Beamr video compression achieves up to 50% improvement for AVs

Introduction & Market Context

Vroom (OTC:VRMMQ) Inc (NASDAQ:VRM), the automotive e-commerce platform, presented its first quarter 2025 earnings results on May 14, 2025, highlighting improved financial metrics and operational progress. The company, which operates through three distinct business segments, reported significant growth in origination volume and a substantial increase in liquidity compared to the previous quarter.

Vroom’s stock closed at $27.57 on July 22, 2025, down 0.25% for the day. The company’s shares have traded between $12.00 and $41.36 over the past 52 weeks, reflecting ongoing market volatility in the automotive retail sector.

Quarterly Performance Highlights

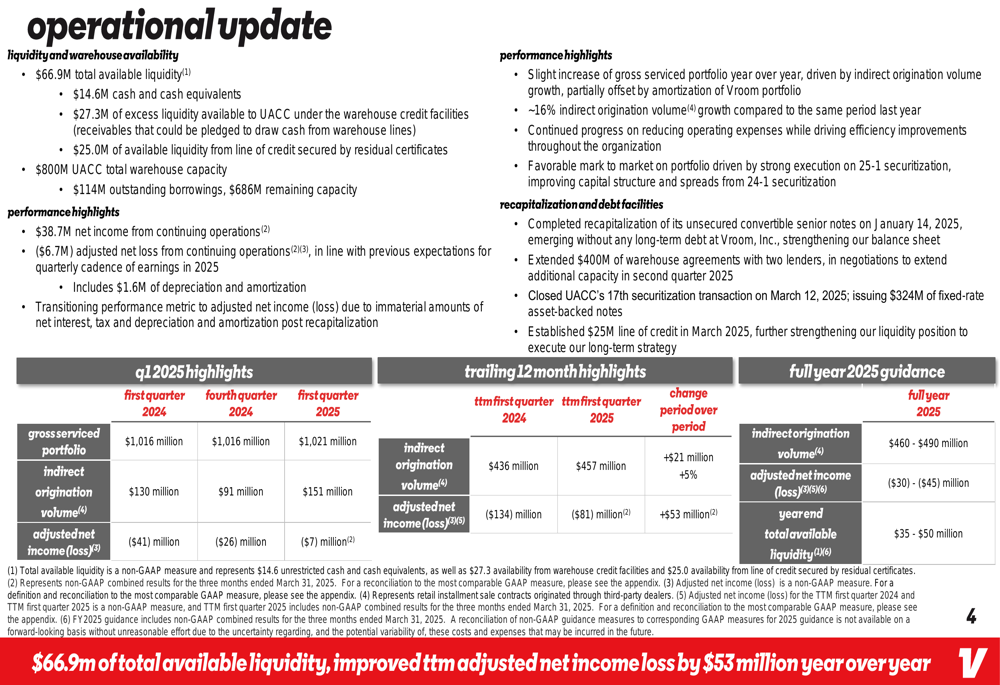

Vroom reported net income from continuing operations of $38.7 million for Q1 2025, while posting an adjusted net loss of $6.7 million. The company achieved approximately 16% growth in indirect origination volume, reaching $130 million for the quarter. Total (EPA:TTEF) available liquidity surged to $66.9 million, a dramatic improvement from just $2 million at the end of December 2024.

As shown in the following operational update slide, Vroom completed several significant financial transactions during the quarter, including a recapitalization, extension of $400 million in warehouse agreements, and the closure of United Auto Credit’s 17th securitization transaction:

The company’s gross serviced portfolio reached $1.021 billion, while its United Auto Credit (UACC) division maintained a total warehouse capacity of $800 million. Management highlighted that trailing twelve-month adjusted net income loss improved by $53 million year-over-year, demonstrating progress in the company’s financial recovery efforts.

