AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Vitrolife AB (STO:VITR) presented its first quarter 2025 results on April 24, showing flat sales growth in Swedish krona but organic growth of 3% when excluding discontinued business. The reproductive health technology company’s stock declined 4.73% to 156.4 SEK following the presentation, suggesting investors were concerned about declining profitability metrics despite the company’s stable sales performance.

The presentation, delivered by CEO Bronwyn Brophy O’Connor and Acting CFO Helena Wennerström, highlighted Vitrolife’s regional diversification strategy, with strong performance in EMEA offsetting significant weakness in the APAC region.

Quarterly Performance Highlights

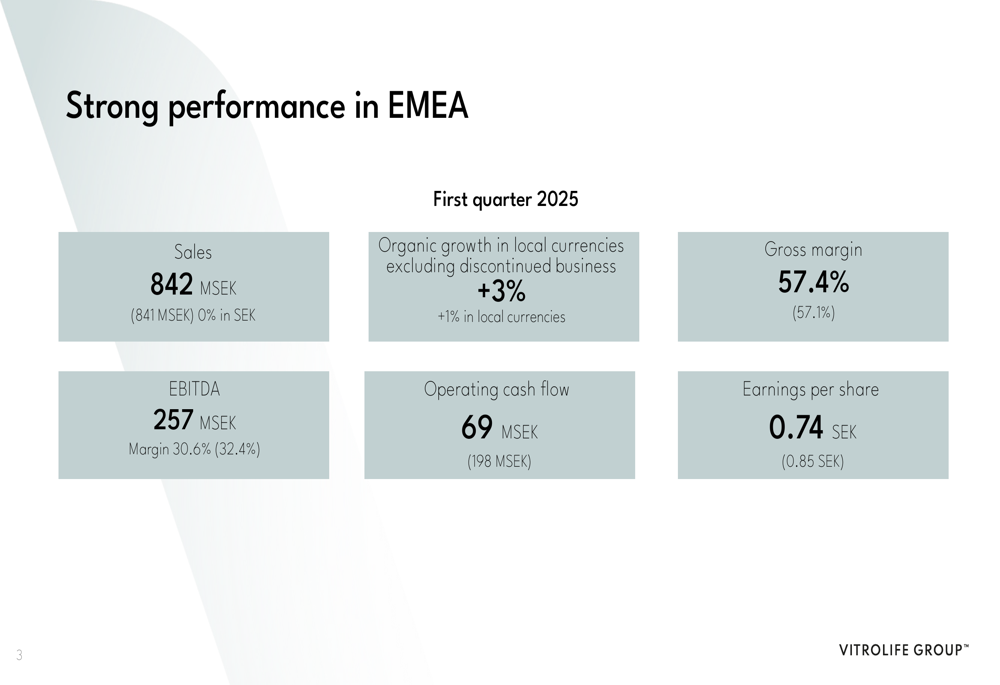

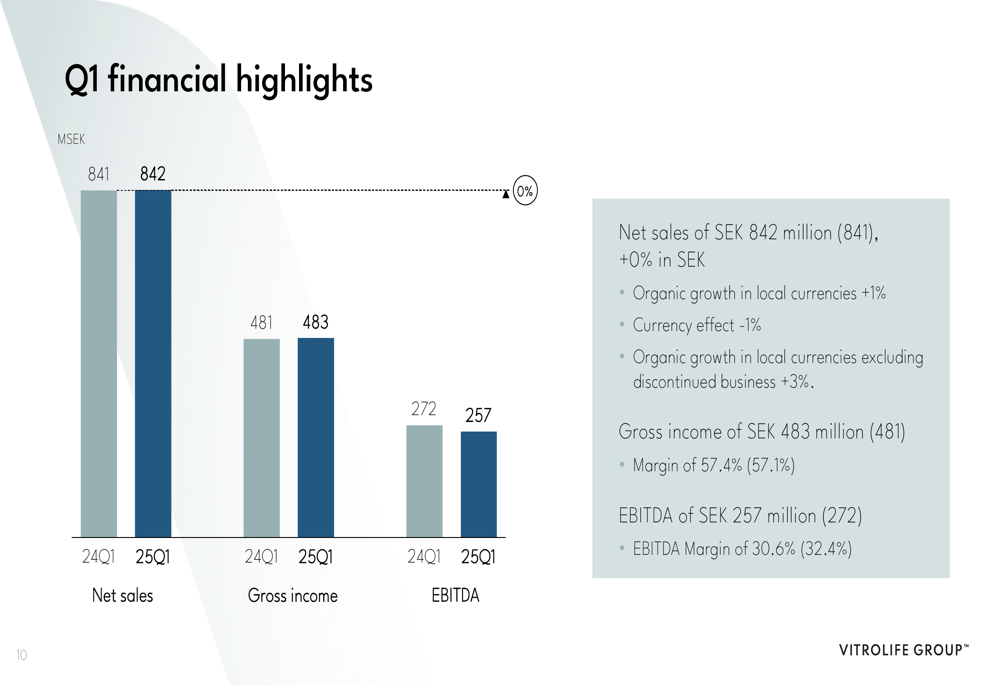

Vitrolife reported Q1 2025 sales of 842 MSEK, virtually unchanged from 841 MSEK in Q1 2024. Organic growth in local currencies was 1%, while organic growth excluding discontinued business reached 3%. The company’s gross margin improved slightly to 57.4% from 57.1% in the same period last year.

As shown in the following comprehensive financial overview:

However, profitability metrics declined year-over-year, with EBITDA falling to 257 MSEK (30.6% margin) compared to 272 MSEK (32.4% margin) in Q1 2024. Earnings per share decreased to 0.74 SEK from 0.85 SEK, while operating cash flow saw a significant reduction to 69 MSEK from 198 MSEK in the prior year.

