Two National Guard members shot near White House

Introduction & Market Context

Wajax Corporation (TSX:WJX) released its Q1 2025 financial results on May 6, showing a 15.1% revenue increase to $555.0 million compared to the same period last year. The industrial products and services distributor demonstrated growth across all regions despite ongoing market challenges and margin pressure.

The company’s stock closed at $18.24 on May 5, 2025, representing a modest recovery from its significant drop following Q4 2024 earnings, which had disappointed investors with an EPS miss of 35.5%. Wajax’s Q1 results suggest some stabilization after that challenging quarter.

Quarterly Performance Highlights

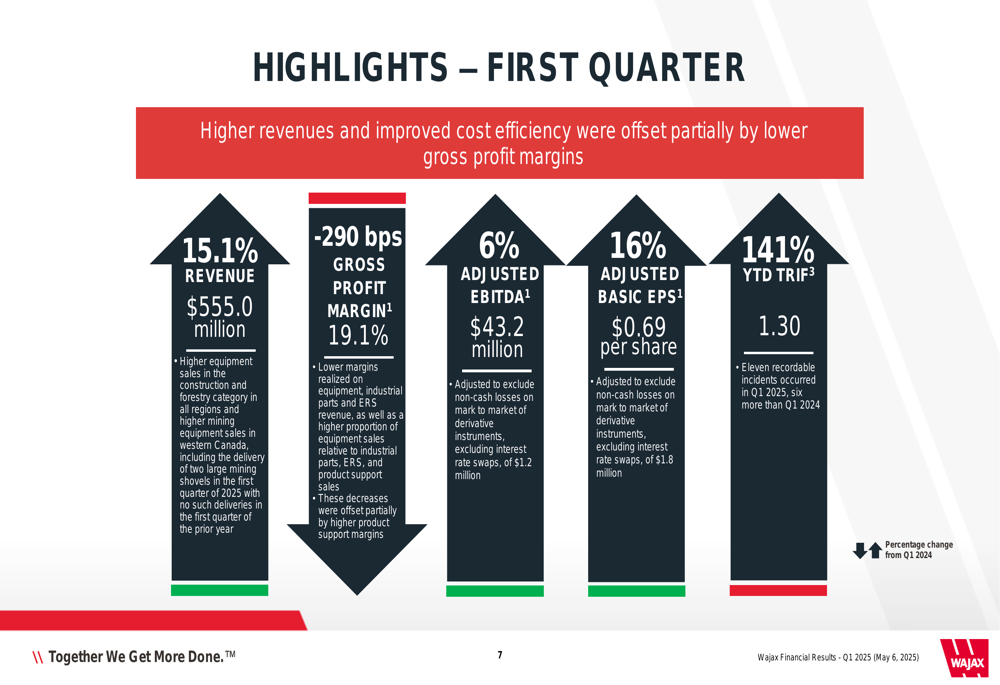

Wajax reported a 15.1% year-over-year revenue increase to $555.0 million for Q1 2025, with growth across all regions. However, gross profit margin decreased by 290 basis points to 19.1%, reflecting continued pressure on profitability despite showing improvement from the 17.1% reported in Q4 2024.

Adjusted EBITDA increased by 6% to $43.2 million, while adjusted basic earnings per share rose 16% to $0.69. The company’s safety performance deteriorated, with Total (EPA:TTEF) Recordable Incident Frequency (TRIF) increasing 141% to 1.30, representing eleven recordable incidents in Q1 2025 compared to five in Q1 2024.

As shown in the following quarterly highlights chart:

