US stock futures flounder amid tech weakness, Fed caution

Veralto Corporation (NYSE:VLTO) reported solid second-quarter 2025 results on July 28, demonstrating continued sales momentum and strong cash flow generation while raising its full-year guidance. The company’s stock rose 0.7% to $104 in after-hours trading following the release.

Quarterly Performance Highlights

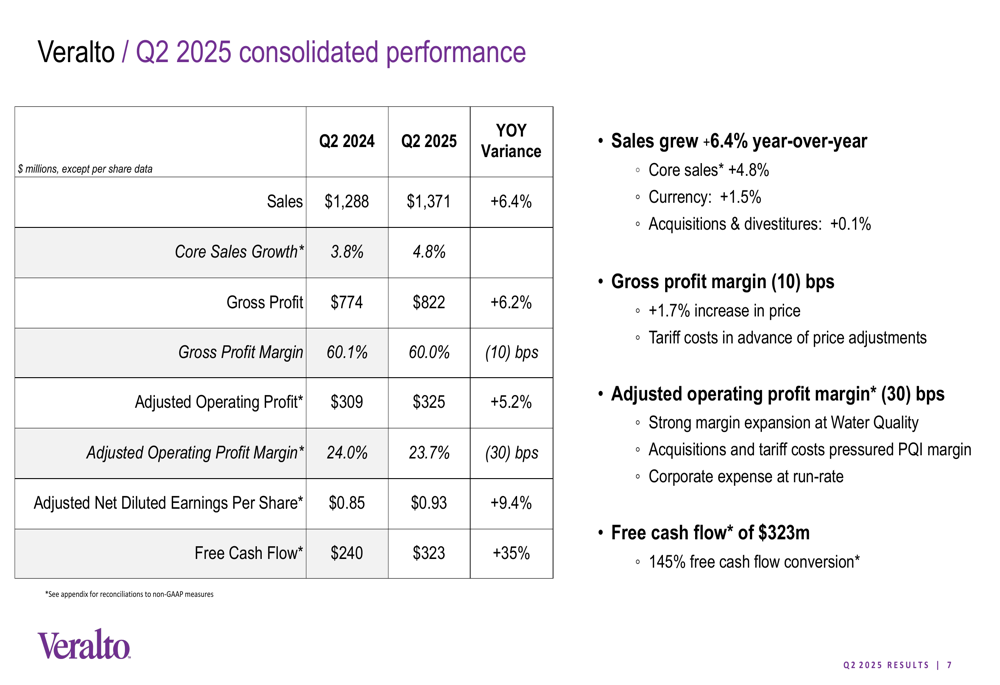

Veralto delivered Q2 2025 sales of $1,371 million, representing 6.4% year-over-year growth with core sales increasing by 4.8%. The growth was driven by both volume (+3.1%) and price (+1.7%) improvements across its business segments. Adjusted earnings per share reached $0.93, up 9.4% compared to the prior year, while free cash flow surged 35% to $323 million.

"Q2 2025 performance reflects durable sales and earnings per share growth," noted the company in its presentation, highlighting the strength of its business model despite some margin pressure.

As shown in the following consolidated performance overview:

While the company maintained strong top-line growth, there was slight margin compression with gross profit margin declining 10 basis points to 60.0% and adjusted operating profit margin decreasing 30 basis points to 23.7% compared to Q2 2024. This represents a sequential decline from Q1 2025, when the company reported a gross profit margin of 60.4% and an all-time high adjusted operating profit margin of 25%.

