Gold prices jump to near 3-week high amid US shutdown progress

Introduction & Market Context

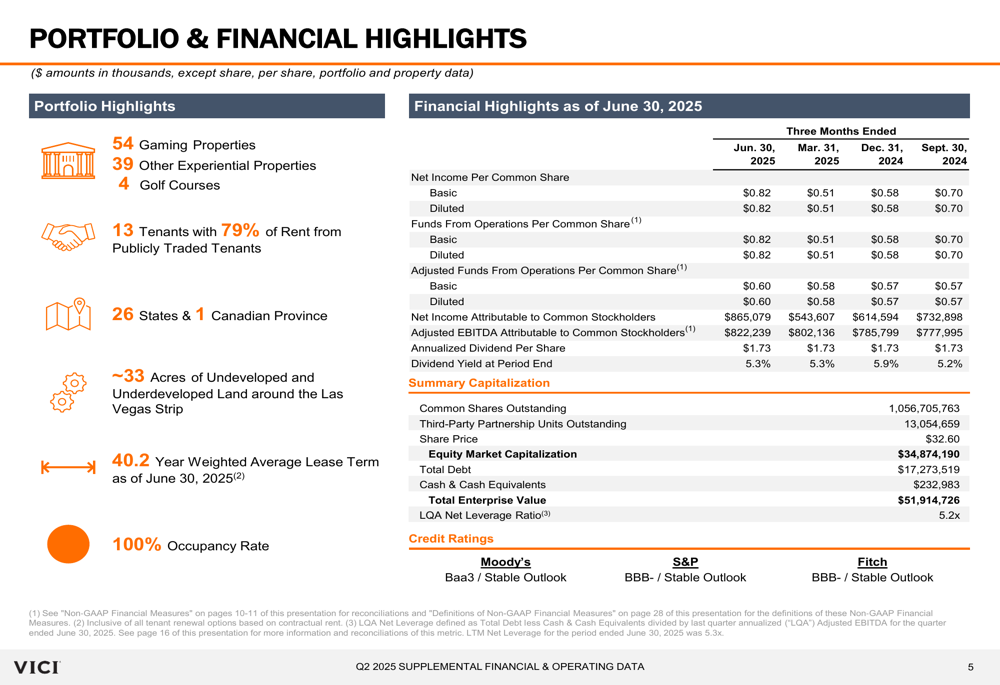

VICI Properties Inc. (NYSE:VICI), an S&P 500 experiential real estate investment trust, released its Q2 2025 financial results on July 31, 2025, showcasing solid performance across its portfolio of gaming and experiential properties. The company’s extensive portfolio spans 93 assets across 26 states and one Canadian province, positioning it as a leader in the experiential real estate sector.

Despite reporting strong fundamentals, VICI’s stock has faced pressure in recent months, trading at $29.52 as of October 31, 2025, significantly below the $32.60 share price reported in the Q2 presentation. This disconnect between operational performance and stock valuation presents an interesting dynamic for investors to consider.

Q2 2025 Financial Performance

VICI Properties reported impressive financial results for the second quarter of 2025, with total revenue reaching $1.001 billion, a 4.6% increase from $957.0 million in the same period last year. Net income attributable to common stockholders rose significantly to $865.1 million, representing a 16.7% jump from Q2 2024.

As shown in the following comprehensive overview of the company’s financial highlights, VICI maintained strong operational metrics, including a 100% occupancy rate across its portfolio and a 40.2-year weighted average lease term, providing exceptional visibility into future cash flows:

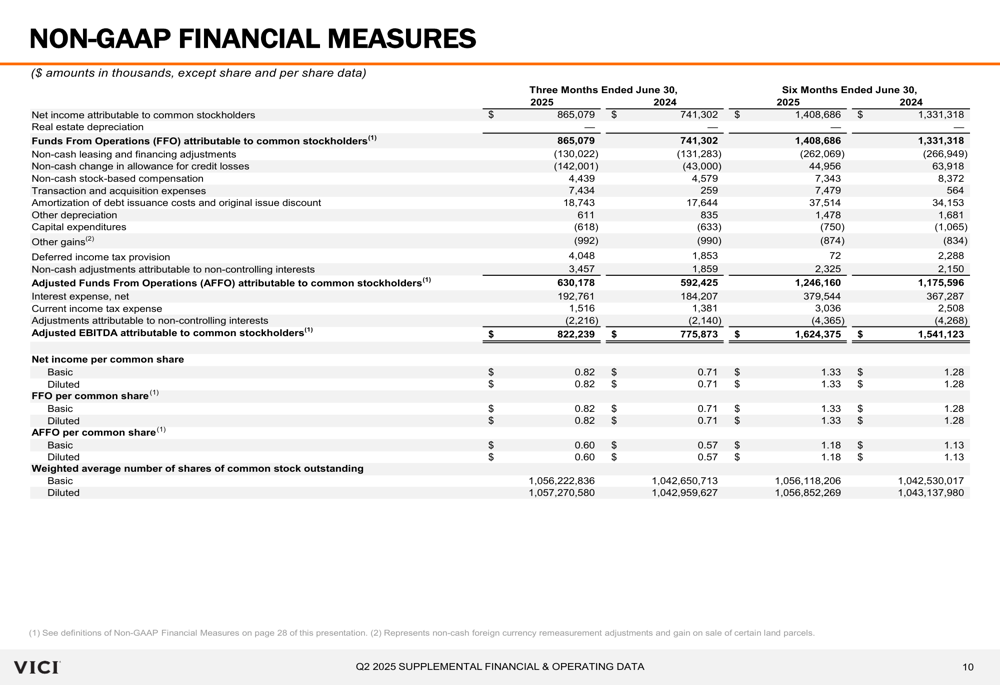

The company’s adjusted funds from operations (AFFO), a key metric for REITs, reached $630.2 million ($0.60 per share) in Q2 2025, up 6.4% from $592.4 million ($0.57 per share) in Q2 2024. This growth demonstrates VICI’s ability to generate increasing cash flow from its portfolio.

A detailed breakdown of the company’s non-GAAP financial measures shows consistent improvement across key metrics:

Portfolio Composition and Tenant Diversification

VICI’s portfolio consists of 54 gaming properties and 39 other experiential properties, providing diversification across property types and geographies. The company’s tenant base includes 13 operators, with 79% of rent coming from publicly traded tenants, enhancing the stability and predictability of rental income.

