EU and US could reach trade deal this weekend - Reuters

Introduction & Market Context

Eyewear retailer Warby Parker (NYSE:WRBY) presented its first quarter 2025 financial results on May 8, showing continued revenue growth and improved profitability as the company expands its retail footprint across North America.

The direct-to-consumer eyewear company, which pioneered the vertically integrated model in the optical industry, reported that its sales represent approximately 1% of the $68 billion U.S. eyewear market, highlighting significant room for growth despite operating 287 stores across the United States and Canada.

The company’s stock has faced pressure in recent months, with shares currently trading at $16.16, down significantly from the pre-market price of $26.01 following its Q4 2024 earnings release.

Quarterly Performance Highlights

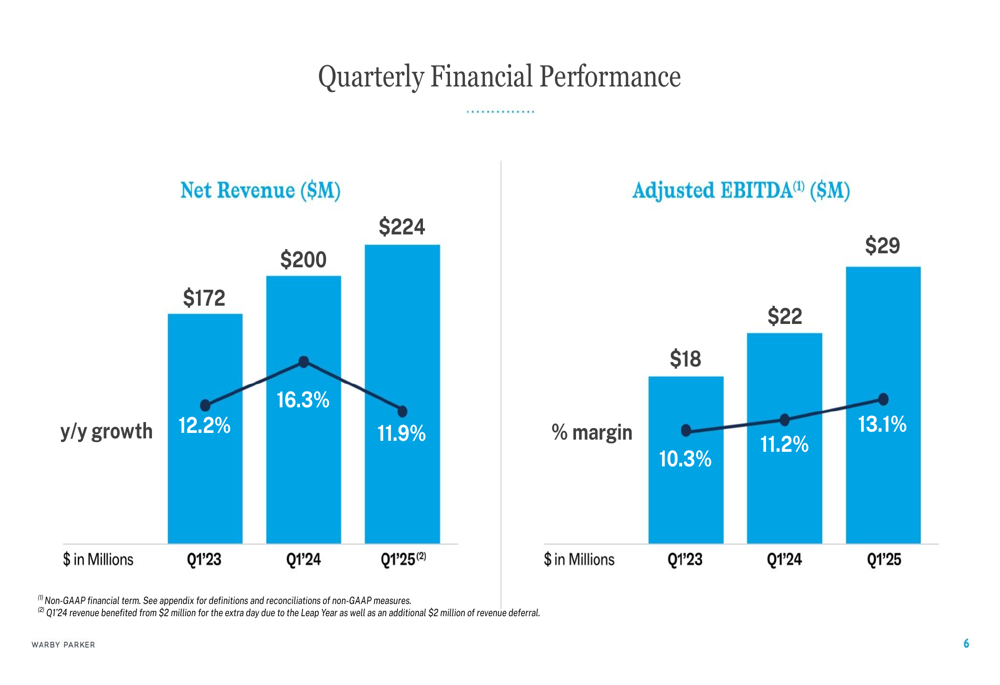

Warby Parker reported Q1 2025 net revenue of $224 million, representing an 11.9% increase year-over-year, continuing the company’s growth trajectory despite a slight deceleration from the 17.8% growth reported in Q4 2024.

The company achieved a notable improvement in profitability, posting adjusted EBITDA of $29.2 million with a 13.1% margin, up from $22.4 million and an 11.2% margin in the same period last year. Warby Parker also reported positive net income of $3.47 million for the quarter, a significant improvement from the $2.68 million loss in Q1 2024.

As shown in the following chart of quarterly financial performance:

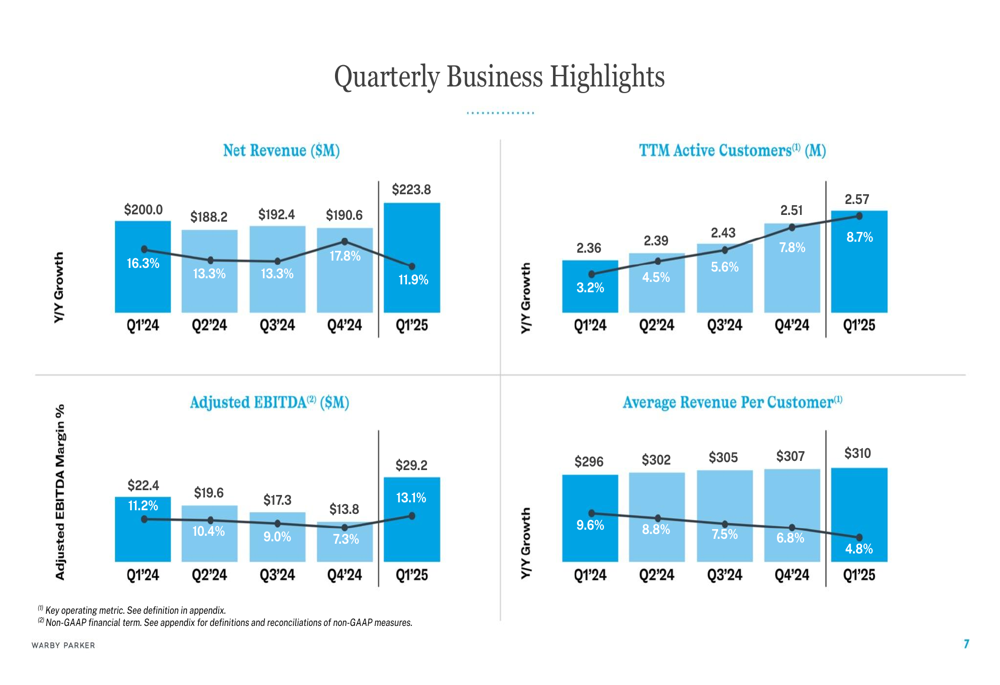

Active customers grew to 2.57 million, an 8.7% increase year-over-year, while average revenue per customer reached $310, up from $296 in Q1 2024. This demonstrates the company’s ability to both attract new customers and increase spending from existing ones.

The following quarterly business metrics illustrate the company’s consistent growth across key performance indicators:

Warby Parker’s customer retention remains strong, with cohorts from 2015-2024 showing retention rates exceeding 100% at the 48-month mark, indicating that customers who stay with the brand tend to increase their spending over time.

Retail Expansion Strategy

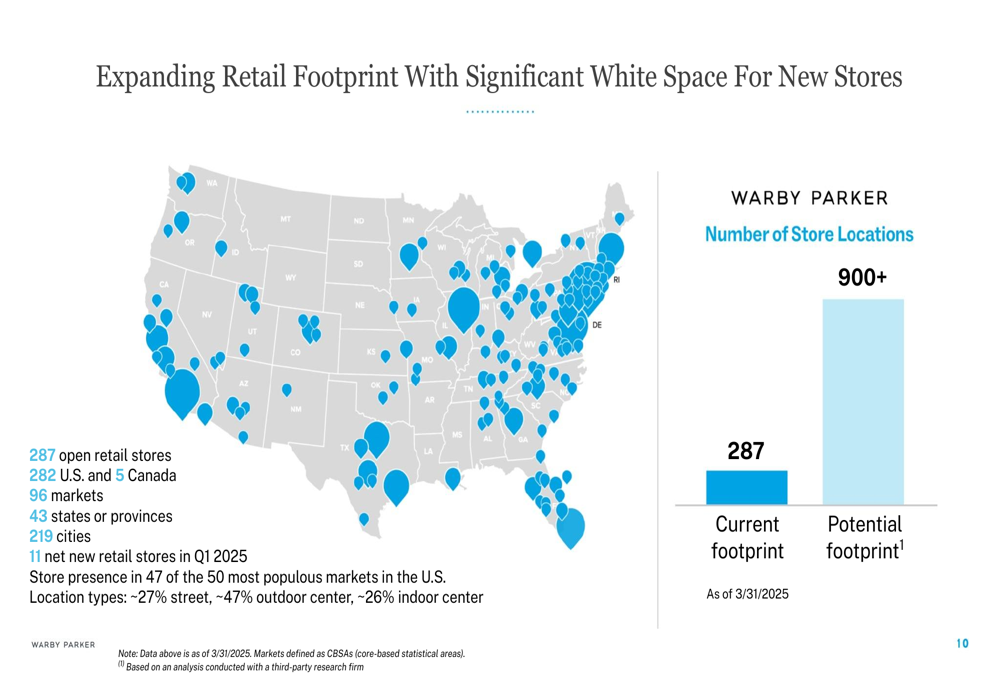

A key element of Warby Parker’s growth strategy is its ongoing retail expansion. The company opened 11 net new retail stores in Q1 2025, bringing its total to 287 locations (282 in the U.S. and 5 in Canada) across 96 markets, 43 states or provinces, and 219 cities.

