Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

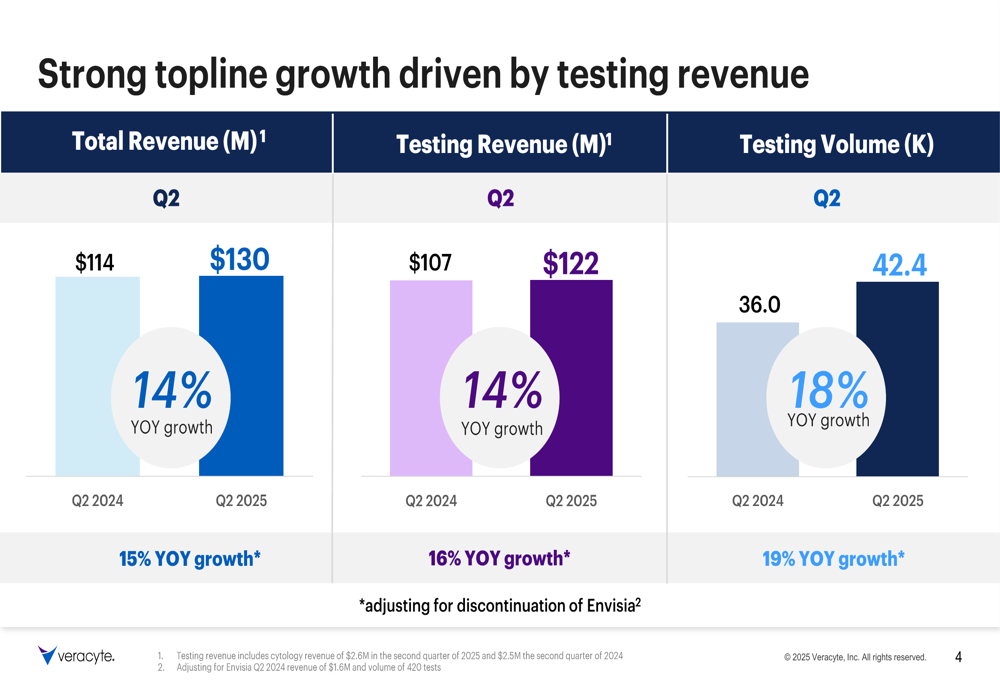

Veracyte Inc (NASDAQ:VCYT) released its second quarter 2025 earnings presentation on August 6, highlighting continued revenue growth driven by strong testing volumes despite posting a net loss due to a one-time impairment charge. The cancer diagnostics company reported a 14% year-over-year increase in total revenue, reaching $130 million for the quarter.

Following the announcement, Veracyte’s stock closed at $25.01, down 4.2% for the day, with minimal movement in after-hours trading. This represents a significant decline from the $32.22 level seen after the company’s Q1 2025 results, suggesting investors may be concerned about the transition to a net loss position despite underlying business strength.

Quarterly Performance Highlights

Veracyte’s Q2 2025 performance was characterized by double-digit growth in both revenue and testing volume. Total (EPA:TTEF) revenue reached $130 million, up 14% year-over-year from $114 million in Q2 2024. Testing revenue, which represents the core of Veracyte’s business, grew at the same rate to $122 million, compared to $107 million in the prior year period.

Testing volume showed even stronger growth, increasing 18% year-over-year to 42,400 tests in Q2 2025. The company maintained stable pricing, with average selling price (ASP) reported at $2,881, which was described as "roughly flat versus the prior year when adjusted for prior period collections."

As shown in the following chart of quarterly revenue and volume growth:

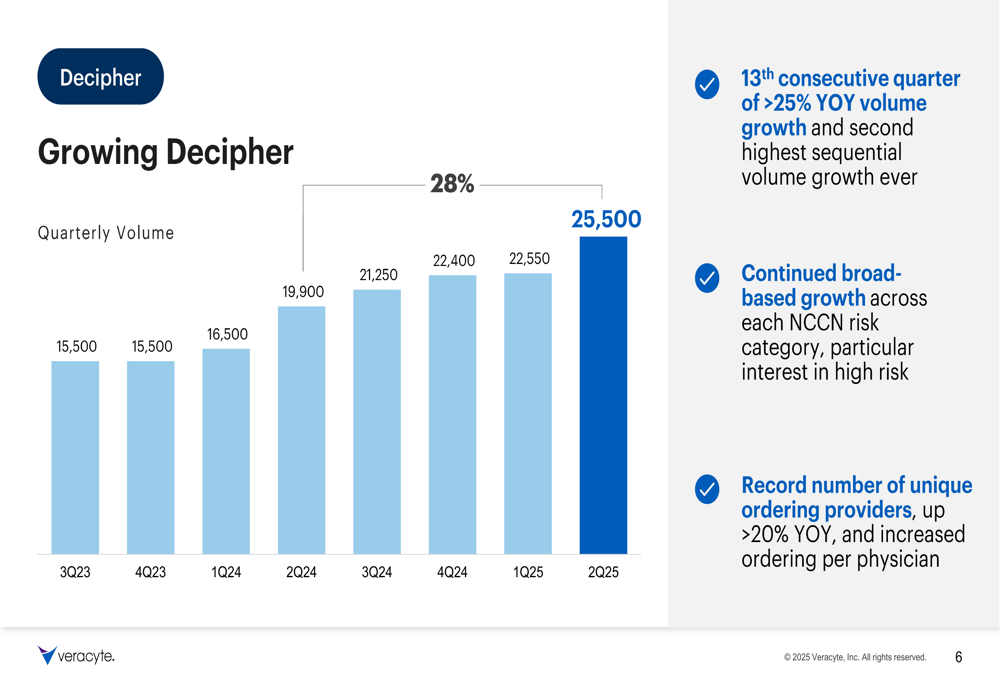

The Decipher prostate cancer test continues to be Veracyte’s strongest growth driver, with volume increasing 28% year-over-year to 25,500 tests in Q2 2025. This marks the 13th consecutive quarter of greater than 25% year-over-year volume growth for the product.

The company highlighted several factors contributing to Decipher’s performance, including its expansion into the metastatic patient population, increased ordering from physicians, and growing clinical evidence supporting its utility. The test is now being used across the entire risk spectrum of prostate cancer care.

As illustrated in the Decipher volume growth chart:

Meanwhile, Veracyte’s Afirma thyroid test showed more modest but still solid growth, with volume increasing 8% year-over-year to 16,950 tests in Q2 2025. The company noted increased year-over-year utilization per account and growing traction with Afirma GRID.

