September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

WESCO International Inc (NYSE:WCC) presented its second quarter 2025 results on July 31, showcasing accelerating sales momentum driven by explosive growth in its data center business. The company’s stock has recovered substantially since its Q1 earnings miss, with shares trading at $212.77 as of the most recent close, reflecting growing investor confidence in the company’s strategic positioning.

The electrical and communications products distributor has successfully navigated supply chain challenges and customer destocking issues to deliver its third consecutive quarter of accelerating sales growth, culminating in 7% organic growth in Q2. This performance comes against the backdrop of the company’s Q1 results, which saw an EPS miss despite a revenue beat.

Quarterly Performance Highlights

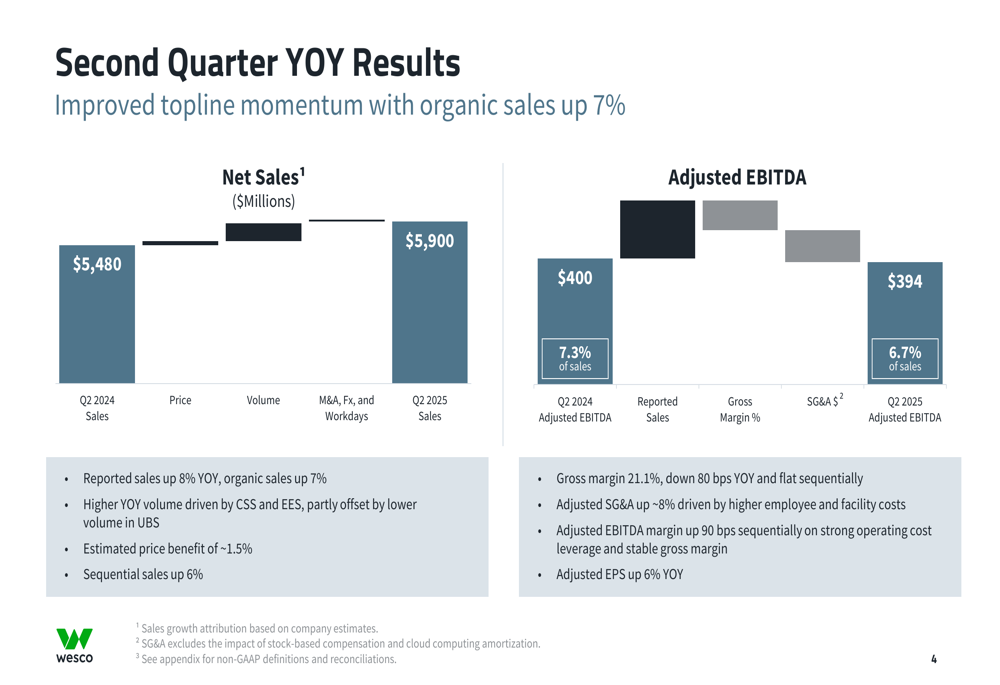

WESCO reported Q2 2025 net sales of $5.9 billion, up 8% year-over-year, with organic sales growth of 7%. Adjusted EBITDA reached $400 million, with margins improving sequentially by 90 basis points, though still facing some year-over-year pressure.

As shown in the following summary of second quarter performance:

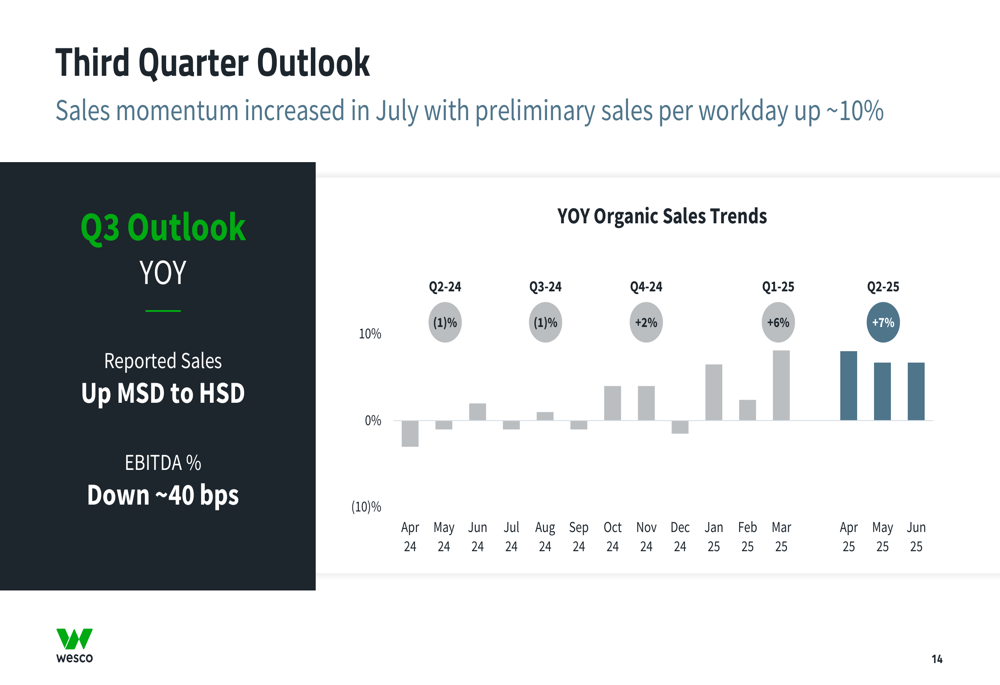

The company highlighted three consecutive quarters of accelerating sales momentum, with strong order activity and backlog growth continuing into the start of the third quarter. Preliminary July sales per workday were up approximately 10%, indicating continued positive momentum.

The quarterly results breakdown reveals both the sales growth and some margin pressure:

While gross margin decreased by 80 basis points year-over-year to 21.1%, the company managed to improve EBITDA margin sequentially, demonstrating effective cost management despite inflationary pressures.