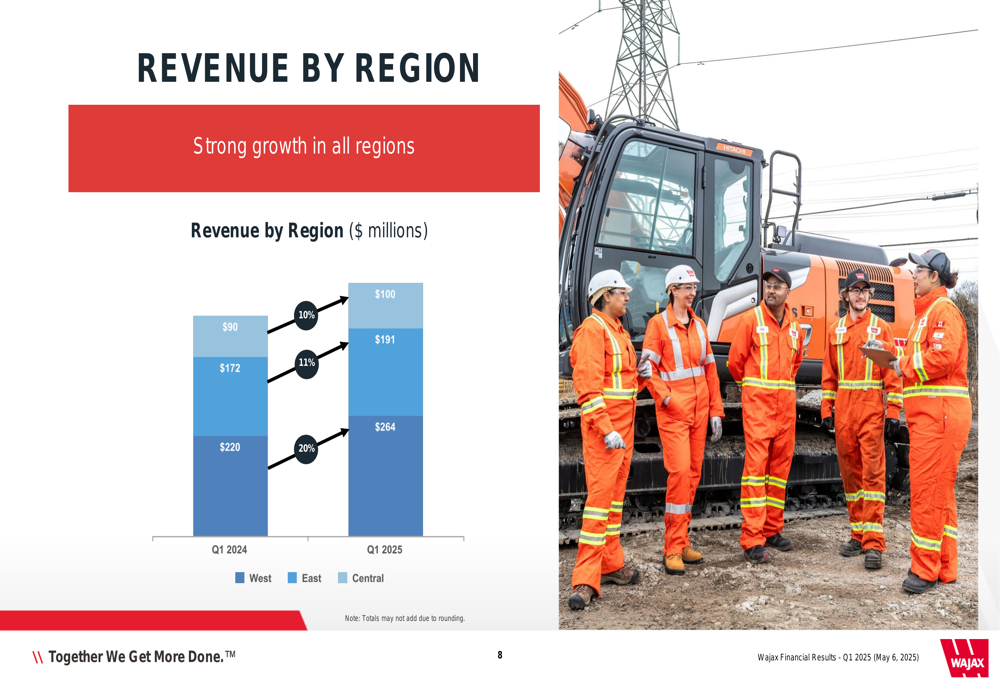

The company’s revenue growth was distributed across all geographic regions, with the Central region showing the strongest performance at a 20% increase, followed by the East region at 11% and the West region at 10%. This regional breakdown demonstrates broad-based demand for Wajax’s products and services.

The following chart illustrates this regional revenue growth:

Detailed Financial Analysis

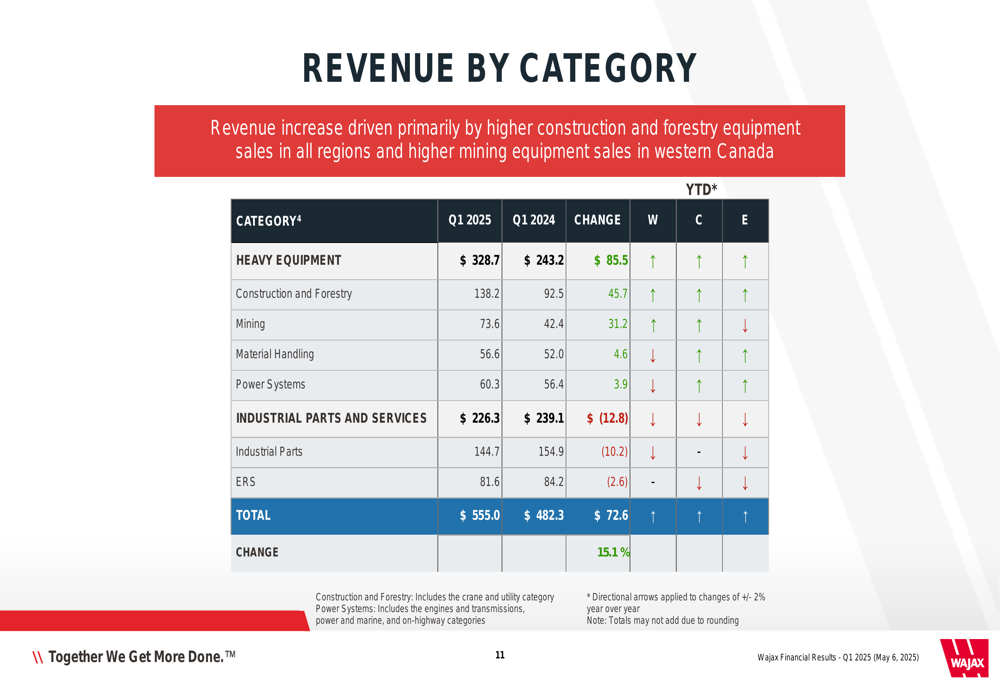

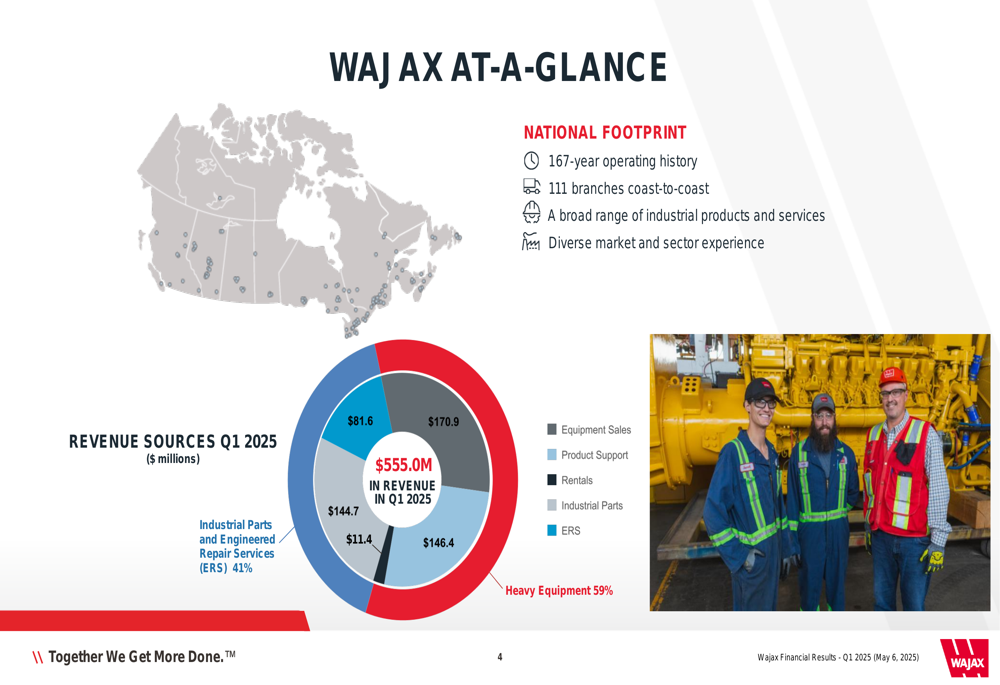

Wajax’s revenue mix for Q1 2025 shows Heavy Equipment accounting for 59% of total revenue ($328.7 million), while Industrial Parts and Engineered Repair Services (ERS) contributed 41% ($226.3 million). This represents a shift from Q1 2024, when Heavy Equipment accounted for $243.2 million and Industrial Parts and ERS contributed $239.1 million.

The breakdown of revenue by category is illustrated here:

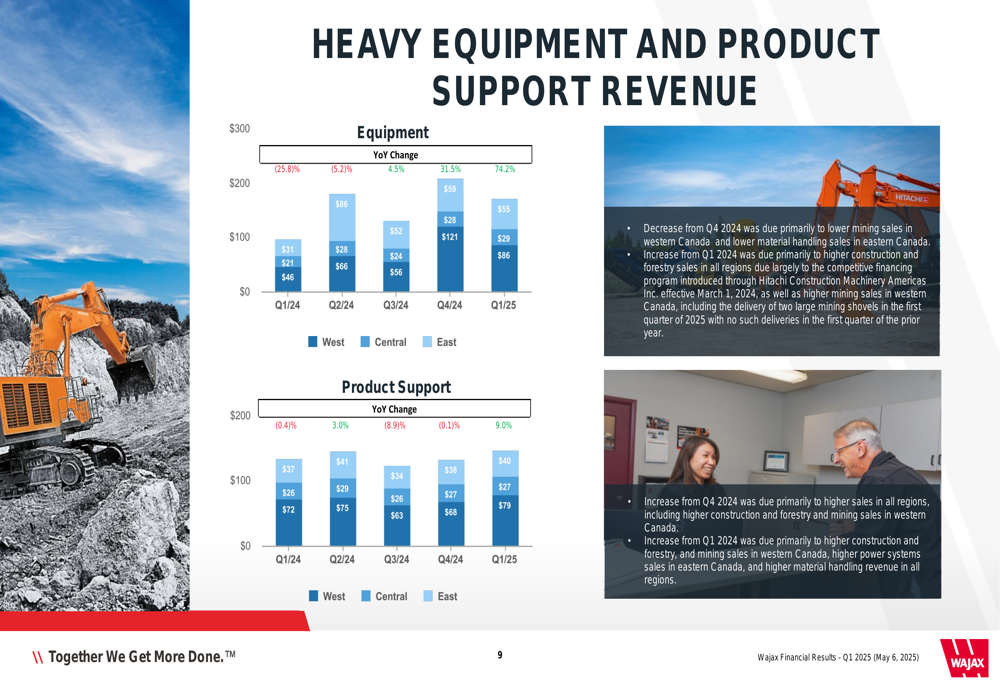

Heavy Equipment and Product Support revenue showed significant regional variations. In Heavy Equipment, the West region led with $86 million in Q1 2025, while Product Support was strongest in the East region at $79 million. This reflects the diverse nature of Wajax’s business across Canada’s regional economies.

