ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Finnish electronics retailer Verkkokauppa.com Oyj (HEL:VERK) presented its Q2 2025 results on July 17, highlighting a strong performance despite lingering market challenges. The company reported significant revenue growth and a return to profitability in what it describes as a "cautiously recovering market."

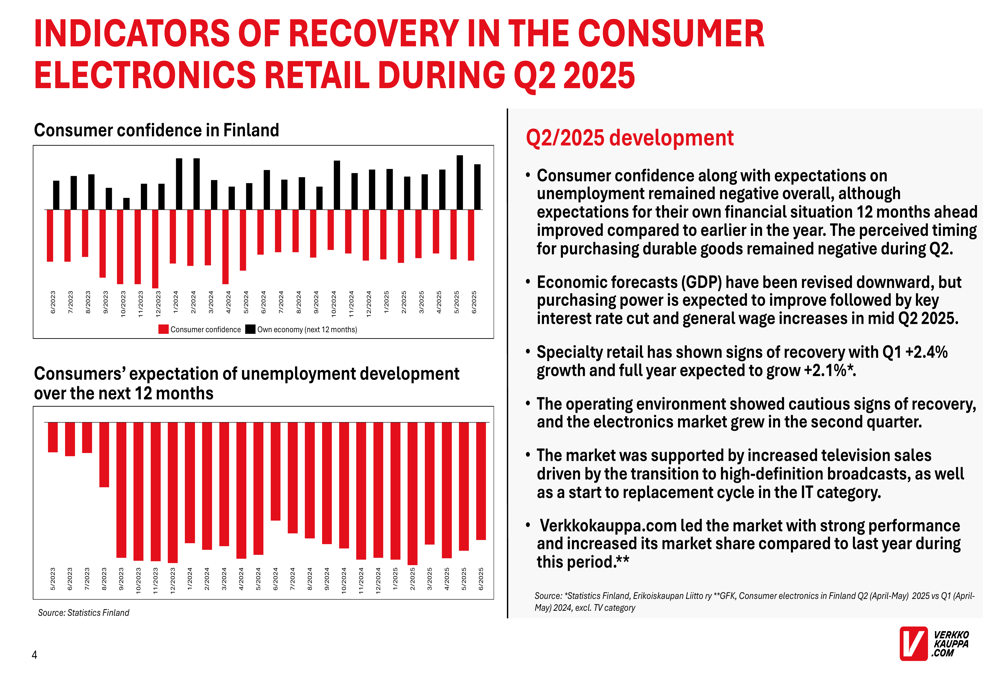

Consumer confidence in Finland remains negative overall, though the company noted some improvement in consumers’ expectations for their personal financial situations. While economic forecasts have been revised downward, purchasing power is expected to improve, and the specialty retail sector showed recovery with 2.4% growth in Q1.

The electronics market specifically grew in Q2, supported by increased television sales due to the transition to high-definition broadcasts and a replacement cycle in the IT category. Against this backdrop, Verkkokauppa.com claims to have led the market with strong performance and increased market share.

As shown in the following chart illustrating market indicators:

Quarterly Performance Highlights

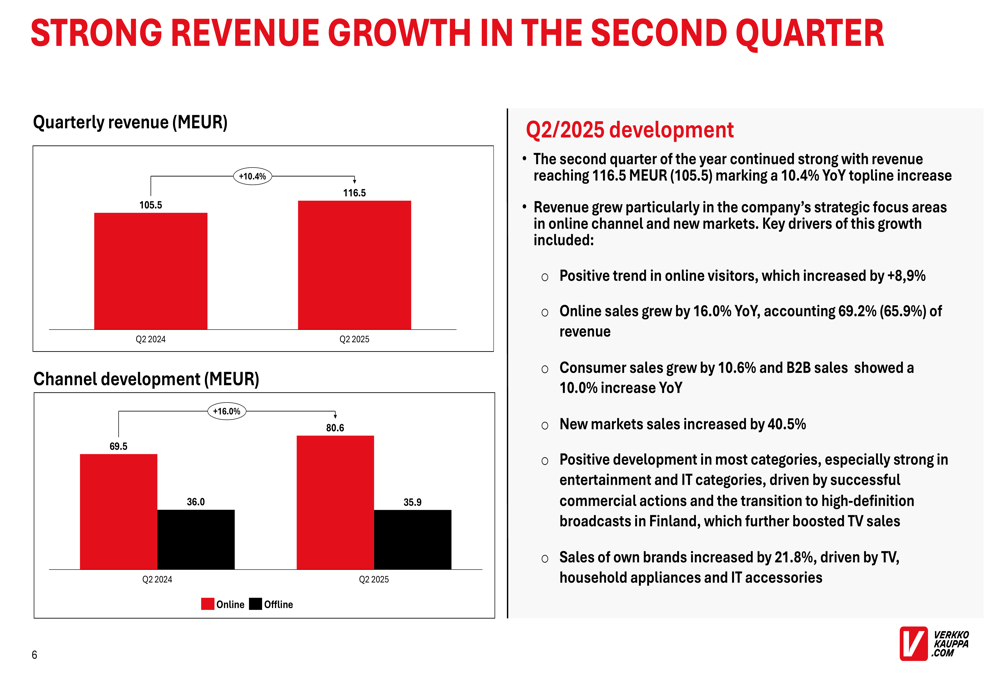

Verkkokauppa.com reported revenue of €116.5 million for Q2 2025, representing a 10.4% increase compared to €105.5 million in Q2 2024. This growth was primarily driven by online sales, which surged 16.0% year-over-year to €80.6 million and accounted for 69.2% of total revenue. Meanwhile, offline sales remained relatively stable at €35.9 million.

The following chart illustrates this revenue growth and channel development:

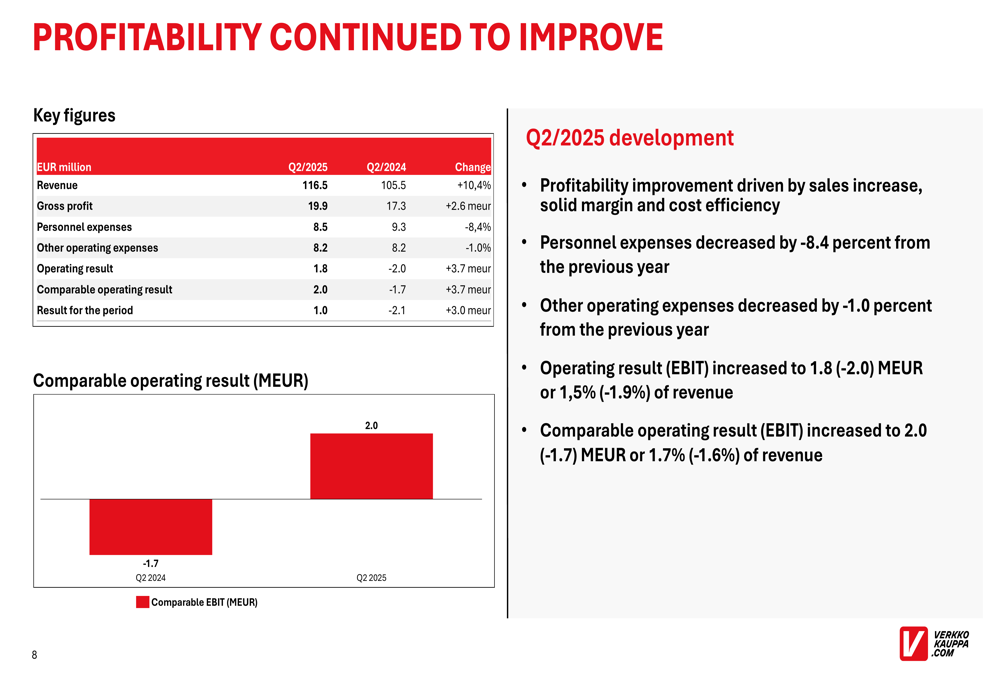

The company’s profitability showed marked improvement, with operating result (EBIT) increasing to €1.8 million, compared to a loss of €2.0 million in the same period last year. The comparable operating result reached €2.0 million, up from a loss of €1.7 million in Q2 2024.

