Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Viscofan (BME:VIS) shares rose 2.21% to €58.90 following the release of its second quarter and first half 2025 results on July 31, 2025. The Spanish casings manufacturer reported accelerating operational growth in the second quarter, though foreign exchange headwinds partially offset these gains. The company’s stock remains near its 52-week low of €58.60, despite the positive market reaction to the latest results.

Quarterly Performance Highlights

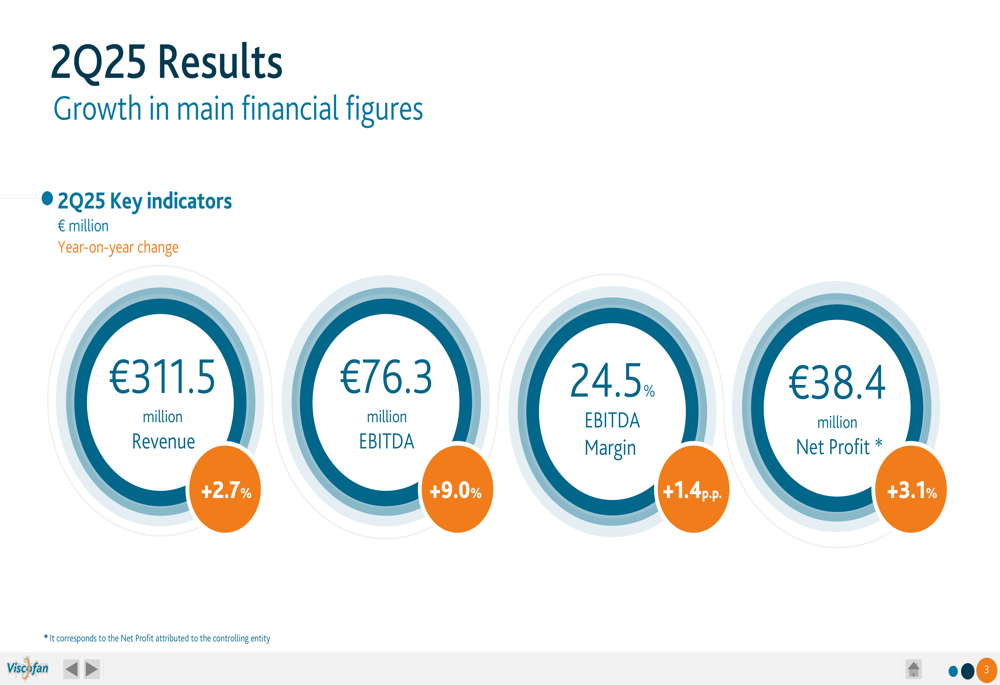

Viscofan delivered solid second-quarter results with revenue reaching €311.5 million, a 2.7% increase year-over-year. More notably, the company achieved a 9.0% growth in EBITDA to €76.3 million, representing an all-time high for a second quarter. The EBITDA margin expanded by 1.4 percentage points to 24.5%, reflecting improved operational efficiency and cost control measures.

As shown in the following chart of key financial indicators for Q2 2025:

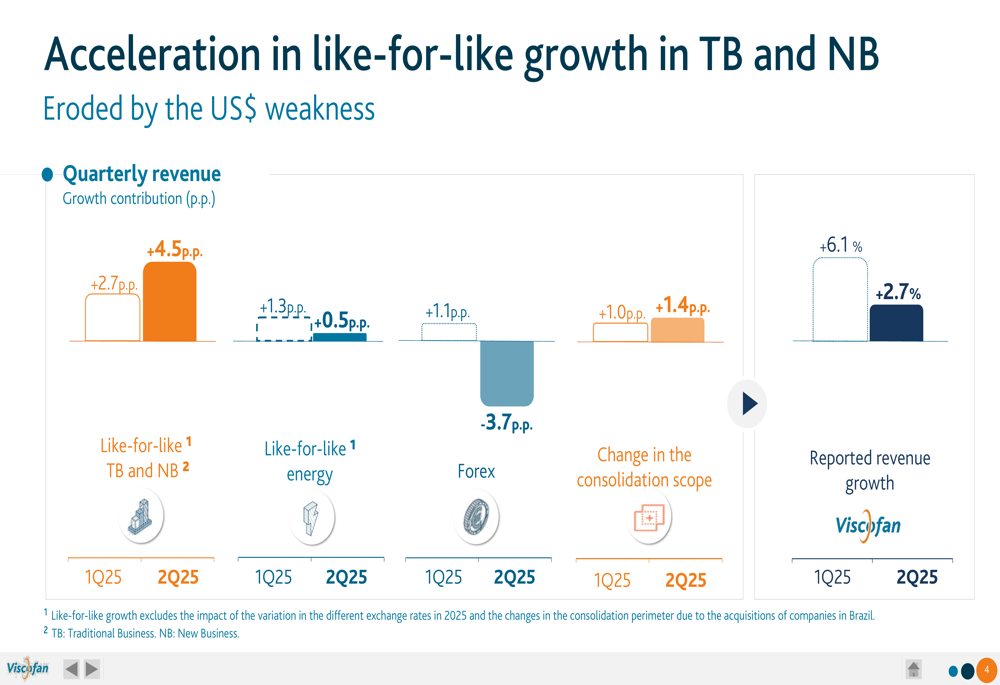

The company’s like-for-like growth in its Traditional Business (TB) and New Business (NB) segments accelerated from 2.7 percentage points in Q1 to 4.5 percentage points in Q2. However, this operational improvement was partially offset by a negative 3.7 percentage point impact from foreign exchange, primarily due to a weaker US dollar. This contrasts with the positive 1.1 percentage point forex contribution in Q1.

The quarterly revenue growth breakdown illustrates this acceleration in core business growth despite currency headwinds:

Detailed Financial Analysis

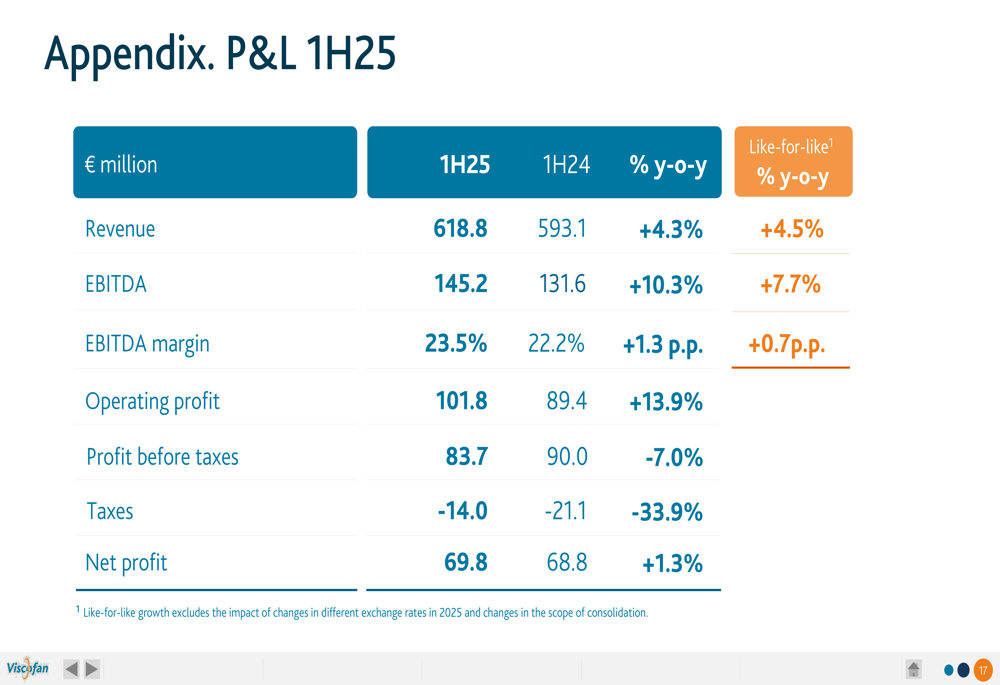

For the first half of 2025, Viscofan reported total revenue of €618.8 million, representing a 4.3% increase compared to the same period in 2024. The company’s EBITDA grew by 10.3% to €145.2 million, with the EBITDA margin expanding by 1.3 percentage points to 23.5%.