Segment Performance Analysis

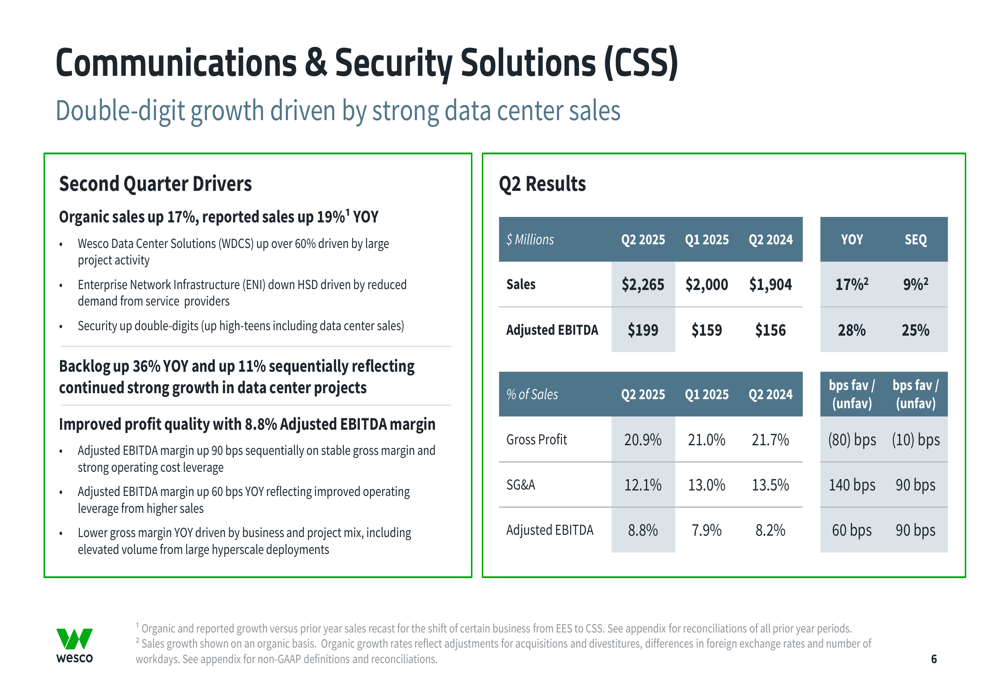

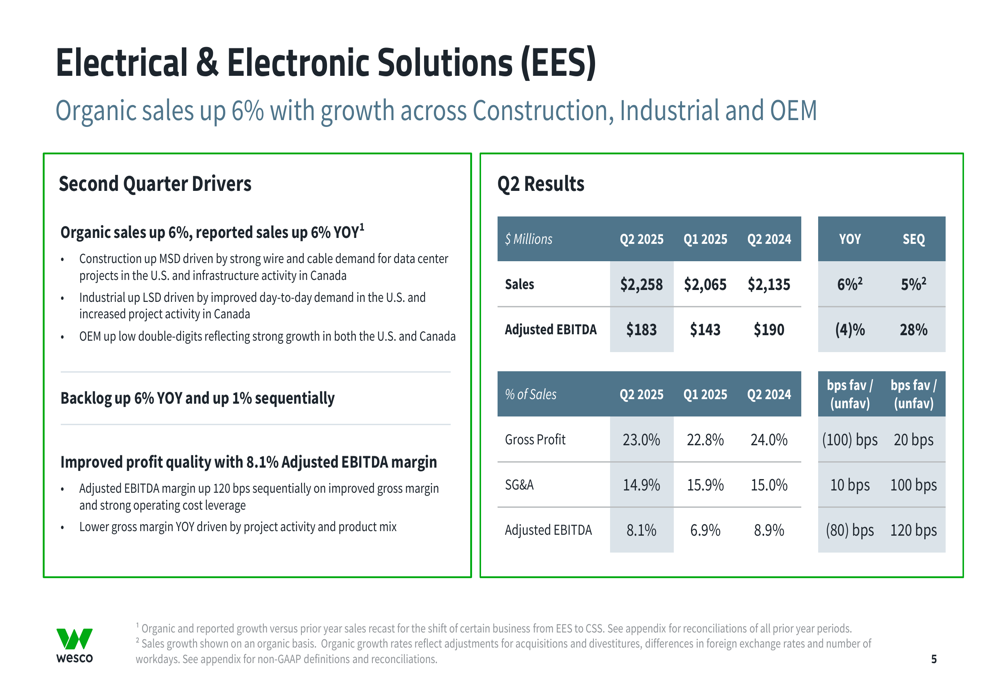

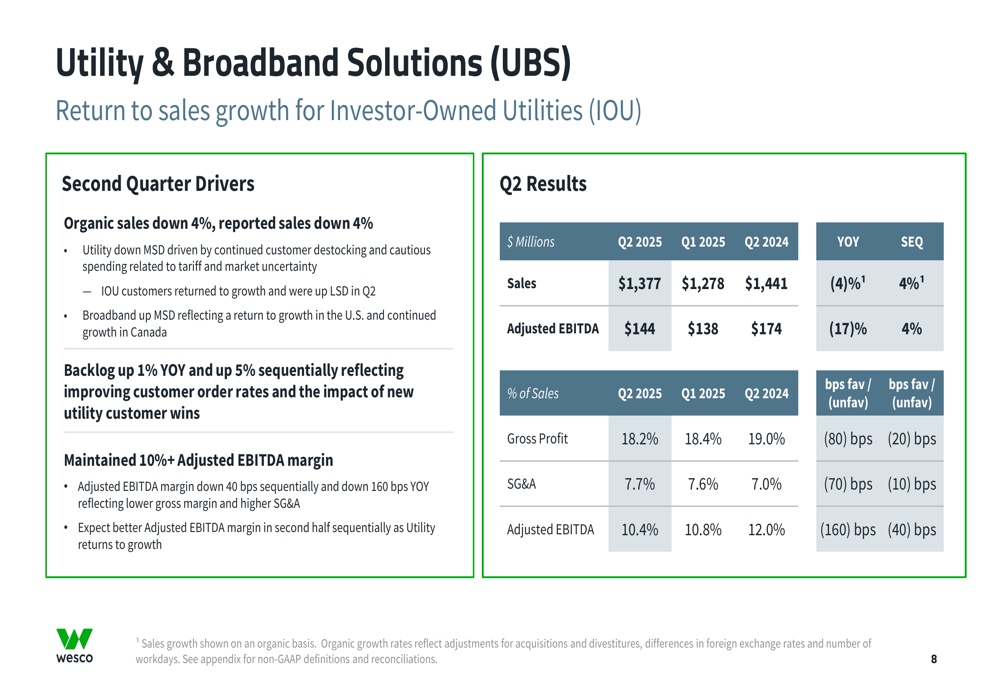

WESCO’s performance varied significantly across its three business segments, with Communications & Security Solutions (CSS) leading the way with 17% organic growth, followed by Electrical & Electronic Solutions (EES) at 6% growth, while Utility & Broadband Solutions (UBS) declined 4%.

