Intel stock spikes after report of possible US government stake

Introduction & Market Context

Vitesse Energy (NYSE:VTS) recently released its August 2025 investor presentation, highlighting the company’s Bakken-focused asset portfolio and high-yield dividend strategy. The presentation comes against a backdrop of mixed financial performance, with the company having missed earnings expectations in Q1 2025 despite beating revenue forecasts.

Currently trading at $23.14 (as of August 1, 2025), Vitesse positions itself as a dividend-focused energy company with significant exposure to the Bakken oil field in North Dakota. The stock has recovered from its 52-week low of $18.90 but remains below its high of $28.41, reflecting ongoing investor concerns following the Q1 earnings miss when EPS came in at $0.08 versus an expected $0.46.

Executive Summary

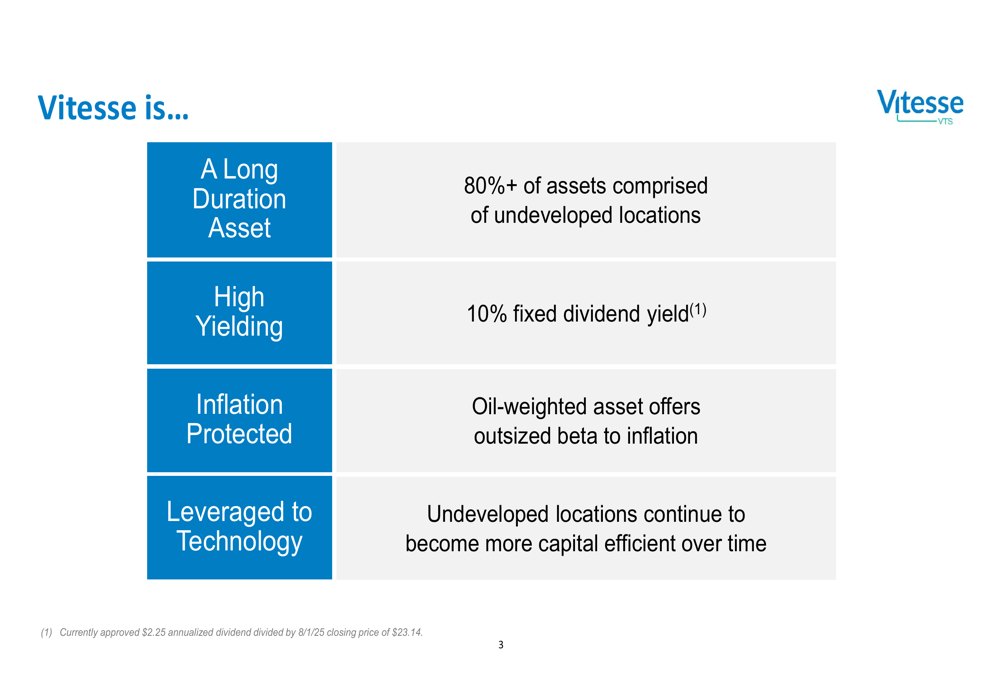

Vitesse’s presentation emphasizes four key investment attributes: long-duration assets, high dividend yield, inflation protection, and technology leverage. The company highlights that over 80% of its assets consist of undeveloped locations, providing a long runway for future development.

As shown in the following highlights slide, the company is positioning itself primarily as a yield vehicle for investors:

The 10% fixed dividend yield (based on the $2.25 annualized dividend and August 1, 2025 closing price) forms the cornerstone of Vitesse’s investor appeal. This yield is slightly lower than the 10.5% mentioned in the Q1 earnings report, reflecting the modest recovery in share price since that announcement.

