Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

Vistra Energy Corp (NYSE:VST) reported strong first-quarter 2025 results on May 7, delivering $1.24 billion in Adjusted EBITDA as the company continues to benefit from its integrated business model and growing power demand. The stock has shown positive momentum, with fundamentals indicating a 3.43% increase to $144.80 at the previous close, and premarket trading up an additional 1.31% to $146.70.

The energy provider has maintained its upward trajectory following a transformative 2024, when it achieved full-year adjusted EBITDA of $5.66 billion. Vistra’s Q1 2025 performance demonstrates continued momentum in both its generation and retail segments, supported by strong demand growth in its key markets.

Quarterly Performance Highlights

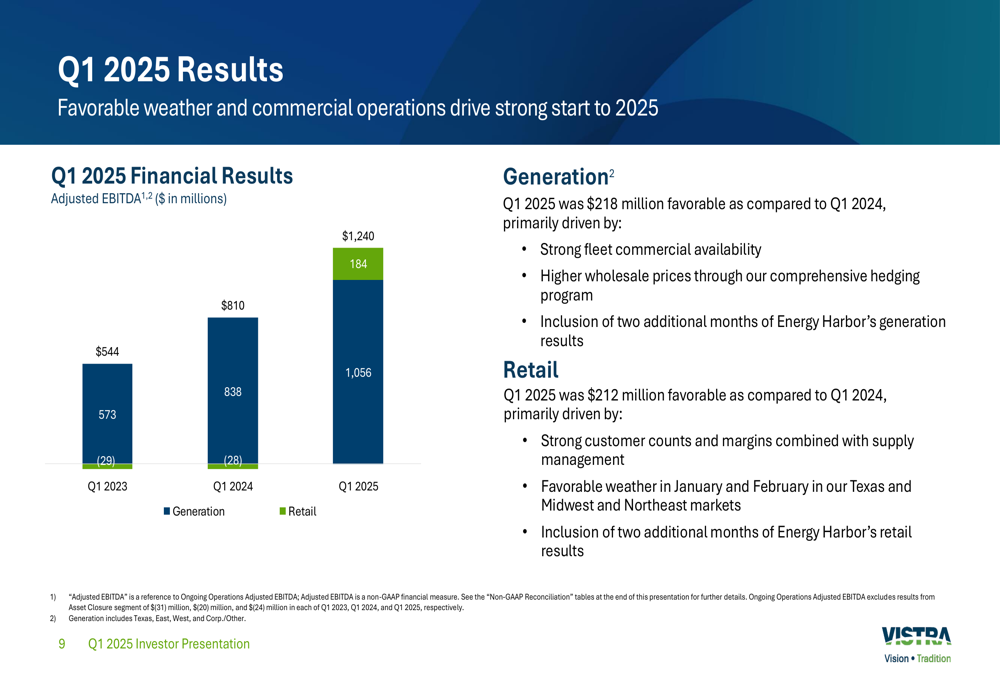

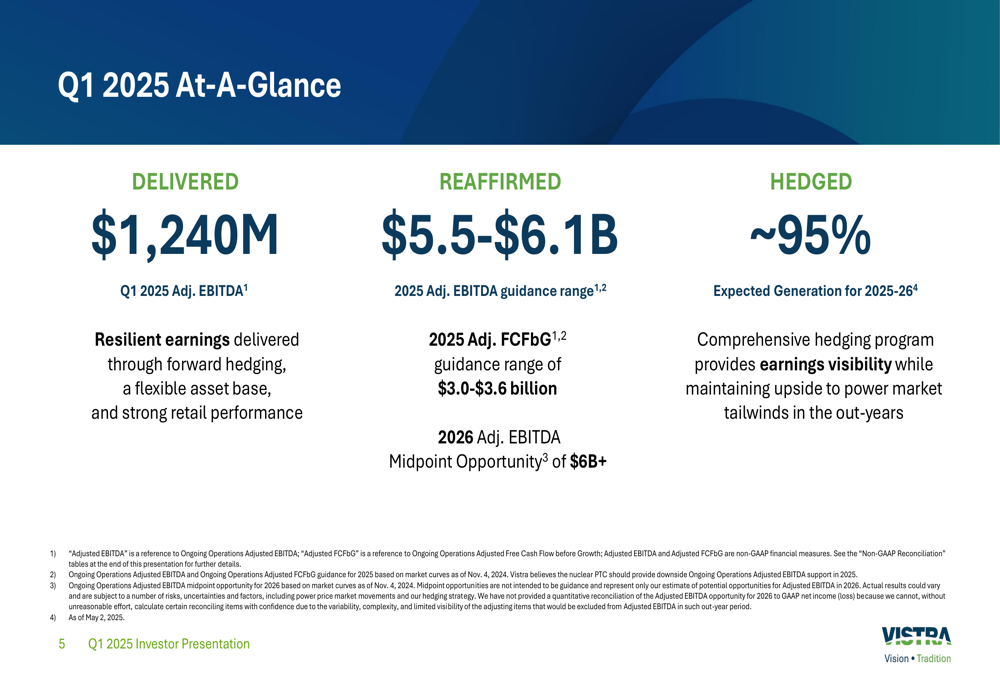

Vistra delivered $1.24 billion in Adjusted EBITDA for Q1 2025, with both generation and retail segments showing significant improvement compared to the same period last year. The company highlighted resilient earnings delivered through forward hedging, a flexible asset base, and strong retail performance.

As shown in the following detailed breakdown of Q1 results, the generation segment contributed $1,056 million, while the retail segment added $184 million:

Generation results were $218 million favorable compared to Q1 2024, driven by strong fleet commercial availability, higher wholesale prices through hedging, and the inclusion of two additional months of Energy Harbor’s generation results. Meanwhile, the retail segment showed even more dramatic improvement, with results $212 million favorable compared to Q1 2024, driven by strong customer counts and margins, favorable weather, and the inclusion of two additional months of Energy Harbor’s retail results.

Financial Outlook and Guidance

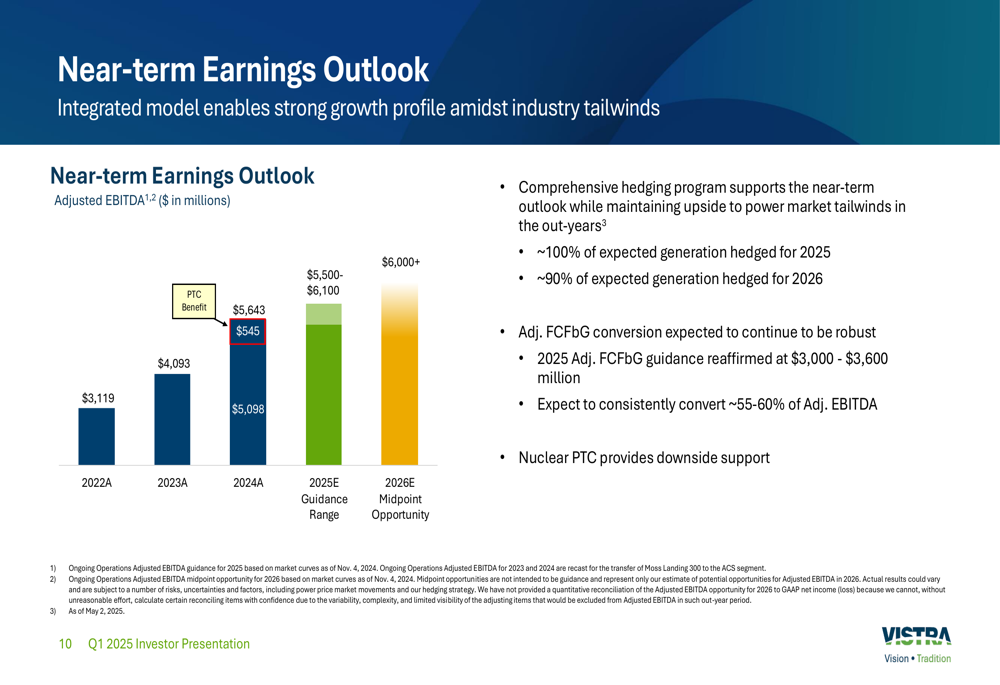

Vistra reaffirmed its 2025 guidance ranges, projecting Adjusted EBITDA between $5.5 billion and $6.1 billion, and Adjusted Free Cash Flow before Growth between $3.0 billion and $3.6 billion. The company also maintained its 2026 Adjusted EBITDA midpoint opportunity of over $6 billion, highlighting continued growth expectations.

The company’s comprehensive hedging program provides earnings visibility while maintaining upside potential from power market tailwinds. As illustrated in the following chart, Vistra has demonstrated consistent earnings growth since 2022 and expects this trend to continue:

Vistra has hedged approximately 95% of its expected generation for 2025-2026, with the near-term outlook supported by this hedging program while maintaining upside to power market tailwinds in later years. The company expects to consistently convert approximately 55-60% of Adjusted EBITDA to free cash flow, with additional downside protection provided by the Nuclear Production Tax Credit.

