Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Introduction & Market Context

Webster Financial Corporation (NYSE:WBS) presented its second quarter 2025 earnings on July 17, 2025, revealing improved performance compared to the previous quarter. The company’s stock is trading up 0.8% in premarket activity at $58.91, following the release of results showing stronger earnings and continued growth in both loans and deposits.

The financial institution, which had missed earnings expectations in Q1 2025 with an EPS of $1.30 versus the forecasted $1.38, has rebounded in Q2 with diluted earnings per share of $1.52. This improvement comes as the company continues to navigate a complex interest rate environment while maintaining strong capital levels and improving asset quality metrics.

Quarterly Performance Highlights

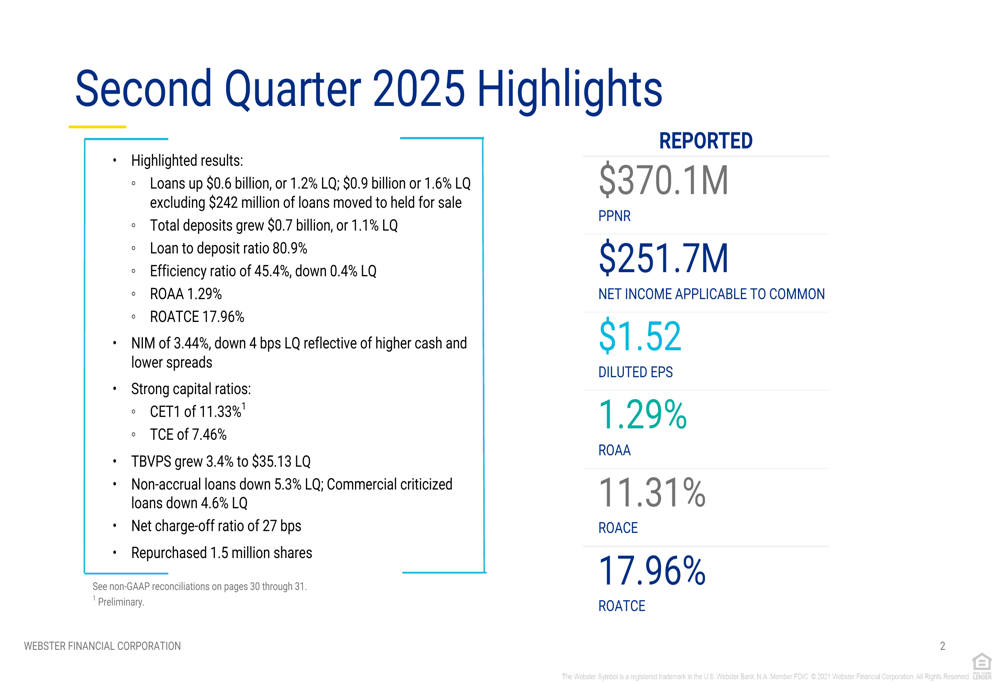

Webster Financial reported net income applicable to common shareholders of $251.7 million for Q2 2025, translating to diluted earnings per share of $1.52. The company achieved a return on average assets (ROAA) of 1.29% and an impressive return on average tangible common equity (ROATCE) of 17.96%.

As shown in the following comprehensive overview of the quarter’s performance:

Loan growth remained solid at $0.6 billion or 1.2% compared to the previous quarter, which would have been even stronger at $0.9 billion (1.6%) excluding $242 million in loans moved to held for sale. Total (EPA:TTEF) deposits grew by $0.7 billion (1.1%) quarter-over-quarter, maintaining a healthy loan-to-deposit ratio of 80.9%.

The company’s efficiency ratio improved to 45.4%, down 0.4% from the previous quarter, indicating enhanced operational efficiency. Asset quality metrics also showed improvement, with non-accrual loans down 5.3% and commercial criticized loans down 4.6% compared to Q1 2025. The net charge-off ratio stood at 27 basis points.