Segment Analysis

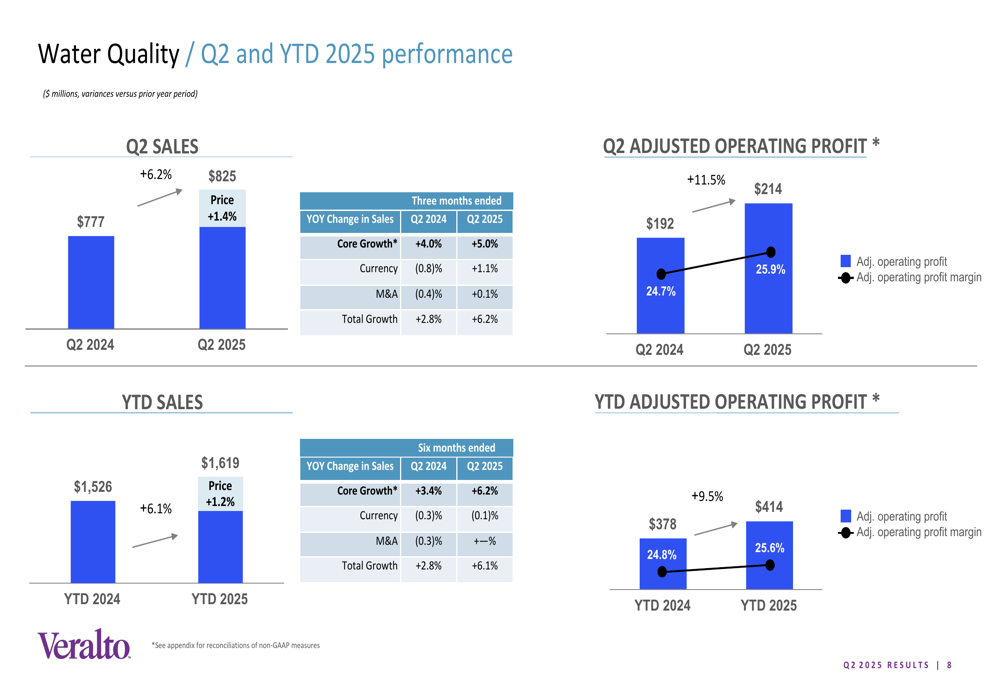

Veralto’s business is divided into two main segments: Water Quality and Product Quality & Innovation, with distinctly different performance profiles in the quarter.

The Water Quality segment, which contributed approximately 60% of total sales, posted strong results with sales of $825 million, up 6.2% year-over-year. More impressively, the segment’s adjusted operating profit increased 11.5% to $214 million, with margins expanding by 120 basis points to 25.9%.

The segment’s performance is illustrated in the following chart:

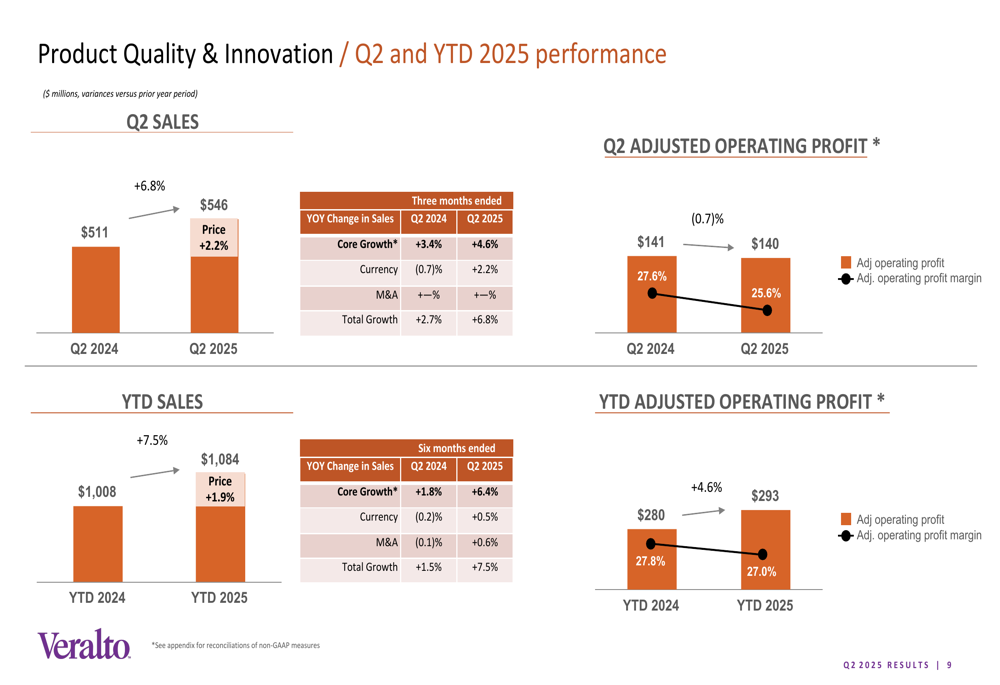

In contrast, the Product Quality & Innovation segment showed mixed results. While sales grew 6.8% to $546 million, adjusted operating profit declined slightly by 0.7% to $140 million, with margins contracting significantly from 27.6% to 25.6% year-over-year.

The following chart details the segment’s performance:

This divergence in segment profitability suggests that while Veralto is successfully growing revenue across both business lines, cost pressures are having a more pronounced impact on the Product Quality & Innovation segment.

