Oracle stock falls after report reveals thin margins in AI cloud business

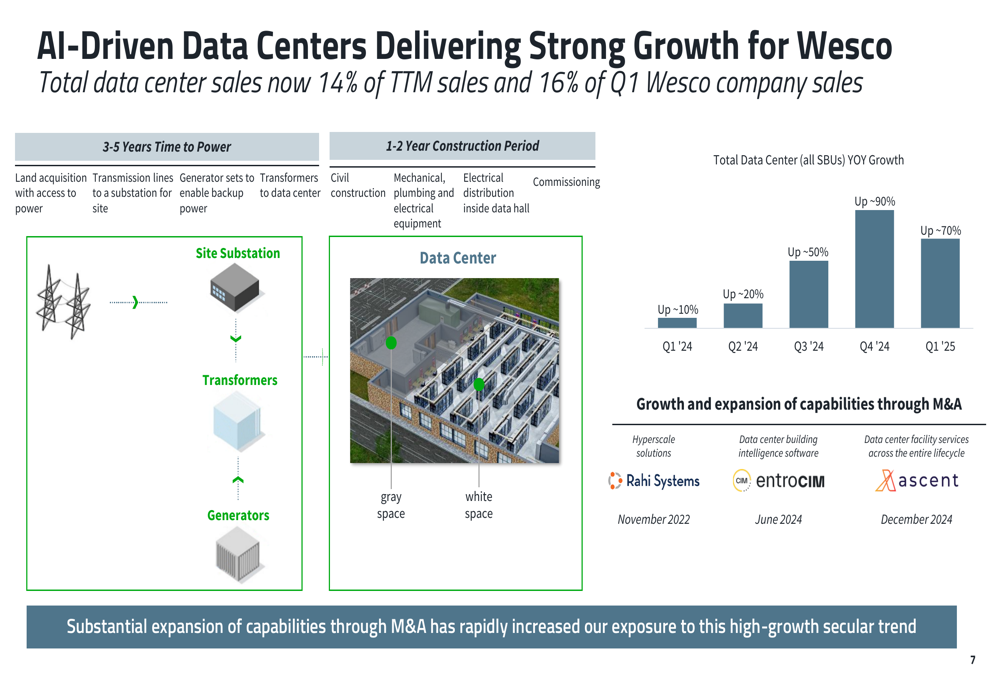

WESCO International Inc (NYSE:WCC) reported strong organic sales growth in its first quarter 2025 earnings presentation on May 1, driven primarily by exceptional performance in its data center business, which saw a year-over-year increase of approximately 70%.

Executive Summary

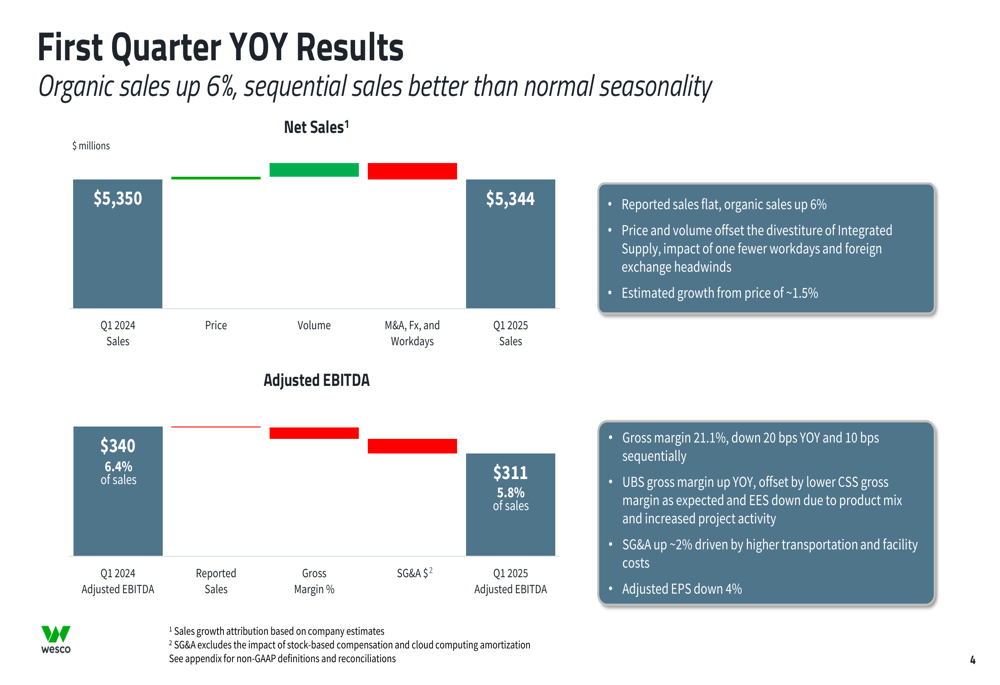

The industrial distribution giant reported flat reported sales of $5.34 billion for Q1 2025 compared to the same period last year, but organic sales grew 6% year-over-year. Adjusted EBITDA came in at $311 million (5.8% of sales), down from $340 million (6.4% of sales) in Q1 2024, while adjusted EPS decreased 4% year-over-year.

