Five things to watch in markets in the week ahead

Vestis Corp (NYSE:VSTS) released its third quarter 2025 results on August 6, 2025, showing continued revenue challenges but some sequential improvement from the previous quarter. The uniforms and workplace supplies provider reported revenue of $674 million, down 3.5% year-over-year, as the company continues to grapple with customer losses and margin pressure.

Introduction & Market Context

Vestis shares have struggled in recent months, trading near the 52-week low of $5.20. Following disappointing Q2 results that saw the stock tumble over 36%, investors were closely watching this quarter for signs of stabilization. The Q3 presentation revealed ongoing challenges but also highlighted sequential improvements and operational initiatives aimed at turning performance around.

The company’s Q3 revenue of $674 million came in at the low end of its previously provided guidance range of $674-682 million, continuing a trend of underperformance that has weighed on investor sentiment.

Quarterly Performance Highlights

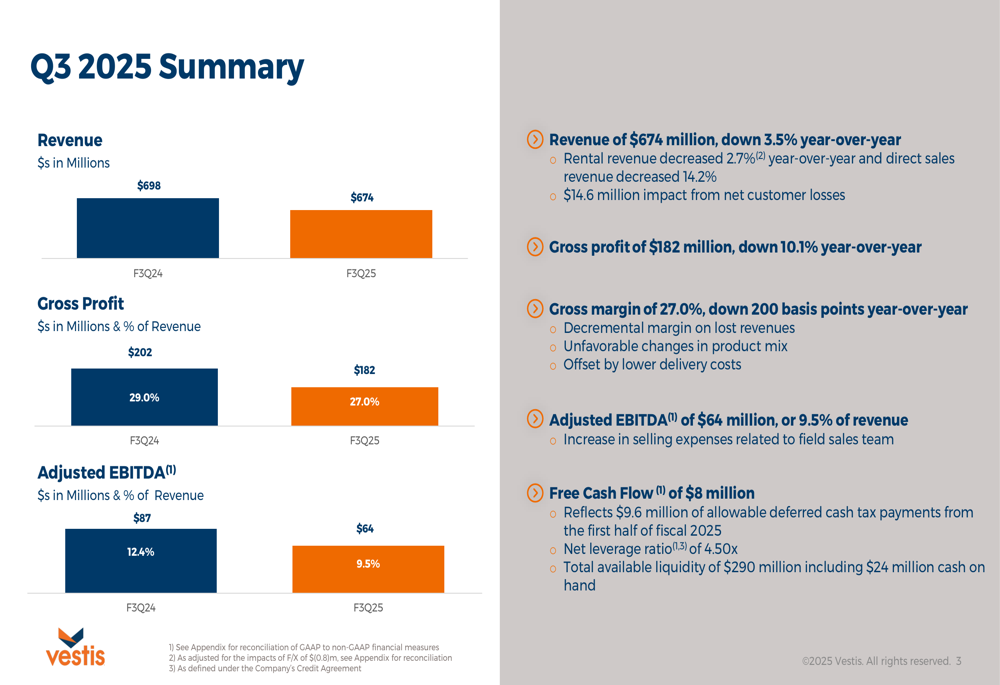

Vestis reported Q3 2025 revenue of $674 million, representing a 3.5% decrease from the $698 million reported in the same period last year. The decline was primarily driven by a 2.7% decrease in rental revenue and a steeper 14.2% drop in direct sales revenue. The company specifically noted a $14.6 million impact from net customer losses during the quarter.

As shown in the following summary of key Q3 metrics, both revenue and profitability measures declined year-over-year:

Gross profit fell 10.1% year-over-year to $182 million, with gross margin contracting 200 basis points to 27.0%. Management attributed this decline to decremental margin on lost revenues and unfavorable changes in product mix, partially offset by lower delivery costs.

Adjusted EBITDA came in at $64 million or 9.5% of revenue, down from 12.4% in the prior year period. However, this represented a 34.4% sequential improvement from Q2 2025, suggesting some operational stabilization.

