Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

Vestas Wind Systems A/S (ETR:VWSB) (CPH:VWS), the world’s leading wind turbine manufacturer, reported a strong start to 2025 with significant revenue growth and a return to profitability despite seasonal challenges. The company presented its first quarter results on May 6, 2025, highlighting its continued market leadership in an evolving industry landscape.

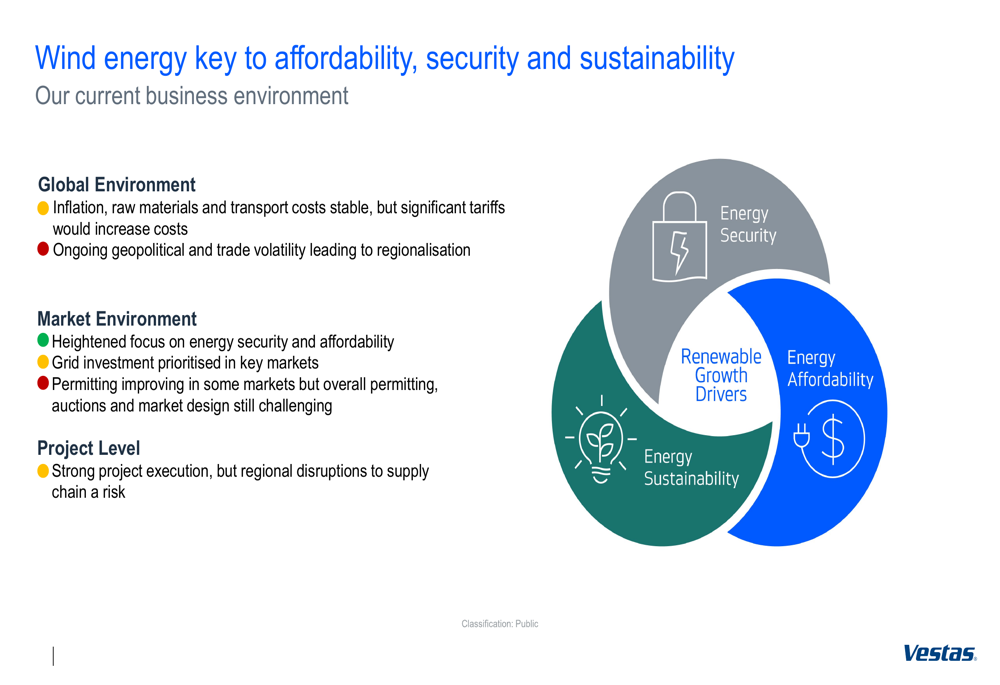

The wind energy sector continues to navigate a complex business environment characterized by stable inflation and raw material costs, but facing ongoing geopolitical and trade volatility that is driving regionalization. Markets are increasingly focused on energy security and affordability, with grid investment being prioritized in key regions.

As shown in the following illustration of the current business environment:

