TSX jumps amid Fed rate cut hopes, ongoing U.S. government shutdown

Introduction & Market Context

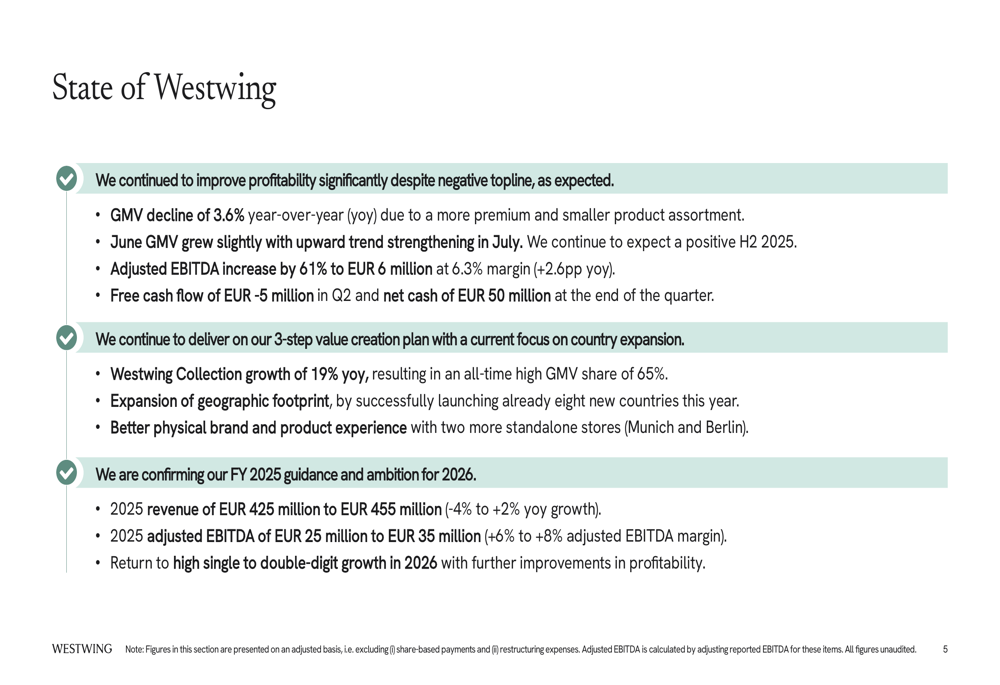

Westwing Group AG (XETRA:ETR:WEW) presented its Q2 2025 results on August 7, showing significant profitability improvements despite declining revenues. The stock responded positively to the results, rising 4.76% to €9.88 by mid-morning trading.

The home furnishings retailer continues to execute its strategic shift toward premium positioning and operational efficiency, prioritizing margin expansion over short-term growth. This approach appears to be gaining traction with investors, as the company maintains a strong cash position while expanding its geographic footprint.

Quarterly Performance Highlights

Westwing reported a 3.6% year-over-year decline in Gross Merchandise Value (GMV) for Q2 2025, though the company noted that June GMV returned to slight growth. Revenue decreased from €106 million in Q2 2024 to €100 million in Q2 2025, representing a 5.7% decline.

Despite the topline challenges, the company delivered substantial profitability improvements. Adjusted EBITDA increased by 61% to €6 million, representing a 6.3% margin compared to 3.7% in the same period last year.

As shown in the following comprehensive overview of Q2 results:

The company’s EBIT turned positive at €2 million, a €5 million improvement from the -€3 million reported in Q2 2024. This shift was primarily driven by lower depreciation and amortization expenses, including reduced lease payments.