Detailed Financial Analysis

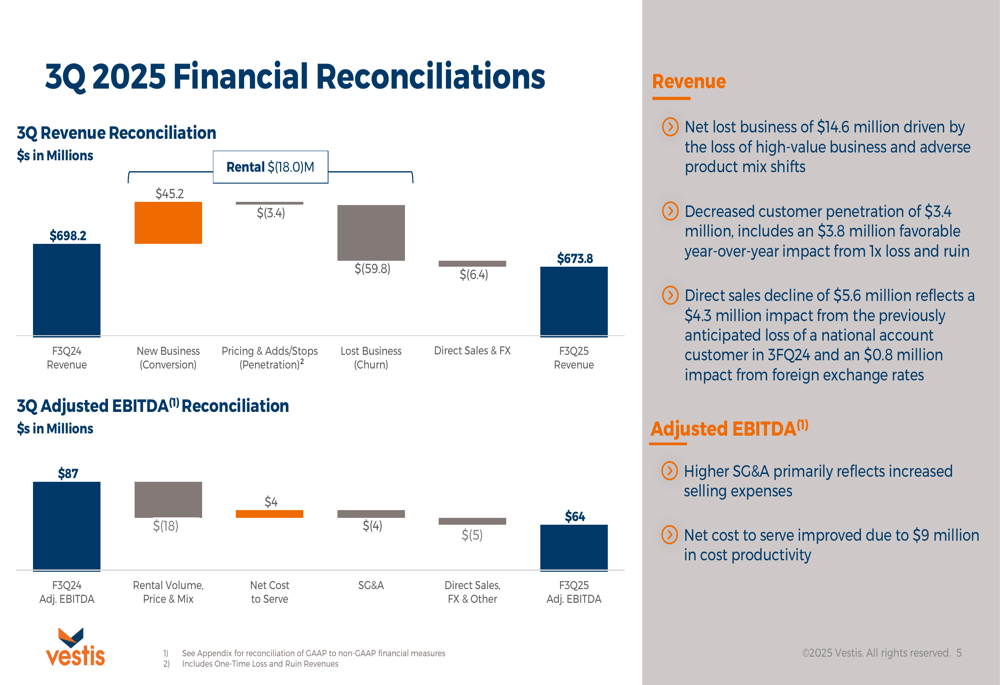

A deeper look at Vestis’ financial reconciliations reveals the specific factors driving the revenue and profitability declines. The following waterfall chart breaks down the components of the company’s revenue performance:

While Vestis gained $45.2 million from new business conversions, this was more than offset by $59.8 million in lost business (churn) and $3.4 million in reduced pricing and penetration. The net impact on rental revenue was negative $18.0 million, with direct sales and foreign exchange effects contributing an additional $6.4 million decline.

Similarly, Adjusted EBITDA fell from $87 million in Q3 2024 to $64 million in Q3 2025, primarily due to $18 million in negative impacts from rental volume, price, and mix changes, along with $4 million in increased SG&A expenses and $5 million from direct sales, FX, and other factors. These were partially offset by $4 million in net cost-to-serve improvements.

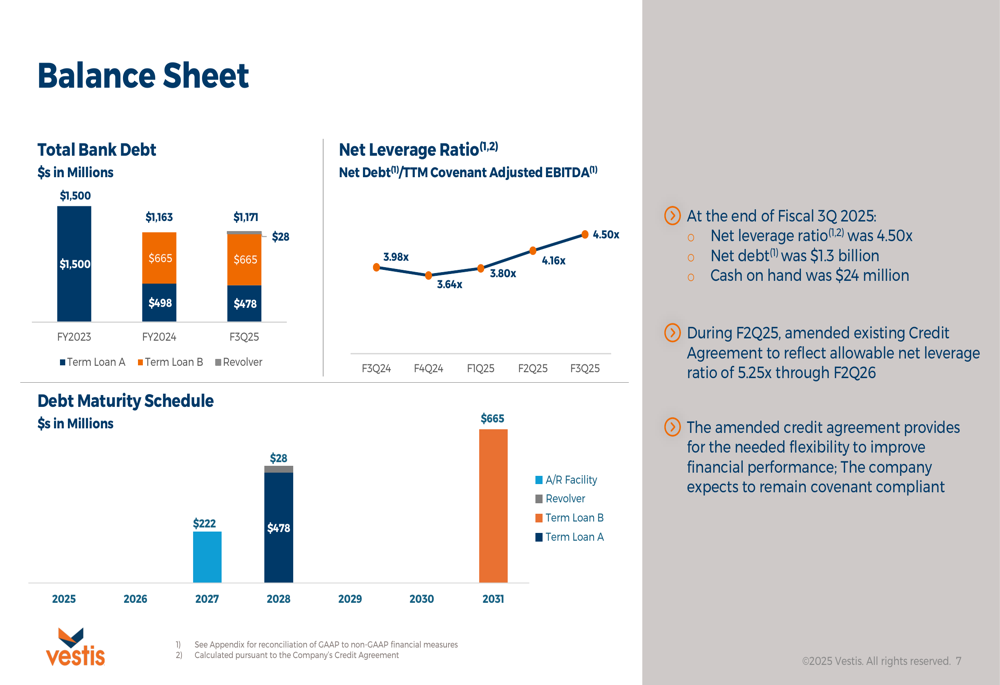

The company’s balance sheet continues to show increasing leverage, with the net leverage ratio rising to 4.50x in Q3 2025 from 3.64x in FY2024:

During the second quarter, Vestis amended its credit agreement to allow for a higher net leverage ratio of 5.25x through Q2 2026, providing financial flexibility as the company works to improve performance. Total (EPA:TTEF) bank debt stood at $1,171 million at the end of Q3, with total available liquidity of $290 million including $24 million in cash on hand.

