Gold prices edge higher with focus on Ukraine-Russia, Jackson Hole

Introduction & Market Context

Weatherford International PLC (NASDAQ:WFRD) released its Q2 2025 investor presentation on July 23, 2025, showcasing strong year-over-year growth despite challenging market conditions. The oilfield services company, which operates in 75 countries with approximately 17,300 employees, reported significant improvements in key financial metrics while continuing to return value to shareholders.

The company’s stock has responded positively to these results, with shares rising 4.27% to $55.73 according to the latest market data, building on momentum from Q1 when the stock rose 1.25% following earnings that exceeded analyst expectations.

Quarterly Performance Highlights

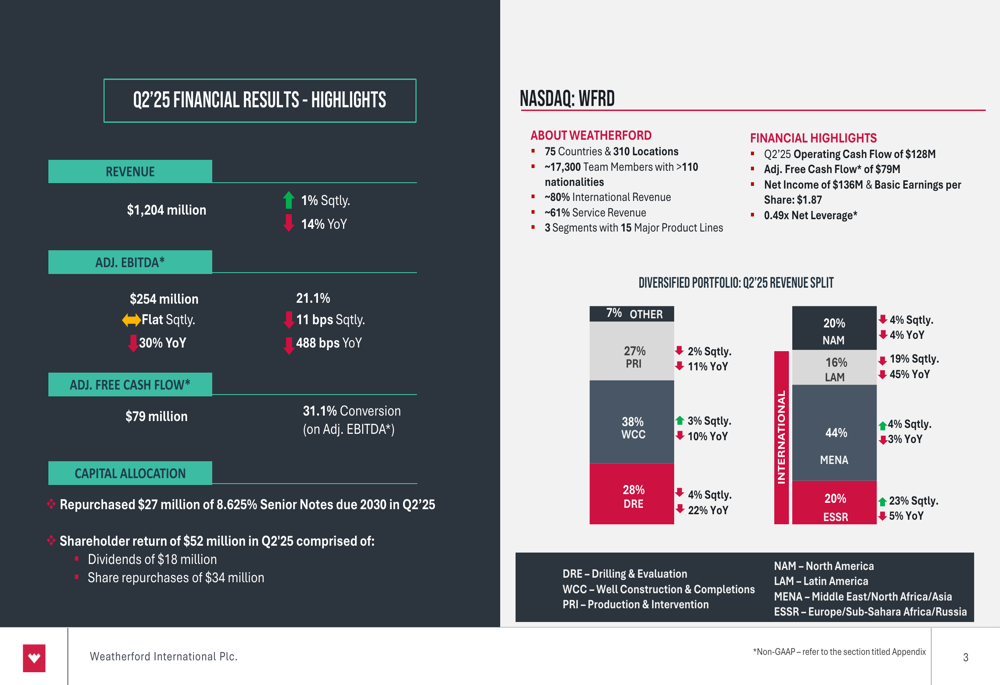

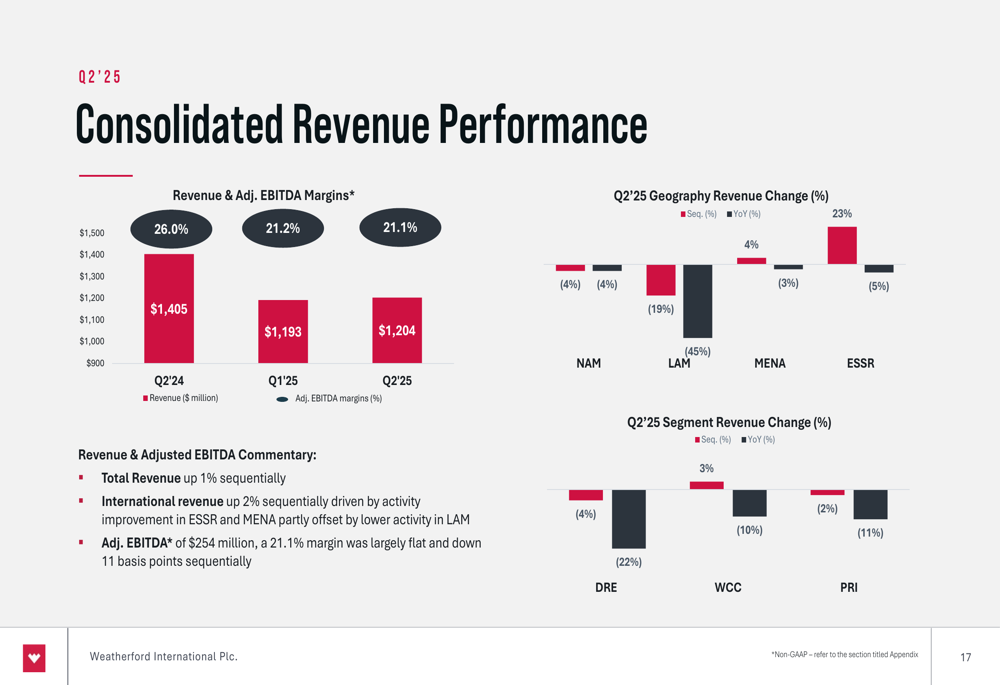

Weatherford reported Q2 2025 revenue of $1,204 million, representing a 1% sequential increase and a robust 14% year-over-year growth. Adjusted EBITDA reached $254 million, flat sequentially but up 30% compared to Q2 2024, with margins expanding to 21.1% - an improvement of 488 basis points year-over-year.