Detailed Financial Analysis

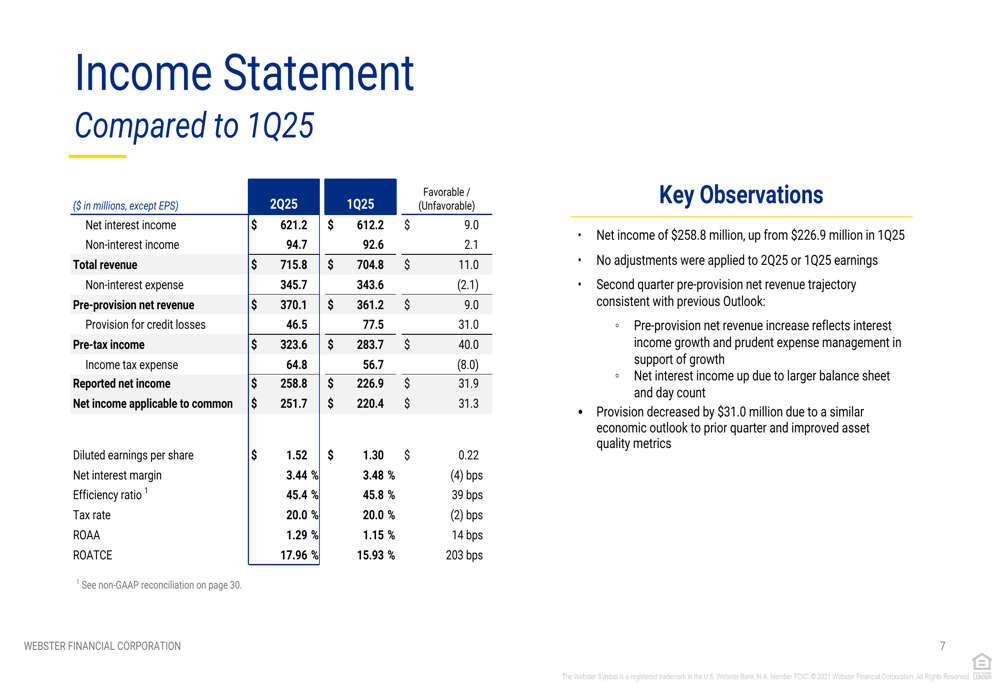

Webster Financial’s income statement revealed pre-provision net revenue of $370.1 million for Q2 2025. Net interest income totaled $621.2 million, though the net interest margin (NIM) decreased slightly by 4 basis points to 3.44% compared to the previous quarter, primarily due to higher cash balances and lower spreads.

The following income statement provides a detailed comparison to the previous quarter:

The company’s balance sheet remains strong, with total assets reaching $81.9 billion. The securities portfolio stood at $17.8 billion, while total loans were $53.7 billion, primarily composed of commercial loans ($42.7 billion) and consumer loans ($11.0 billion). Total deposits reached $66.3 billion, with transactional deposits accounting for $19.2 billion and healthcare financial services deposits totaling $10.2 billion.

