Sprouts Farmers Market closes $600 million revolving credit facility

Introduction & Market Context

Viasat Inc. (NASDAQ:VSAT) presented its fourth quarter fiscal year 2025 earnings results on May 20, 2025, revealing a mixed financial performance with notable strength in its defense business offsetting challenges in other segments. The satellite communications provider, which operates 23 satellites and has 8 more under development, continues to expand its global footprint across 76 countries while navigating a competitive landscape in the satellite communications industry.

The company’s stock closed at $10.53 on the day of the presentation, down 1.59% from the previous close, and continued to decline by 1.71% in after-hours trading, reflecting investor concerns about the company’s revised outlook for fiscal year 2026.

Quarterly Performance Highlights

Viasat reported Q4 FY2025 revenue of $1.147 billion, representing a marginal decrease of $3 million compared to $1.150 billion in Q4 FY2024. Despite the flat revenue, the company achieved notable improvements in profitability and cash flow metrics.

Adjusted EBITDA increased by 5% year-over-year to $375 million, up from $358 million in the same quarter last year. Operating cash flow showed significant improvement, reaching $298 million compared to $232 million in the prior year period, representing a $66 million increase.

The company also substantially reduced its capital expenditures to $248 million, down 34% from $378 million in Q4 FY2024, reflecting the completion of certain satellite development programs.

As shown in the following financial summary:

New contract awards increased by 5% to $1.170 billion, though backlog decreased by 4% to $3.553 billion compared to the prior year. This mixed performance reflects varying dynamics across Viasat’s business segments.

Segment Performance Analysis

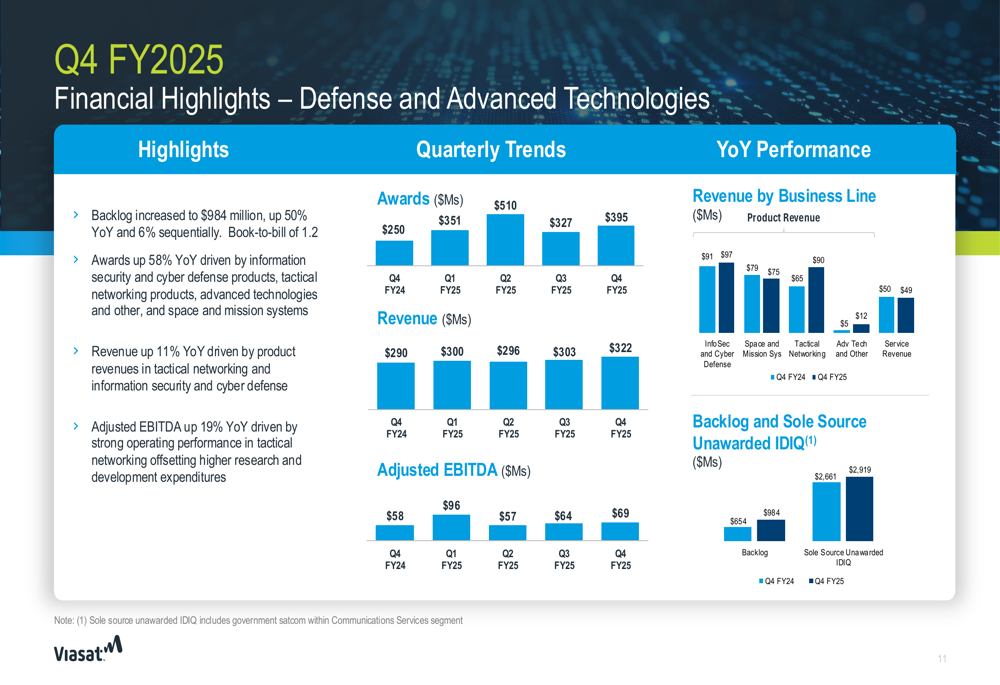

The Defense and Advanced Technologies (DAT) segment emerged as the standout performer in Q4 FY2025, with revenue increasing 11% year-over-year and adjusted EBITDA growing by an impressive 19%. The segment’s backlog surged by 50% to $984 million, indicating strong future growth potential.