The company’s global footprint continues to be a key strength, with approximately 80% of revenue generated internationally. The Middle East and North Africa (MENA) region remains Weatherford’s largest market, accounting for 44% of Q2 revenue.

As shown in the following financial highlights:

Detailed Financial Analysis

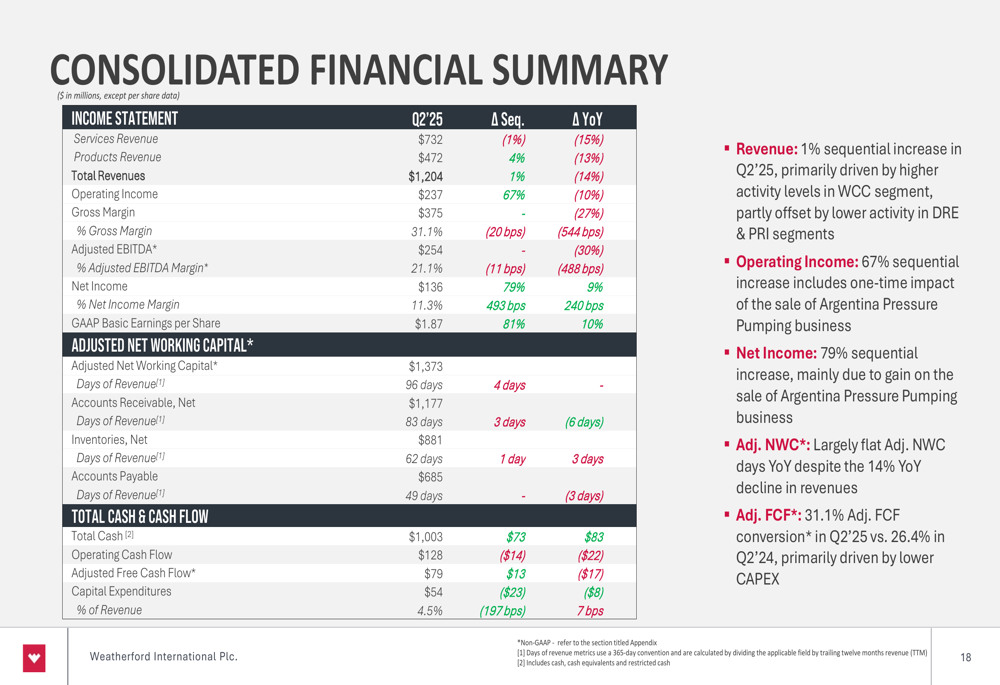

Weatherford’s financial performance demonstrates continued strength across multiple metrics. Net income for Q2 2025 reached $136 million, translating to basic earnings per share of $1.87. The company generated $128 million in operating cash flow and $79 million in adjusted free cash flow, with a conversion rate of 31.1% on adjusted EBITDA.

The company’s balance sheet remains robust with total liquidity of $1.3 billion - the highest level since emergence - including approximately $1 billion in cash and restricted cash. Weatherford has reduced its gross debt by over $1 billion since Q4 2021, achieving a net leverage ratio of 0.49x (calculated as Net Debt/TTM Adj. EBITDA).