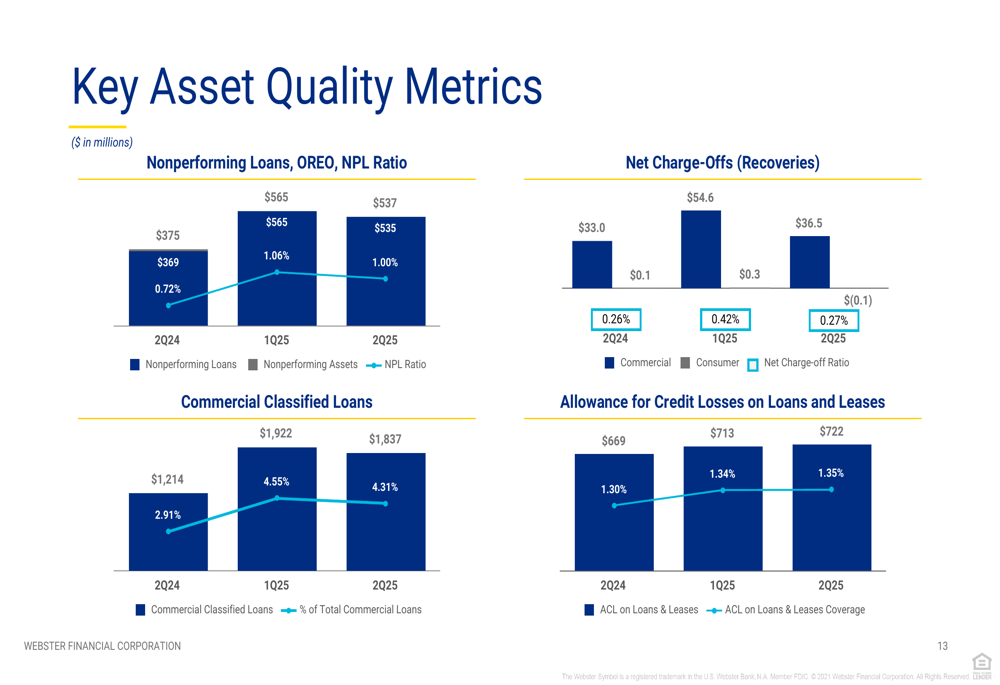

Asset quality continues to be a strength for Webster Financial, as evidenced by the following metrics:

The allowance for credit losses on loans and leases increased slightly to 1.35% of total loans, up from 1.34% in the previous quarter. This modest increase reflects the company’s prudent approach to risk management while maintaining appropriate coverage for potential credit losses.

Strategic Initiatives

Webster Financial continues to benefit from its diversified deposit base, which provides stability and low-cost funding. The company’s deposit profile spans multiple business lines, including Consumer Bank/brio direct (42% of total deposits), Commercial Bank (24%), HSA Bank (14%), interSYNC (13%), Corporate (5%), and Ametros (2%).

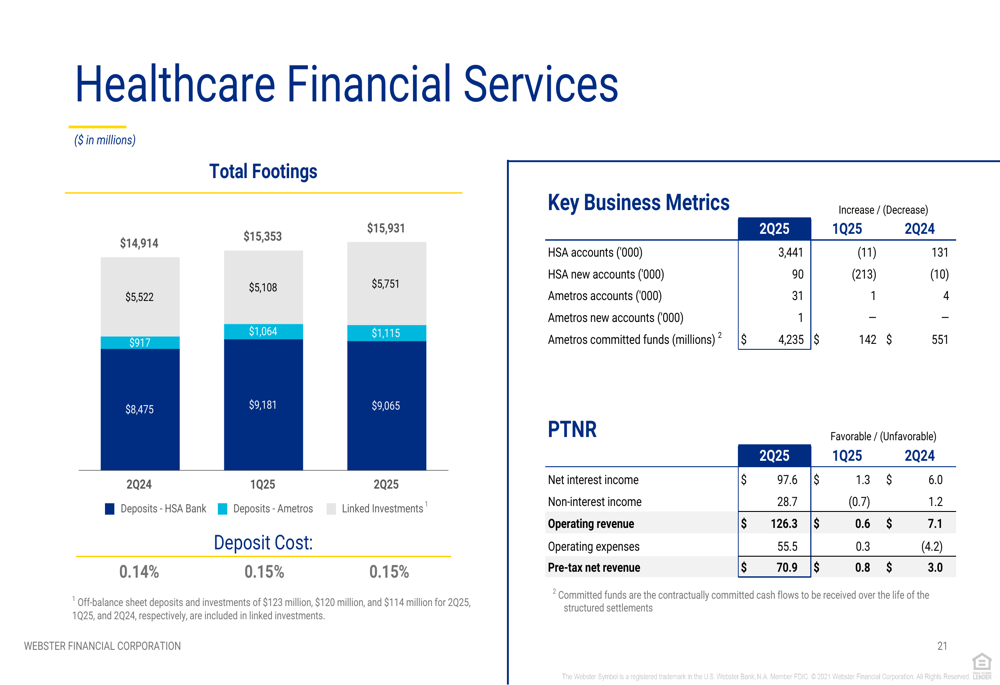

The company’s Healthcare Financial Services segment remains a particular strength, with the following performance metrics:

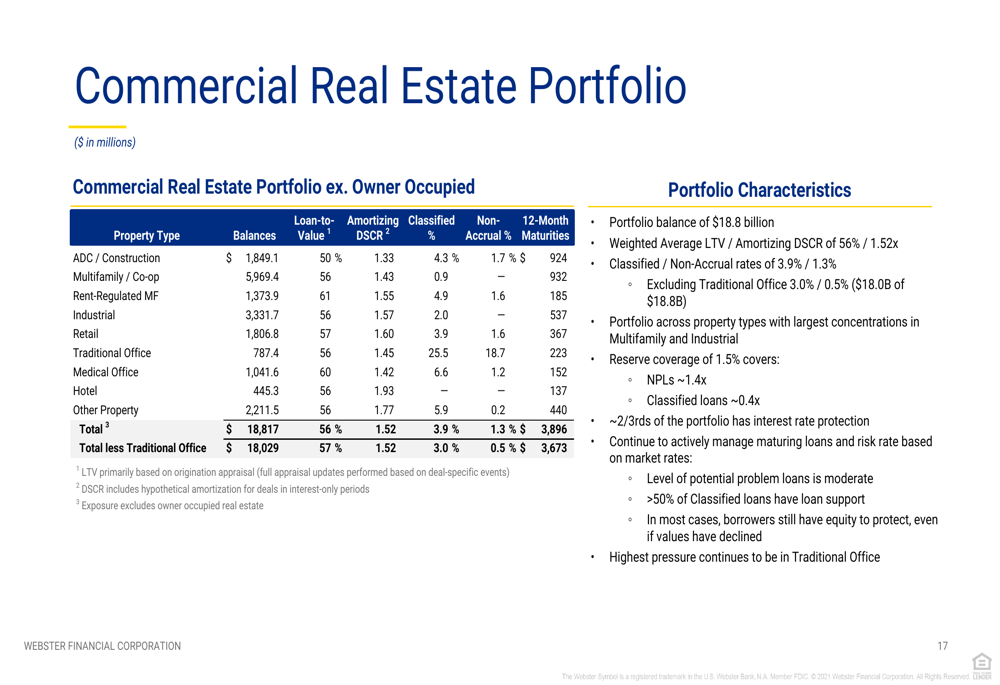

The company’s commercial real estate portfolio appears well-managed with a loan-to-value ratio of 56% and a debt service coverage ratio of 1.52. The portfolio is diversified across property types and geographic regions, with detailed metrics as follows:

Webster Financial has positioned its balance sheet to be resilient in both rising and falling interest rate environments. The company maintains a hedge portfolio of $5 billion, including interest rate collars of $2.75 billion and floating to fixed rate SOFR swaps of $2.25 billion, which provides benefits to net interest income in a declining rate environment.