Strategic Initiatives

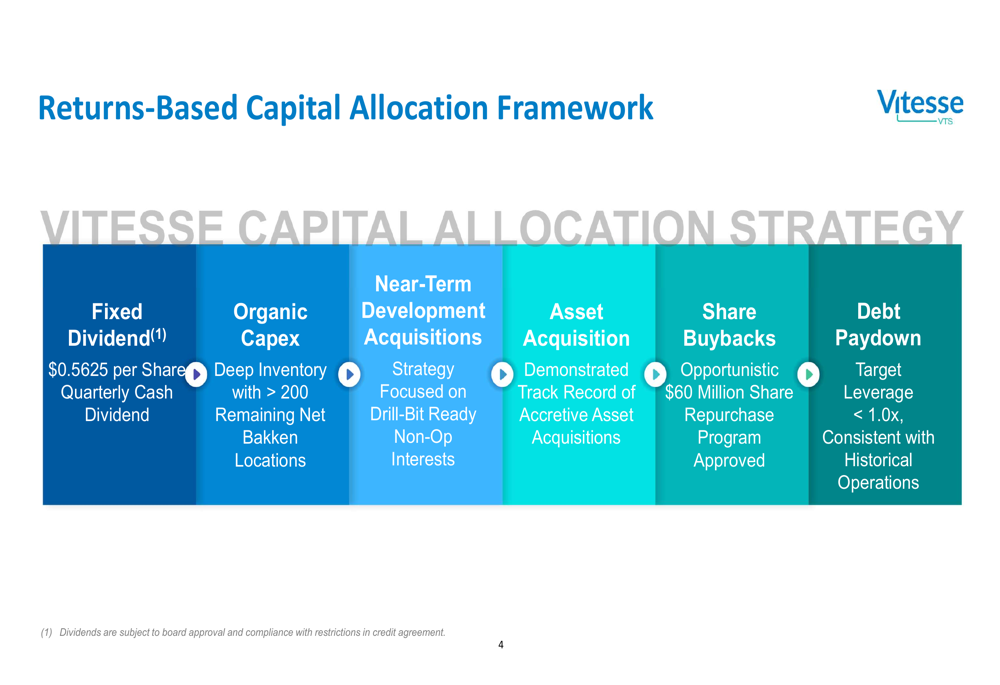

Vitesse’s capital allocation strategy prioritizes its dividend while balancing growth opportunities and financial discipline. The company has established a clear hierarchy for deploying capital, starting with its fixed quarterly dividend of $0.5625 per share.

The following capital allocation framework illustrates the company’s priorities:

Beyond dividends, Vitesse focuses on organic capital expenditure to develop its inventory of over 200 remaining net Bakken locations. The company has also approved a $60 million share repurchase program and targets a conservative leverage ratio below 1.0x, consistent with its historical operations.

Notably, in the Q1 2025 earnings report, Vitesse announced a 32% reduction in its CapEx guidance for 2025 to a range of $80-110 million, suggesting a more cautious approach to development than might be indicated by the presentation’s growth-oriented messaging.

Detailed Financial Analysis

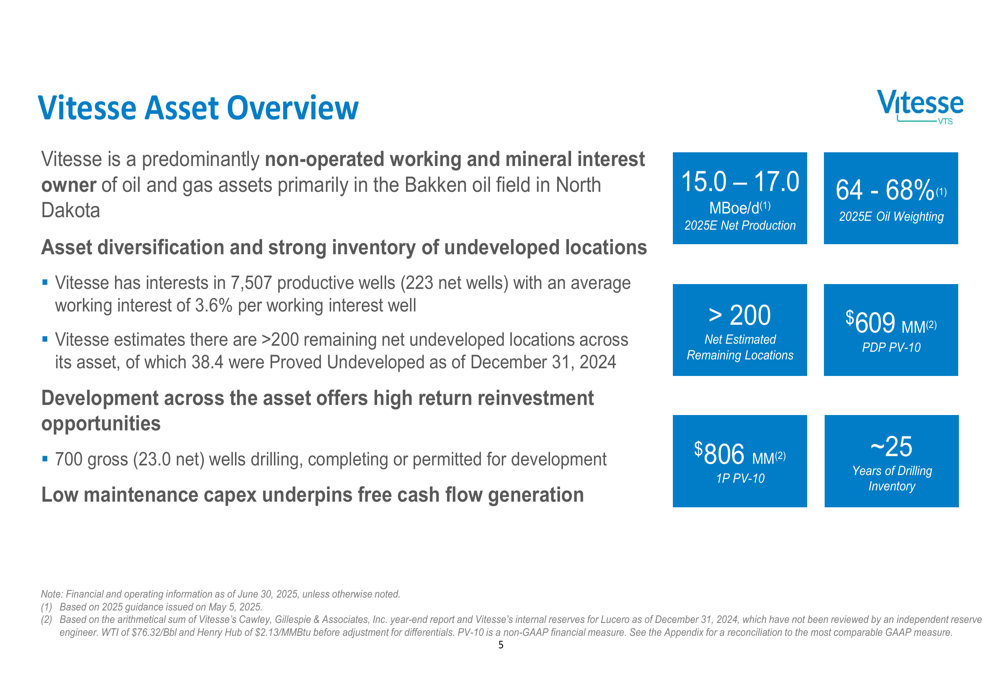

Vitesse’s asset base consists primarily of non-operated working and mineral interests in the Bakken oil field. The company has interests in 7,507 productive wells (223 net wells) and estimates more than 200 remaining net undeveloped locations, representing approximately 25 years of drilling inventory.