Detailed Financial Analysis

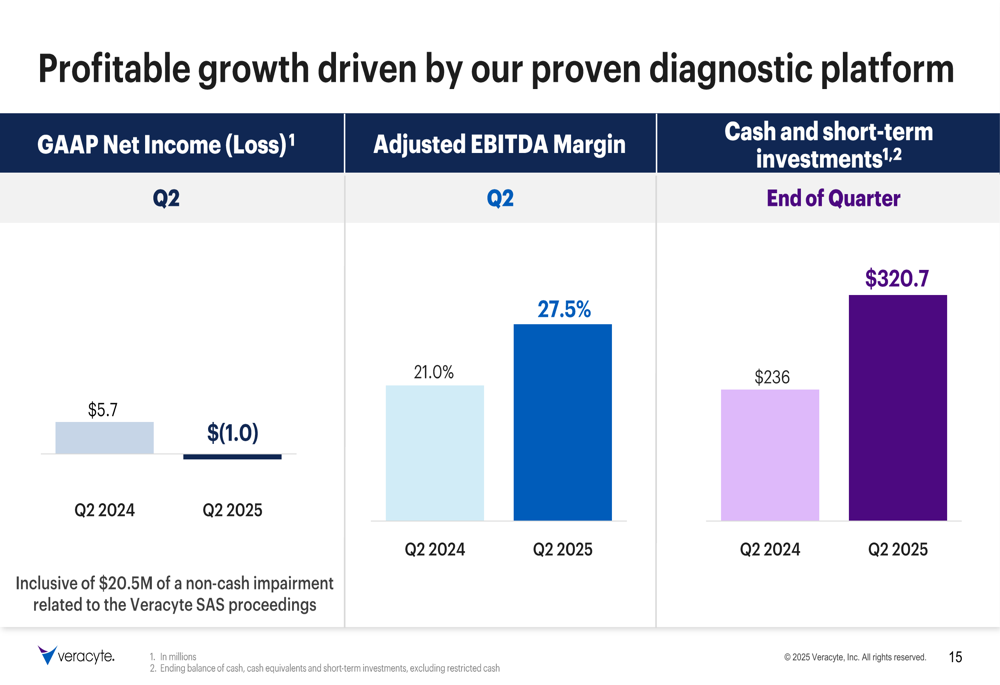

Despite the strong revenue growth, Veracyte reported a GAAP net loss of $1.0 million for Q2 2025, compared to net income of $5.7 million in Q2 2024. This shift to a loss position was primarily due to a $20.5 million non-cash impairment charge related to the company’s French subsidiary, Veracyte SAS.

However, the company’s adjusted EBITDA margin showed significant improvement, increasing to 27.5% in Q2 2025 from 21.0% in the prior year period. This suggests that the underlying operational efficiency of the business continues to strengthen despite the one-time impairment charge.

Veracyte also maintained a strong balance sheet, with cash and short-term investments increasing to $320.7 million at the end of Q2 2025, compared to $236 million a year earlier.

The following chart illustrates these key profitability metrics:

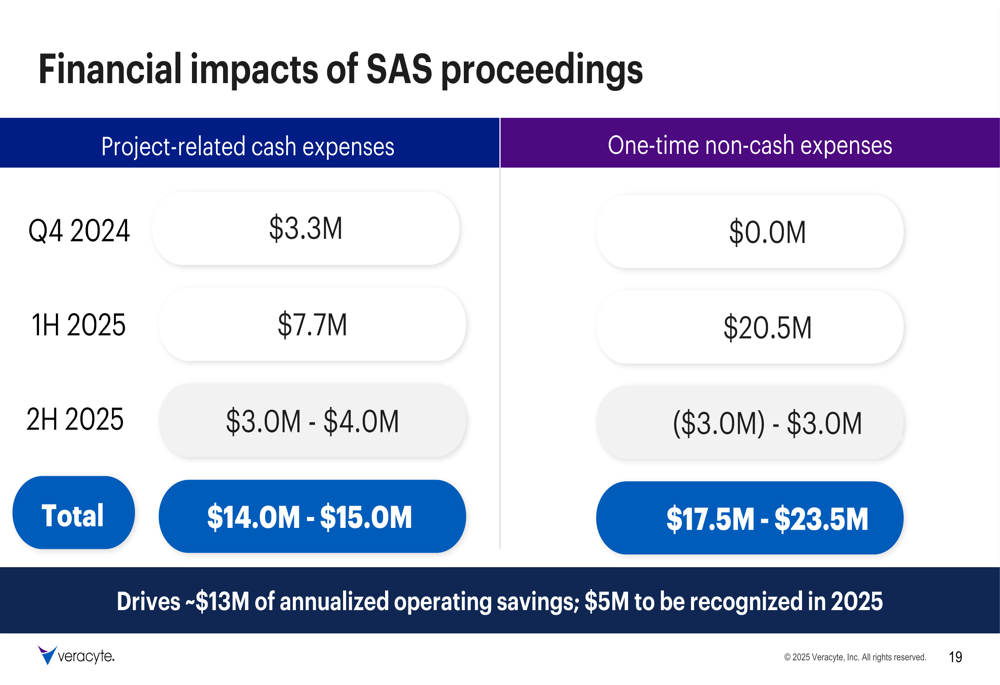

The company provided details on the financial impacts of the SAS proceedings, which include both cash expenses and non-cash charges. The total project-related cash expenses are expected to be $14.0-15.0 million, while one-time non-cash expenses are projected at $17.5-23.5 million. Importantly, Veracyte expects these changes to drive approximately $13 million in annualized operating savings, with $5 million to be recognized in 2025.