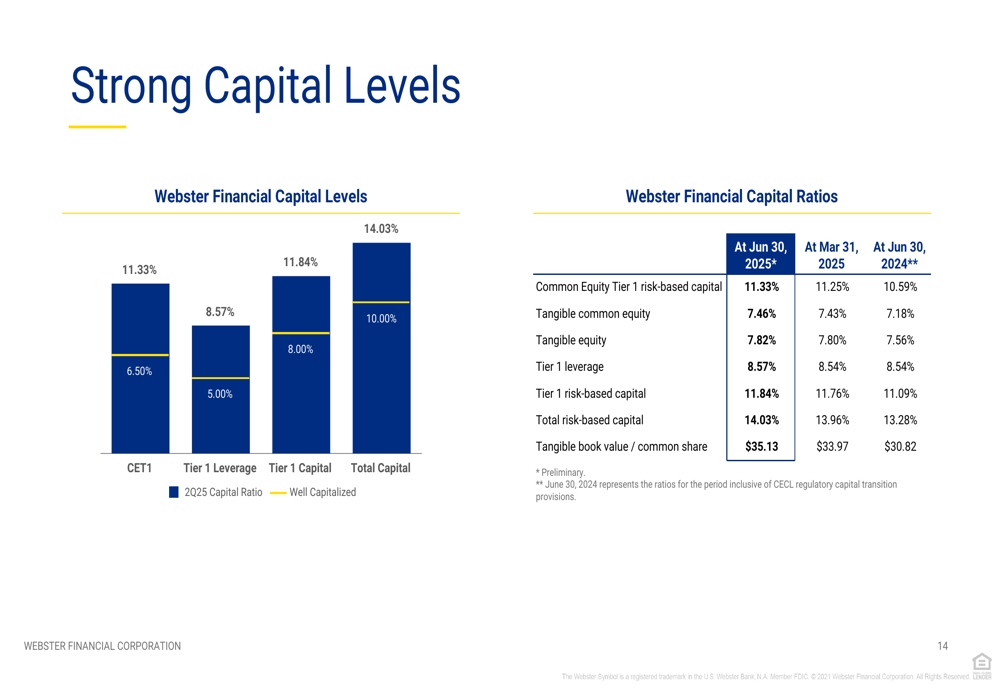

Capital Position

Webster Financial maintains strong capital levels, well above regulatory requirements. The Common Equity Tier 1 (CET1) ratio stood at 11.33% as of June 30, 2025, while the tangible common equity ratio was 7.46%. The company’s tangible book value per share grew by 3.4% quarter-over-quarter to $35.13.

The following chart illustrates the company’s robust capital position:

During the quarter, Webster Financial continued its capital return program, repurchasing 1.5 million shares. This demonstrates the company’s commitment to delivering shareholder value while maintaining strong capital levels.

Forward-Looking Statements

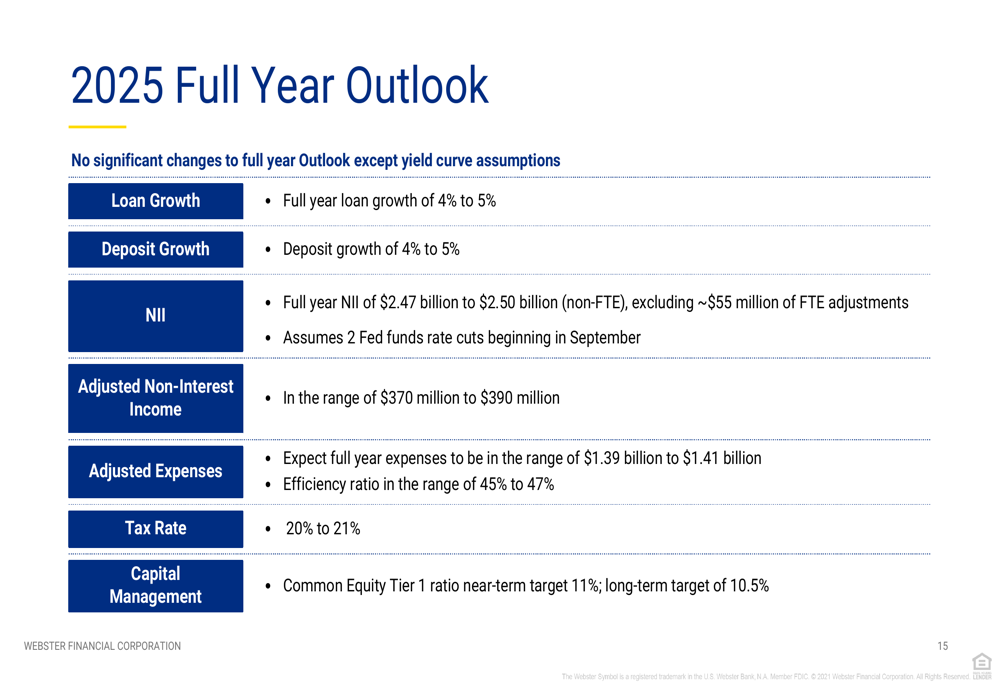

Looking ahead, Webster Financial provided a positive outlook for the full year 2025, projecting continued growth across key metrics. The company expects loan and deposit growth of 4-5% for the full year, with net interest income projected to be between $2.47 billion and $2.50 billion, assuming two Federal Reserve rate cuts during the year.

The detailed 2025 outlook is presented below:

The company anticipates adjusted non-interest income to be in the range of $370 million to $390 million for the full year. Management remains focused on maintaining a strong efficiency ratio while continuing to invest in strategic initiatives to drive long-term growth.

Conclusion

Webster Financial’s Q2 2025 results demonstrate a significant improvement from the previous quarter, with stronger earnings, continued loan and deposit growth, and enhanced asset quality metrics. The company’s diversified business model, strong capital position, and strategic positioning for various interest rate scenarios provide a solid foundation for continued performance.

While the slight compression in net interest margin bears watching, particularly in light of anticipated Federal Reserve rate cuts, the company’s overall financial health and forward guidance suggest Webster Financial is well-positioned to navigate the evolving economic landscape through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.