The following asset overview highlights key operational and financial metrics:

The company projects 2025 net production of 15.0-17.0 MBoe/d with oil comprising 64-68% of total production. These projections align with the guidance maintained in the Q1 earnings report despite the CapEx reduction.

Vitesse’s PDP (Proved Developed Producing) PV-10 value stands at $609 million, while its 1P (Proved) PV-10 value reaches $806 million. These valuations provide significant coverage for the company’s market capitalization of approximately $824 million.

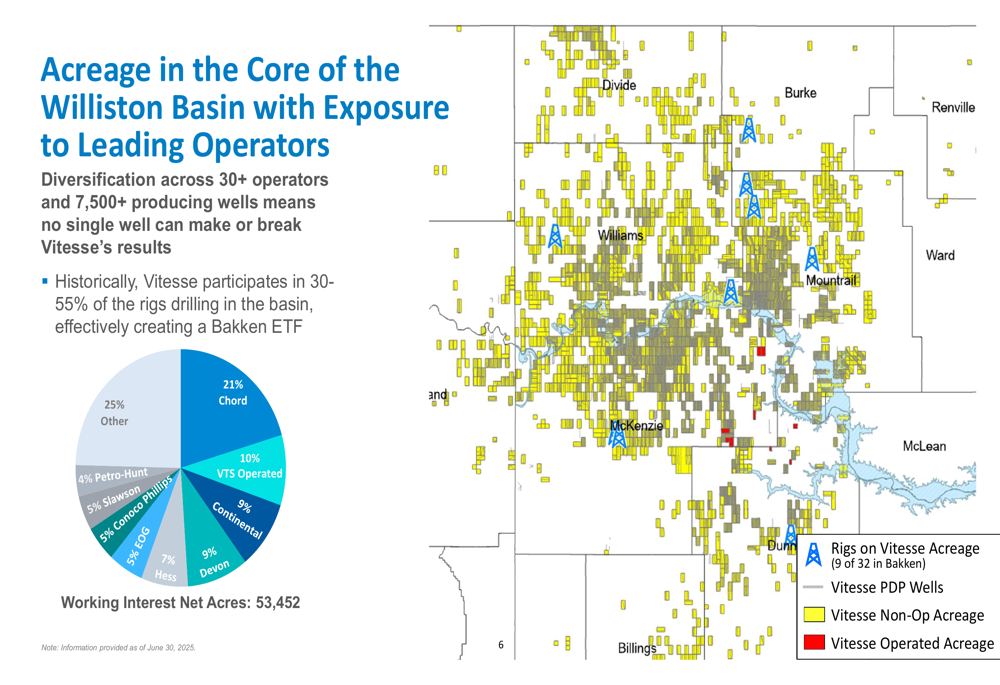

The company’s core acreage is strategically positioned within the Williston Basin, with exposure to more than 30 operators:

This diversification across operators reduces single-operator risk, with Chord representing the largest exposure at 21%, followed by Vitesse’s operated assets at 10%, and Devon at 9%.

Competitive Advantages

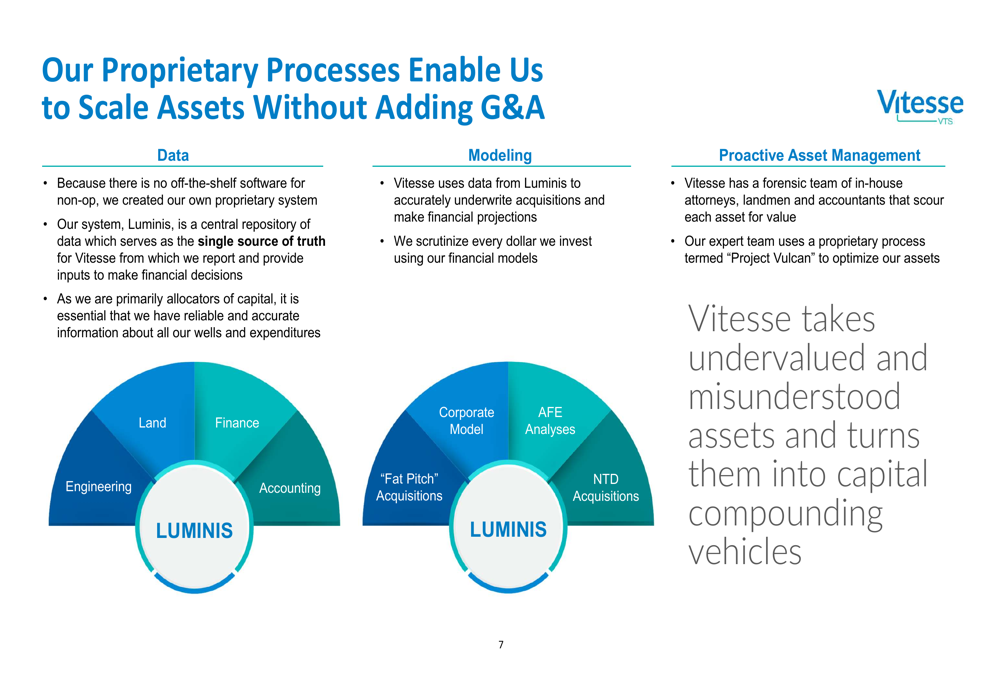

Vitesse emphasizes its proprietary processes as a key differentiator, enabling the company to scale assets efficiently without adding significant general and administrative expenses.

