Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Veeco Instruments Inc. (NASDAQ:VECO) presented its Q2 2025 financial results on August 6, 2025, reporting revenue and earnings that exceeded the high end of its guidance range. The semiconductor equipment manufacturer’s shares edged up 0.35% in aftermarket trading to $20.01, building on the day’s closing price of $19.94.

The company’s strong performance comes amid growing demand for advanced semiconductor manufacturing equipment, particularly for artificial intelligence applications, despite broader market concerns about potential shipment delays to China that were highlighted in the previous quarter’s earnings call.

Quarterly Performance Highlights

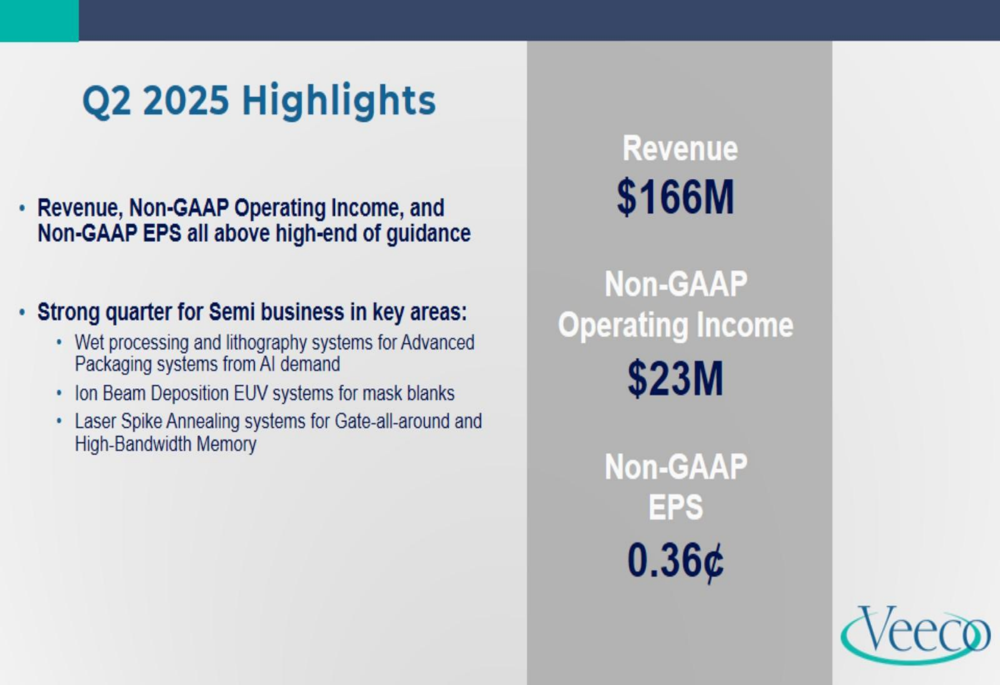

Veeco reported Q2 2025 revenue of $166.1 million, exceeding the high end of its guidance range of $135-$165 million. Non-GAAP operating income reached $23.1 million, with non-GAAP earnings per share of $0.36, also above the high end of guidance.

The semiconductor segment continued to be the company’s primary growth driver, accounting for 75% of total revenue in the quarter. Management highlighted strong performance across key product lines, including wet processing and lithography systems for advanced packaging, ion beam deposition EUV systems, and laser spike annealing systems for gate-all-around and high-bandwidth memory applications.

As shown in the following financial highlights slide:

The company’s GAAP earnings per share for the quarter was $0.20, with the difference between GAAP and non-GAAP figures primarily due to share-based compensation, amortization, and other adjustments as detailed in the reconciliation tables.