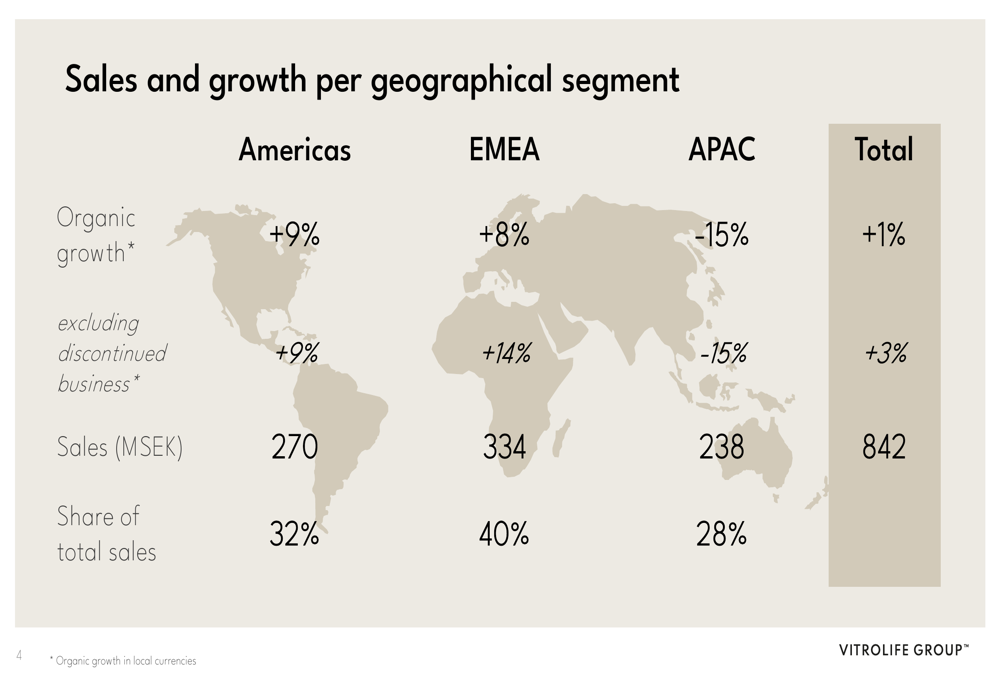

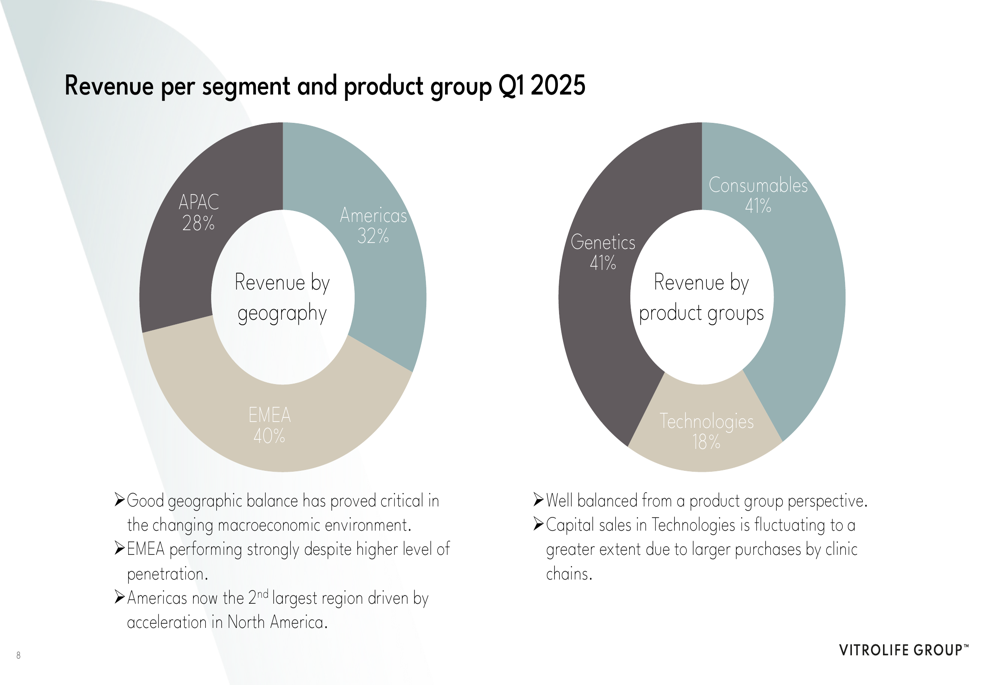

The company’s regional performance varied significantly, with EMEA showing strong organic growth of 14% excluding discontinued business, while APAC declined by 15%, as illustrated in this geographical breakdown:

Regional Analysis

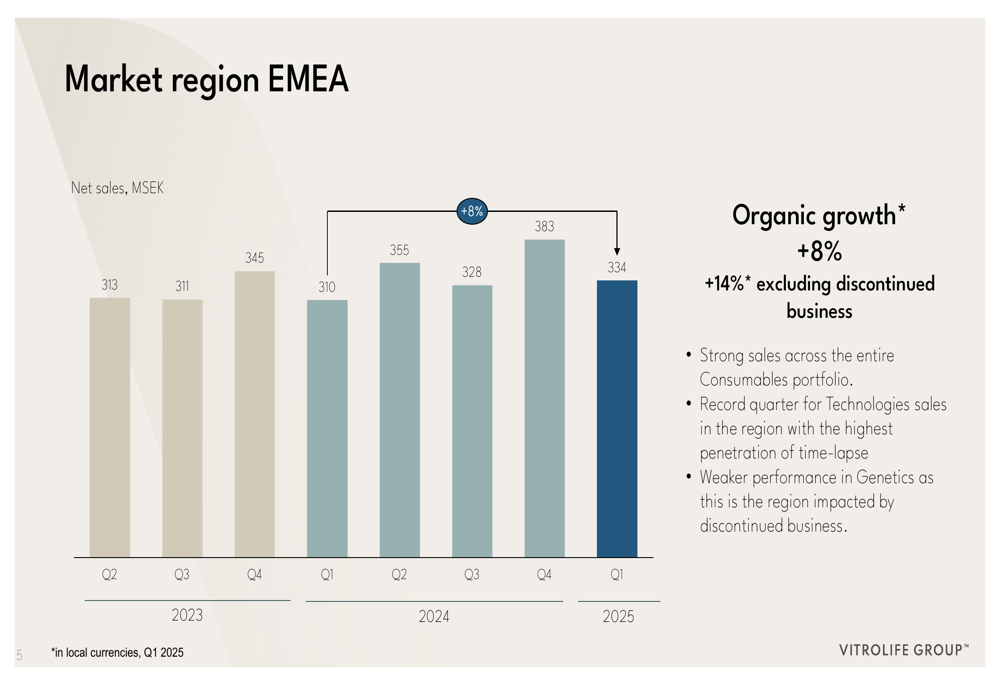

EMEA emerged as Vitrolife’s strongest performing region, accounting for 40% of total sales at 334 MSEK. The company reported strong sales across its entire Consumables portfolio and a record quarter for Technologies sales in the region, which has the highest penetration of time-lapse technology. However, the Genetics segment showed weaker performance due to discontinued business.