The following chart details this category breakdown by region:

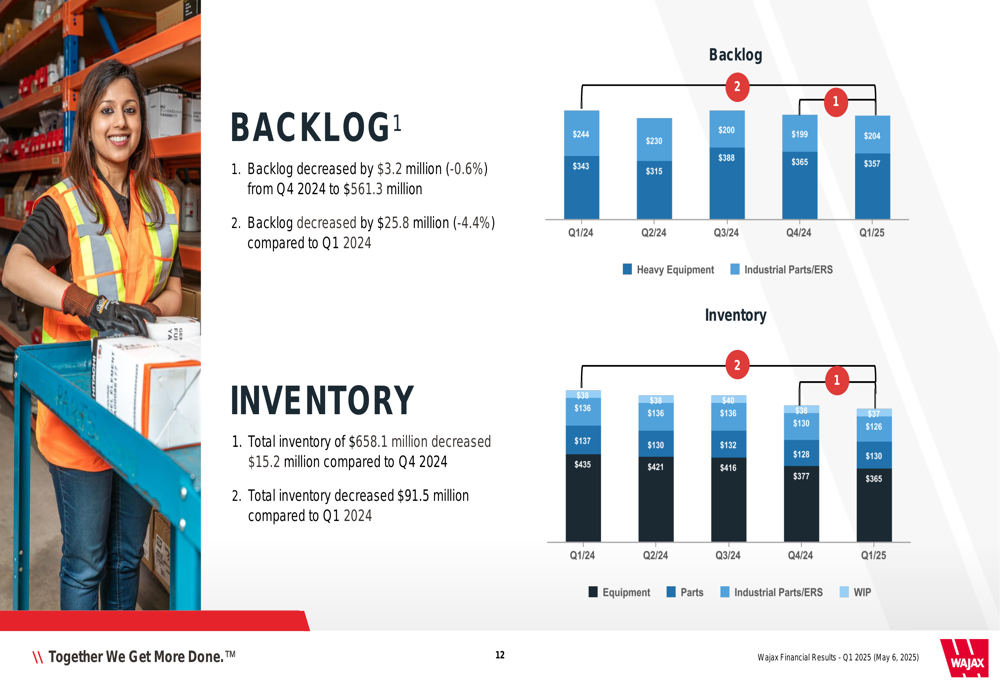

The company’s backlog decreased slightly by $3.2 million (-0.6%) from Q4 2024 to $561.3 million and decreased by $25.8 million (-4.4%) compared to Q1 2024. Total inventory stood at $658.1 million, down $15.2 million from Q4 2024 and $91.5 million from Q1 2024, showing progress on the company’s inventory reduction initiatives.

The backlog and inventory trends are shown in the following chart:

Working capital efficiency improved from Q4 2024 due to higher trailing 12-month revenue, and inventory turns improved due to higher trailing 12-month sales and lower average inventory levels. These improvements align with management’s stated focus on enhancing operational efficiency.

Strategic Initiatives

Wajax outlined six strategic priorities for 2025, focusing on building a people-first company, growing the existing business with emphasis on parts and service, maximizing the Hitachi (OTC:HTHIY) relationship, acquiring and integrating Industrial Parts and ERS businesses, improving cost structure, and continuing ERP system roll-out.

The company’s national footprint includes 111 branches coast-to-coast, supporting its diverse portfolio of industrial products and services. This extensive network provides Wajax with significant market reach across Canada’s industrial sectors.

As shown in the following overview of Wajax’s operations:

Management continues to execute initiatives to reduce inventory, lower costs, and improve margins, addressing investor concerns that emerged following the disappointing Q4 2024 results. The company’s focus on working capital efficiency appears to be yielding results, with improvements in inventory management compared to previous quarters.

Forward-Looking Statements

Wajax management indicated that they continue to see strong customer demand in the mining and energy sectors, which has been a consistent bright spot for the company. However, they acknowledged that headwinds are expected to persist, with broader market conditions remaining soft and continued uncertainty surrounding tariffs and counter-tariffs on Canada-U.S. trade.

This cautious outlook aligns with CEO Igi Domagalski’s "playing it safe" approach mentioned in the Q4 2024 earnings call, suggesting that management remains concerned about potential market volatility despite the improved revenue performance in Q1 2025.

The company’s leverage ratio, which was reported at 2.61x in Q4 2024 (above the target range of 1.5-2.0x), remains an area of focus for management. The Q1 2025 results show progress on inventory reduction, which should help improve the leverage position if sustained throughout 2025.

Overall, Wajax’s Q1 2025 results demonstrate revenue growth momentum across all regions despite continued margin challenges. The company’s strategic focus on inventory management and cost control appears to be showing initial positive results, though management remains cautious about broader market conditions and trade uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.