Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

Veeco Instruments Inc (NASDAQ:VECO) presented its Q1 2025 financial results on May 7, 2025, highlighting continued strength in its semiconductor business despite an overall revenue decline. The company’s stock closed at $19.19 but traded down 1.56% to $18.89 in after-hours trading following the presentation.

Veeco, a manufacturer of semiconductor and thin film processing equipment, has been strategically positioning itself to capitalize on key industry inflections such as Gate-all-around (GAA) transistors and High-Bandwidth-Memory (HBM) technologies that are critical for AI and high-performance computing applications.

Quarterly Performance Highlights

Veeco reported Q1 2025 revenue of $167 million, which was above the mid-point of guidance but represented a sequential decline from the $182 million reported in Q4 2024. Non-GAAP operating income reached $24 million with diluted non-GAAP earnings per share of $0.37, exceeding the company’s guidance.

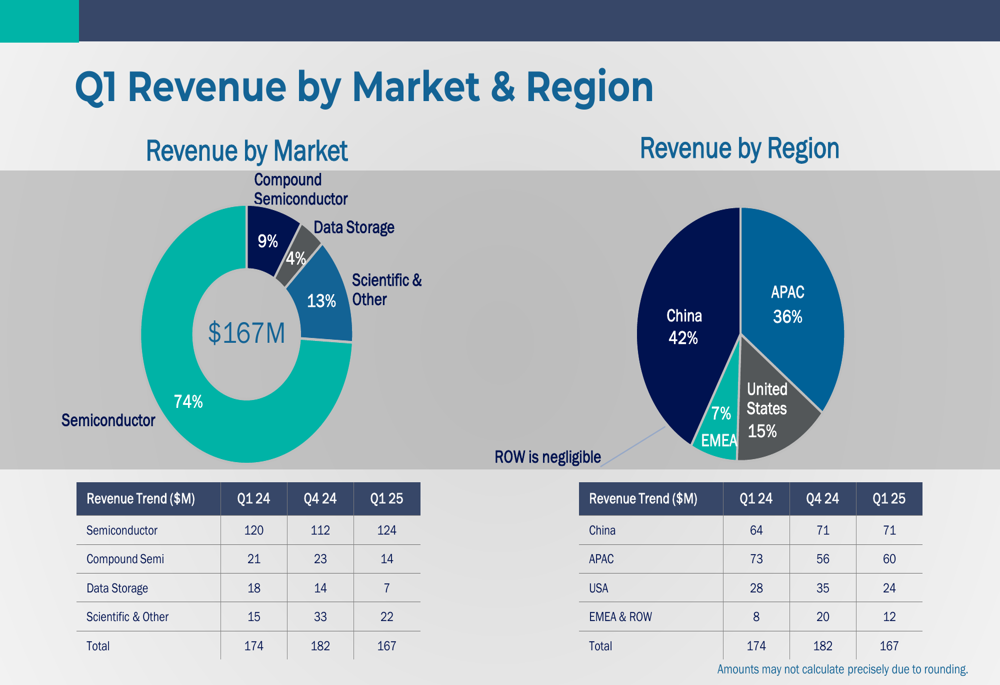

The semiconductor segment continued to be the primary revenue driver, accounting for 74% of total revenue ($124 million) and showing growth both sequentially and year-over-year. This growth was primarily driven by wet processing and lithography system shipments in Advanced Packaging (NYSE:PKG), as well as Laser Spike Annealing (LSA) systems for GAA and HBM applications.

As shown in the following chart of quarterly revenue by market and region, China represented 42% of Veeco’s revenue, followed by APAC at 36%, the United States at 15%, and EMEA at 7%:

The company highlighted several strategic wins during the quarter, including Intel (NASDAQ:INTC)’s 2025 EPIC Supplier Award, LSA system orders for GAA and HBM applications, and the qualification of a wet processing system at an Integrated Device Manufacturer (IDM).

