Oracle stock falls after report reveals thin margins in AI cloud business

Weave Communications Inc (NYSE:WEAV) presented its Q2 2025 results on July 31, showcasing continued revenue growth and strategic expansion into AI-powered healthcare solutions. The company’s stock closed at $7.52, down 2.99% for the day, with a slight recovery in after-hours trading.

Quarterly Performance Highlights

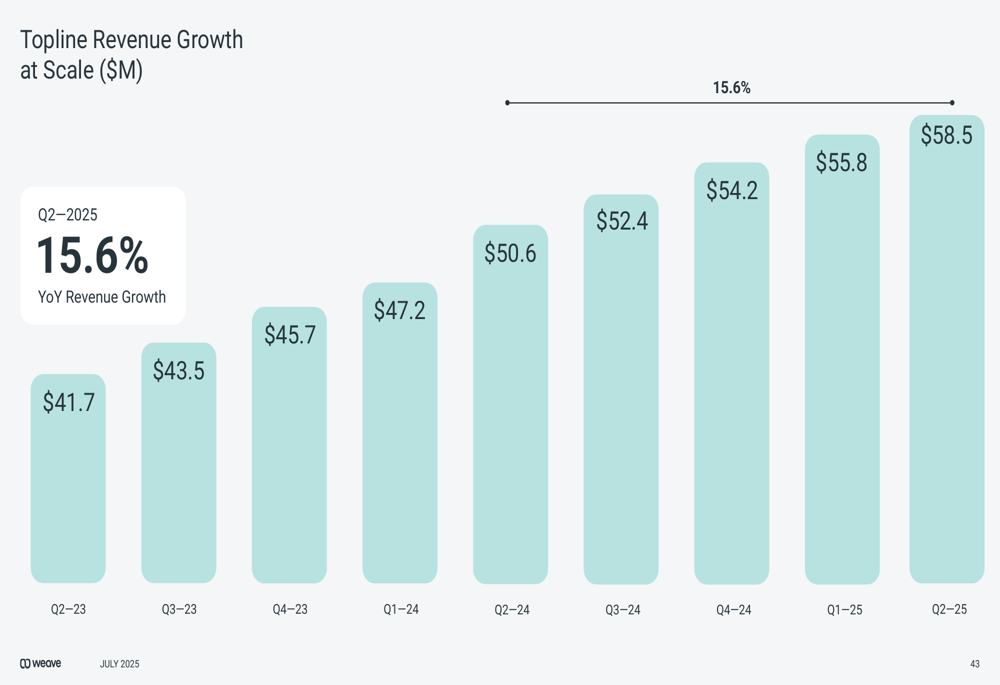

Weave reported Q2 2025 total revenue of $58.5 million, representing 16% year-over-year growth. The company’s trailing twelve-month (TTM) revenue reached $221 million, growing 18% compared to the previous year. Subscription and payment processing revenue, which forms the core of Weave’s business model, grew 19% year-over-year to $217 million on a TTM basis.

As shown in the following financial highlights, the company maintained strong customer retention metrics while improving margins:

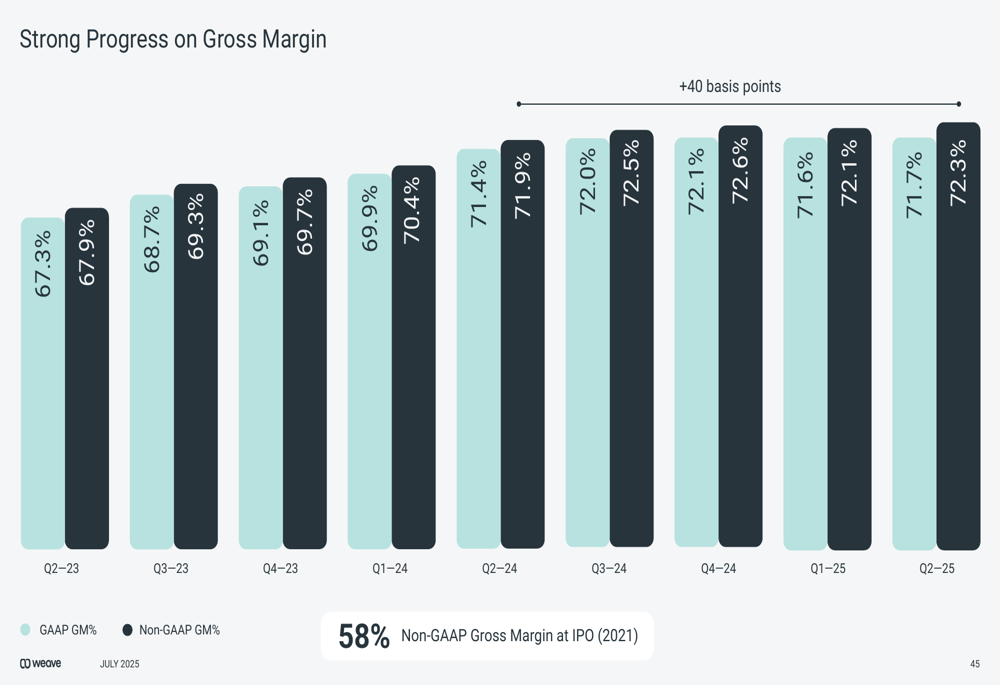

The company’s gross revenue retention rate stood at 90% for Q2 2025, while net revenue retention reached 96%, indicating successful upselling to existing customers. Non-GAAP gross margin improved to 72.3%, a 40 basis point increase compared to the same period last year.

Weave’s customer base expanded to over 35,000 locations, primarily across dental, optometry, veterinary, and specialty medical practices. The company’s platform facilitates millions of patient interactions monthly through its integrated communications and payments system.

Strategic Initiatives

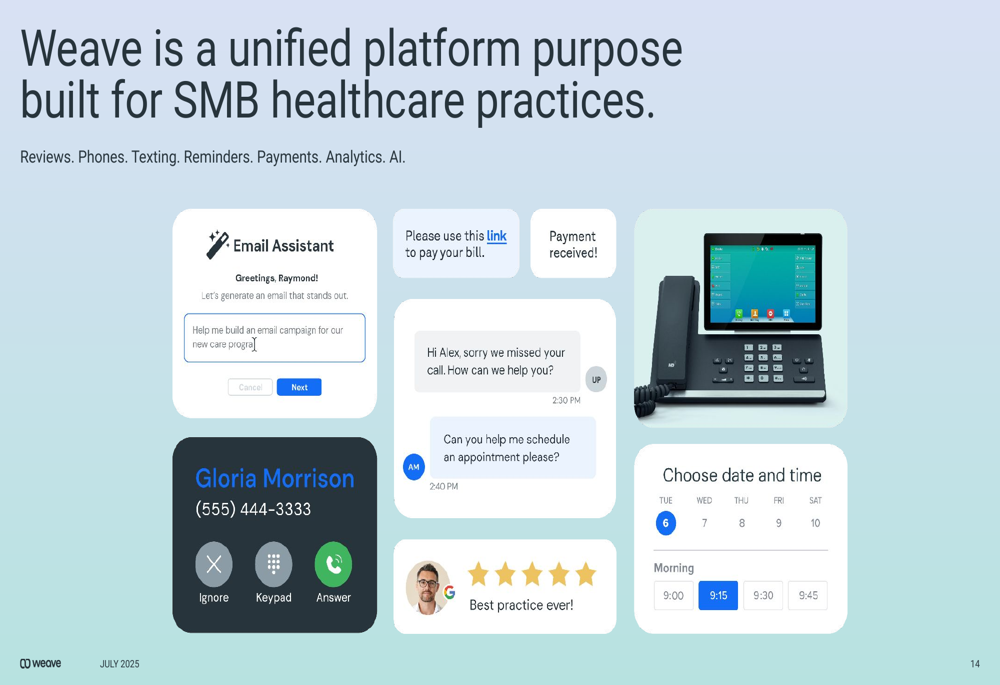

Weave’s presentation emphasized its unified platform approach, contrasting with the "patchwork of point solutions" that many healthcare practices currently use. The company positions itself as an all-in-one solution for customer communications, engagement, and payments specifically designed for small and medium-sized healthcare businesses.

The following slide illustrates how Weave’s platform integrates multiple functions into a cohesive solution:

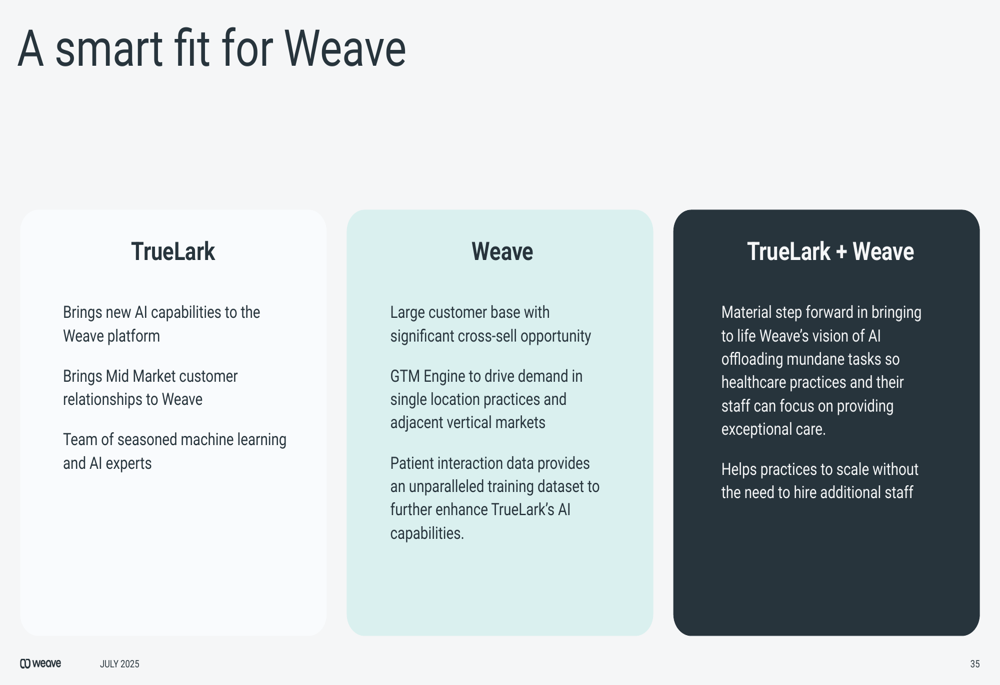

A significant strategic development highlighted in the presentation was Weave’s acquisition of TrueLark, an AI-powered virtual receptionist solution. This acquisition, valued at $35 million according to the company’s recent earnings report, enhances Weave’s AI capabilities and expands its service offerings.

The company presented TrueLark as a strategic fit that brings new AI capabilities, an experienced machine learning team, and an established customer base:

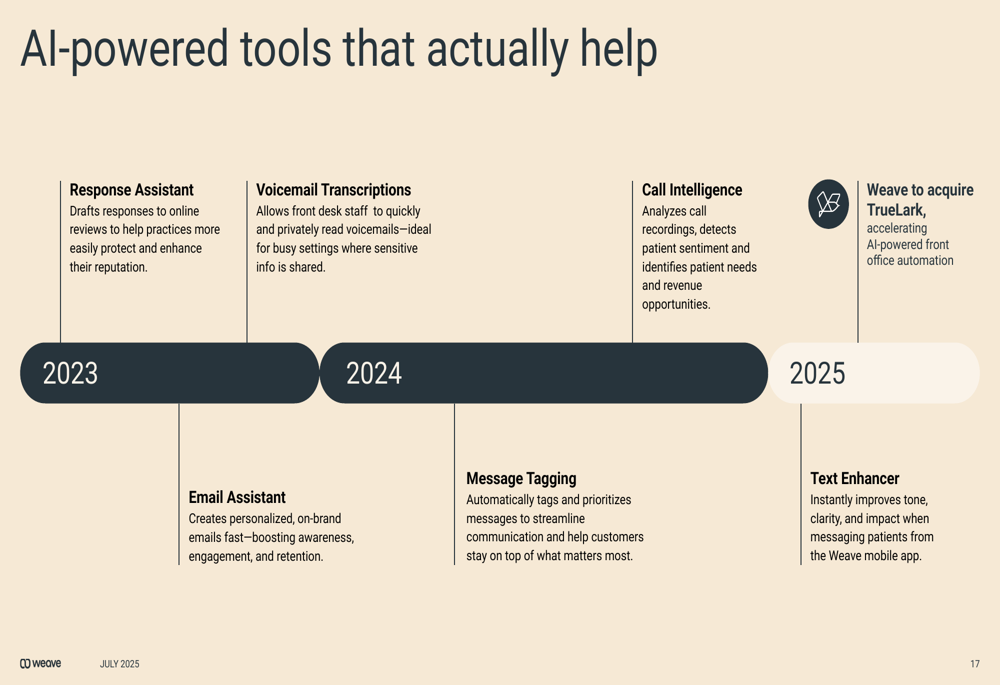

Weave emphasized its ongoing investment in AI-powered tools, presenting a timeline of AI feature releases from 2023 through 2025, including response assistants, voicemail transcriptions, call intelligence, and text enhancers:

Detailed Financial Analysis

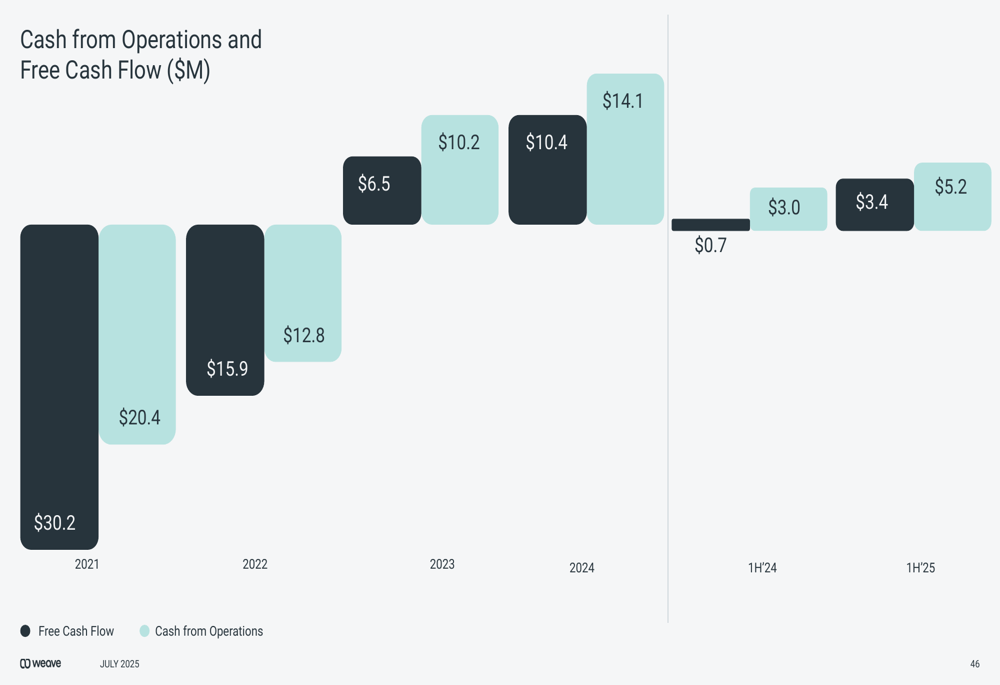

Weave’s presentation revealed continued progress toward profitability, with free cash flow reaching $13.1 million on a TTM basis, representing a $7.4 million improvement year-over-year. For the first half of 2025, free cash flow was $3.4 million, up $2.7 million from the same period last year.

The company’s revenue growth trajectory shows consistent quarter-over-quarter increases:

Gross margin has shown steady improvement since the company’s IPO in 2021, when non-GAAP gross margin stood at 58%. By Q2 2025, this figure had improved to 72.3%:

Operating margins have also shown improvement, though GAAP operating margin remains slim at just 0.1% for Q2 2025. The company’s non-GAAP operating margin was 17.4% for the same period, indicating significant non-cash or one-time expenses affecting GAAP results.

Cash flow trends demonstrate Weave’s progress toward sustainable profitability:

Market Opportunity (SO:FTCE11B) and Expansion

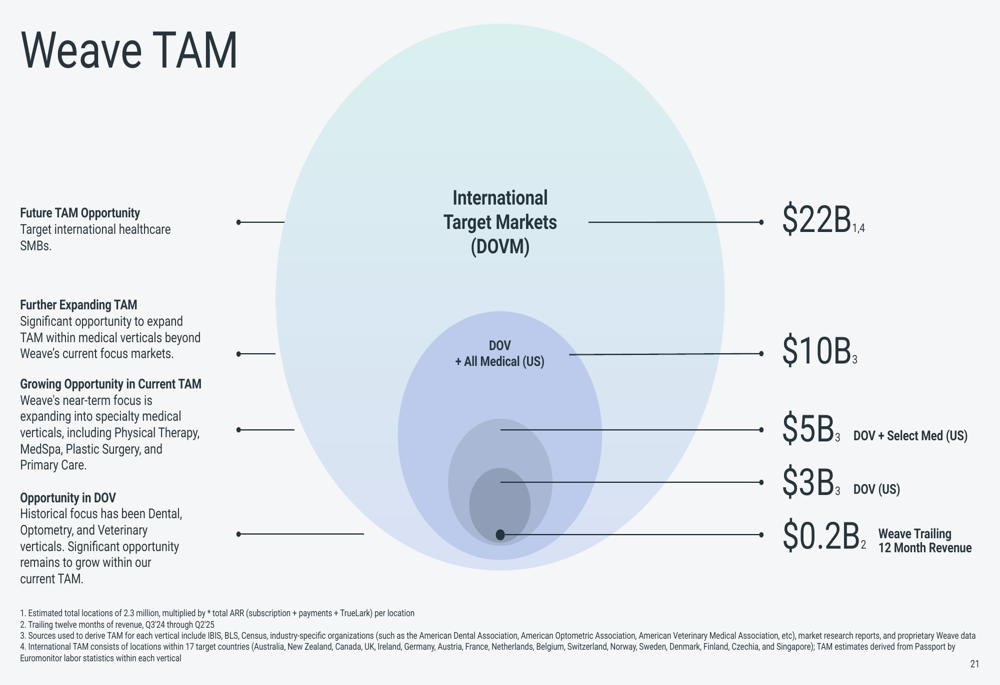

Weave presented an analysis of its total addressable market (TAM), showing significant room for growth beyond its current revenue base of approximately $221 million annually:

The company’s core market of dental, optometry, and veterinary practices in the US represents a $3 billion opportunity. By expanding into select medical verticals, this grows to $5 billion, and further to $10 billion when including all US medical verticals. International expansion could potentially increase the TAM to $22 billion.

Weave highlighted its strong position in the competitive landscape, noting its leadership in the G2 Grid for Patient Relationship Management, particularly in the healthcare sector.

Forward-Looking Statements

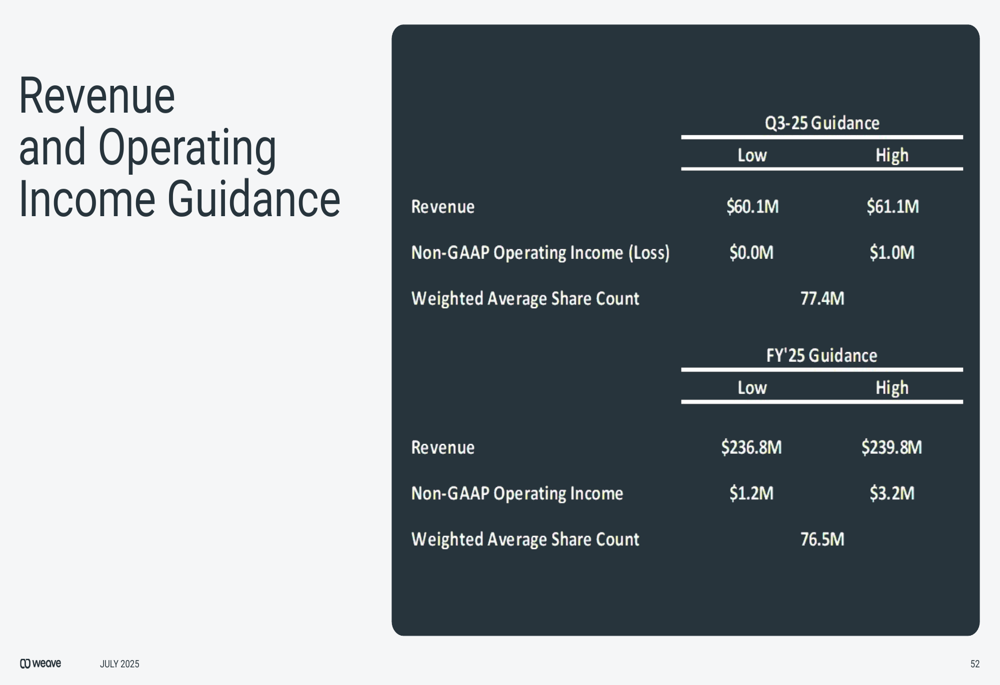

For Q3 2025, Weave provided revenue guidance of $60.1-$61.1 million and projected non-GAAP operating income between $0 and $1 million:

For the full fiscal year 2025, the company expects revenue between $236.8 million and $239.8 million, with non-GAAP operating income of $1.2-$3.2 million. This guidance aligns with the updated outlook provided in the company’s recent earnings report.

According to the earnings call, Weave expects the TrueLark acquisition to be accretive by 2026. CEO Brett White highlighted the strategic importance of this acquisition, stating, "TrueLark is a virtual receptionist that enables fully autonomous patient engagement."

While Weave continues to show revenue growth and margin improvement, investors should note that the company faces challenges including market saturation in certain verticals, economic pressures that could impact customer spending, integration risks with acquisitions like TrueLark, and a competitive healthcare technology landscape that requires continuous innovation to maintain advantage.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.