Semiconductor Market Positioning

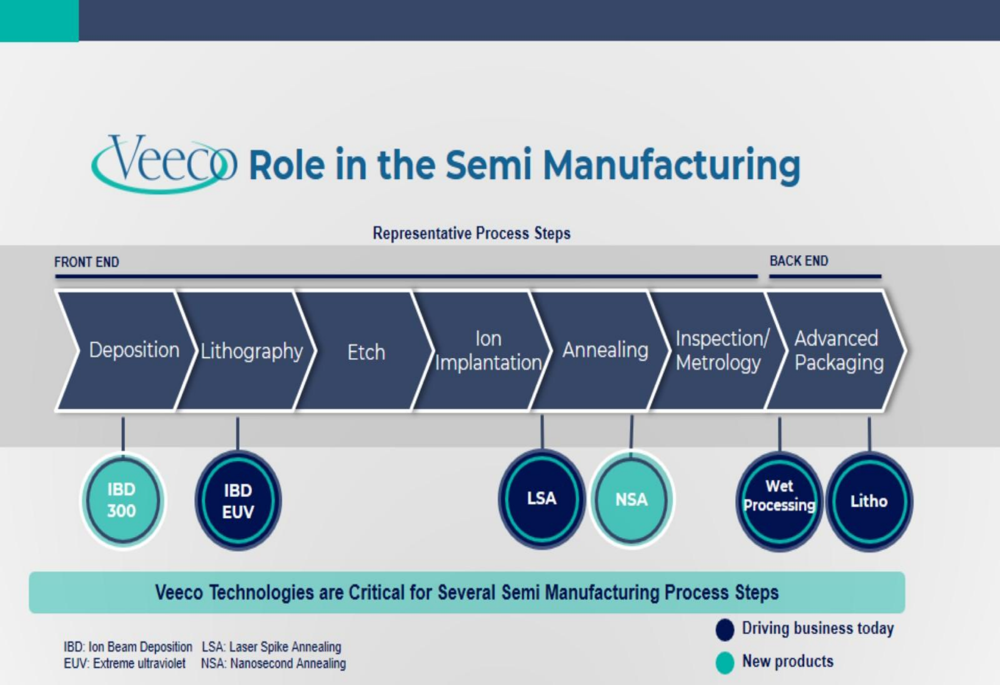

Veeco’s presentation emphasized its strategic positioning within the semiconductor manufacturing process, with technologies addressing both front-end and back-end applications. The company illustrated how its ion beam deposition (IBD), laser spike annealing (LSA), nano-scale annealing (NSA), and wet processing technologies fit into the semiconductor production workflow:

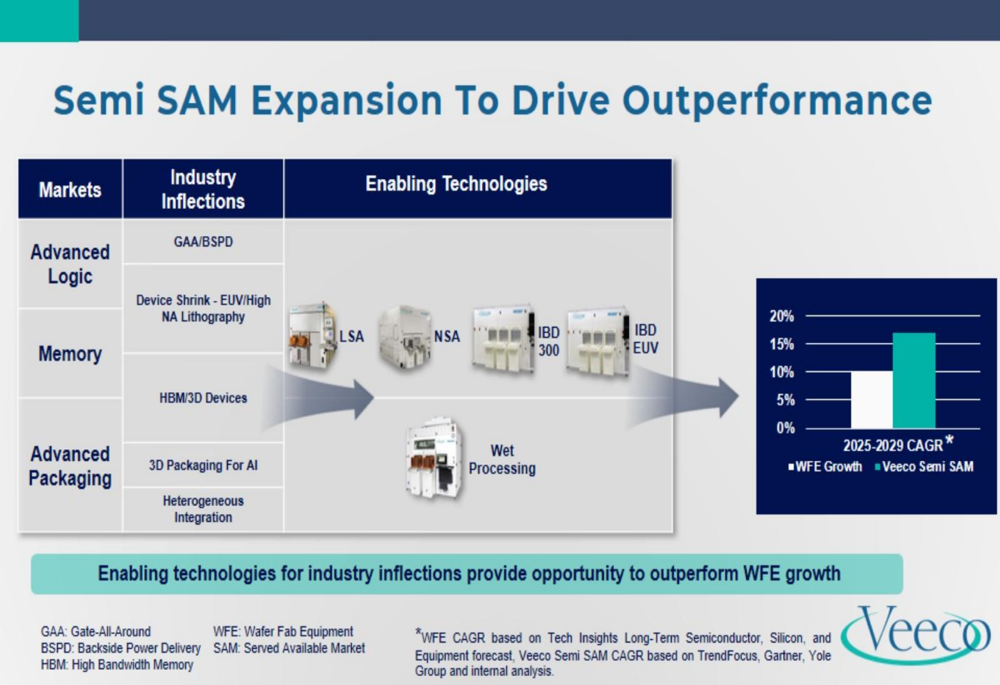

Management highlighted how industry inflections are driving expansion of Veeco’s served available market (SAM), positioning the company to outperform overall wafer fab equipment (WFE) growth. Key industry trends driving this growth include gate-all-around/backside power delivery for advanced logic, device shrink enabled by EUV/High NA lithography, high-bandwidth memory, and 3D packaging for AI applications.