Consumer sales grew by 10.6% and B2B sales by 10.0%, while new markets sales increased by an impressive 40.5%. The company also reported positive development in entertainment and IT categories, driven by high-definition broadcast transitions.

Detailed Financial Analysis

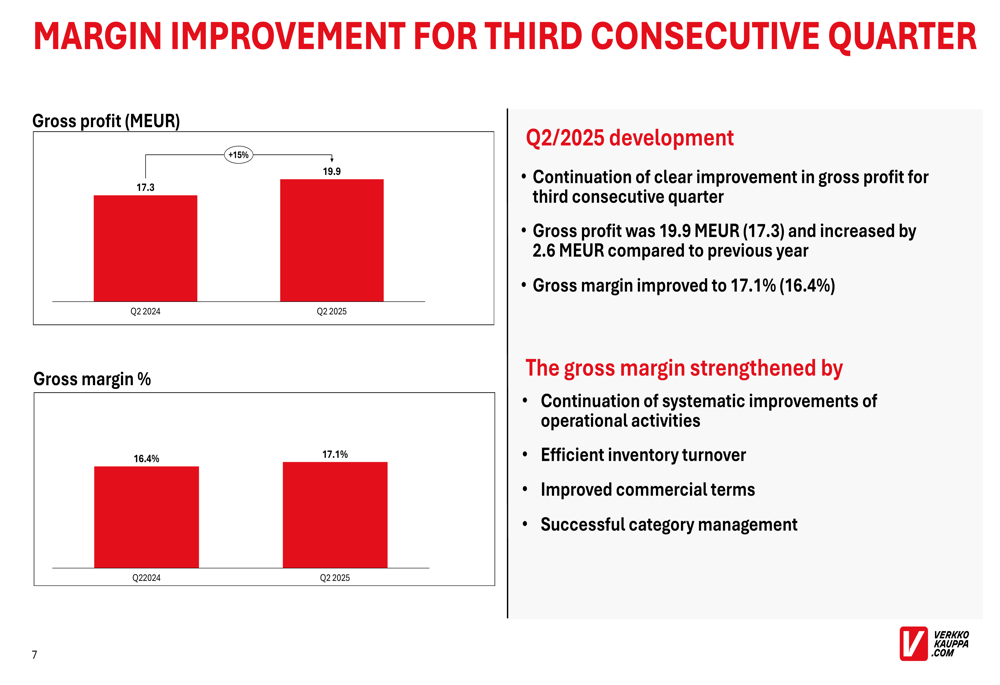

Gross profit for Q2 2025 reached €19.9 million, a 15% increase from €17.3 million in Q2 2024. The gross margin improved to 17.1%, up from 16.4% in the previous year, marking the third consecutive quarter of margin improvement.

This margin improvement is illustrated in the following chart:

The company attributed its profitability improvement to a combination of sales increases, solid margins, and cost efficiency measures. Personnel expenses decreased by 8.4% year-over-year, while other operating expenses decreased by 1.0%.