Strategic Initiatives

Veracyte outlined several strategic growth drivers in its presentation, focusing on expanding its test portfolio and geographic reach. Key initiatives include:

1. Continuing to grow U.S. CLIA tests with Decipher, Afirma, and Prosigna

2. Serving more of the patient journey with Minimal Residual Disease (MRD) testing

3. Expanding geographically with In Vitro Diagnostics (IVD)

4. Developing new cancer diagnostics with the Nasal Swab test

5. Improving operational efficiency through transition to v2 Veracyte transcriptome

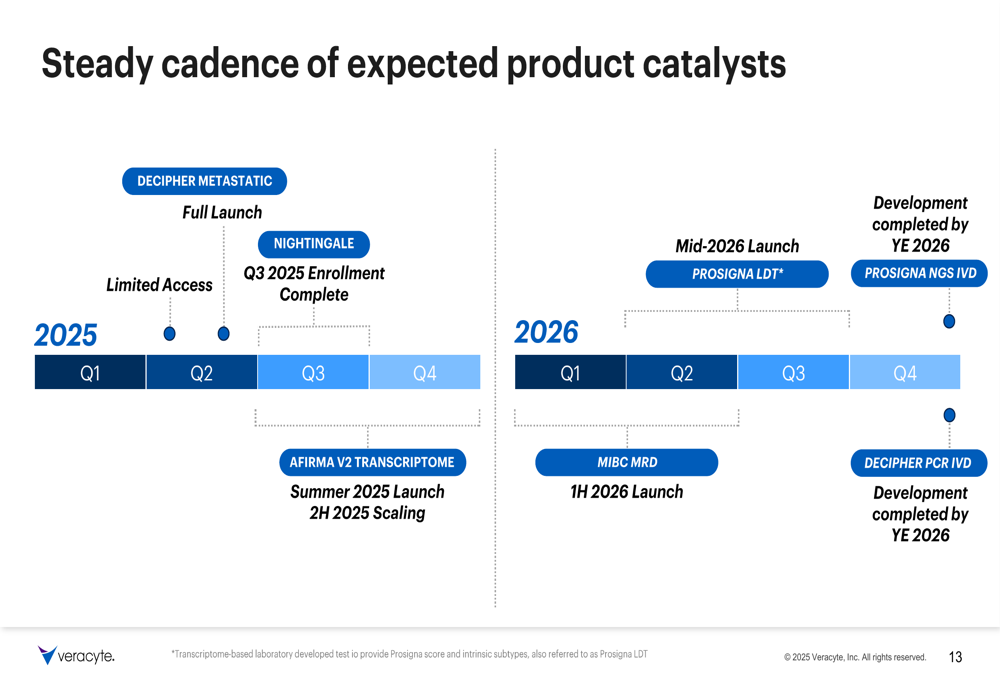

The company provided a timeline of expected product catalysts for 2025 and 2026, including the full launch of Decipher Metastatic, completion of Nightingale enrollment, launch of Afirma v2 Transcriptome, and introduction of new products such as MIBC MRD and Prosigna LDT.

As shown in the product catalysts timeline:

Veracyte also highlighted its progress on geographic expansion, noting that the sale of its contract manufacturing business closed on August 1st. The company remains on track to complete development for both IVD launches (Decipher on PCR and Prosigna on NGS) by the end of 2026.