Semiconductor Strategy and Market Positioning

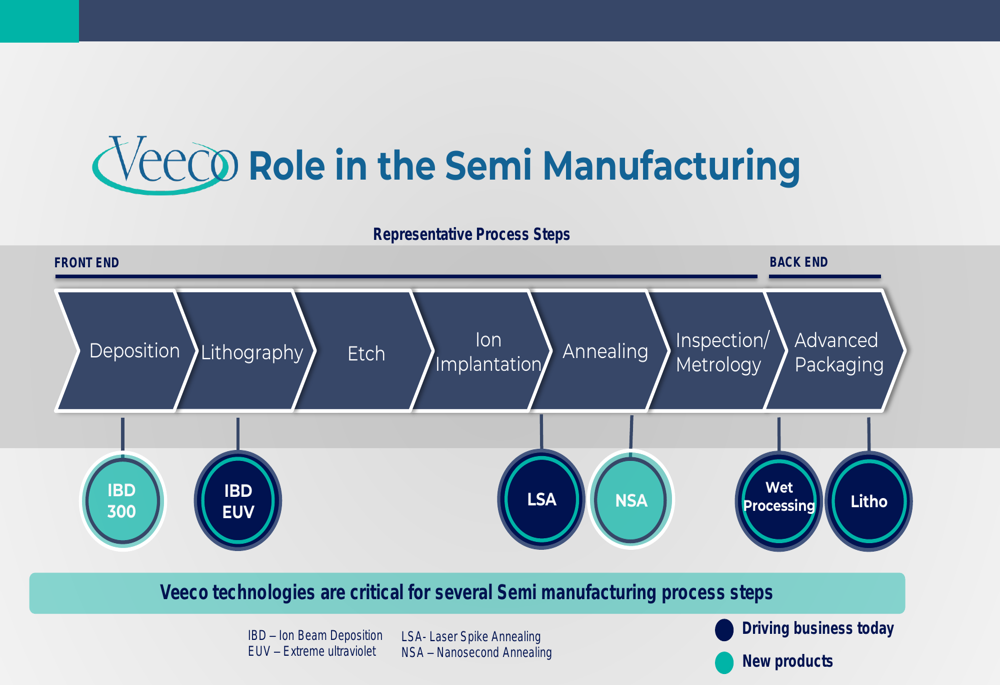

Veeco’s presentation emphasized its expanding role in the semiconductor manufacturing process, with technologies spanning both front-end and back-end operations. The company’s key technologies include Ion Beam Deposition (IBD), Laser Spike Annealing (LSA), Nanosecond Annealing (NSA), and Wet Processing solutions.

The following diagram illustrates Veeco’s position across the semiconductor manufacturing value chain:

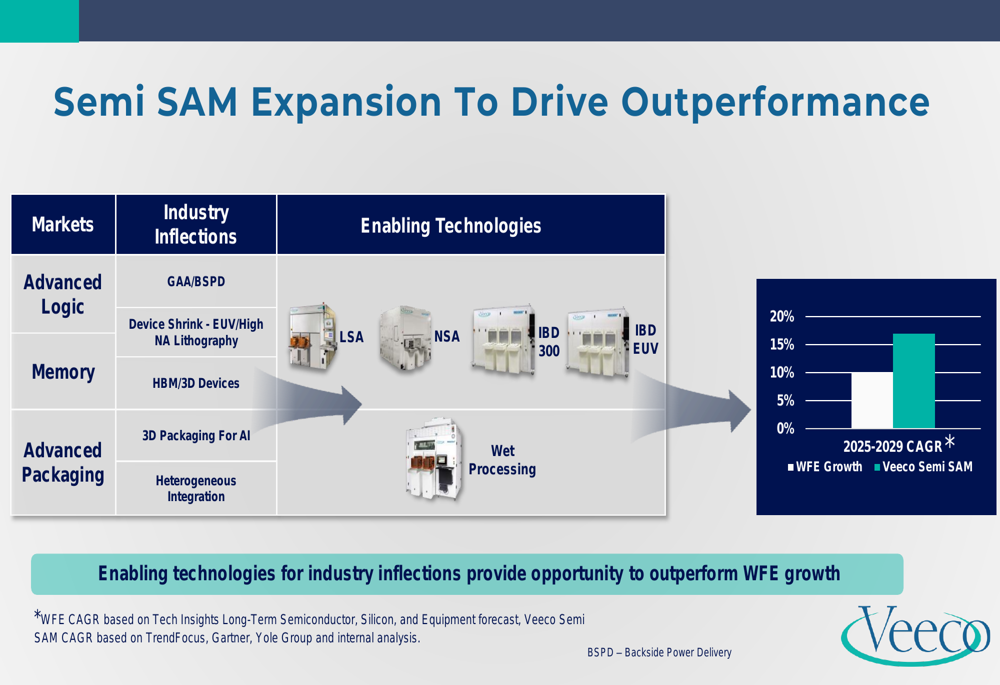

A significant focus of the presentation was Veeco’s expanding Serviceable Available Market (SAM), which the company projects will grow at approximately 16% CAGR from 2025-2029, compared to overall Wafer Fab Equipment (WFE) growth of around 6%. This expansion is driven by industry inflections in advanced logic, memory, and packaging technologies.