The CSS segment’s impressive performance was primarily driven by data center projects:

The segment saw double-digit growth with reported sales up 19% year-over-year to $2.27 billion. Wesco Data Center Solutions (WDCS) grew over 60%, and the segment’s backlog increased 36% year-over-year and 11% sequentially, reflecting continued strong growth in data center projects.

The EES segment also performed well, with construction activity up mid-single digits driven by strong wire and cable demand for data center projects:

Meanwhile, the UBS segment faced challenges but showed signs of improvement:

Despite the 4% organic sales decline, WESCO maintained double-digit adjusted EBITDA margins in this segment at 10.4%. The company expects Utility to return to sales growth in the second half of 2025 as customer destocking activities subside.

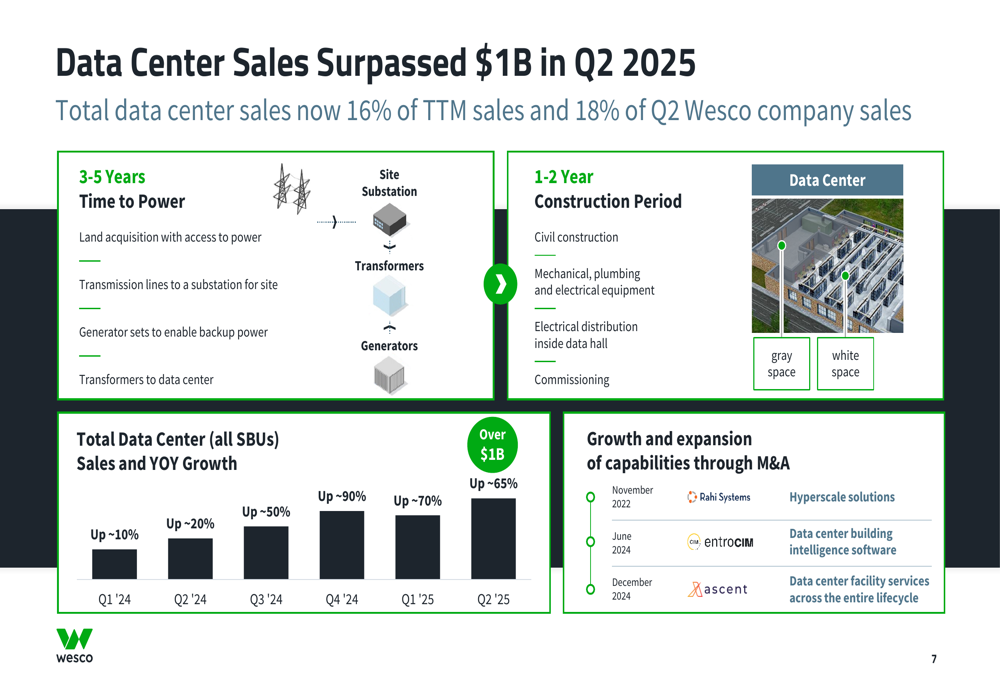

Data Center Growth Strategy

The standout story in WESCO’s Q2 results was the exceptional performance of its data center business, which surpassed $1 billion in quarterly sales for the first time, representing 18% of Q2 company sales and 16% of trailing twelve-month sales.

The company’s comprehensive approach to the data center market is illustrated in this lifecycle overview:

WESCO has strategically expanded its data center capabilities through acquisitions, including Rahi Systems in November 2022, Entrocim in June 2024, and Xascent in December 2024. This has positioned the company to capture value across the entire data center lifecycle, from initial power infrastructure to ongoing operations.