The comprehensive financial performance is shown in this table:

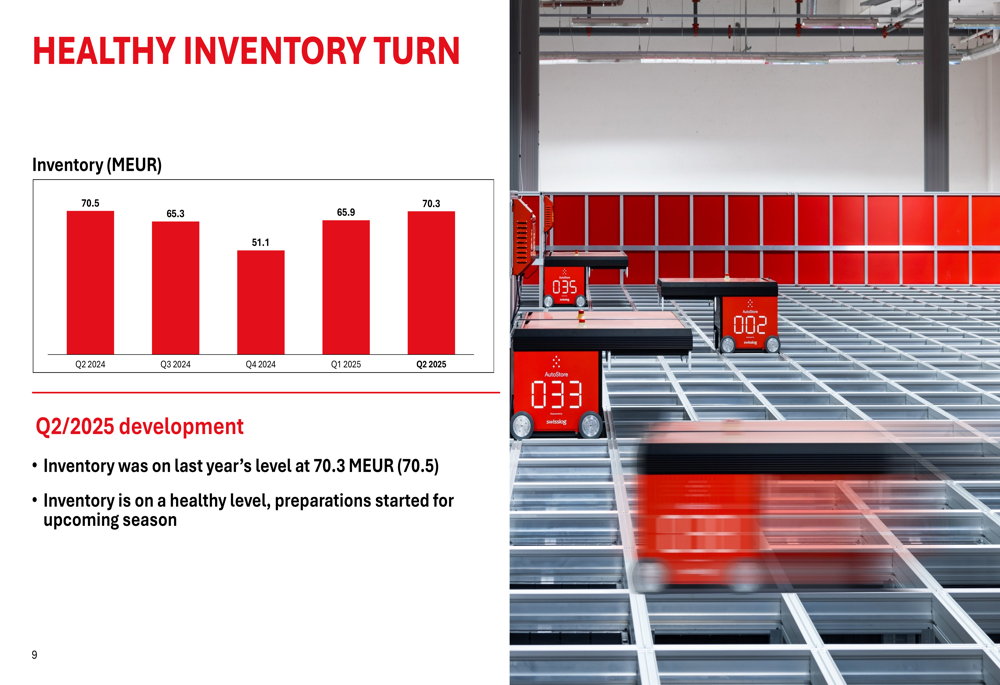

Inventory levels remained healthy at €70.3 million, slightly below the €70.5 million reported in Q2 2024. The company noted that preparations for the upcoming season have begun.

The inventory trend is illustrated in the following chart:

Cash flow from operations totaled -€0.3 million, down from €2.2 million in Q2 2024. However, the equity ratio improved to 18.3% from 15.7% a year earlier. Cash at hand stood at €16.1 million at the end of June 2025, compared to €16.3 million a year ago. Investments amounted to €1.1 million, primarily related to IT infrastructure updates and fast delivery capabilities.

Strategic Initiatives

Verkkokauppa.com announced a significant strategic move during the quarter: an agreement to sell its consumer financing business to Norion Bank AB and its payment solutions unit Walley for approximately €34 million. The transaction is expected to result in a non-recurring gain of about €3 million and will significantly improve the company’s balance sheet structure. The deal is expected to be completed during the second half of 2025.

The company continues to focus on three key strategic initiatives: fast deliveries, own brands, and international expansion.

