-date free cash flow reached $82.7 million, representing a 23.4% increase from $67 million in the same period last year, demonstrating the company’s ability to generate increasing cash flow despite the transitional headwinds.

SaaS Transition Impact

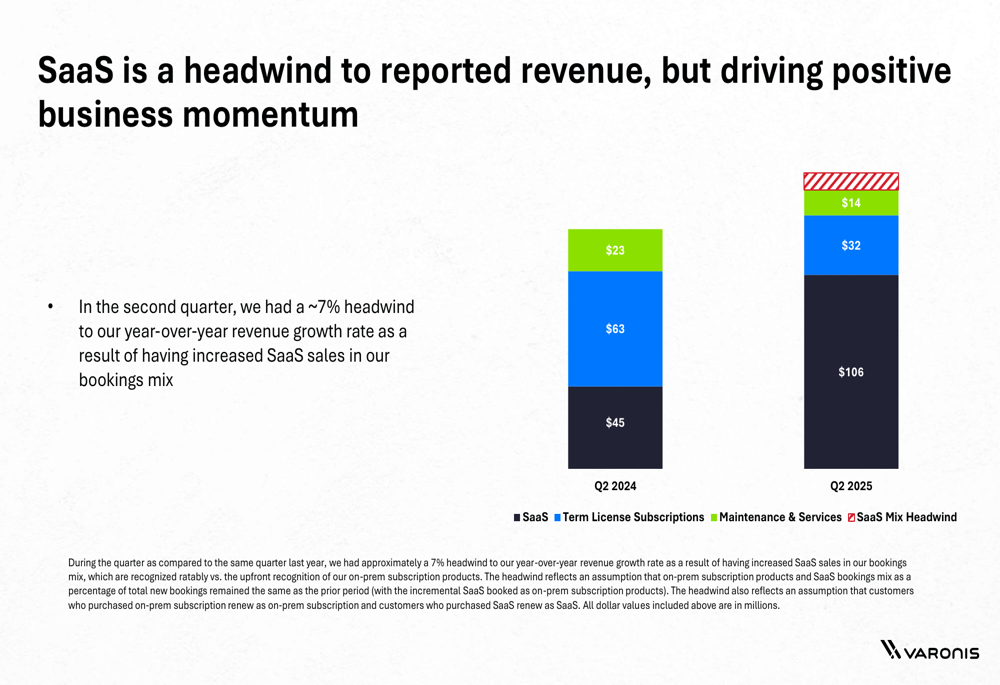

While Varonis’s ARR growth remains strong, the company’s transition to SaaS has created temporary headwinds for reported revenue and operating margins. The following slide illustrates how the revenue mix has shifted dramatically toward SaaS:

In Q2 2025, SaaS revenue more than doubled to $106 million from $45 million in Q2 2024, while term license subscriptions declined from $63 million to $32 million. This shift resulted in approximately a 7% headwind to year-over-year revenue growth due to the different revenue recognition patterns between SaaS and term licenses.