Strategic Initiatives and Capital Allocation

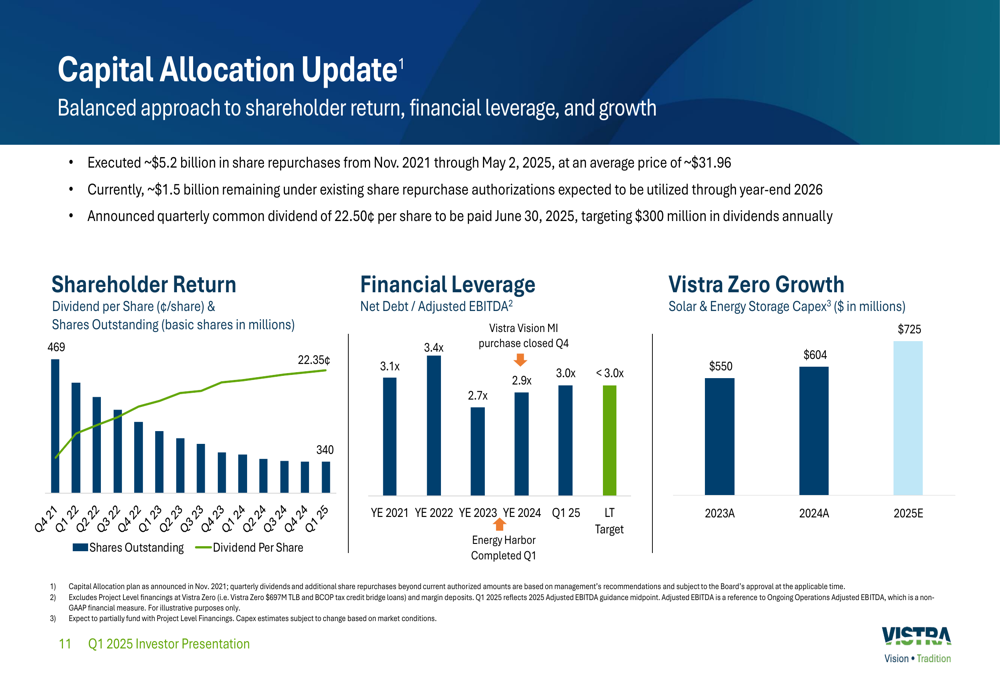

Vistra continues to execute on its capital allocation strategy, focusing on shareholder returns while maintaining a strong balance sheet. The company has executed approximately $5.2 billion in share repurchases from November 2021 through May 2, 2025, at an average price of around $31.96 per share. Additionally, Vistra announced a quarterly common dividend of 22.50 cents per share to be paid on June 30, 2025, targeting $300 million in annual dividends.

The following chart illustrates Vistra’s capital allocation priorities, including dividend growth, share count reduction, and financial leverage management:

The company maintains a strong balance sheet with net leverage of 3.0x as of Q1 2025, below its long-term target of less than 3.0x. This financial flexibility supports Vistra’s comprehensive hedging program and provides options for additional debt reduction, share repurchases, or growth investments.

Vistra is also advancing its clean energy transition through its Vistra Zero initiative, with planned capital expenditures of $725 million in 2025 for solar and energy storage projects. Construction continues on Vistra Zero projects for major customers including Amazon (NASDAQ:AMZN) and Microsoft (NASDAQ:MSFT), with a significant development pipeline across the fleet, including potential for approximately 10% nuclear uprates.