Free cash flow for the quarter was $8 million, a significant decline from $27.7 million in Q3 2024 but an improvement from the negative free cash flow reported in the first two quarters of fiscal 2025. The company noted that Q3 free cash flow reflected $9.6 million of allowable deferred cash tax payments from the first half of fiscal 2025.

Strategic Initiatives

Vestis outlined several key strategic initiatives aimed at addressing its operational challenges and improving financial performance:

Management is prioritizing improved operating leverage through value-based pricing, product mix optimization, and cost of service improvements. The company is also assessing various initiatives to enhance commercial and operational processes, with a focus on improved utilization, plant reliability, and customer service.

From a capital allocation perspective, Vestis is emphasizing cash flow generation, debt repayment, and return-based capital investment. These initiatives are intended to serve as the foundation for establishing a long-term value creation framework.

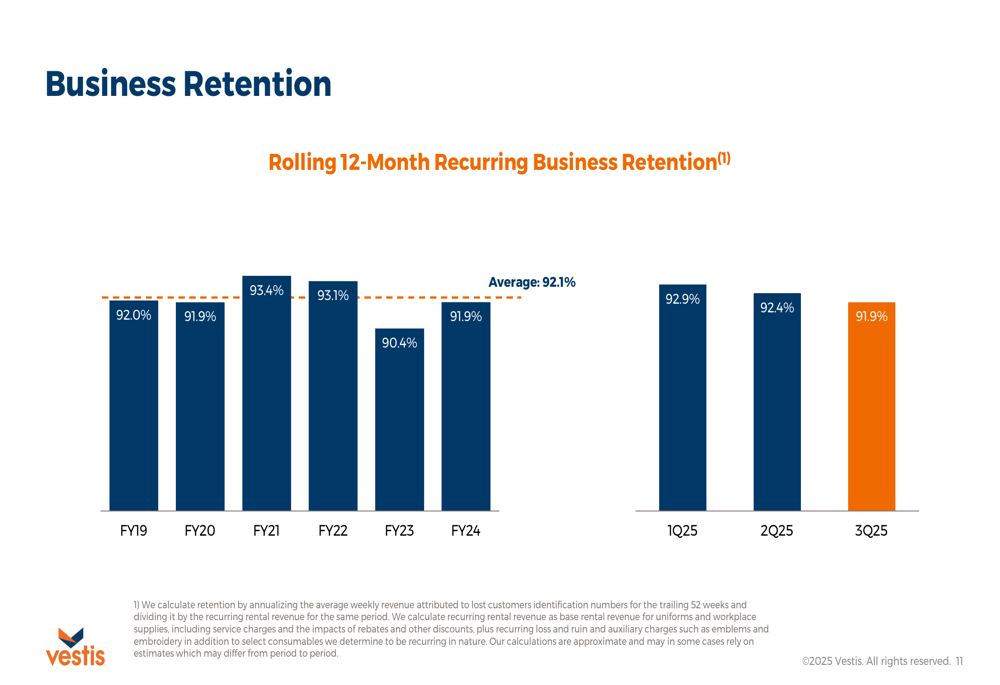

The company’s business retention rate, a critical metric for its rental-based business model, stood at 91.9% for Q3 2025, down slightly from 92.4% in Q2 2025 and below the company’s historical average of 92.1%:

Improving this retention rate will be crucial for Vestis to stabilize its revenue base and return to growth.

Forward-Looking Statements

Looking ahead, Vestis emphasized that its near-term initiatives will serve as the foundation for establishing a long-term value creation framework. The company expects to remain covenant compliant despite the increased leverage, thanks to the amended credit agreement that provides flexibility through Q2 2026.

Management is focused on operational improvements enabled by better utilization, plant reliability, and customer service. These efforts are aimed at unlocking value through improved operating leverage and utilization.

The Q3 results reflect the continued challenges Vestis faces following its disappointing Q2 performance, but the sequential improvement in several metrics suggests the company’s operational initiatives may be beginning to gain traction. Investors will be watching closely to see if these improvements can be sustained and accelerated in future quarters as the company works to stabilize its financial performance and reduce leverage.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.