This market expansion strategy is illustrated in the following chart:

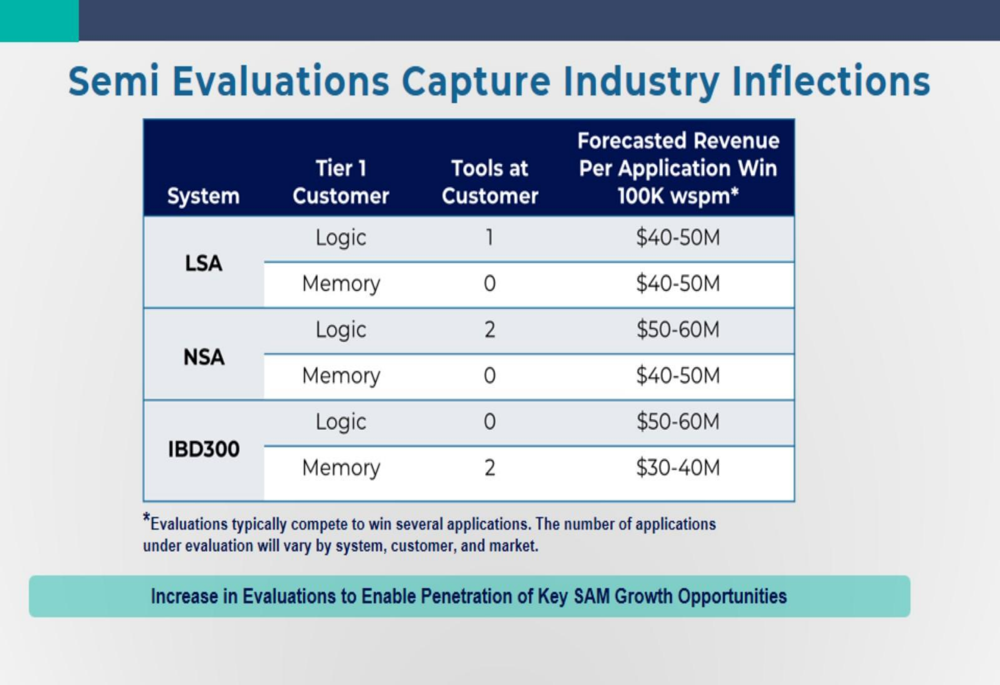

The company also detailed its progress with tier 1 customer evaluations across multiple product lines, which are expected to drive significant revenue opportunities upon successful qualification:

Detailed Financial Analysis

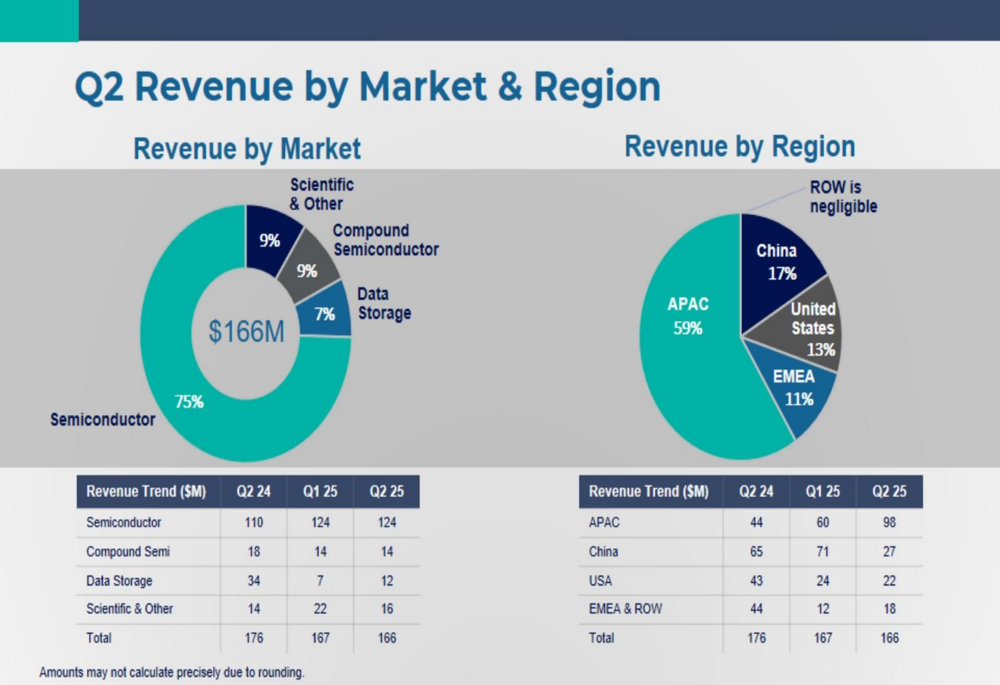

Veeco’s Q2 revenue breakdown shows the semiconductor segment’s dominance at 75% of total revenue, followed by compound semiconductor (9%), data storage (7%), and scientific & other applications (9%). Geographically, the Asia-Pacific region excluding China accounted for 59% of revenue, with China contributing 17%, the United States 13%, and EMEA 11%.