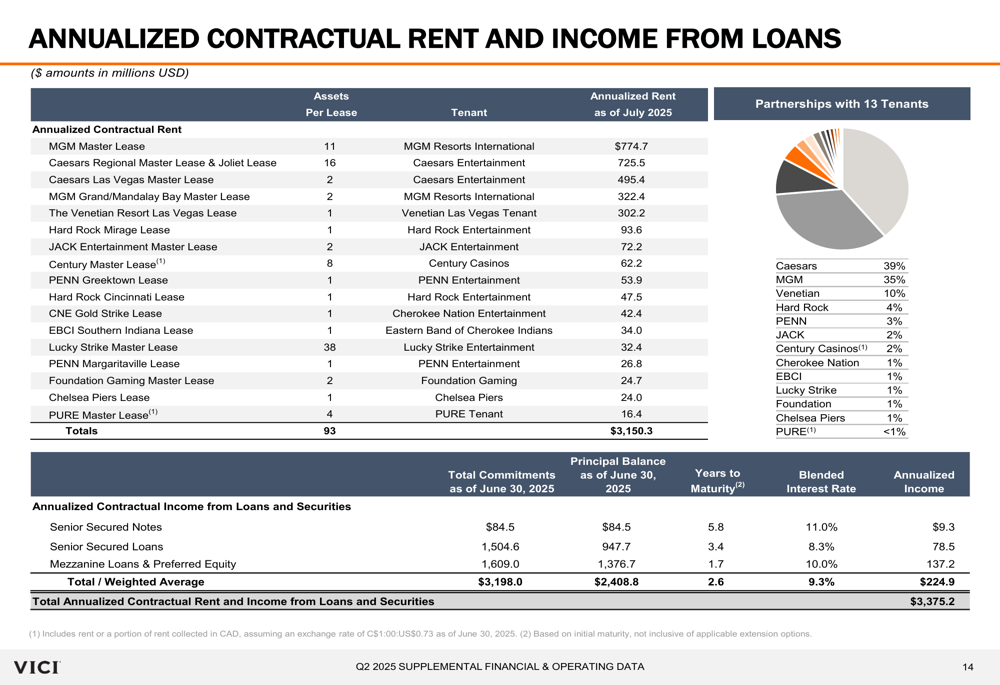

The following chart illustrates VICI’s tenant diversification, with Caesars (39%) and MGM (35%) representing the largest contributors to the company’s $3.15 billion in annualized contractual rent:

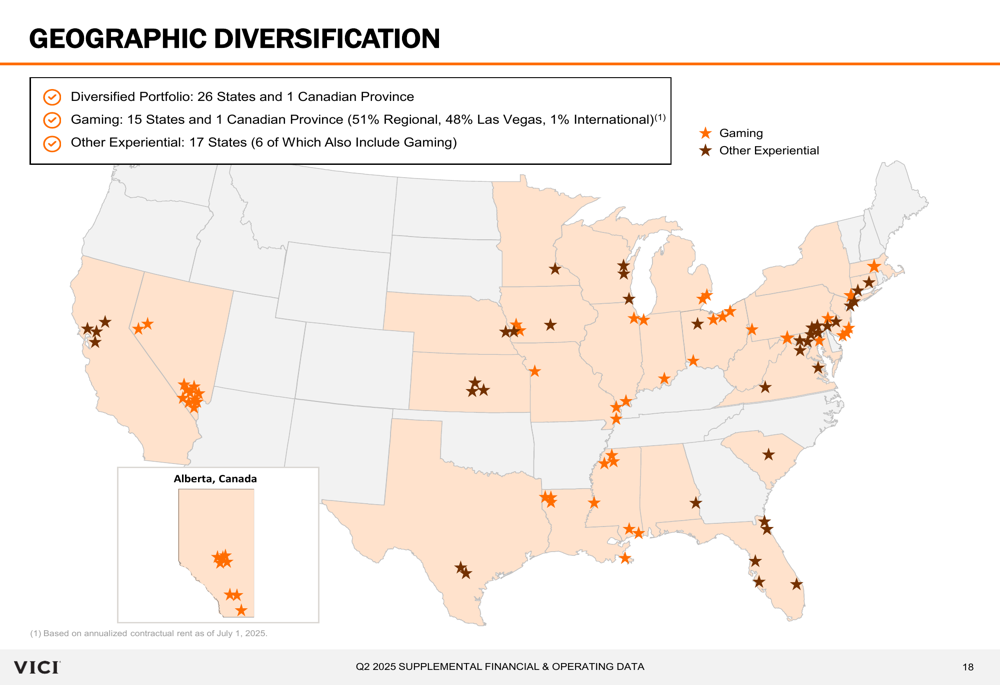

Geographic diversification is another key strength of VICI’s portfolio, with properties spread across 26 states and one Canadian province. This widespread presence helps mitigate regional economic risks and provides exposure to various markets:

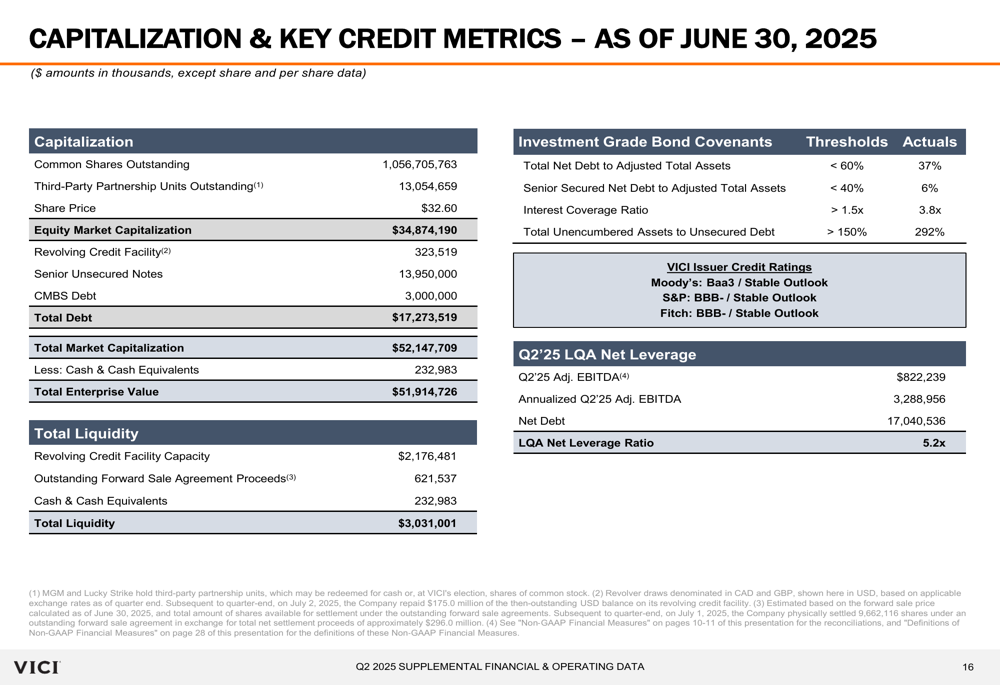

Balance Sheet and Credit Metrics

VICI maintains a solid financial position with investment grade credit ratings from all three major rating agencies (Moody’s, S&P, and Fitch). As of June 30, 2025, the company reported total debt of $17.3 billion and a total enterprise value of $51.9 billion.

The following breakdown of VICI’s capitalization and key credit metrics demonstrates the company’s financial strength and adherence to investment grade bond covenants:

The company’s debt profile is well-structured with a weighted average maturity of 6.5 years and 98.1% fixed-rate debt, providing stability in the current interest rate environment. VICI maintains strong liquidity with $3.03 billion available, including $2.18 billion in revolving credit facility capacity and $233 million in cash and cash equivalents.

Updated 2025 Guidance

Based on strong first-half performance, VICI raised its full-year 2025 AFFO guidance. The company now expects AFFO to be between $2,500 million and $2,520 million, or between $2.35 and $2.37 per diluted common share, up from the previous guidance of $2,470-$2,500 million ($2.33-$2.36 per share).

The following table details the updated guidance compared to prior projections:

This guidance upgrade reflects management’s confidence in the company’s ability to execute its strategy and continue generating strong results. However, it’s worth noting that the guidance does not include the impact of any pending or possible future acquisitions or dispositions, capital markets activity, or other non-recurring transactions.

Recent Stock Performance and Outlook

Despite VICI’s strong operational performance and raised guidance, the company’s stock has faced pressure in recent months. According to the most recent data, VICI shares traded at $29.52 on October 31, 2025, well below the $32.60 share price reported in the Q2 presentation, representing a decline of approximately 9.4%.

This disconnect between fundamental performance and stock valuation may present an opportunity for investors, particularly considering the company’s 5.3% dividend yield at the end of Q2 2025. The stock remains within its 52-week range of $27.98 to $34.03.

Looking ahead, VICI’s subsequent Q3 2025 results (reported after this presentation) showed continued solid performance with EPS of $0.71 and revenue of approximately $1 billion, slightly above analyst expectations. However, the stock experienced a minor decline of 0.95% in premarket trading following the Q3 earnings announcement, suggesting ongoing market skepticism despite consistent operational execution.

VICI’s CEO Ed Pitoniak expressed optimism about the company’s prospects in the Q3 earnings call, stating, "Welcome back to a total return world," while highlighting the unique value proposition of VICI’s real estate category. With its diversified portfolio, long-term leases, and solid financial position, VICI appears well-positioned to navigate market challenges while continuing to deliver value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.