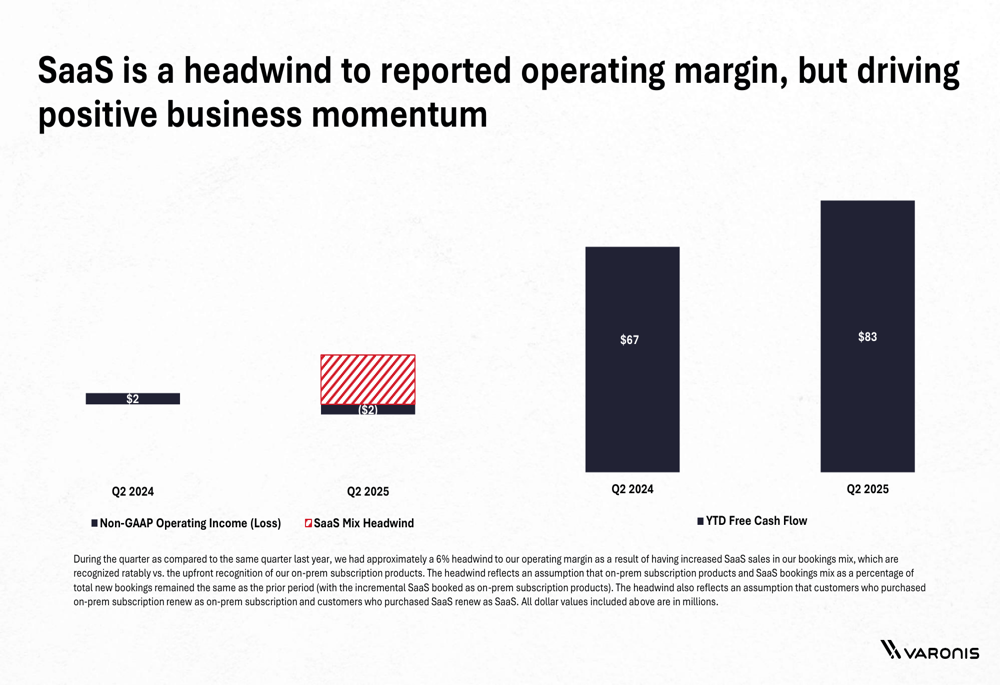

Similarly, the SaaS transition created a 6% headwind to operating margin, as shown in this comparison:

Non-GAAP operating income shifted from $2 million in Q2 2024 to a loss of $2 million in Q2 2025. However, the company’s free cash flow continued to strengthen, increasing from $67 million to $83 million year-to-date, highlighting the underlying financial health of the business despite accounting-driven impacts.

Strategic Initiatives & Market Position

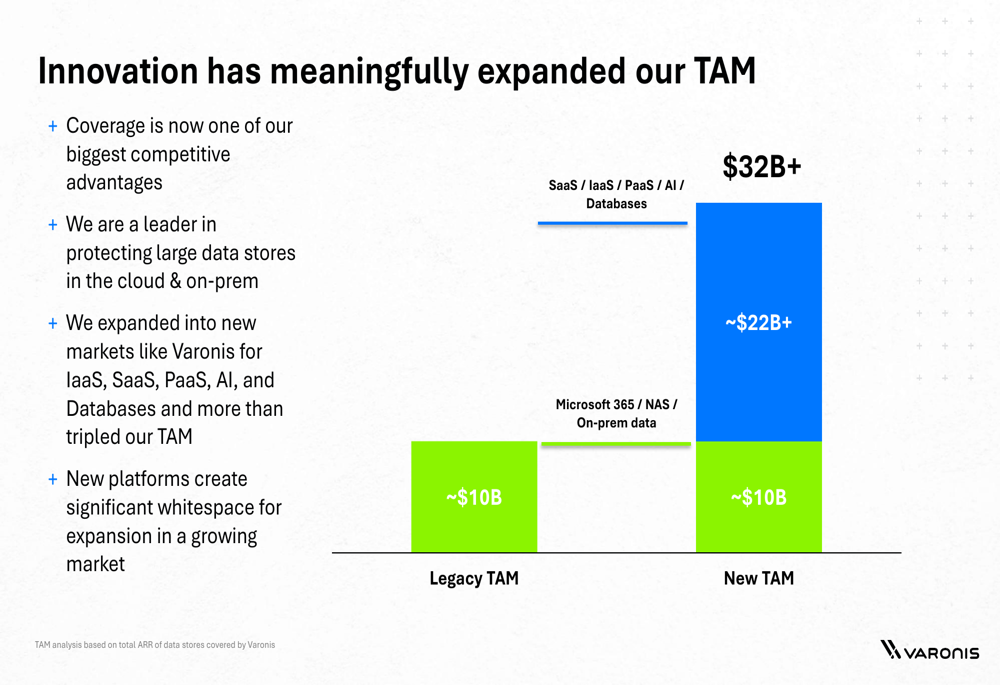

Varonis has significantly expanded its total addressable market (TAM) through innovation in recent years. The company’s presentation highlights how new platforms like Varonis for IaaS, SaaS, PaaS, AI, and Databases have tripled its TAM:

The legacy TAM of approximately $10 billion has expanded to roughly $32 billion through these innovations, creating substantial growth opportunities. Varonis emphasizes its first-mover advantage in the data security market, having pioneered data-first security in 2005 and continuously expanded its platform capabilities.