Regional Performance

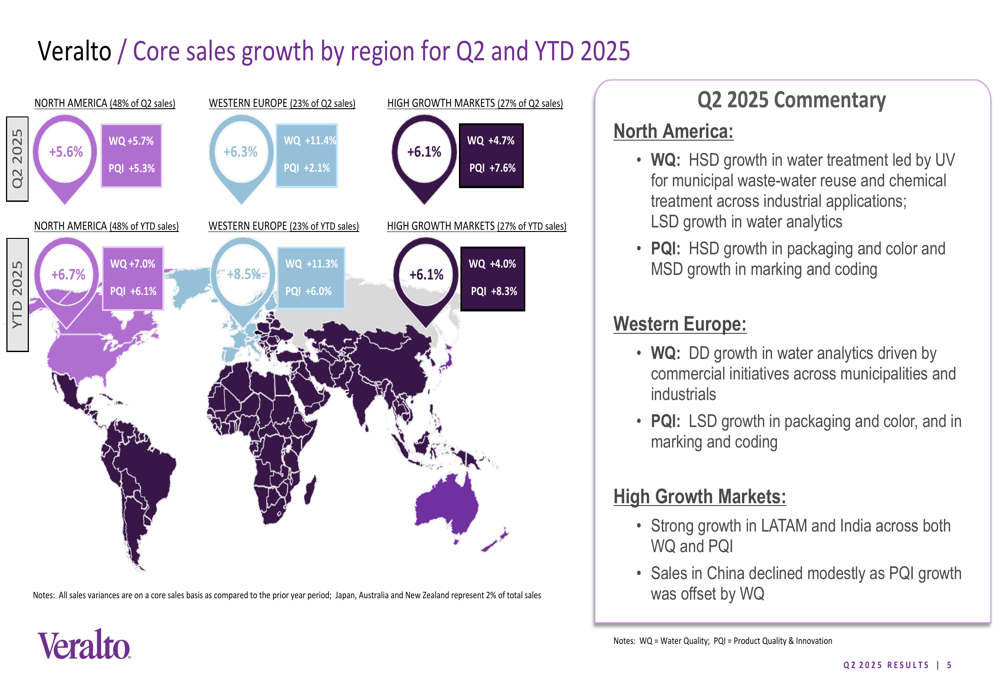

Veralto demonstrated broad-based geographic growth, with particularly strong performance in Western Europe. The company’s regional breakdown reveals varied growth rates across its global footprint.

As illustrated in the following regional performance map:

North America, representing 48% of Q2 sales, showed solid growth with Water Quality up 5.7% and Product Quality & Innovation up 5.3%. Western Europe, accounting for 23% of sales, was a standout performer with Water Quality surging 11.4%, though Product Quality & Innovation growth was more modest at 2.1%.

High Growth Markets, contributing 27% of sales, showed strength in Latin America and India, with Water Quality growing 4.7% and Product Quality & Innovation up 7.6%. However, the company noted a modest decline in China, which could be a potential area of concern for future quarters.

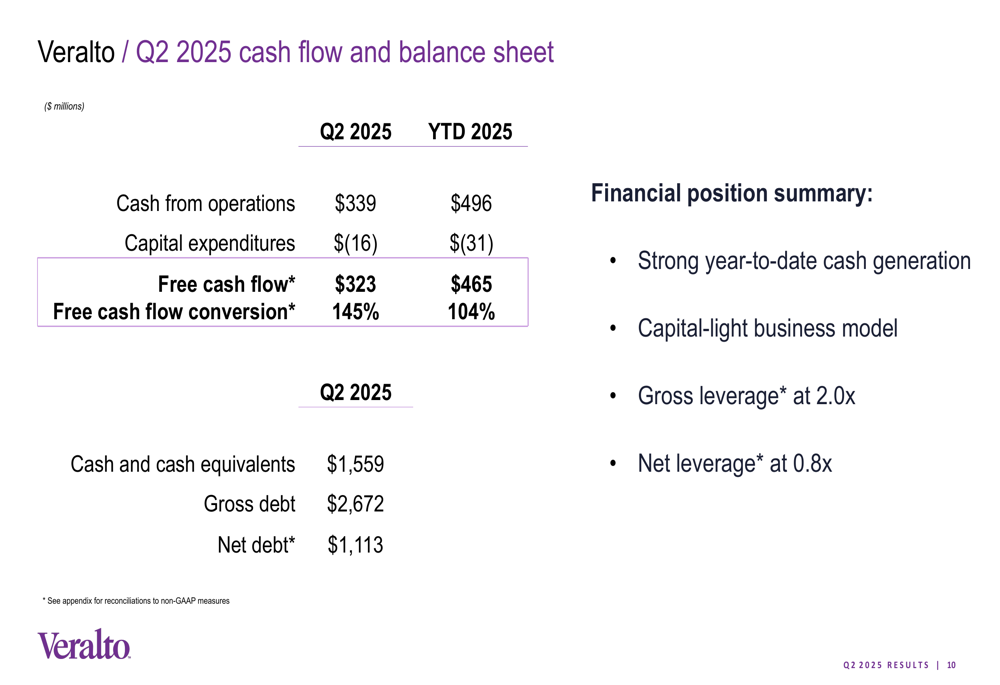

Financial Position & Cash Flow

Veralto maintained a strong financial position in Q2 2025, generating $339 million in cash from operations and $323 million in free cash flow, representing a robust 145% free cash flow conversion rate.