The company’s P&L statement for the first half of 2025 shows double-digit growth in key operational metrics:

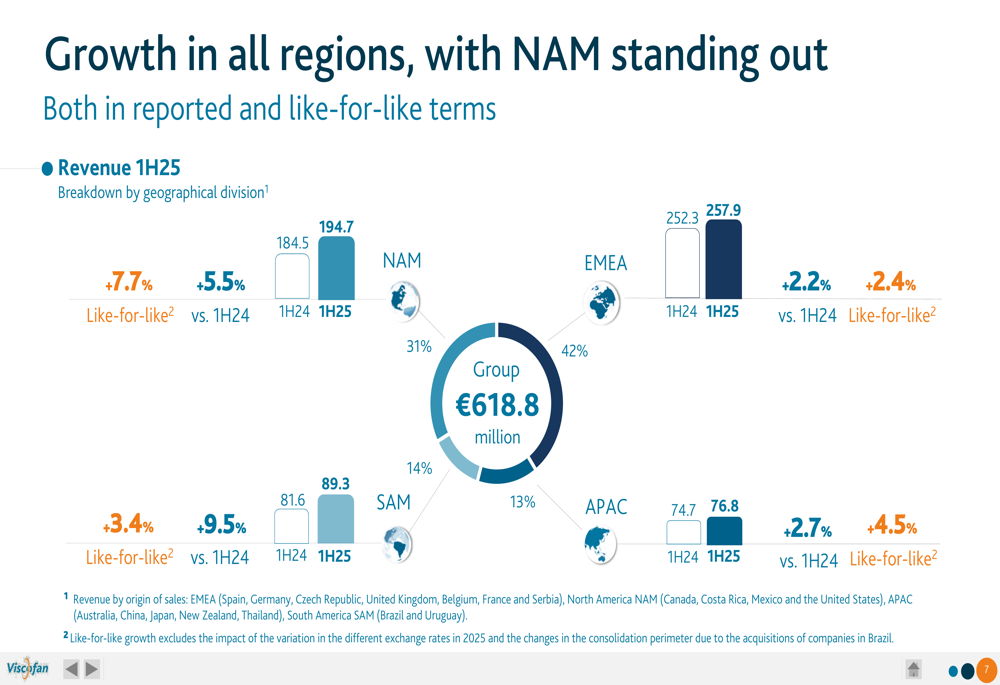

All geographical regions contributed to growth, with South America (SAM) leading at 9.5% year-over-year, followed by North America (NAM) at 5.5%, Asia-Pacific (APAC) at 2.7%, and Europe, Middle East and Africa (EMEA) at 2.2%. EMEA remains the largest contributor to revenue at 42%, followed by NAM at 31%.

The geographical revenue breakdown provides insight into the company’s global performance:

By business division, Viscofan’s Traditional Business, which accounts for 82% of total revenue, grew by 2.2% year-over-year to €506.6 million. The New Business segment, representing 13% of revenue, showed impressive growth of 14.0% to reach €81.4 million. The Energy division, though only 5% of total revenue, posted the strongest growth at 18.6%.

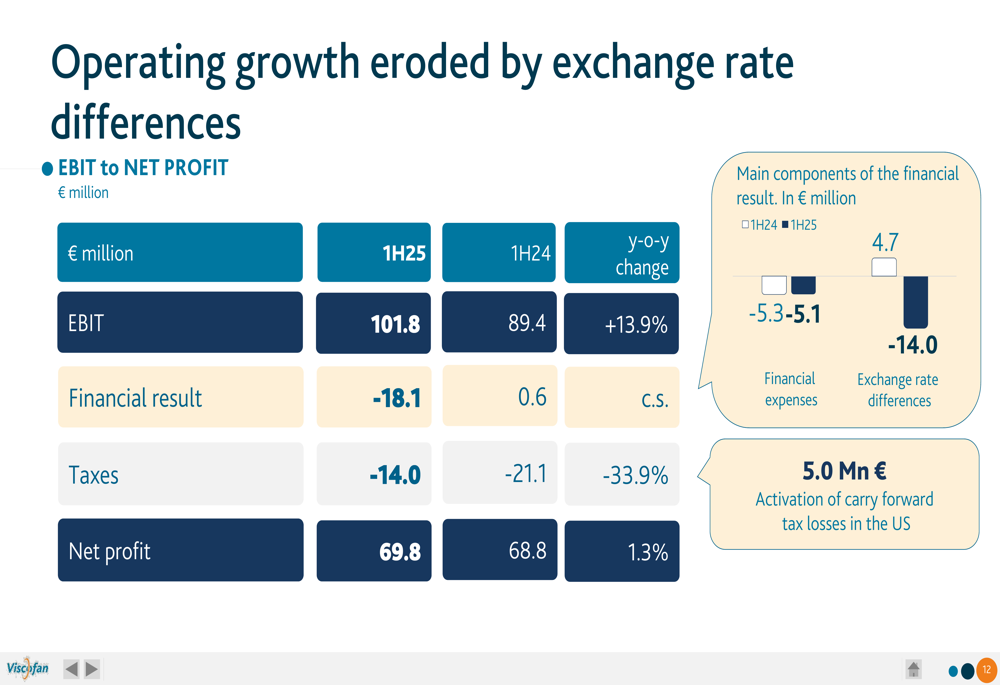

Despite strong operational performance, Viscofan’s net profit growth was limited to 1.3% year-over-year, reaching €69.8 million for the first half. This modest bottom-line growth was primarily due to negative exchange rate differences of €14.0 million, compared to a positive €4.7 million in the same period last year.