The company’s strategy to capture this growing market is illustrated in the following slide:

Veeco is actively pursuing evaluations with Tier 1 customers for its LSA, NSA, and IBD300 systems across both logic and memory applications. These evaluations are critical for capturing future revenue opportunities, with potential revenue per application win ranging from $30-60 million at 100K wafer starts per month.

Detailed Financial Analysis

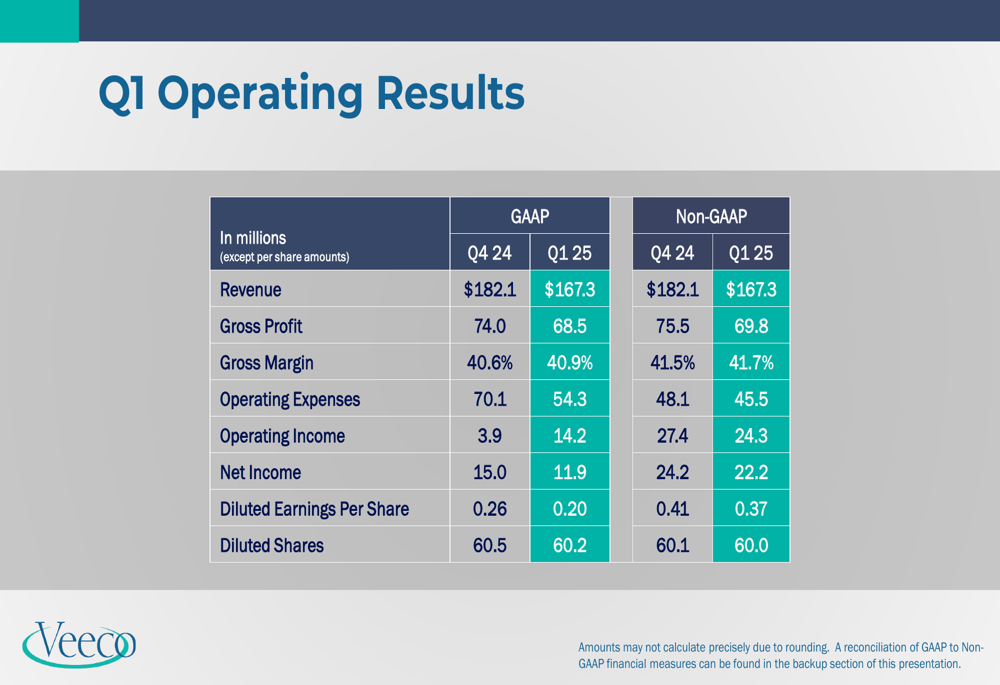

The Q1 2025 operating results showed a non-GAAP gross margin of 41.7%, slightly improved from 41.5% in Q4 2024. Non-GAAP operating expenses were $45.5 million, down from $48.1 million in the previous quarter.

The detailed financial performance is presented in the following table:

Veeco maintained a strong balance sheet with $353 million in cash and short-term investments as of Q1 2025, up from $345 million in Q4 2024. However, the company’s Days Sales Outstanding (DSO) increased from 48 to 62 days, and Days Inventory Outstanding (DIO) rose from 203 to 228 days, potentially indicating some operational challenges.