The company’s balance sheet remains healthy with $1,559 million in cash and cash equivalents against $2,672 million in gross debt, resulting in net debt of $1,113 million. This translates to a comfortable net leverage ratio of 0.8x, providing Veralto with significant financial flexibility.

The following slide details the company’s cash flow and balance sheet highlights:

This strong cash generation underscores Veralto’s capital-light business model and its ability to convert earnings into cash, a key strength highlighted in previous earnings reports.

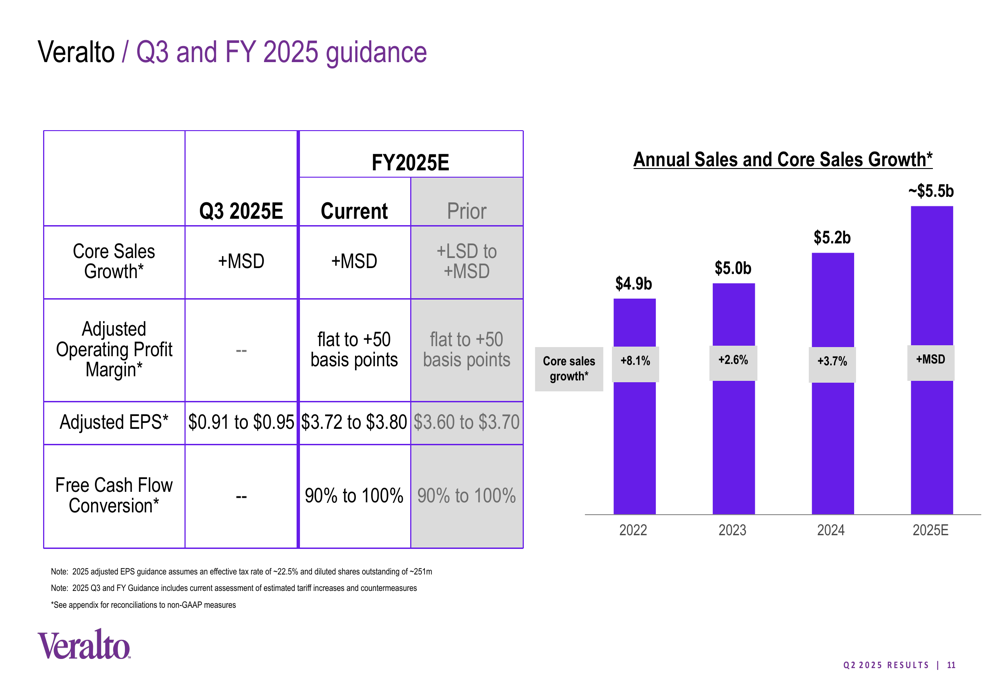

Updated Guidance & Outlook

In a significant vote of confidence in its business outlook, Veralto raised its full-year 2025 guidance. The company now expects mid-single-digit core sales growth for the full year, up from its previous guidance of low-to-mid-single-digit growth. Adjusted EPS guidance was also increased to $3.72-$3.80, compared to the prior range of $3.60-$3.70.

For Q3 2025, Veralto projects mid-single-digit core sales growth and adjusted EPS of $0.91-$0.95.

The following guidance summary provides a comprehensive view of the company’s expectations:

The guidance upgrade follows a similar pattern to Q1 2025, when the company also exceeded analyst expectations. According to the previous earnings report, Veralto had projected adjusted EPS between $3.60 and $3.70 for the full year 2025, with core sales growth in the low to mid-single digits.

The company’s annual sales trajectory shows consistent growth from $4.9 billion in 2022 to an expected $5.5 billion in 2025, representing steady expansion of its market presence.

Strategic Positioning

Veralto continues to position itself as a company focused on "safeguarding the world’s most vital resources," leveraging secular growth drivers and its proven value creation approach.

As illustrated in the company’s strategic positioning slide:

The company’s emphasis on its durable business model and attractive secular growth drivers appears to be resonating with investors, as evidenced by the positive after-hours stock movement following the earnings release.

With its raised guidance, strong cash flow generation, and solid sales growth across segments and regions, Veralto demonstrates confidence in its ability to navigate the current economic environment while continuing to deliver shareholder value through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.