Forward-Looking Statements

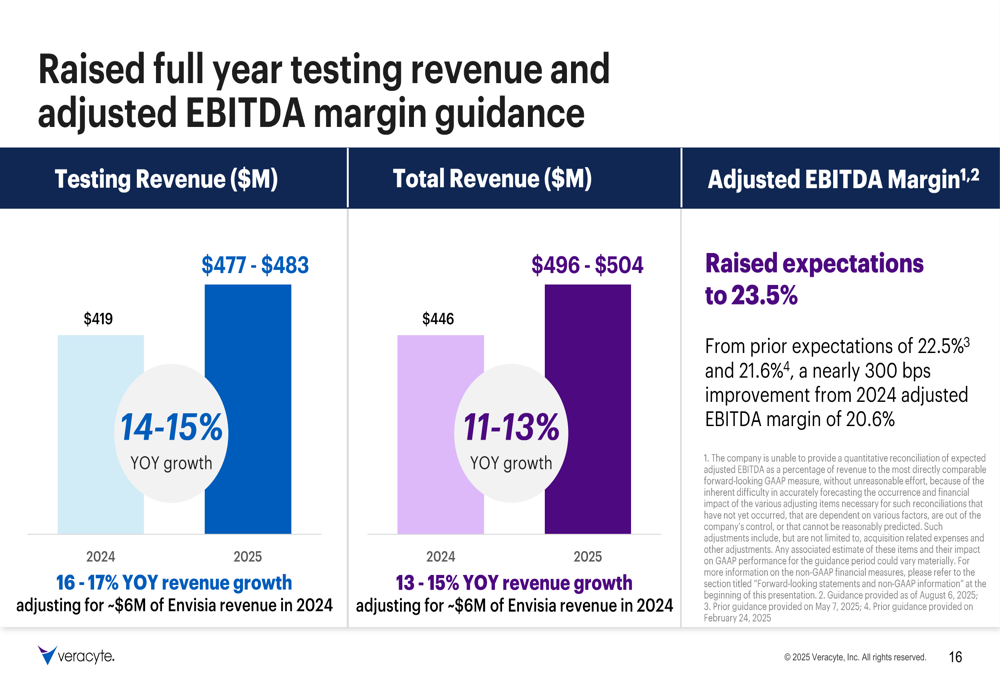

Veracyte raised its full-year 2025 adjusted EBITDA margin guidance to 23.5%, while maintaining its revenue growth expectations. The company projects testing revenue of $477-483 million for 2025, representing 14-15% year-over-year growth, and total revenue of $496-504 million, representing 11-13% growth.

The following chart illustrates Veracyte’s full-year guidance:

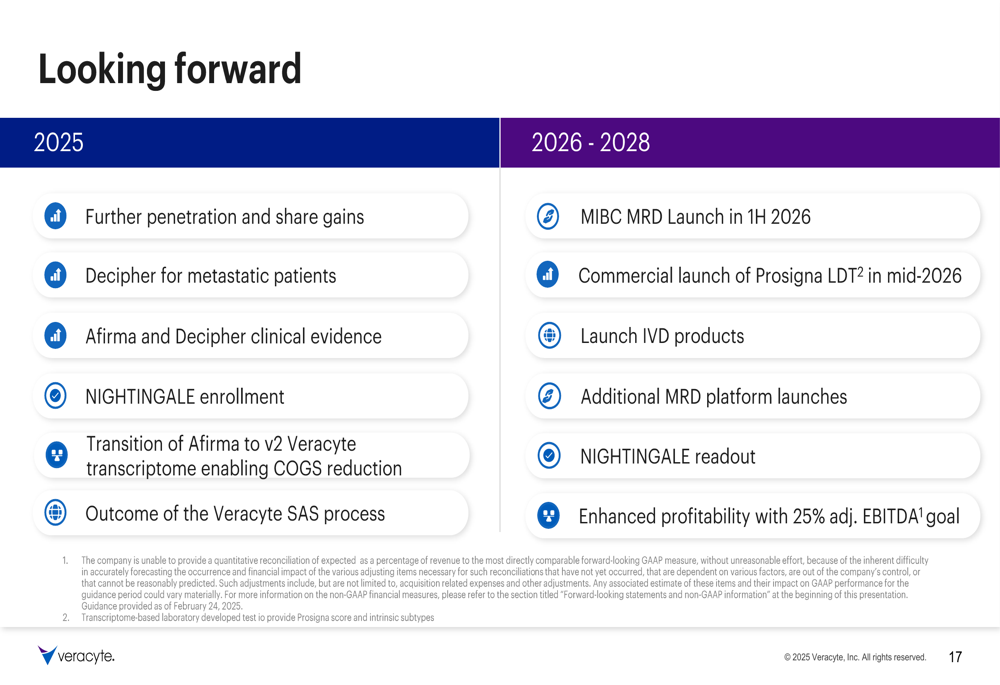

Looking beyond 2025, Veracyte outlined its focus areas for 2026-2028, including the launch of MIBC MRD in the first half of 2026, commercial launch of Prosigna LDT in mid-2026, launch of IVD products, additional MRD platform launches, and NIGHTINGALE readout. The company also set a goal of achieving 25% adjusted EBITDA margin during this period.

Overall, Veracyte’s Q2 2025 presentation depicts a company with strong underlying business performance and growth, temporarily affected by a one-time impairment charge. The continued expansion of testing volumes, particularly for the Decipher product, and improving adjusted EBITDA margins suggest the company’s core operations remain on a positive trajectory despite the near-term financial impact of the SAS proceedings.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.