Quarterly Performance Highlights

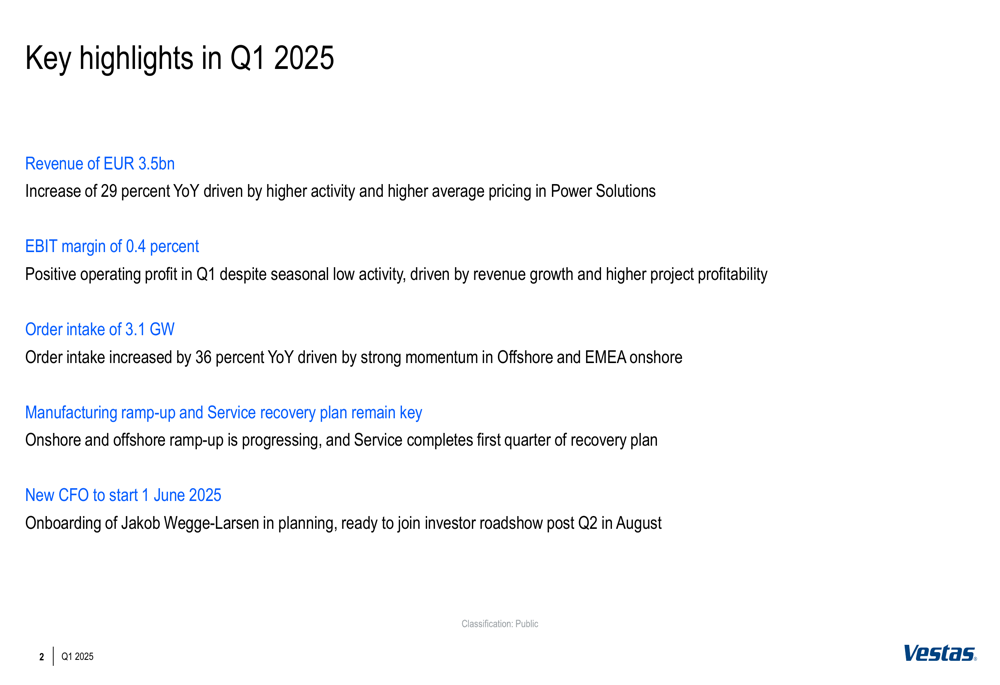

Vestas reported revenue of EUR 3.5 billion in Q1 2025, representing a substantial 29% increase year-over-year. This growth was primarily driven by higher activity and improved average pricing in the Power Solutions segment. The company achieved a positive EBIT margin of 0.4% despite the traditionally low seasonal activity in the first quarter.

Order intake reached 3.1 GW, increasing 36% compared to the same period last year, with strong momentum in Offshore and EMEA onshore markets. The company noted that the US market is awaiting policy clarity, which affected orders in that region.

The following slide summarizes the key quarterly highlights:

Detailed Financial Analysis

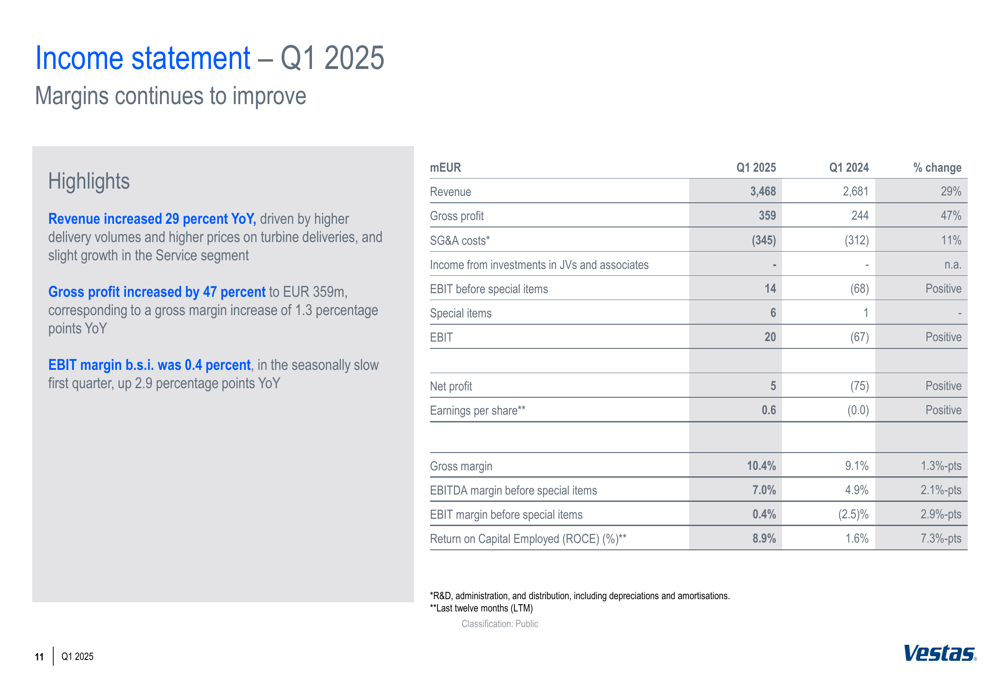

Vestas’ gross profit increased by 47% to EUR 359 million, corresponding to a gross margin improvement of 1.3 percentage points year-over-year to 10.4%. The company reported positive net profit of EUR 5 million, a significant improvement from the EUR 75 million loss in Q1 2024.