The following chart illustrates EMEA’s consistent sales performance over recent quarters:

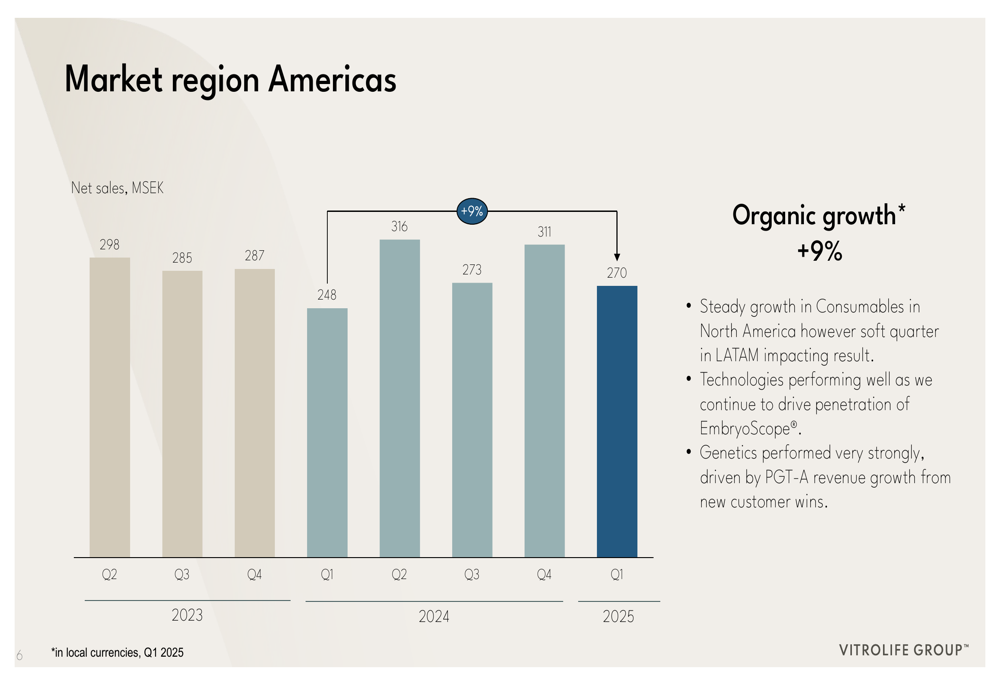

The Americas region, now Vitrolife’s second-largest market at 32% of total sales, delivered 9% organic growth. North America showed steady growth in Consumables, while Latin America had a softer quarter. The Genetics segment performed strongly in this region, driven by PGT-A (preimplantation genetic testing for aneuploidy) revenue growth from new customer wins.

APAC experienced the most challenging quarter with a 15% organic decline, representing 28% of total sales. The company attributed this weakness to the Year of the Dragon comparison and an exceptionally strong Q1 2024, which included a record number of EmbryoScope sales. Vitrolife noted that cycle numbers began showing signs of recovery toward the end of March, suggesting potential improvement in coming quarters.

Product Mix and Profitability

Vitrolife’s revenue is well-balanced across product categories, with Consumables and Genetics each accounting for 41% of sales, while Technologies represents 18%. This distribution reflects the company’s diversified approach to the reproductive health market.

The following chart illustrates this balanced revenue distribution:

Despite stable sales, Vitrolife’s profitability metrics declined year-over-year. EBITDA fell by 5.5% to 257 MSEK, with margin compression of 1.8 percentage points to 30.6%. This decline was partly driven by a 6% increase in operating expenses, primarily in selling expenses, which rose from 169 MSEK in Q1 2024 to 183 MSEK in Q1 2025.

