Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Waters Corporation (NYSE:WAT) reported solid first-quarter 2025 results during its earnings presentation on May 6, 2025, highlighting 7% constant currency revenue growth fueled by particularly strong instrument sales. The analytical instrument maker continues to benefit from growth in pharmaceutical testing, environmental monitoring, and expansion in Asian markets.

Quarterly Performance Highlights

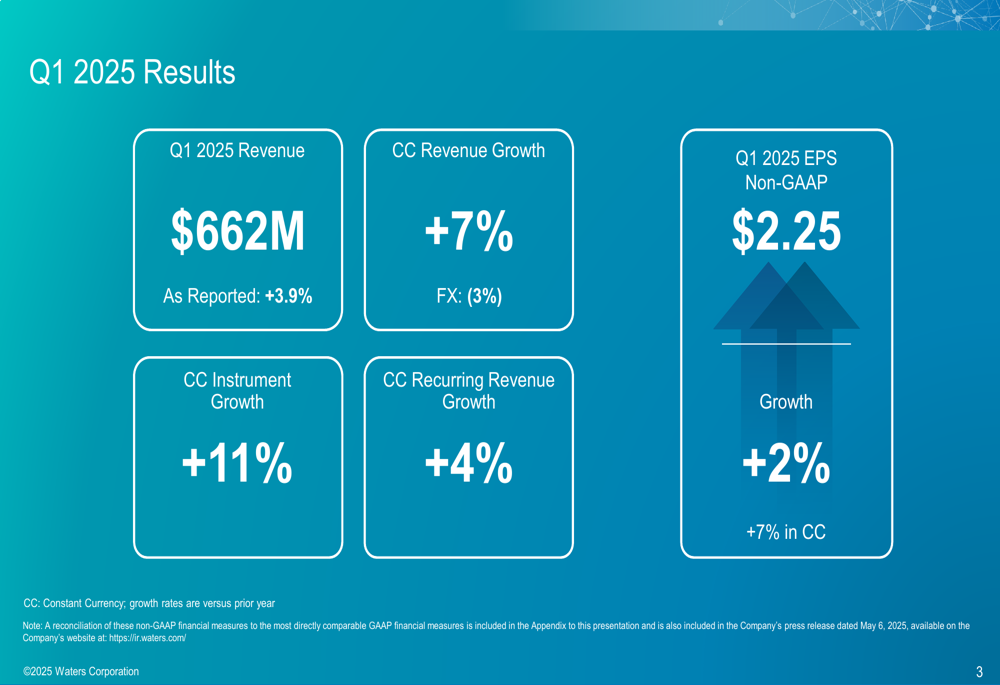

Waters reported Q1 2025 revenue of $662 million, representing 3.9% growth as reported and 7% growth in constant currency. Non-GAAP earnings per share reached $2.25, up 2% as reported and 7% in constant currency. The company’s performance was notably driven by robust instrument sales, which grew 11% in constant currency.

As shown in the following financial results summary:

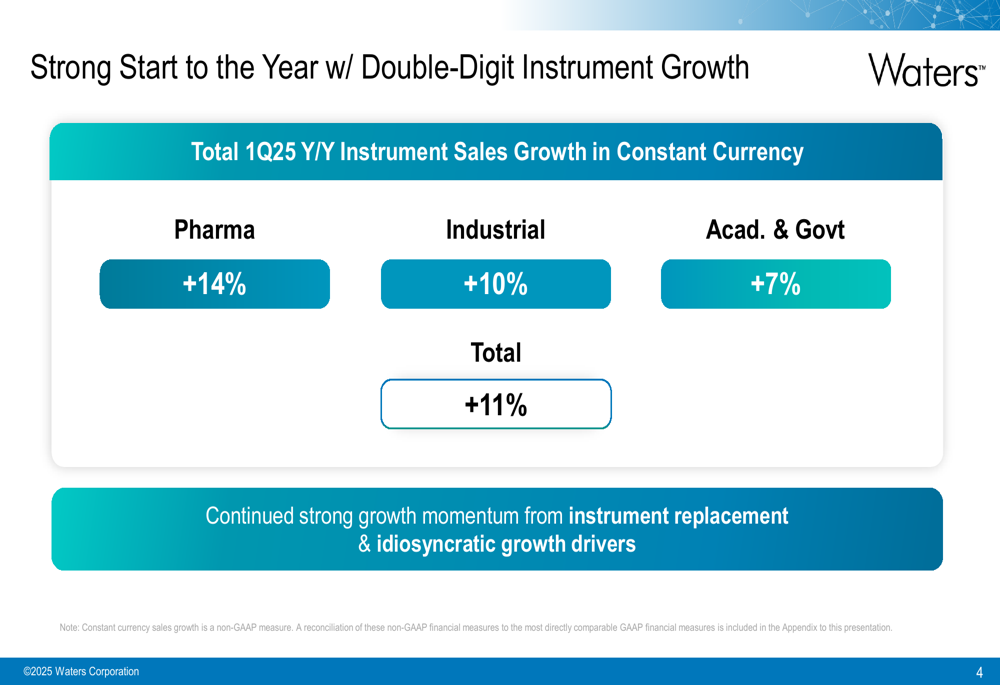

Breaking down the company’s instrument sales by market segment, Waters achieved double-digit growth in its pharmaceutical and industrial segments, with academic and government sales also showing solid performance.