The following diagram illustrates Vitesse’s integrated approach to data management and asset optimization:

The company has developed a proprietary system called "Luminis" that serves as a central repository for data, addressing the lack of off-the-shelf software solutions for non-operated assets. This system supports accurate financial modeling and asset management through a process termed "Project Vulcan."

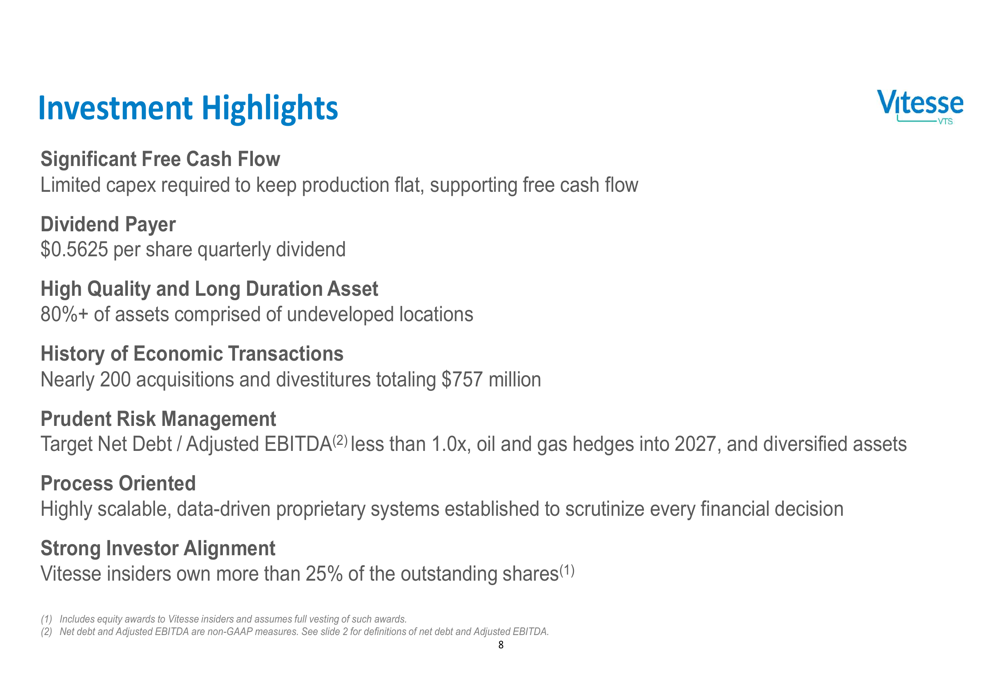

Investment Case

Vitesse summarizes its investment thesis with seven key points that emphasize free cash flow generation, dividend payments, and prudent risk management:

Notably, insiders own more than 25% of outstanding shares, suggesting strong alignment with shareholder interests. This insider ownership may provide some reassurance to investors concerned about the recent earnings miss.

Forward-Looking Statements

Despite the optimistic tone of the presentation, Vitesse faces several challenges that warrant investor attention. The significant Q1 2025 earnings miss (EPS of $0.08 versus expected $0.46) raises questions about the company’s ability to consistently deliver on financial expectations, even as revenue exceeded forecasts at $66.17 million.

The reduction in CapEx guidance by 32% for 2025 suggests potential constraints on growth or a more conservative outlook than previously anticipated. However, this reduced capital spending could support free cash flow and dividend sustainability in the near term.

CEO Bob Garrity emphasized in the Q1 earnings call that "Our product is our dividend," reinforcing the company’s commitment to maintaining its payout despite operational challenges. With a current yield of approximately 10%, Vitesse offers one of the higher dividend yields in the energy sector, though sustainability will depend on commodity price stability and operational execution.

As Vitesse navigates the volatile energy market, investors should closely monitor production performance, capital efficiency, and the company’s ability to maintain its dividend while managing leverage targets below 1.0x. The company’s long-duration asset base provides a solid foundation, but execution will be key to delivering on the promises outlined in this August 2025 presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.