The consolidated financial summary provides a comprehensive view of Weatherford’s performance:

Strategic Initiatives & Capital Allocation

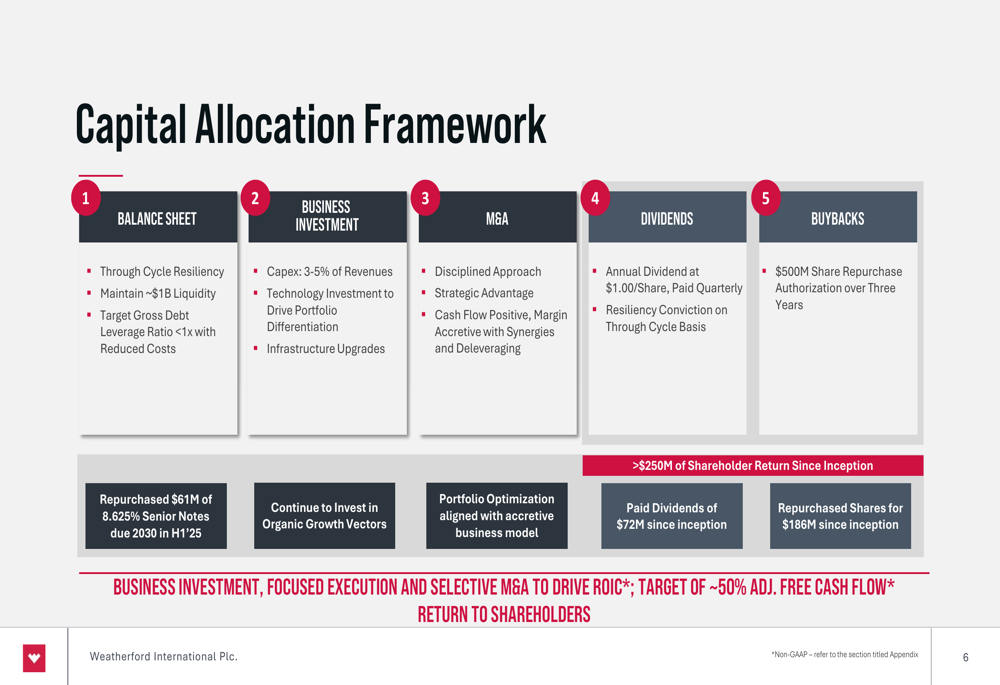

Weatherford continues to execute on its capital allocation framework, balancing investments in the business with shareholder returns. In Q2 2025, the company returned $52 million to shareholders, comprising $18 million in dividends and $34 million in share repurchases. Additionally, Weatherford repurchased $27 million of its 8.625% Senior Notes due 2030.

The company maintains its annual dividend of $1.00 per share, paid quarterly, and has a $500 million share repurchase authorization over three years. Since inception of its capital return program, Weatherford has returned over $250 million to shareholders, including $72 million in dividends and $186 million in share repurchases.

The capital allocation framework illustrates Weatherford’s balanced approach:

Weatherford’s strategic priorities focus on five key areas: Financial Performance, Customer Experience, Organizational Vitality, LEAN Operations, and Creating The Future. These priorities support the company’s overarching goal of sustainable profitability and positive free cash flow.

Segment Performance

Weatherford operates through three main segments, each showing varying performance in Q2 2025:

1. Well Construction & Completions (WCC): Revenue increased by 3% sequentially, primarily driven by higher Liner Hangers and Cementation Products activity, partially offset by lower Completions activity, especially in Latin America.

2. Drilling & Evaluation (DRE): Revenue decreased by 4% sequentially, primarily due to lower Wireline activity in North America and Latin America, partly offset by higher Drilling Services activity in Europe, Sub-Saharan Africa, Russia (ESSR) and Latin America.

3. Production & Intervention (PRI): Revenue decreased by 2% sequentially, primarily from lower Pressure Pumping activity in Latin America following the sale of the Argentina Pressure Pumping business, partly offset by higher Artificial Lift and Sub-sea Intervention activity.

The consolidated revenue performance across geographies and segments is illustrated below:

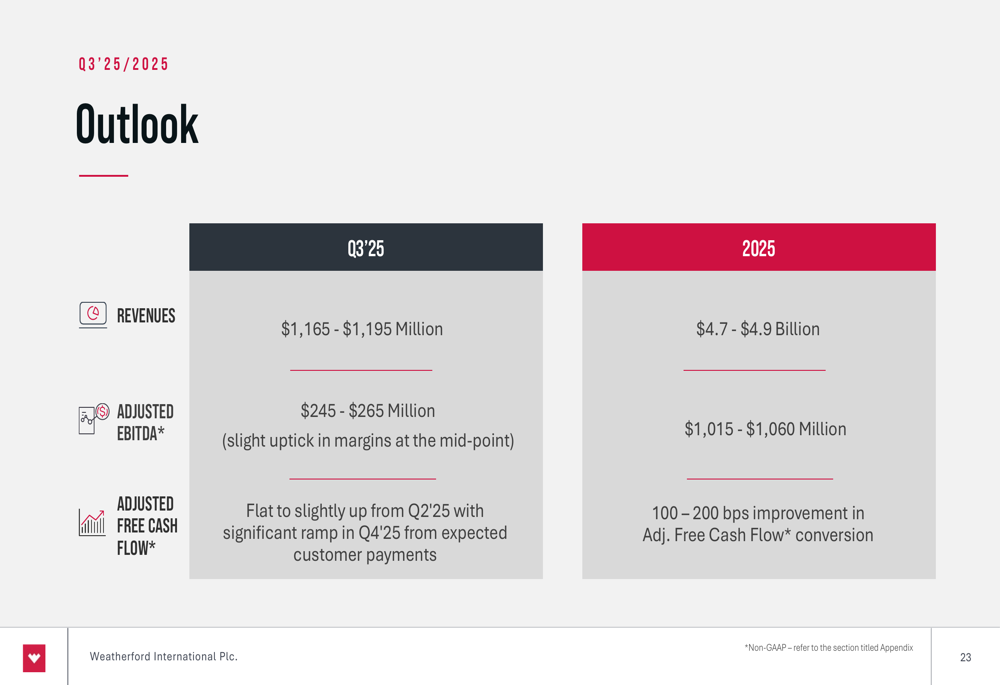

Outlook & Forward Guidance

Looking ahead, Weatherford provided specific guidance for both Q3 2025 and the full year. For Q3, the company expects revenues between $1,165-$1,195 million and adjusted EBITDA of $245-$265 million. For the full year 2025, Weatherford forecasts revenues of $4.7-$4.9 billion and adjusted EBITDA of $1,015-$1,060 million.

This outlook reflects Weatherford’s confidence in its business model despite anticipated challenges in certain markets, as highlighted in the company’s guidance:

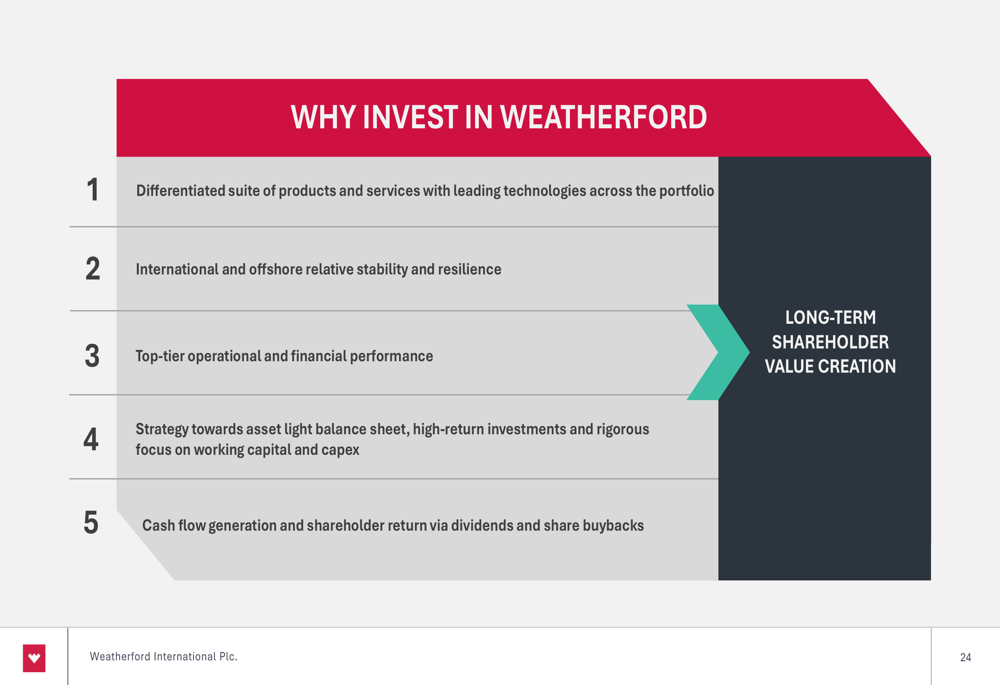

Investment Thesis

Weatherford presents a compelling investment case based on five key factors: a differentiated suite of products and services with leading technologies, international and offshore stability, top-tier operational and financial performance, an asset-light balance sheet strategy, and strong cash flow generation supporting shareholder returns.

The company’s investment thesis is summarized in the following slide:

This investment proposition aligns with Weatherford’s Q1 2025 performance, where the company exceeded EPS expectations by 12% despite challenging market conditions. CEO Girish Saligram had emphasized during the Q1 earnings call that "margins must be defended" and that "the dividend is sacrosanct and will be maintained" - commitments that appear to be upheld in the Q2 results.

With its strong international presence, improving financial metrics, and commitment to shareholder returns, Weatherford continues to position itself as a resilient player in the oilfield services sector despite industry headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.