"Momentum continued in Q1 and is building to start Q2," the company stated in its presentation, noting that preliminary April sales per workday were up approximately 7%. Based on this positive momentum, WESCO reaffirmed its full-year 2025 outlook.

As shown in the following chart detailing the company’s first quarter year-over-year results, organic sales growth was driven by both price and volume factors, while divestitures had a negative impact:

Segment Performance

WESCO’s performance varied significantly across its three business segments:

The Communications & Security Solutions (CSS) segment was the standout performer, with organic sales up 18% year-over-year, driven by Wesco Data Center Solutions (WDCS) which surged over 65%. Adjusted EBITDA for this segment increased 21% to $159 million, with margins improving 20 basis points to 7.9%.

The Electrical & Electronic Solutions (EES) segment saw organic sales increase by 3%, led by growth in the OEM market. However, adjusted EBITDA declined 12% to $143 million, with margins contracting from 7.8% to 6.9% due to lower gross margin and higher SG&A expenses.

The Utility & Broadband Solutions (UBS) segment experienced a 5% decline in organic sales, primarily due to ongoing customer destocking in the utility business. This was partially offset by strong broadband growth, particularly in Canada. Adjusted EBITDA fell 18% to $138 million, though margin improved slightly to 10.8%.

Data Center Growth Strategy

The most impressive aspect of WESCO’s Q1 performance was the continued acceleration of its data center business, which now accounts for 14% of trailing twelve-month sales and 16% of Q1 company sales. This represents a significant increase from the 40% growth reported in the previous quarter’s earnings call.

The company’s presentation highlighted how AI-driven data centers are delivering strong growth, with year-over-year increases accelerating from approximately 10% in Q1 2024 to approximately 90% in Q1 2025:

WESCO has strategically expanded its capabilities in this high-growth area through acquisitions, including Rahi Systems (November 2022), CIM entrocIM (June 2024), and Ascent (December 2024). The company emphasized that data center projects typically have long lead times, with 3-5 years for power infrastructure and 1-2 years for construction, positioning WESCO for sustained growth in this segment.

Strategic Financial Initiatives

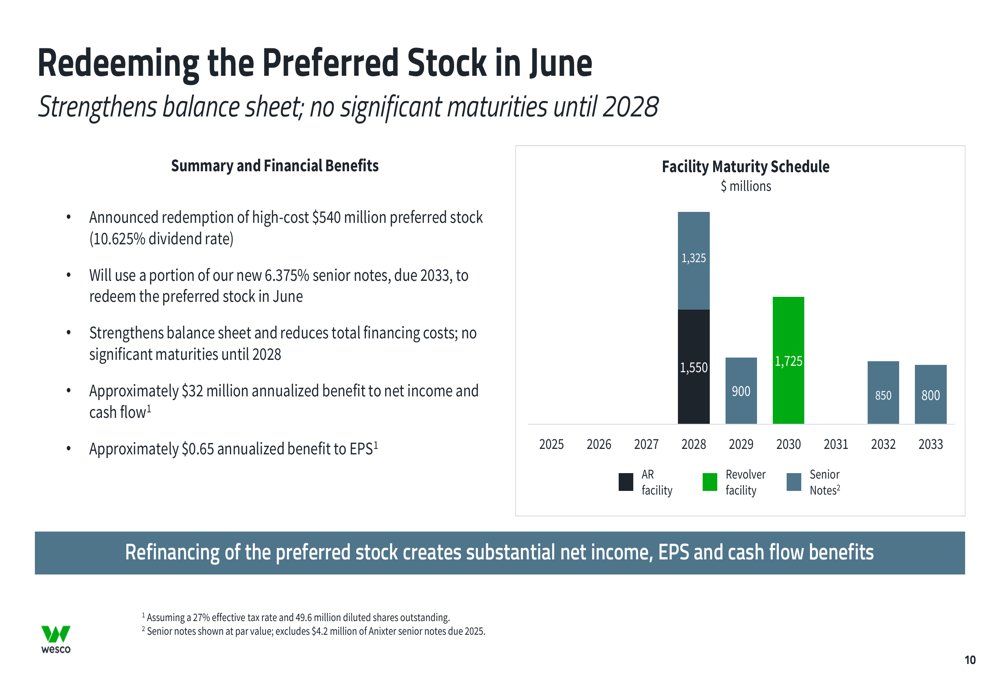

In addition to its operational performance, WESCO announced plans to redeem its $540 million preferred stock in June using a portion of new 6.375% senior notes due 2033. This financial engineering move is expected to provide approximately $32 million in annualized benefit to net income and cash flow, and approximately $0.65 annualized benefit to EPS.