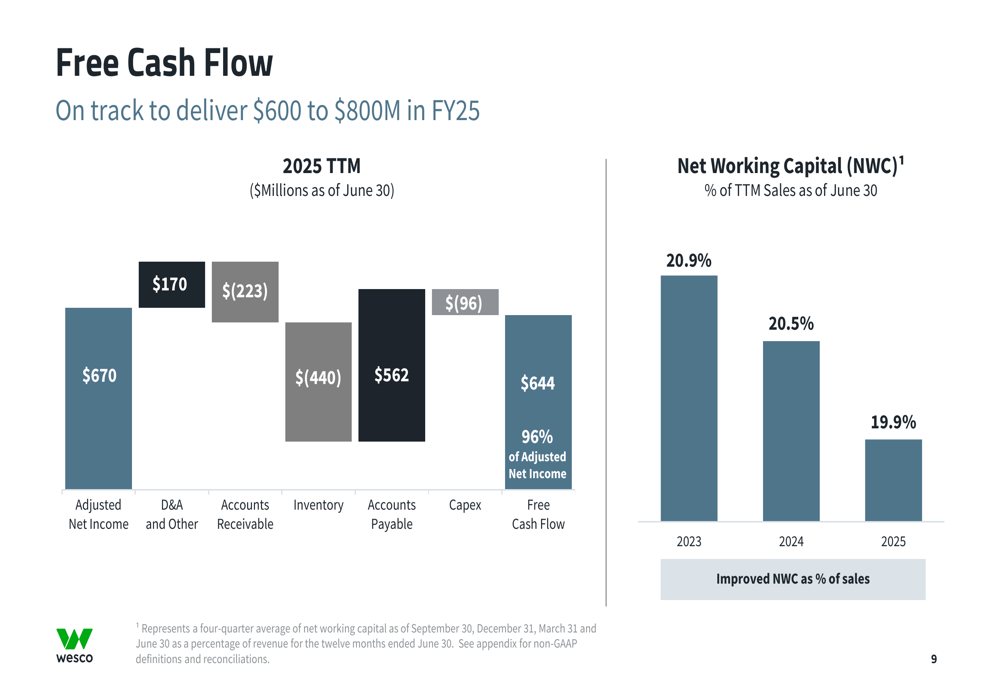

Financial Position and Capital Allocation

WESCO reported strong free cash flow generation, on track to deliver $600 to $800 million for the full year 2025. The company’s working capital management has improved, with net working capital as a percentage of trailing twelve-month sales decreasing to 19.9% in 2025 from 20.5% in 2024.

The free cash flow breakdown shows the company’s effective cash management:

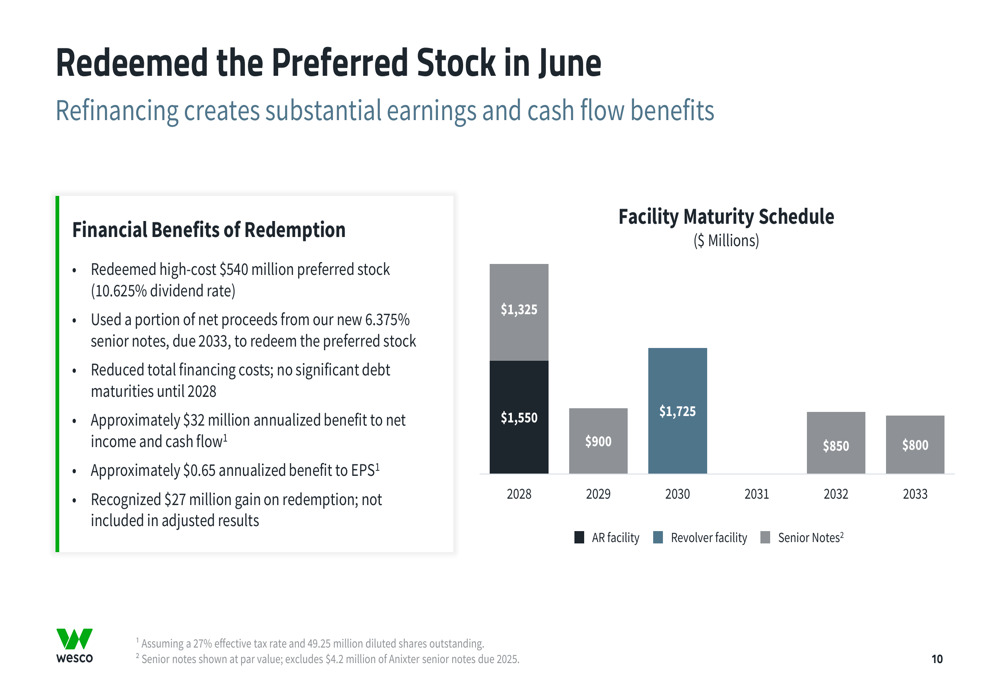

In a significant financial move, WESCO redeemed its high-cost preferred stock in June:

The company redeemed $540 million of preferred stock with a 10.625% dividend rate, using proceeds from new 6.375% senior notes due 2033. This refinancing reduces total financing costs and provides a more favorable debt maturity schedule with no significant maturities until 2028.