The Power Solutions segment saw revenue increase by 43% year-over-year, primarily driven by higher delivery volumes in Americas and APAC, along with higher average pricing. The segment’s EBIT margin before special items improved to negative 2.4%, up 7.1 percentage points year-over-year, despite ongoing costs related to manufacturing ramp-up in both Offshore and onshore operations in the USA.

The Service segment generated EBIT of EUR 166 million, corresponding to an EBIT margin of 18.0% on 2% higher revenue year-over-year. Vestas continues to execute on its Service recovery plan announced with its FY 2024 results.

The comprehensive income statement shows the company’s financial performance:

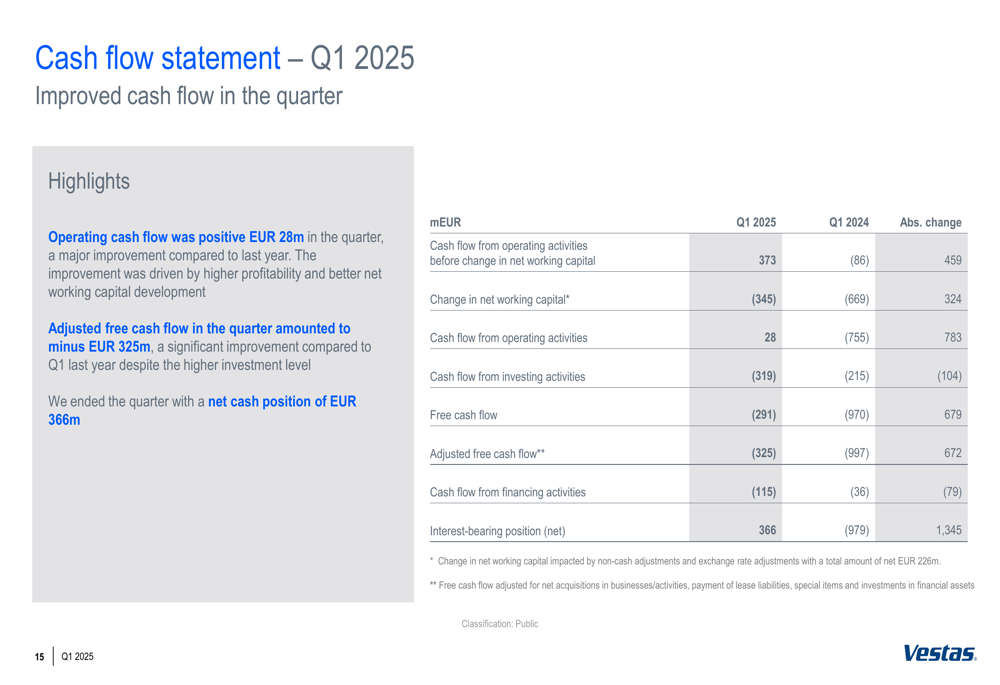

Operating cash flow was positive at EUR 28 million in the quarter, a major improvement compared to the previous year. The company ended Q1 with a net cash position of EUR 366 million. Total (EPA:TTEF) investments amounted to EUR 307 million, with continued investment in the V236 offshore manufacturing footprint.

The cash flow statement demonstrates this financial improvement:

Competitive Industry Position

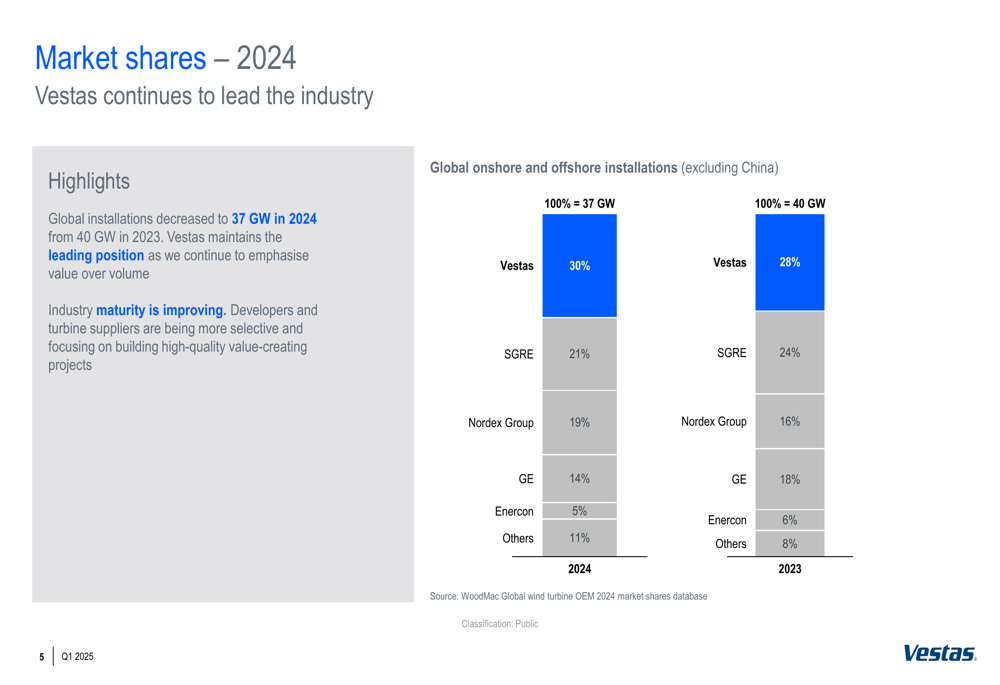

Vestas maintained its industry leadership with a 30% market share in 2024, up from 28% in 2023, despite global installations (excluding China) decreasing to 37 GW from 40 GW. The company emphasized its strategy of prioritizing value over volume in a maturing industry where developers and turbine suppliers are becoming more selective and focusing on high-quality, value-creating projects.

The market share data illustrates Vestas’ dominant position:

The company’s Service business continues to grow, with the order backlog increasing to almost EUR 37 billion from EUR 34 billion a year ago. Vestas now has 157 GW under service compared to 149 GW a year ago, solidifying its position as the largest Service business in the industry. The average contract duration stands at 11 years, providing long-term revenue visibility.