As illustrated in the following chart, this refinancing will strengthen the company’s balance sheet and reduce total financing costs:

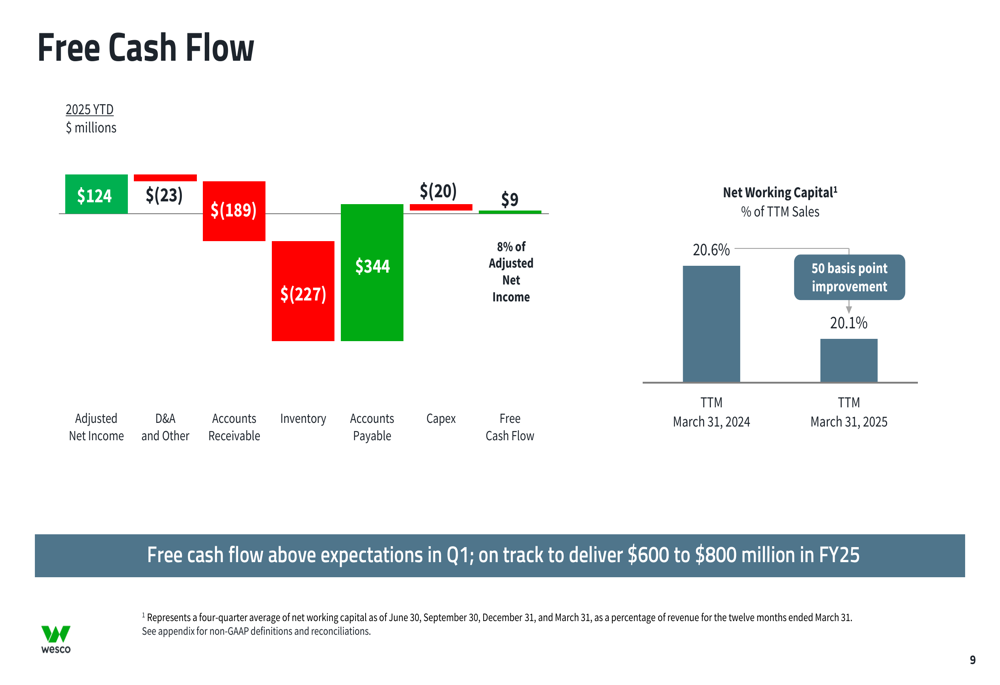

The company also reported free cash flow of $9.4 million for Q1, which was above expectations. Management confirmed they are on track to deliver $600 to $800 million in free cash flow for fiscal year 2025. The components of this cash flow are broken down in the following chart:

Tariff Management Strategy

WESCO addressed potential tariff impacts in its presentation, noting that it is the importer of record on less than 4% of its Cost of Goods Sold. The company outlined its response strategy, which includes passing through price increases, leveraging scale to provide locally sourced products, reducing imports from high tariff countries, and optimizing supply chain logistics.

As part of this strategy, WESCO increased inventory in anticipation of tariff management needs, demonstrating proactive supply chain management.