As illustrated in the instrument growth breakdown:

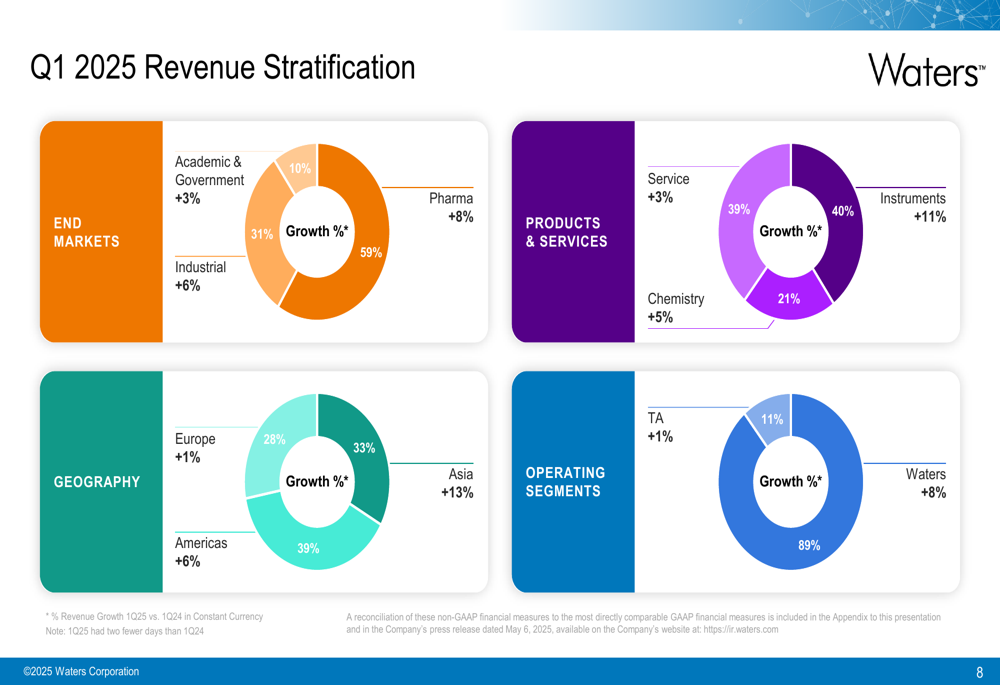

The company’s revenue stratification reveals varied performance across regions, with Asia leading growth at 13%, followed by the Americas at 6%, while Europe showed more modest growth of 1%. By end market, pharmaceutical remained the strongest segment with 8% growth, followed by industrial at 6% and academic/government at 3%.

Waters’ stock closed at $348.38 on May 5, down 0.59% from the previous session, though premarket trading on May 6 showed a slight increase of 0.62%. The stock has been trading in a 52-week range of $279.24 to $423.56, according to available market data.

Strategic Initiatives

Waters highlighted three key messages underpinning its performance: a strong start to the year, momentum tied to resilient growth drivers, and demonstrated operational excellence.

The company’s strategic messaging is summarized in this slide:

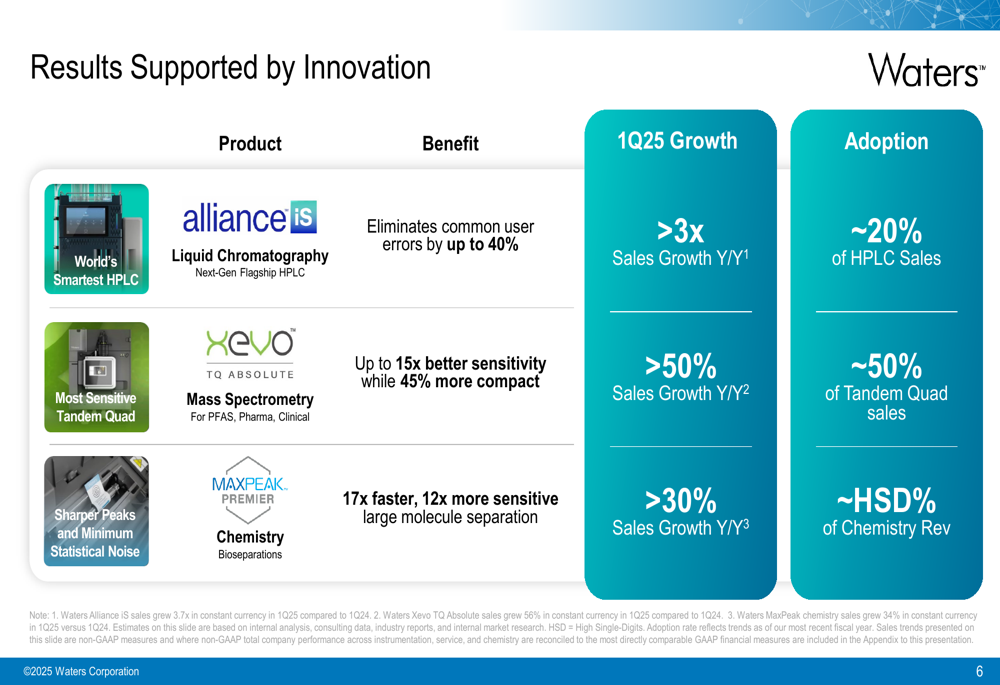

Innovation remains a central focus for Waters, with several new products driving significant sales growth. The company highlighted three key product lines delivering strong year-over-year performance: the Alliance iS Liquid Chromatography system, the Xevo TQ Absolute Mass Spectrometry platform, and MAXPeak Premier Chemistry.

These innovation-driven results are detailed in the following slide:

Waters also identified several idiosyncratic growth drivers that differentiate its market position, including the expanding GLP-1 therapeutics market, PFAS environmental testing, and growth in the Indian pharmaceutical market driven by the patent cliff and aging global populations.

The company’s unique growth drivers are illustrated here:

Forward-Looking Statements

Looking ahead, Waters provided guidance for both Q2 2025 and the full fiscal year. For Q2, the company expects constant currency revenue growth of 5.0% to 7.0% compared to Q2 2024, with non-GAAP EPS projected between $2.88 and $2.98.

For the full year 2025, Waters maintained its constant currency revenue growth guidance of 5.0% to 7.0%, with non-GAAP EPS expected to range from $12.75 to $13.05. This represents approximately 11% constant currency EPS growth for the year.

The detailed guidance is presented in this forward-looking slide:

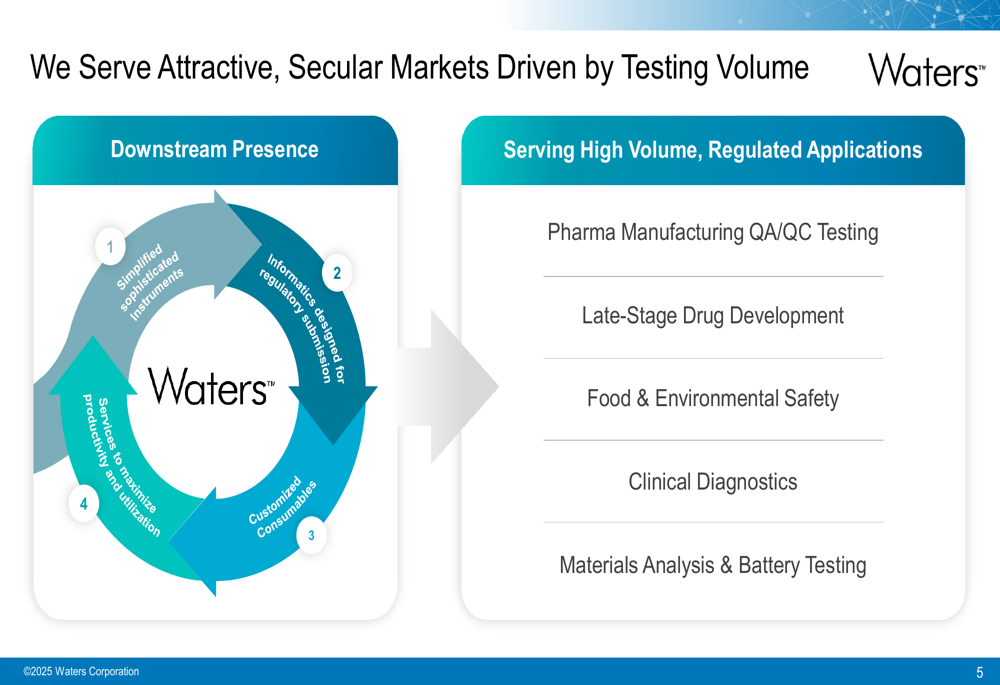

Competitive Industry Position

Waters continues to position itself in attractive, regulated markets with high-volume applications. The company emphasized its downstream presence across instruments, informatics, consumables, and services, serving critical applications in pharmaceutical manufacturing, food and environmental safety, clinical diagnostics, and materials analysis.

This market positioning is visualized in the following slide:

The company’s focus on high-growth areas like GLP-1 therapeutics testing, which is expected to contribute approximately 30 basis points per year to growth through 2030, and PFAS environmental testing, a $400 million global market growing at approximately 20%, demonstrates Waters’ strategy to capitalize on emerging opportunities in regulated testing markets.

Waters’ Q1 2025 results suggest the company is executing well on its strategy of focusing on high-value, regulated markets while driving innovation across its product portfolio. The strong instrument growth indicates potential customer confidence in capital investments, while the company’s guidance reflects management’s optimism about continued momentum through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.