The company’s presentation highlighted significant room for growth, with a potential footprint of over 900 locations, more than triple its current store count. Warby Parker currently has stores in 47 of the 50 most populous markets in the U.S., with a balanced mix of location types: approximately 27% street locations, 47% outdoor centers, and 26% indoor centers.

The following map illustrates Warby Parker’s current retail footprint and expansion potential:

This expansion strategy appears to be working effectively, as evidenced by the company’s continued revenue growth and improving profitability metrics. The physical store network complements Warby Parker’s digital presence, supporting its omnichannel approach to the eyewear market.

Financial Outlook

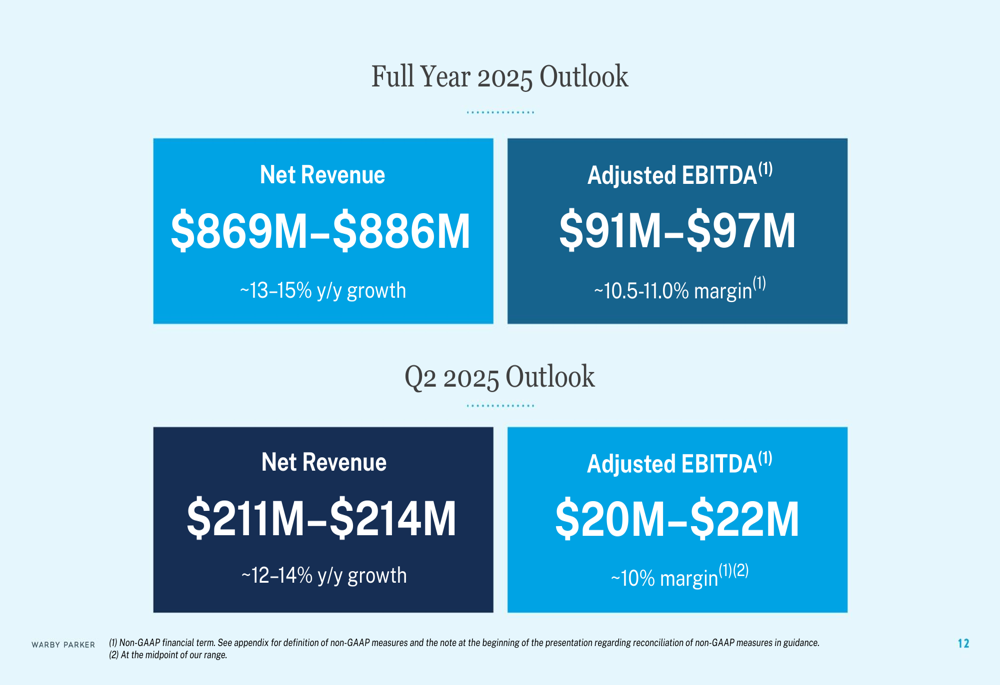

Looking ahead, Warby Parker provided guidance for both Q2 2025 and the full year. For Q2, the company expects net revenue between $211 million and $214 million, representing 12-14% year-over-year growth, with adjusted EBITDA of $20-22 million (approximately 10% margin).

For the full year 2025, Warby Parker projects net revenue of $869-886 million, reflecting 13-15% annual growth, and adjusted EBITDA of $91-97 million with a 10.5-11.0% margin.

The following slide details the company’s financial outlook:

This guidance suggests management expects continued steady growth through 2025, with modest margin improvement compared to previous quarters. The full-year revenue guidance represents a slight adjustment from the 14-16% growth projection mentioned in the company’s Q4 2024 earnings report.

Market Reaction & Analyst Perspectives

Despite Warby Parker’s positive Q1 results and improved profitability, the company’s stock has faced significant pressure in recent months. After trading as high as $26.01 in pre-market following Q4 2024 results, the stock has declined to $16.16, well below its 52-week high of $28.68.

This disconnect between improving fundamentals and stock performance may reflect broader market concerns about the retail sector, potential growth deceleration (Q1’s 11.9% revenue growth was lower than Q4’s 17.8%), or valuation concerns following the stock’s previous run-up.

The company’s Q1 financial highlights demonstrate solid execution across key metrics:

Warby Parker’s long-term growth narrative remains intact, with the company continuing to execute its retail expansion strategy while maintaining strong customer retention and increasing average revenue per customer. However, investors appear to be taking a more cautious approach to valuing the company’s growth prospects in the current market environment.

As Warby Parker continues to expand its retail footprint and enhance its technological capabilities, including its Virtual Vision Test and Virtual Try-On features, the company remains positioned to capitalize on its small but growing share of the substantial U.S. eyewear market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.