The following chart illustrates the DAT segment’s performance:

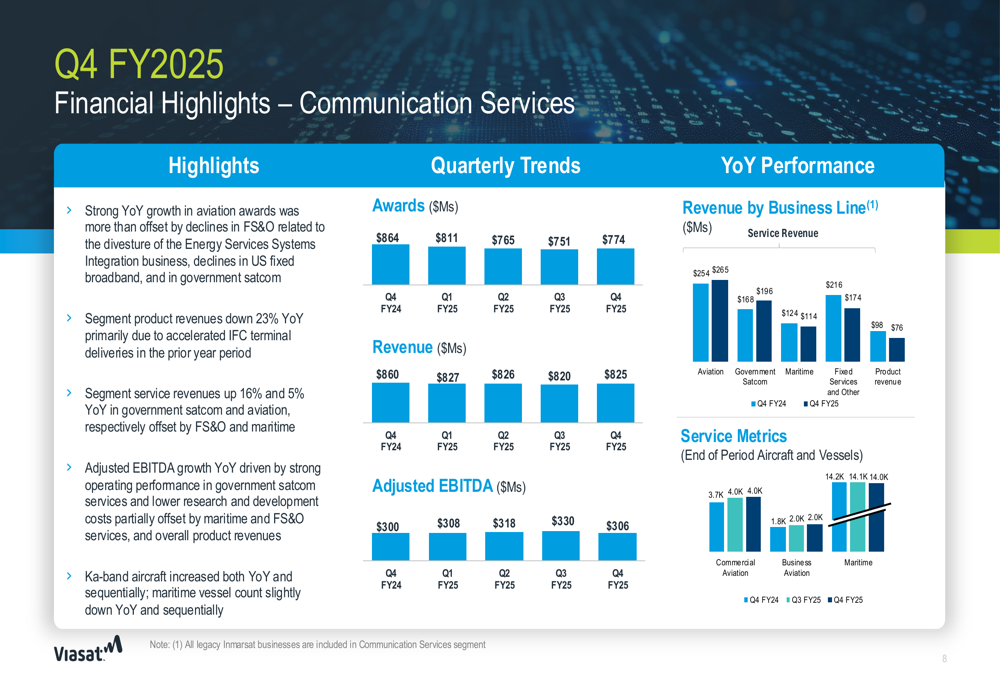

In the Communication Services segment, results were more mixed. Aviation service revenues increased by 5% year-over-year, and government satcom services grew by 16%. However, product revenue declined by 23% compared to the same period last year.

The segment’s performance is detailed in this breakdown:

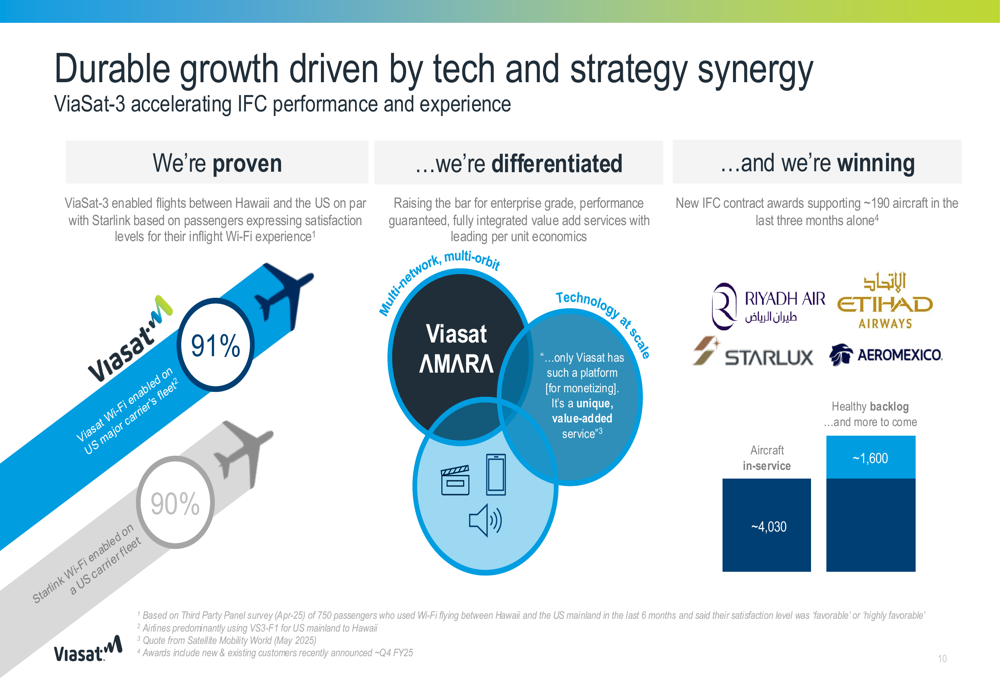

Viasat’s aviation connectivity business continues to show momentum, with the company highlighting its "Full, Fast, Free" Wi-Fi offering that has achieved 91% passenger satisfaction on enabled flights, slightly outperforming competitor Starlink’s reported 90% satisfaction rate. The company secured new in-flight connectivity contracts supporting approximately 190 additional aircraft in the last three months with airlines including Riyadh Air, Etihad Airways, Starlux, and Aeromexico.

The following slide illustrates Viasat’s competitive positioning in the aviation market:

Strategic Initiatives and Competitive Positioning

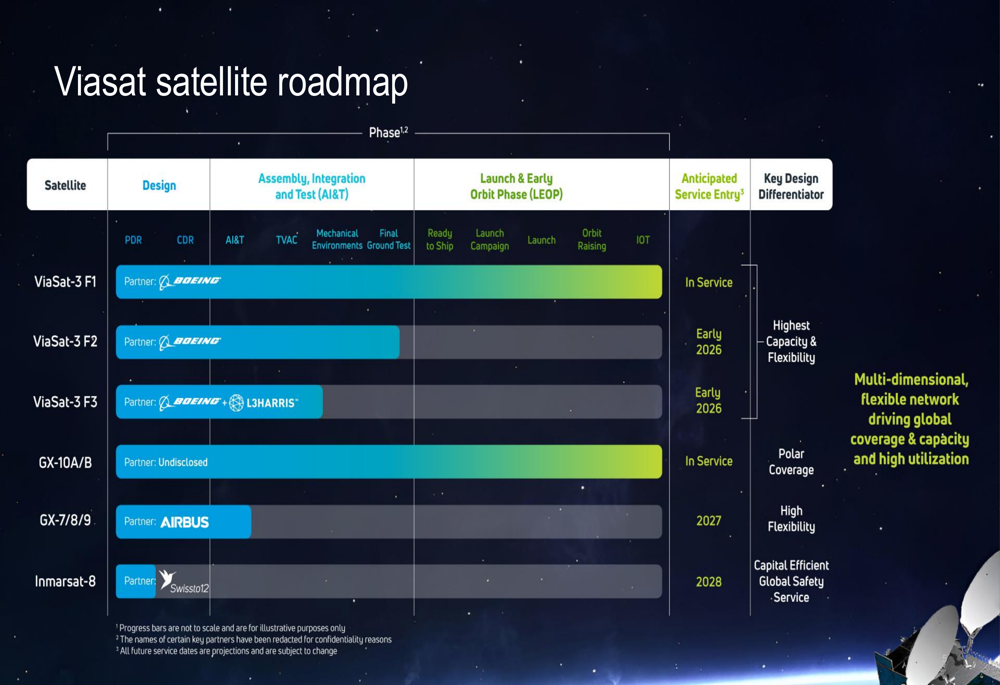

Viasat continues to invest in its satellite infrastructure, with a roadmap detailing the design, assembly, launch, and service entry for various satellites including ViaSat-3 F1, F2, and F3, as well as GX-7/8/9 and Inmarsat-8. The company emphasizes its differentiators in terms of capacity, flexibility, and polar coverage.