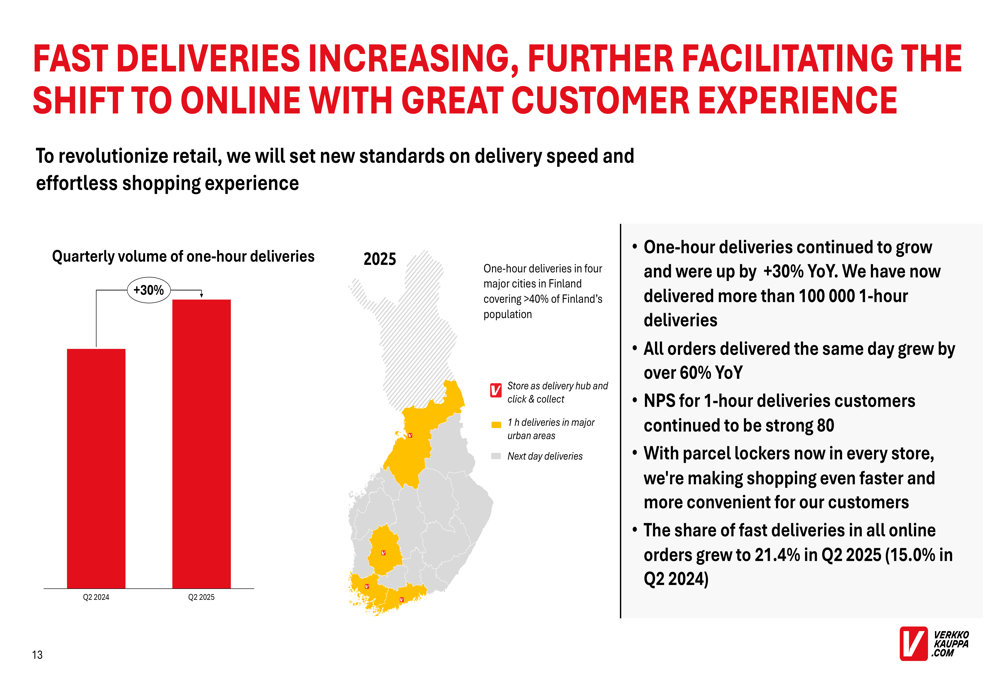

One-hour deliveries grew by 30% year-over-year, with over 100,000 deliveries completed in Q2. All orders delivered the same day grew by over 60% year-over-year. The share of fast deliveries increased to 21.4% in Q2 2025, up from 15.0% in Q2 2024.

The growth in fast deliveries is shown in this chart:

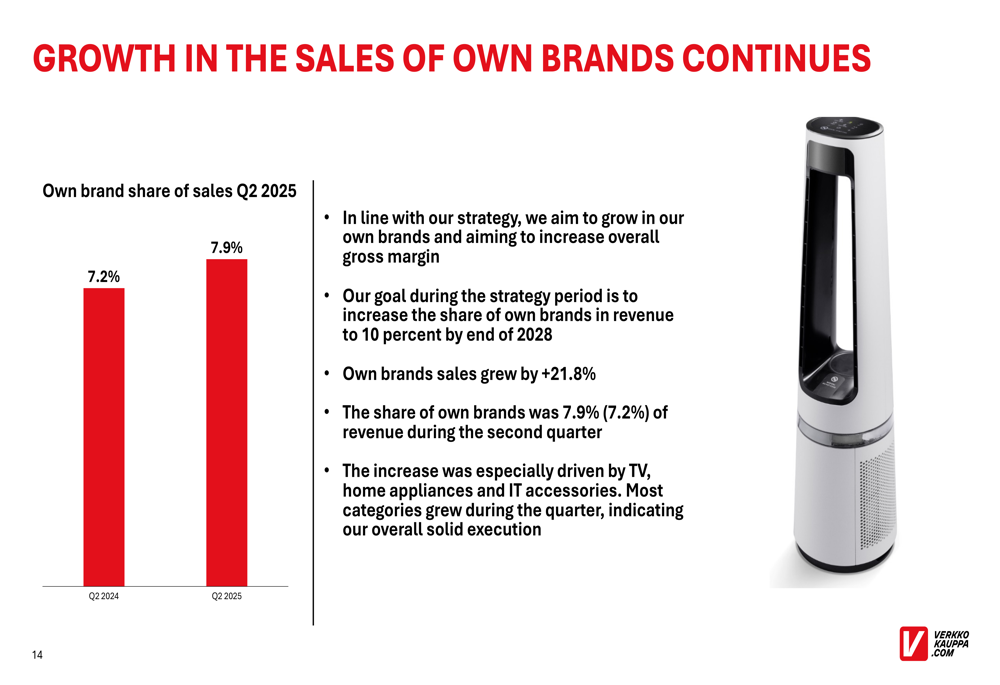

Sales of own brands grew by 21.8% year-over-year, with their share of revenue increasing to 7.9% from 7.2% in Q2 2024. The company aims to increase the share of own brands to 10% of revenue by the end of 2028 as part of its strategy to improve overall gross margin.