The detailed revenue breakdown by market and region is shown in the following slide:

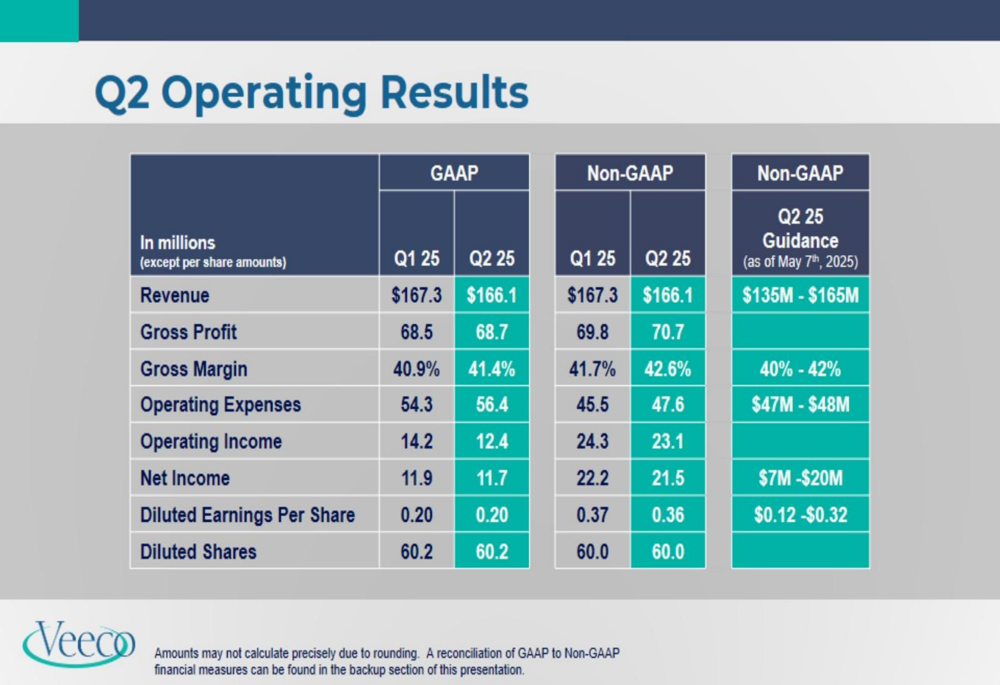

The company’s Q2 operating results show strong profitability, with a non-GAAP gross margin of 42.6% and non-GAAP operating income of $23.1 million, representing 13.9% of revenue:

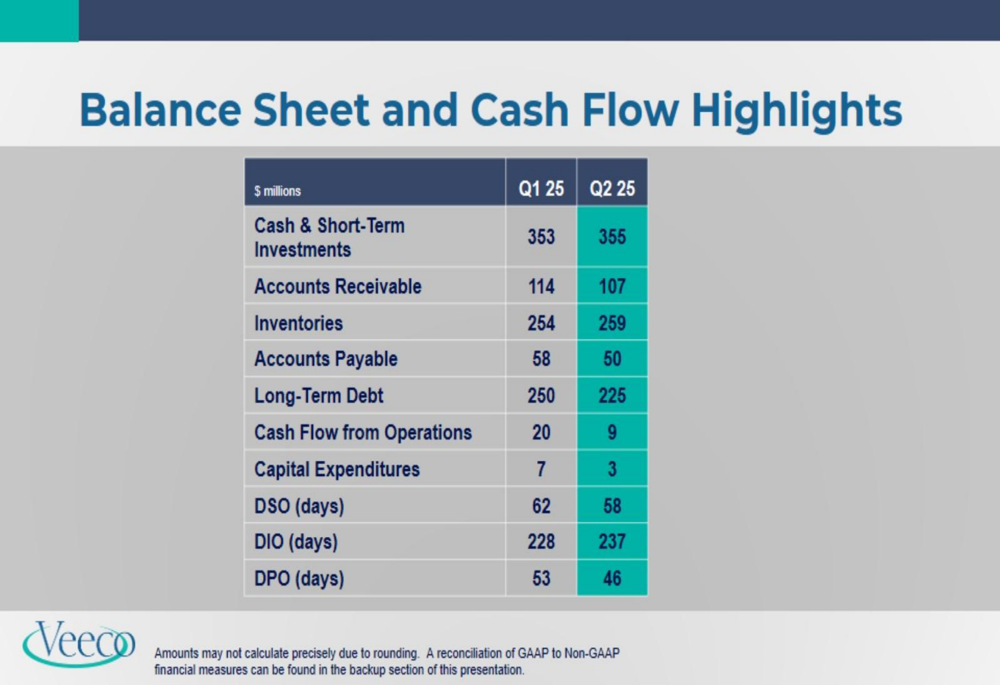

Veeco maintained a strong balance sheet with $355 million in cash and short-term investments and $225 million in long-term debt. The company generated $9 million in cash flow from operations during the quarter, while maintaining inventory levels that reflect ongoing supply chain management with days inventory outstanding (DIO) at 237 days:

Forward Guidance

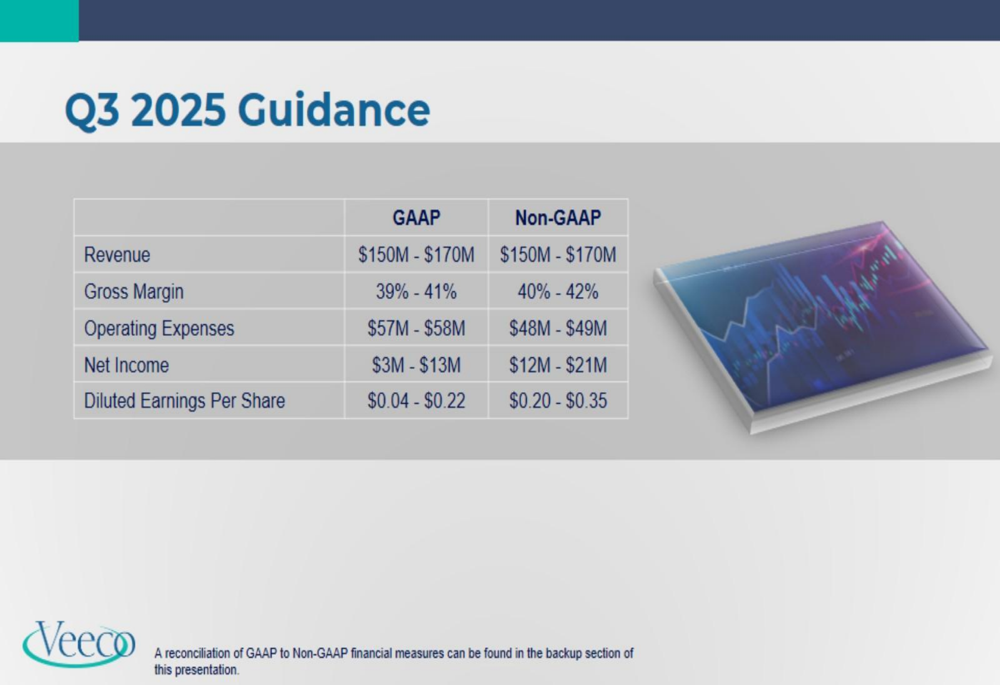

For Q3 2025, Veeco provided revenue guidance of $150-$170 million, with non-GAAP gross margin expected to be 40-42%. The company projects non-GAAP operating income of $13-$24 million and non-GAAP earnings per share of $0.20-$0.35.

The detailed Q3 guidance is presented in the following slide:

This guidance represents a potential sequential revenue range from a 9.7% decline to a 2.3% increase compared to Q2 results. While the midpoint suggests a slight sequential decline, it’s worth noting that this follows a quarter that exceeded expectations.

The guidance aligns with management’s commentary from the previous quarter about potential shipment delays to China, though specific updates on this situation weren’t highlighted in the current presentation. Despite these near-term fluctuations, the company remains focused on its long-term growth strategy tied to semiconductor industry inflections and expanding its served available market.

Veeco’s strategic positioning in high-growth semiconductor segments, particularly those related to AI applications, suggests the company is well-positioned to capitalize on industry trends despite potential quarter-to-quarter volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.