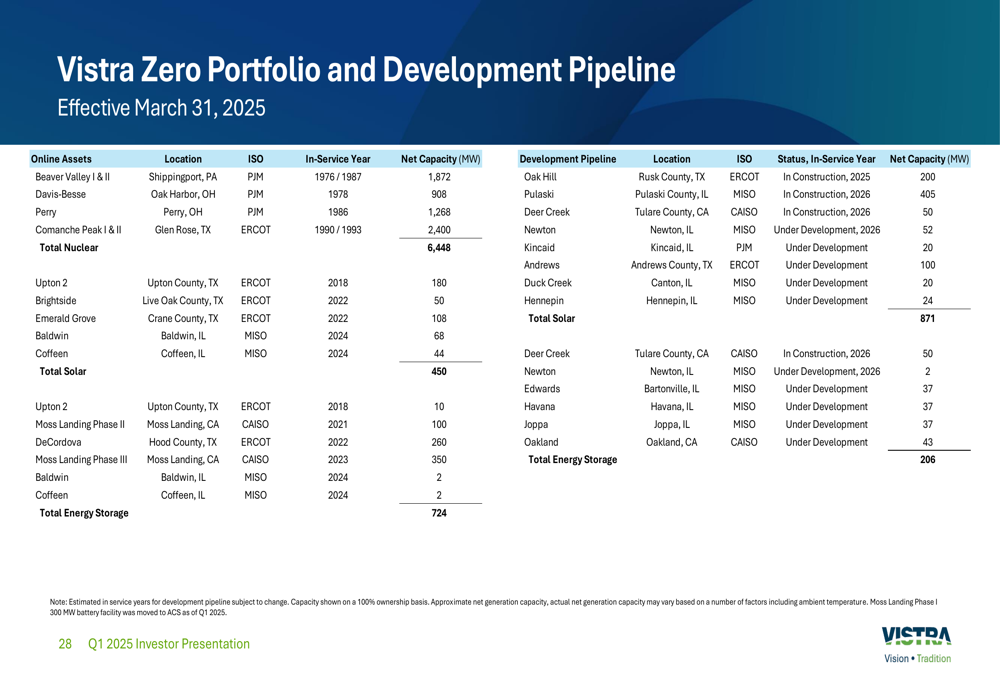

The following slide details Vistra’s zero-carbon portfolio and development pipeline:

Industry Position and Growth Drivers

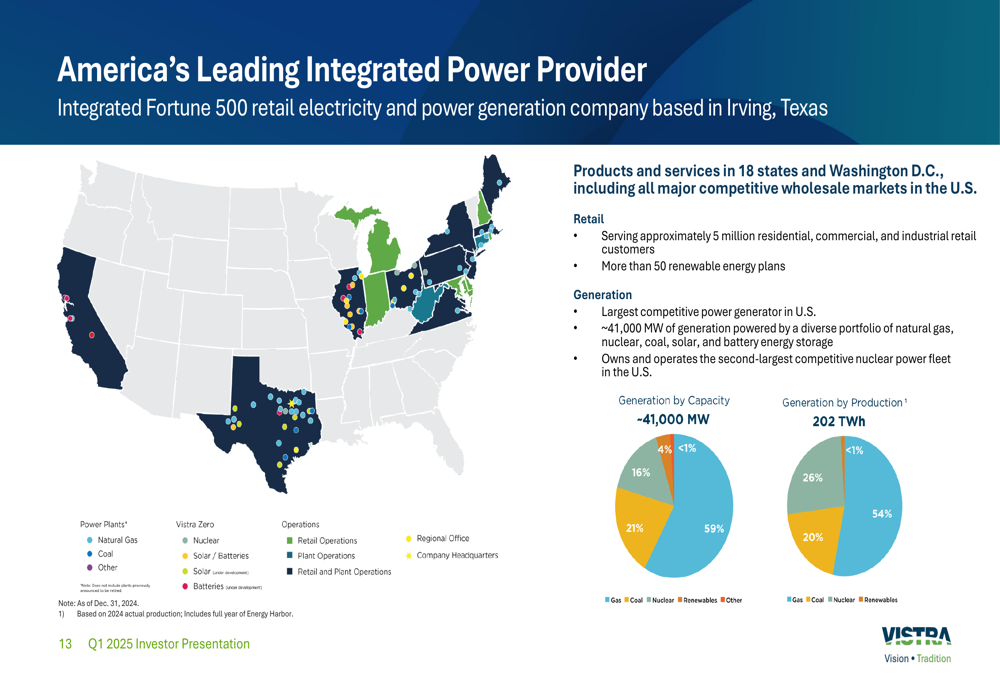

As America’s leading integrated power provider, Vistra operates a diverse portfolio of generation assets totaling approximately 41,000 MW and serves around 5 million retail customers across 18 states and Washington D.C. The company owns the second-largest competitive nuclear fleet in the U.S. and offers more than 50 renewable energy plans.

The following overview illustrates Vistra’s scale and diversification:

Vistra is benefiting from strong demand growth in its key markets, with year-over-year weather-adjusted growth in energy of 3.0% in PJM and 6.5% in ERCOT during Q1 2025. The company expects load growth at approximately 4% CAGR through 2030, with data centers accounting for about 40% of new demand. Additional growth drivers include oil and gas electrification led by the Permian Basin and LNG projects, as well as continued reshoring of industrial activities.

This demand growth is illustrated in the following chart:

Vistra’s environmental stewardship efforts continue to progress, with a 50% reduction in greenhouse gas emissions achieved in 2024 compared to the 2010 baseline. The company has retired approximately 15,150 MW of fossil generation since 2010 and is on track for approximately 20,000 MW total retired by 2027. Simultaneously, Vistra has achieved over 200% growth in zero-carbon generation since 2018, with 7,922 MW online and additional projects under development.

The company’s at-a-glance summary for Q1 2025 highlights its key achievements and outlook:

With its integrated business model, disciplined capital allocation, resilient balance sheet, and strategic energy transition initiatives, Vistra is well-positioned to continue delivering strong results amid growing power demand and evolving market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.