The following chart illustrates the growth in own brand sales:

International sales grew by 40.5% year-over-year, driven by strong sales through European partners and good momentum in Nordic markets. The company also began selling through Amazon (NASDAQ:AMZN) Sweden in the latter part of Q2, though this initiative is still in the ramp-up phase.

Forward-Looking Statements

Verkkokauppa.com maintained its guidance for 2025, expecting both revenue and comparable operating result to increase compared to 2024, when the company reported revenue of €467.8 million and a comparable operating result of €1.8 million.

The company noted that general market demand is expected to remain cautious due to uncertainties impacting consumer confidence. Despite these challenges, private consumption is forecasted to recover as purchasing power strengthens. Competition is expected to remain tight and the geopolitical environment uncertain.

Verkkokauppa.com believes it can take advantage of the ongoing shift to online business and improve its market position. The company emphasized that its business is seasonal, with revenue and operating profit depending largely on fourth-quarter sales.

Following the earnings presentation, Verkkokauppa.com’s stock (HEL:VERK) was trading at €3.06, down 2.24% on July 16, 2025. The stock has shown significant volatility, with a 52-week range of €1.27 to €3.15, suggesting investors are still assessing the company’s recovery trajectory and long-term growth potential.

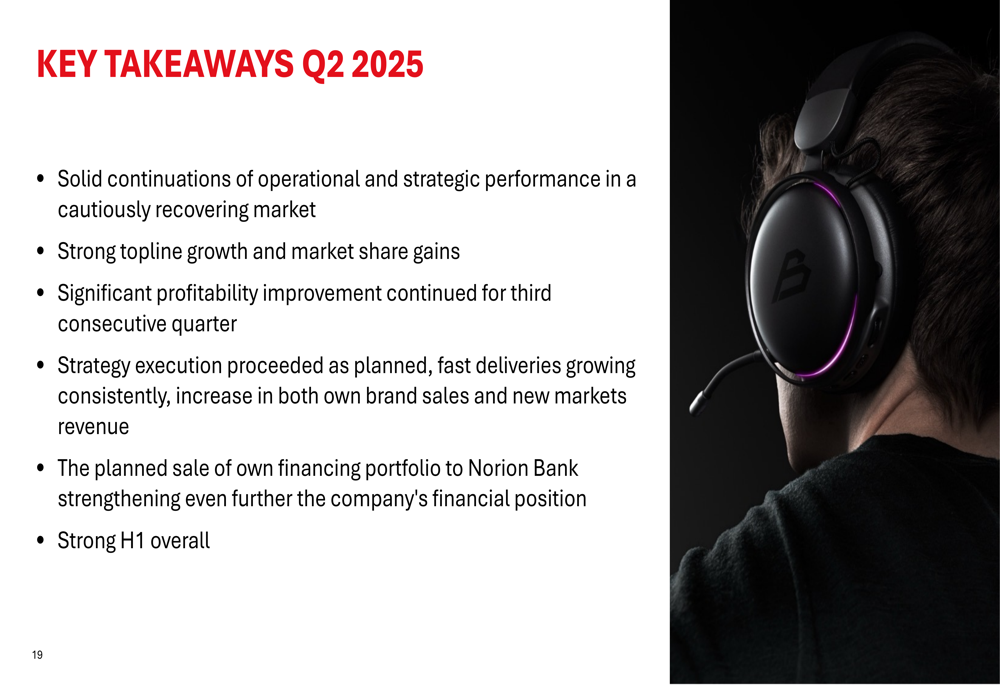

The company summarized its Q2 performance with these key takeaways:

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.