Detailed Financial Analysis

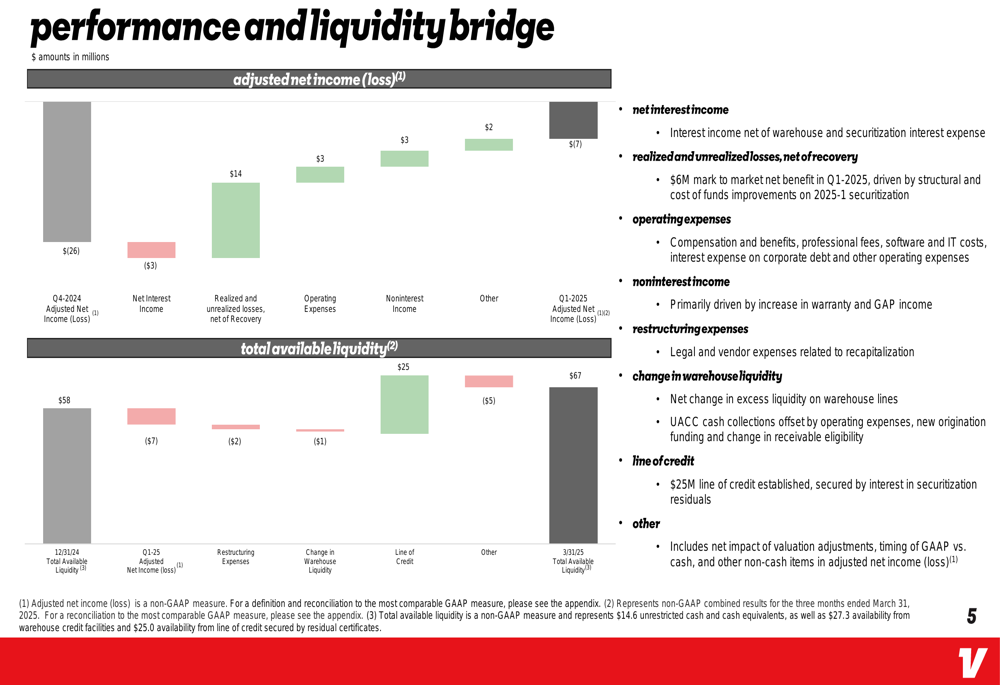

Vroom’s financial performance showed notable improvement from Q4 2024 to Q1 2025. The company reduced its adjusted net loss from $26 million to $7 million, driven by several positive factors including a $14 million increase in net interest income and $3 million improvements in both realized/unrealized losses and noninterest income.

The following bridge chart illustrates the key components that contributed to the company’s improved financial performance and liquidity position:

The establishment of a $25 million line of credit, secured by interest in securitization residuals, played a significant role in bolstering Vroom’s liquidity position. This strategic financial move, combined with operational improvements, helped transform the company’s liquidity situation from a precarious $2 million at year-end 2024 to a much healthier $67 million by March 31, 2025.

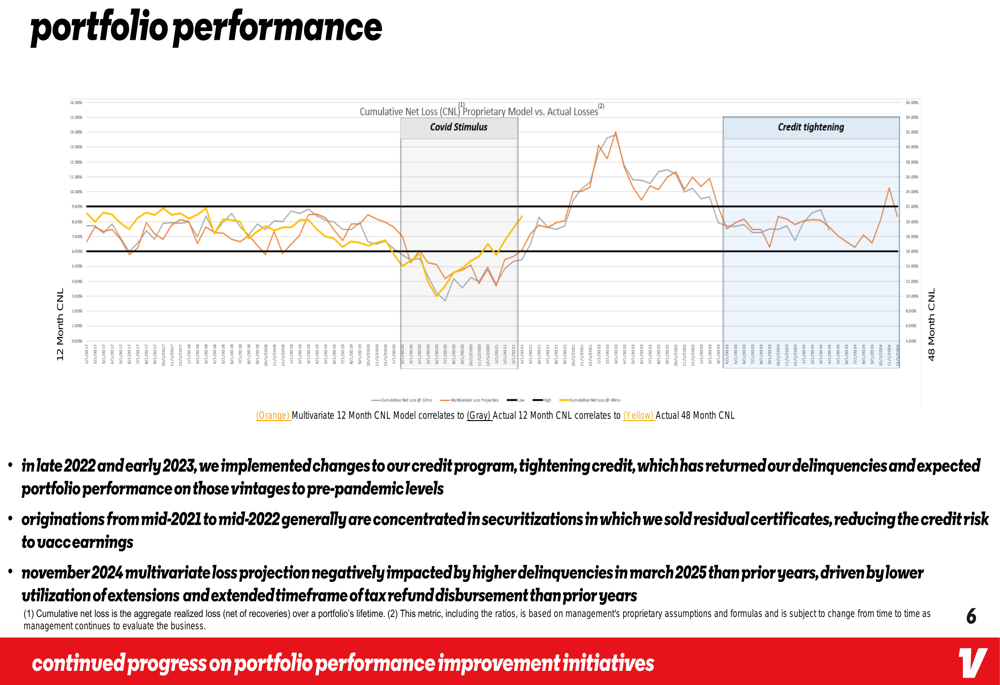

Portfolio performance remains a key focus area for the company. Management noted that credit program tightening implemented in late 2022 and early 2023 has returned delinquencies and expected portfolio performance to pre-pandemic levels for those vintages. However, the company did acknowledge higher delinquencies in March 2025 compared to prior years, attributed to lower utilization of extensions and extended timeframes for tax refund disbursements.