The company’s financial position remains solid, with Net Debt/EBITDA improving to 0.6 from 0.9 a year earlier. However, the significant decline in operating cash flow to 69 MSEK from 198 MSEK warrants attention and may explain some of the negative market reaction to the results.

Strategic Initiatives

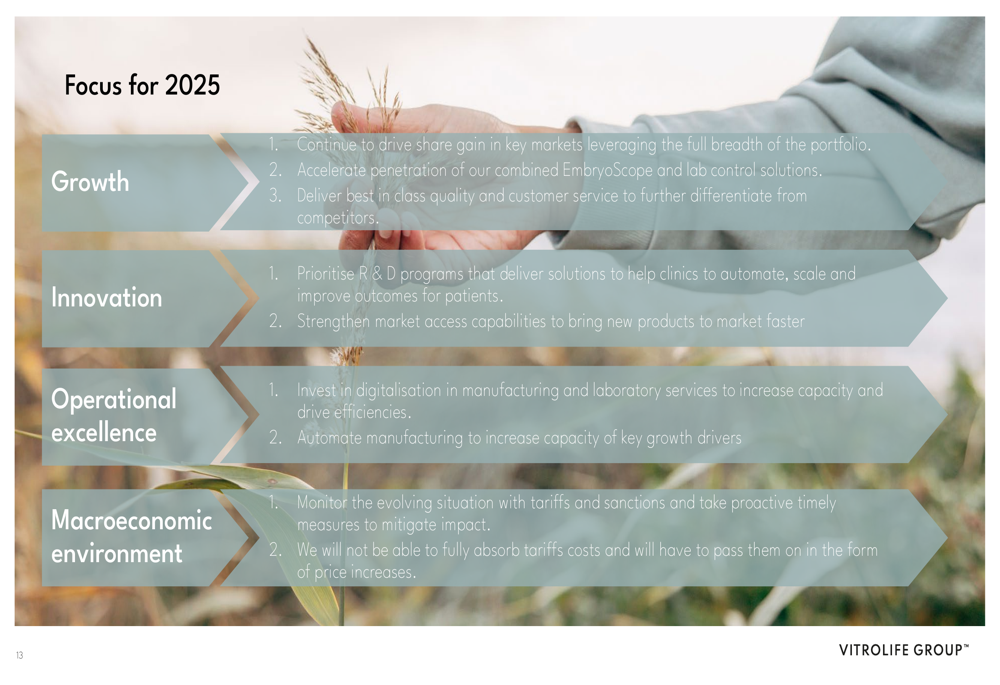

Looking ahead, Vitrolife outlined four key focus areas for 2025: growth, innovation, operational excellence, and addressing macroeconomic challenges. The company aims to drive market share gains by leveraging its full portfolio and accelerating the penetration of its combined EmbryoScope and lab control solutions.

The following slide details Vitrolife’s strategic priorities:

In innovation, Vitrolife is prioritizing R&D programs that help clinics automate, scale, and improve patient outcomes, while strengthening market access capabilities to bring new products to market faster. For operational excellence, the company is investing in digitalization in manufacturing and laboratory services to increase capacity and drive efficiencies.

Notably, Vitrolife highlighted concerns about the evolving situation with tariffs and sanctions, stating it would need to pass on some tariff costs through price increases. This follows the company’s previous disclosure about discontinuing certain business due to international sanctions, which impacted about 3% of 2024 sales.

Forward-Looking Statements

While Vitrolife did not provide specific numerical guidance for the remainder of 2025, the company’s strategic focus suggests continued emphasis on geographic diversification and product innovation. The signs of recovery in APAC cycle numbers toward the end of Q1 could indicate improved performance in that region for upcoming quarters.

The macroeconomic challenges, particularly related to tariffs and sanctions, remain a concern that could impact margins if the company is unable to fully pass increased costs to customers. However, Vitrolife’s balanced geographic and product portfolio provides some resilience against regional fluctuations, as demonstrated by the strong EMEA performance offsetting APAC weakness in Q1 2025.

Investors will likely focus on whether Vitrolife can reverse the declining trends in profitability and cash flow while maintaining its sales momentum, particularly as the APAC region potentially recovers in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.