The satellite deployment timeline is illustrated in this roadmap:

The company’s scale and global reach are highlighted in its corporate overview:

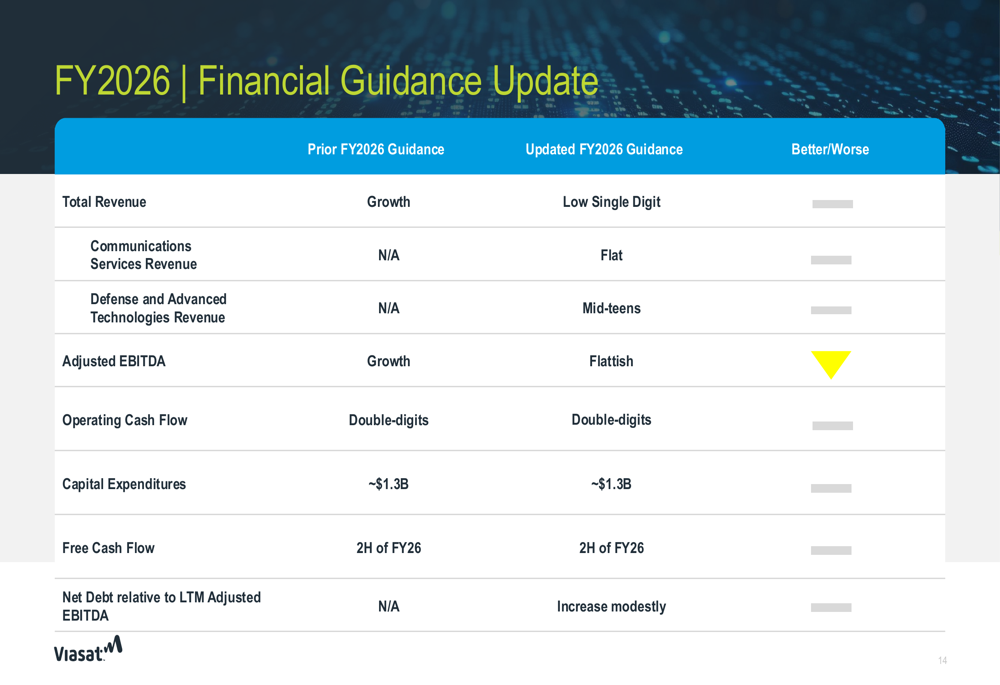

FY2026 Outlook and Guidance

In a concerning development for investors, Viasat downgraded several aspects of its FY2026 guidance. The company now expects only low single-digit total revenue growth, down from its previous more optimistic growth projection. The Communications Services revenue is expected to be flat, while the Defense and Advanced Technologies revenue is projected to grow at a mid-teens rate.

Adjusted EBITDA outlook was also downgraded from growth to "flattish," suggesting potential margin pressure. Capital expenditures are still expected to be approximately $1.3 billion, and the company anticipates positive free cash flow in the second half of FY2026.

The revised guidance is detailed in the following slide:

Financial Position and Debt Profile

Viasat’s balance sheet shows a total liquidity position of $2.313 billion as of Q4 FY2025, down from $3.042 billion in the prior year. Gross outstanding debt decreased to $6.762 billion from $7.476 billion, though net debt slightly increased to $5.592 billion from $5.575 billion.

The company’s debt maturity profile indicates that 83% of its debt is secured and 55% is at fixed rates, providing some stability in the current interest rate environment. Viasat has managed its near-term maturities, including the retirement of its 2025 unsecured notes.

Overall, Viasat’s Q4 FY2025 results reflect a company in transition, with strong performance in its defense business offset by challenges in other segments. The downward revision of FY2026 guidance suggests continued headwinds, though the company’s strategic positioning in defense and aviation markets, along with its satellite deployment roadmap, provide potential growth avenues for the future.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.