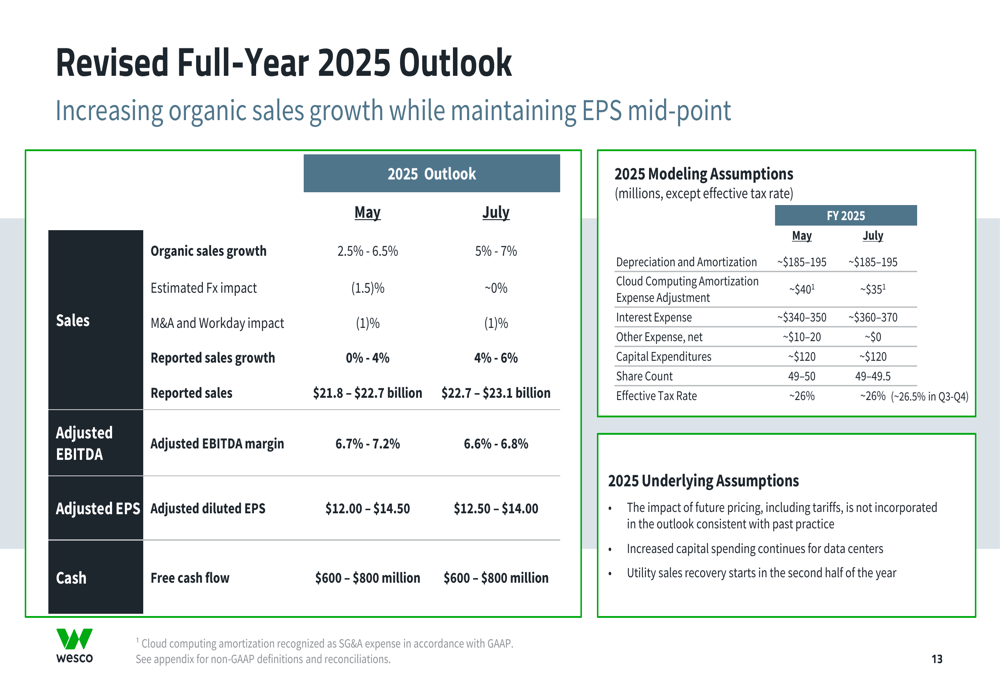

Revised Outlook and Forward Guidance

Based on the strong performance through the first seven months of the year, WESCO has revised its full-year 2025 outlook upward:

The company increased its organic sales growth forecast from 2.5%-6.5% to 5%-7%, while maintaining its EPS guidance. Reported sales are now expected to grow 4%-6%, up from the previous 0%-4% forecast.

Looking ahead to the third quarter, WESCO expects continued momentum:

The company projects third-quarter reported sales to increase by mid to high single digits year-over-year, though EBITDA margin is expected to be down approximately 40 basis points.