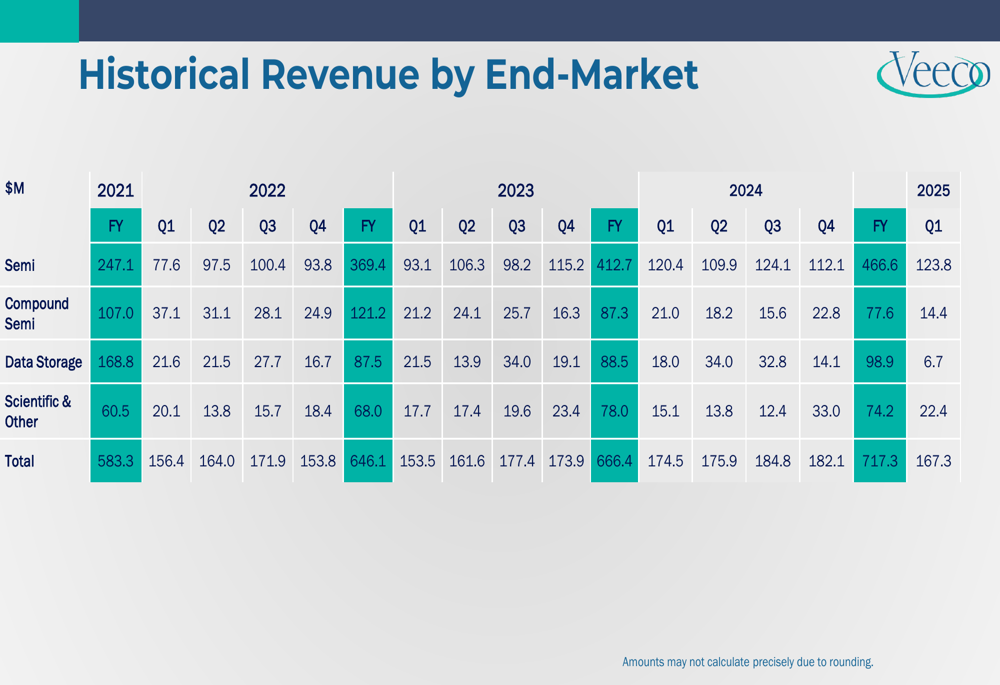

The company’s historical revenue trend by end-market shows the growing importance of the semiconductor segment, which has consistently increased as a percentage of total revenue:

Forward-Looking Statements

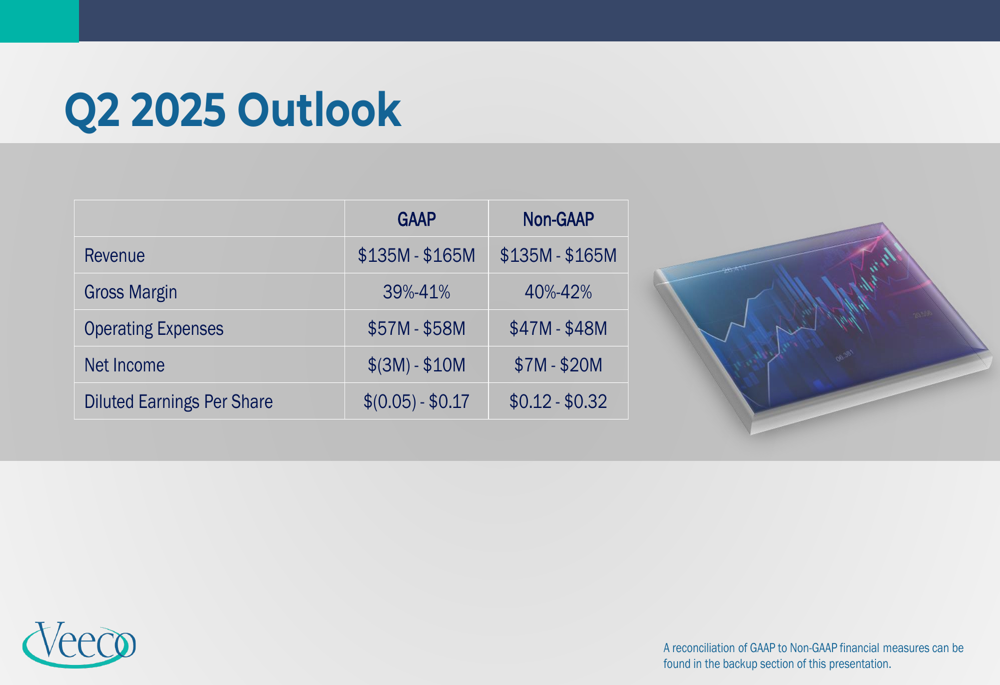

For Q2 2025, Veeco provided guidance of $135-165 million in revenue, representing a potential sequential decline from Q1. Non-GAAP gross margin is expected to be 40-42%, with non-GAAP operating expenses of $47-48 million and diluted non-GAAP EPS of $0.12-0.32.

The Q2 outlook is summarized in the following slide:

This guidance suggests some caution in the near-term outlook, potentially reflecting broader industry dynamics or specific customer timing issues. The projected revenue range for Q2 is notably lower than the $185 million reported in Q3 2024, indicating a significant deceleration from the company’s performance just two quarters ago.

During the Q3 2024 earnings call, management had anticipated a decline in China revenue for 2025, which appears to be materializing as China-related business transitions from the strong initial demand seen in 2024. Additionally, the data storage market was projected to experience a substantial revenue reduction of $60-70 million in 2025 due to customers’ lack of investment in new systems.

Despite these near-term challenges, Veeco remains optimistic about its long-term growth prospects, particularly in the semiconductor segment. The company’s focus on key industry inflections such as GAA, HBM, and advanced packaging positions it to benefit from the ongoing AI and high-performance computing boom, even as it navigates the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.