Forward-Looking Statements

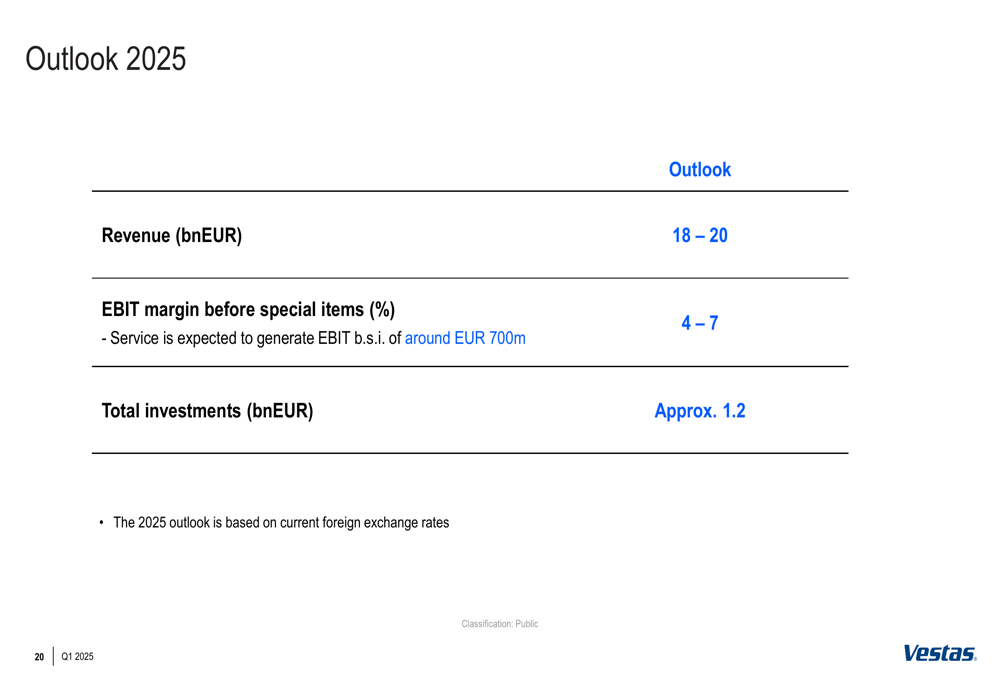

Vestas maintained its full-year 2025 guidance, projecting revenue between EUR 18-20 billion and an EBIT margin before special items of 4-7%. The Service segment is expected to generate EBIT before special items of around EUR 700 million. Total investments for the year are projected at approximately EUR 1.2 billion.

The company announced that new CFO Jakob Wegge-Larsen will start on June 1, 2025, and will join the investor roadshow following the Q2 results in August.

Vestas’ outlook for 2025 is summarized in the following slide:

On the sustainability front, turbines produced and shipped in the last twelve months are expected to avoid 490 million tonnes of greenhouse gas emissions over their lifetime, an increase of 97 million tonnes. Carbon emissions from Vestas’ own operations decreased by 1% compared to last year, though the company noted that its safety metric (TRIR) increased from 2.9 to 3.2 year-over-year.

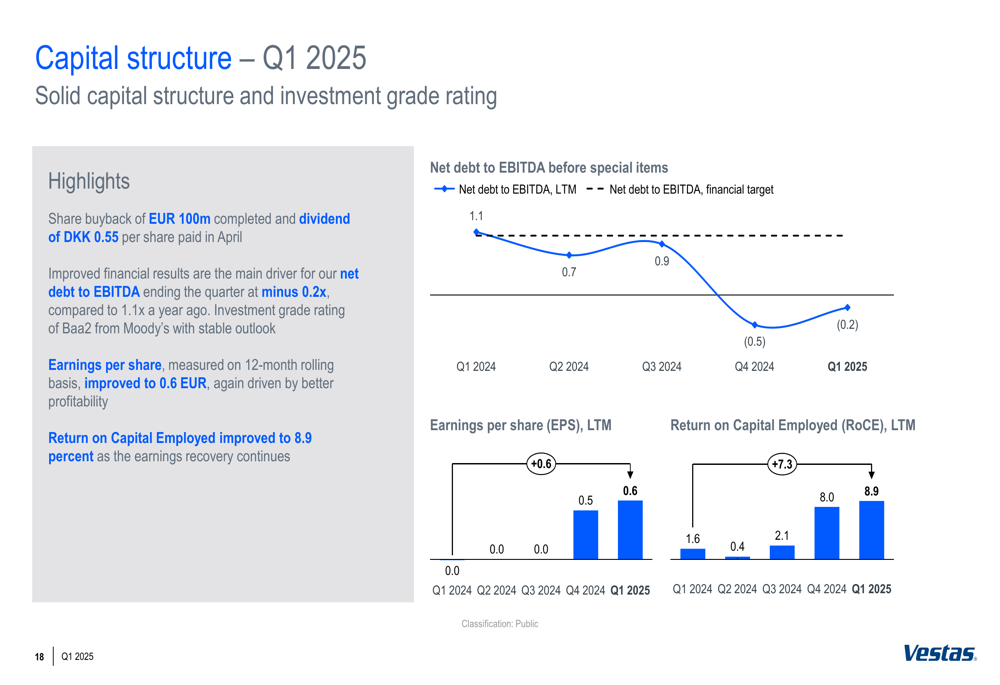

The company’s capital structure remains strong, with the completion of a EUR 100 million share buyback and payment of a dividend of DKK 0.55 per share in April. Improved financial results have driven the net debt to EBITDA ratio to negative 0.2x, and Vestas maintains an investment grade rating of Baa2 from Moody’s with a stable outlook.

As Vestas continues its manufacturing ramp-up and Service recovery plan, the company appears well-positioned to capitalize on the growing focus on renewable energy, despite ongoing challenges in permitting, auctions, and market design in various regions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.