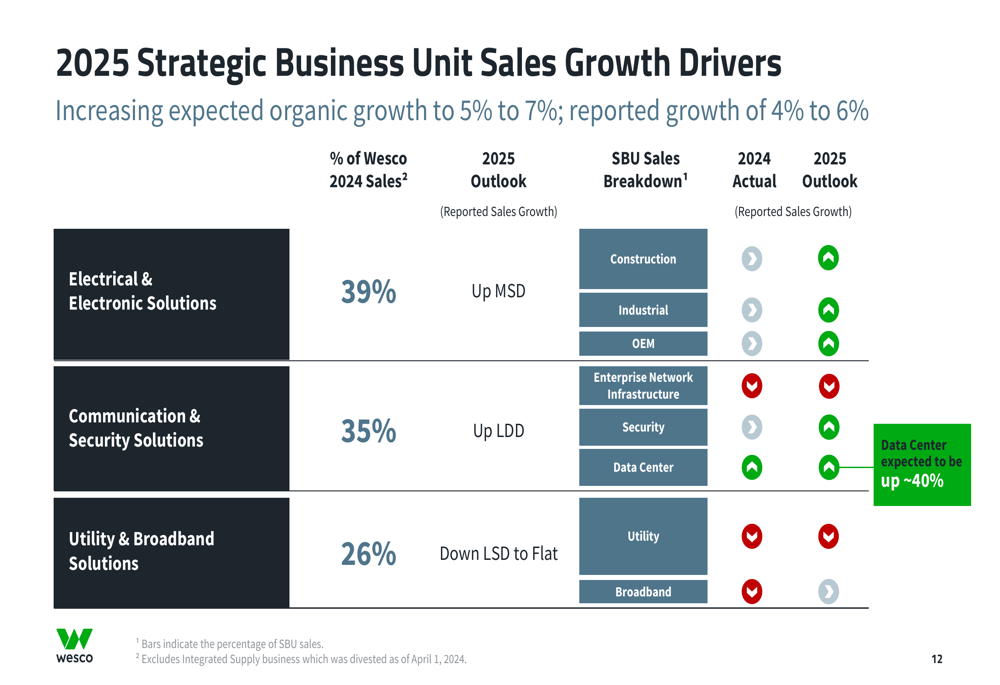

WESCO’s strategic business unit outlook shows varied growth expectations across segments:

The Communications & Security Solutions segment is expected to lead growth with low double-digit increases, while Electrical & Electronic Solutions should see mid-single-digit growth. The Utility & Broadband Solutions segment is projected to range from a low-single-digit decline to flat performance. Most notably, data center sales are expected to grow approximately 40% for the full year.

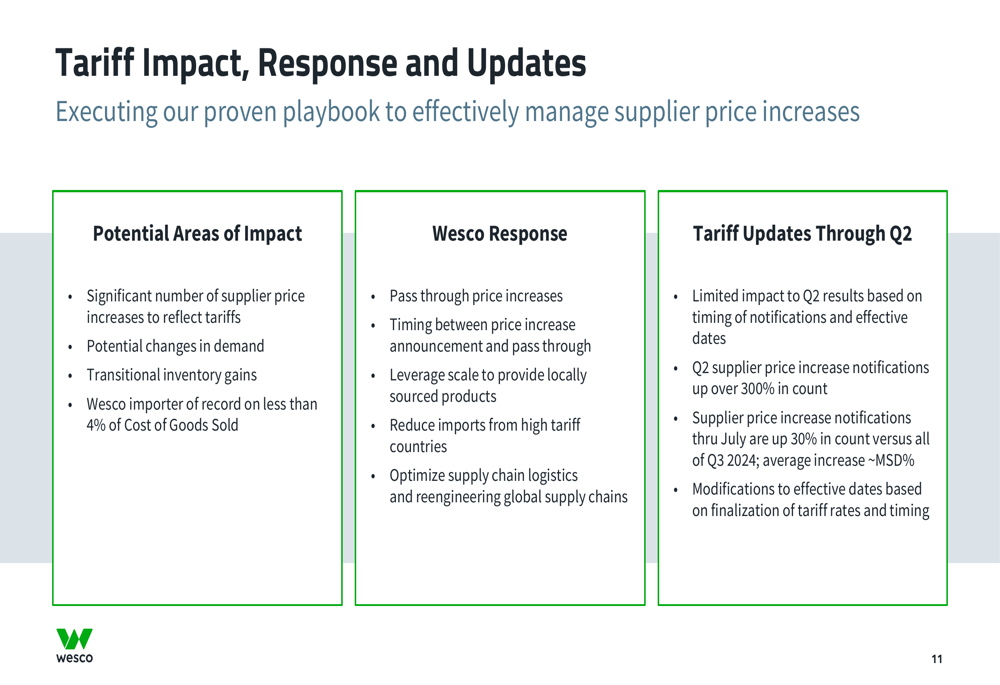

As WESCO navigates potential tariff impacts, the company has outlined a comprehensive approach:

The company is actively managing supplier price increases by passing through price increases, leveraging scale for locally sourced products, reducing imports from high-tariff countries, and optimizing supply chain logistics.

With its strong position in the rapidly growing data center market, improving financial metrics, and strategic capital allocation, WESCO appears well-positioned to continue its growth trajectory through the remainder of 2025, despite ongoing challenges in certain market segments and potential margin pressures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.