The following portfolio performance chart shows the company’s cumulative net loss projections versus actual losses:

Strategic Initiatives

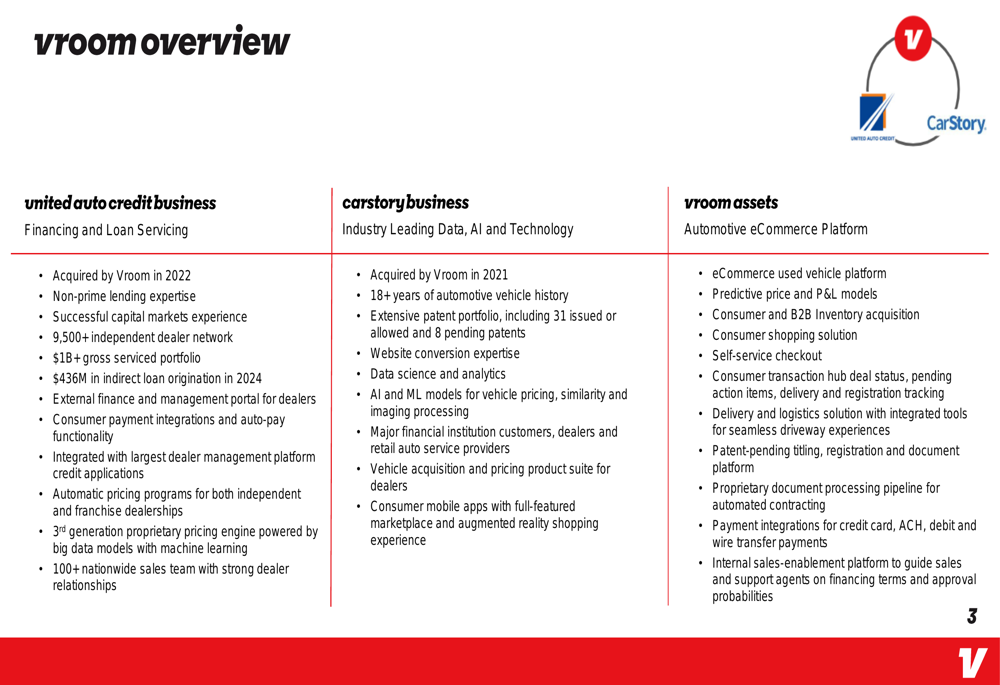

Vroom operates through three complementary business segments that provide diversified revenue streams and strategic advantages in the automotive retail space. The company’s business model leverages technology, financing capabilities, and e-commerce expertise to create an integrated automotive platform.

As illustrated in the company overview slide, each segment contributes unique capabilities to Vroom’s overall business strategy:

United Auto Credit, acquired by Vroom in 2022, brings non-prime lending expertise and a network of over 9,500 independent dealers. With a gross serviced portfolio exceeding $1 billion and $436 million in indirect loan origination in 2024, this division represents a significant component of Vroom’s business.

CarStory, acquired in 2021, provides data science, AI, and technology capabilities with 18+ years of automotive vehicle history and an extensive patent portfolio. This technology foundation supports Vroom’s pricing models and customer acquisition strategies.

The Vroom Assets segment encompasses the company’s e-commerce platform, featuring predictive pricing models, consumer and B2B inventory acquisition capabilities, and various tools for vehicle delivery and transaction processing.

Forward-Looking Statements

Looking ahead, Vroom provided full-year 2025 guidance projecting indirect origination volume between $460-$490 million, representing continued growth from the $436 million achieved in 2024. The company expects an adjusted net loss between $30-$45 million for the full year and anticipates year-end total available liquidity in the range of $35-$50 million.

This guidance suggests management expects some reduction in liquidity from current levels by year-end, potentially indicating planned investments or operational expenditures. However, the projected range still represents a substantial improvement from the $2 million liquidity position at the end of 2024.

The company’s focus on improving financial metrics while growing its origination volume reflects a balanced approach to achieving sustainable growth. With its diversified business model and improved liquidity position, Vroom appears positioned to continue its recovery trajectory, though challenges remain in achieving consistent profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.