The company’s unified data security platform now encompasses a wide range of use cases, including data discovery and classification, data security posture management, insider risk management, ransomware prevention, and AI security, positioning it to address the evolving needs of organizations facing increasingly complex data security challenges.

Forward-Looking Guidance

For Q3 2025, Varonis expects total revenues between $163.0 million and $168.0 million, representing 10-13% year-over-year growth, with non-GAAP operating income between $4.0 million and $7.0 million.

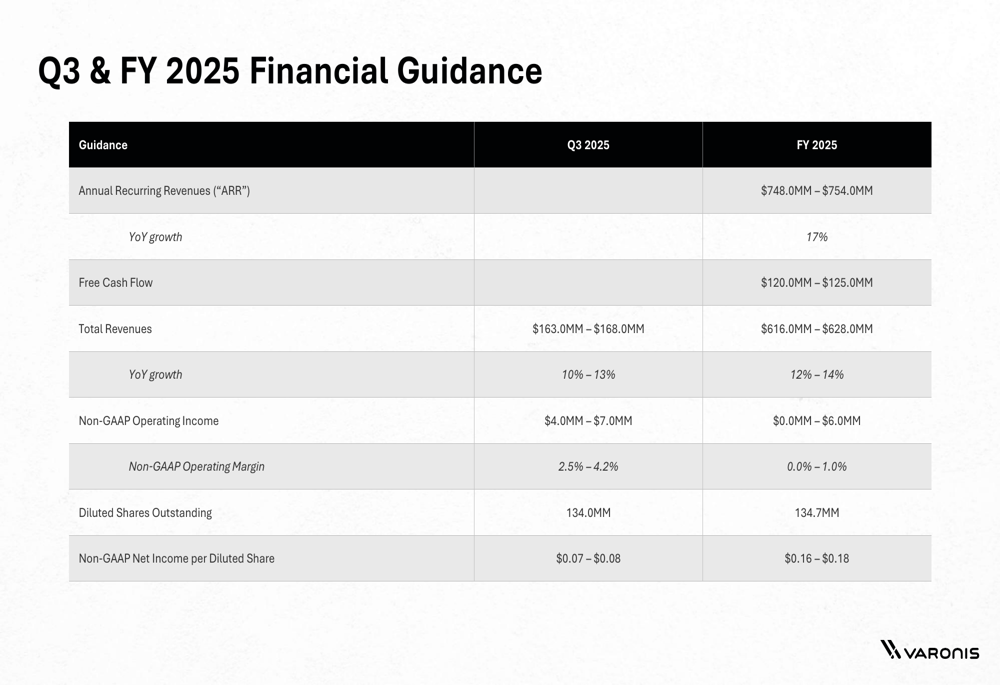

The company’s full-year 2025 guidance is detailed in the following slide:

Varonis projects annual recurring revenue to reach between $748.0 million and $754.0 million by year-end, representing 17% year-over-year growth. Free cash flow is expected to be between $120.0 million and $125.0 million, while total revenues are forecast at $616.0 million to $628.0 million, reflecting 12-14% growth.

The company maintains its long-term goal of building "a billion-dollar business that grows meaningfully with expanding profit and cash flow," suggesting confidence in its ability to continue scaling while improving profitability once the SaaS transition is complete.

Despite near-term margin pressure from the SaaS transition, Varonis’s consistent ARR growth, expanding free cash flow, and strategic market positioning indicate the company is successfully executing its transformation while laying the groundwork for sustainable long-term growth in the expanding data security market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.