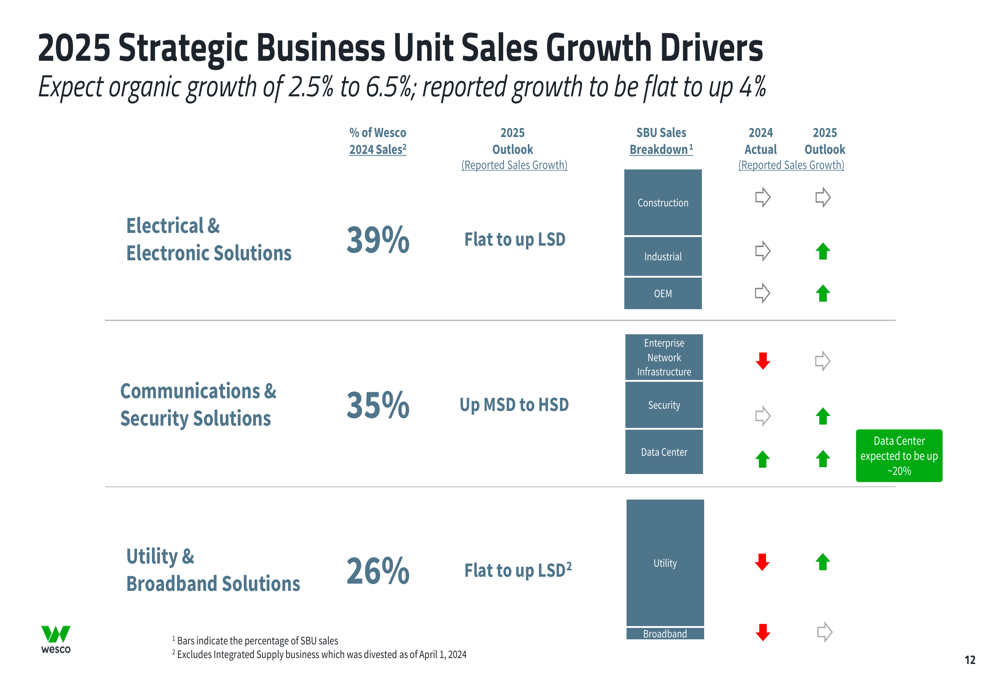

2025 Outlook

WESCO reaffirmed its full-year 2025 outlook, projecting organic sales growth of 2.5% to 6.5% and reported sales growth of 0% to 4%. The company expects reported sales between $21.8 billion and $22.7 billion, with adjusted EBITDA margin of 6.7% to 7.2% and adjusted diluted EPS of $12.00 to $14.50.

The following chart details the company’s outlook for each strategic business unit:

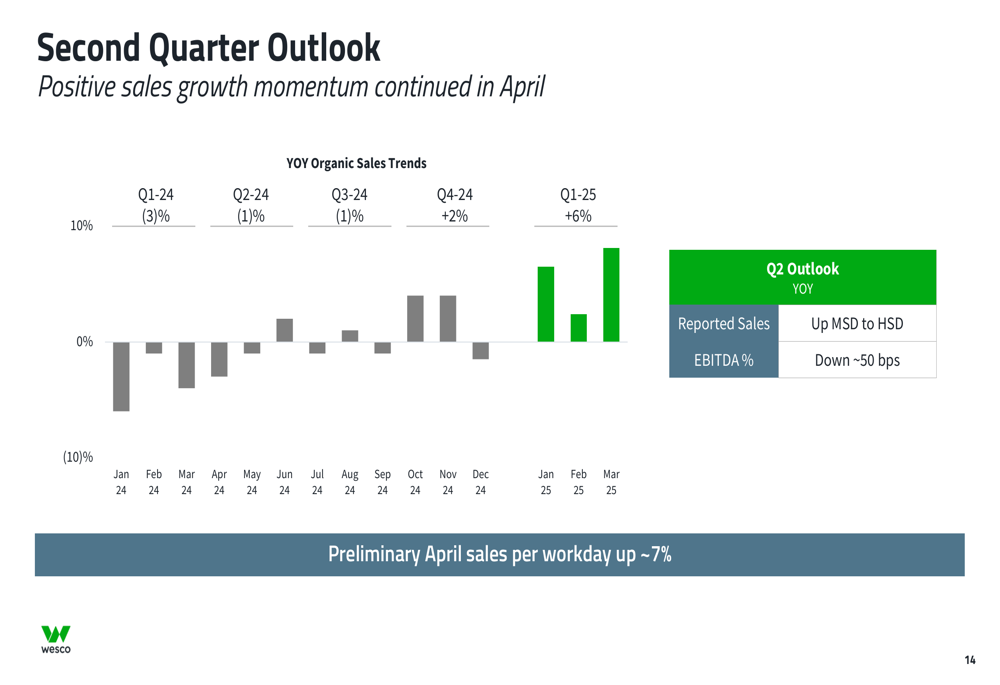

For the second quarter specifically, WESCO expects reported sales to increase mid-single digits to high-single digits, though EBITDA percentage is projected to be down approximately 50 basis points. The company provided the following chart showing the positive sales momentum continuing into April:

Conclusion

WESCO’s Q1 2025 results demonstrate the company’s ability to leverage its position in high-growth sectors like data centers while navigating challenges in other segments such as utilities. The reaffirmation of its full-year outlook suggests management confidence in continued momentum throughout 2025.

The company appears well-positioned to benefit from several macro trends, including AI-driven data centers, increased power generation, electrification, automation, and reshoring. With strategic financial initiatives like the preferred stock redemption and proactive tariff management strategies, WESCO is taking steps to enhance shareholder value while preparing for potential market challenges.

Investors will likely focus on whether the exceptional growth in the data center segment can continue to offset weakness in other areas, particularly as the company anticipates a recovery in utility sales in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.