The following chart illustrates how operating growth was eroded by exchange rate differences:

Strategic Initiatives

Viscofan has significantly increased its capital expenditure, which rose 68.8% year-over-year to €40.5 million in the first half of 2025. The company expects total capex for 2025 to reach €75.0 million, a 5.6% increase from 2024.

Key investment projects include collagen casings capacity expansion, a new bag production facility in Mexico, environmental equipment, and continuous process improvements. These investments align with the company’s strategy to enhance production capacity while improving environmental sustainability.

The company’s net bank debt increased to €228.7 million as of June 2025, up from €146.9 million in December 2024. This increase was primarily driven by working capital changes (+€73.9 million), capital expenditures (+€40.5 million), and shareholder remuneration (+€77.9 million), partially offset by strong EBITDA generation (-€145.2 million).

Forward-Looking Statements

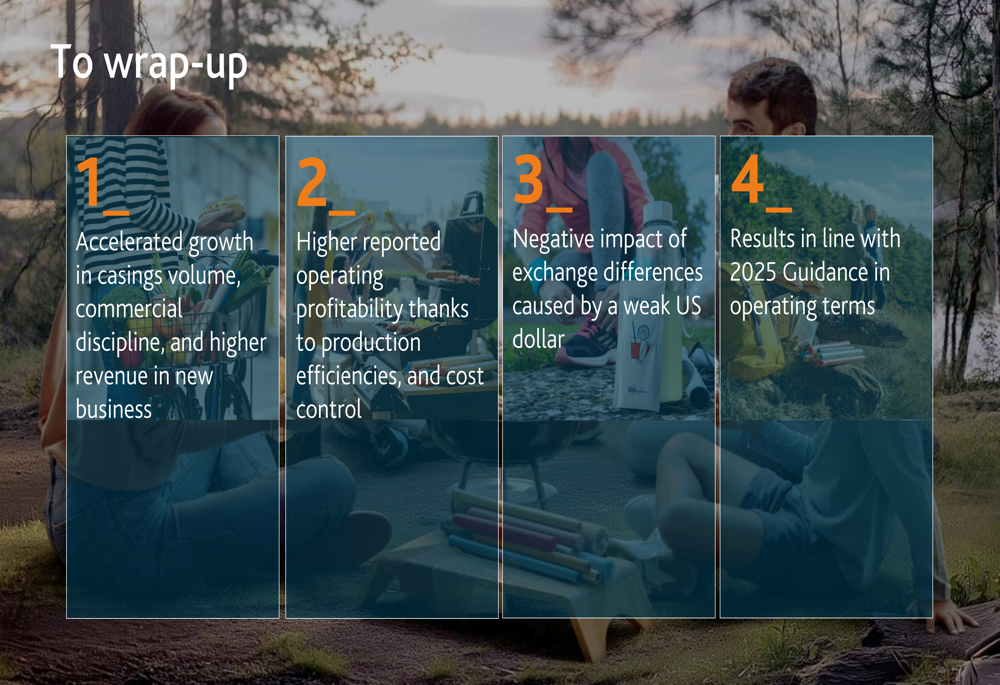

Viscofan management indicated that the first-half results are in line with the company’s 2025 guidance in operational terms. The company highlighted the acceleration in casings volume growth, maintained commercial discipline, and higher revenue in new business segments as key positive factors.

Looking ahead, Viscofan emphasized its focus on production efficiencies and cost control to maintain margin improvement. However, the company acknowledged the ongoing challenge of exchange rate volatility, particularly the weak US dollar, which continues to impact reported results.

The company summarized its first-half performance with these key takeaways:

With continued investments in capacity expansion and efficiency improvements, Viscofan appears well-positioned to maintain its operational momentum through the second half of 2025, though currency fluctuations remain a significant external factor that could impact reported results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.