Strategic Initiatives

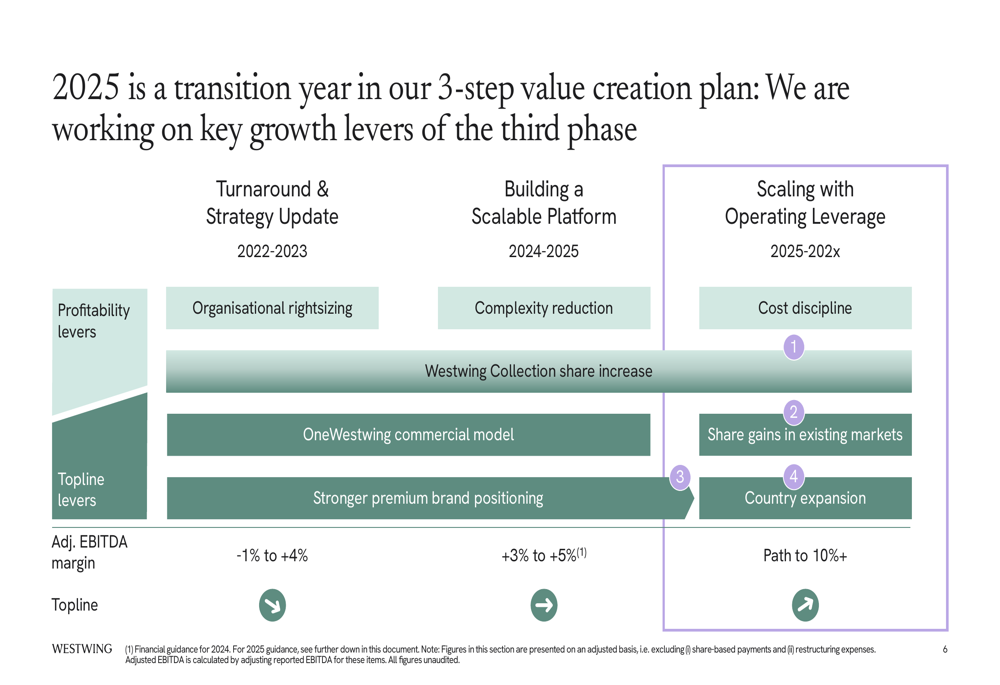

Westwing continues to execute its three-step value creation plan, currently focused on building a scalable platform while preparing for accelerated growth in 2026 and beyond.

The company’s strategic roadmap shows clear progression through defined phases:

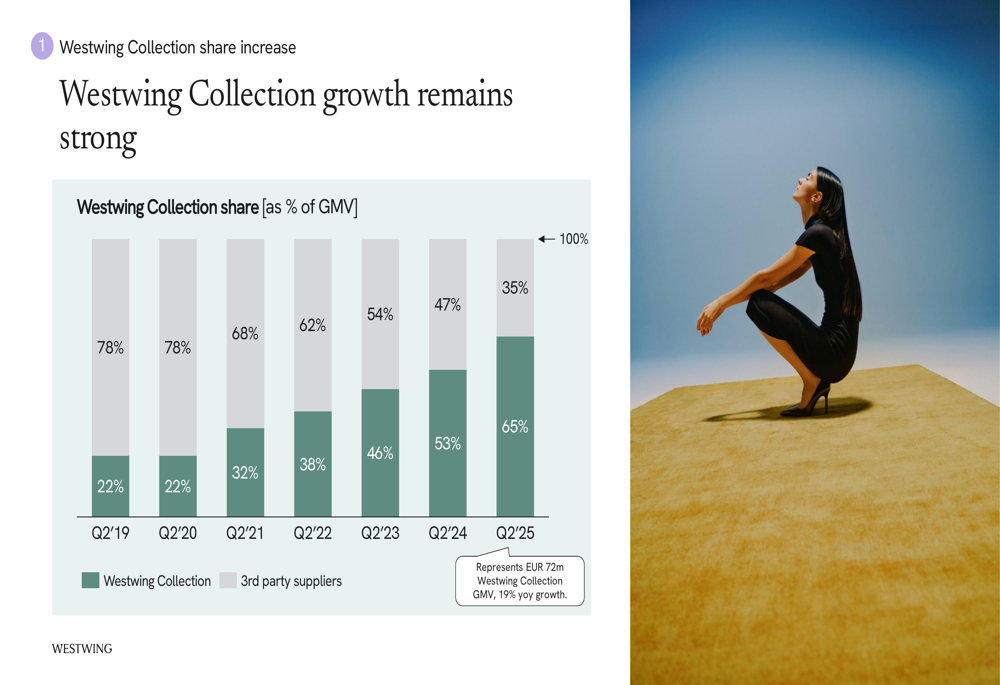

A key growth driver for Westwing remains its private label business. The Westwing Collection grew by 19% year-over-year and now represents 65% of total GMV, up from 53% in Q2 2024 and continuing a steady multi-year expansion.

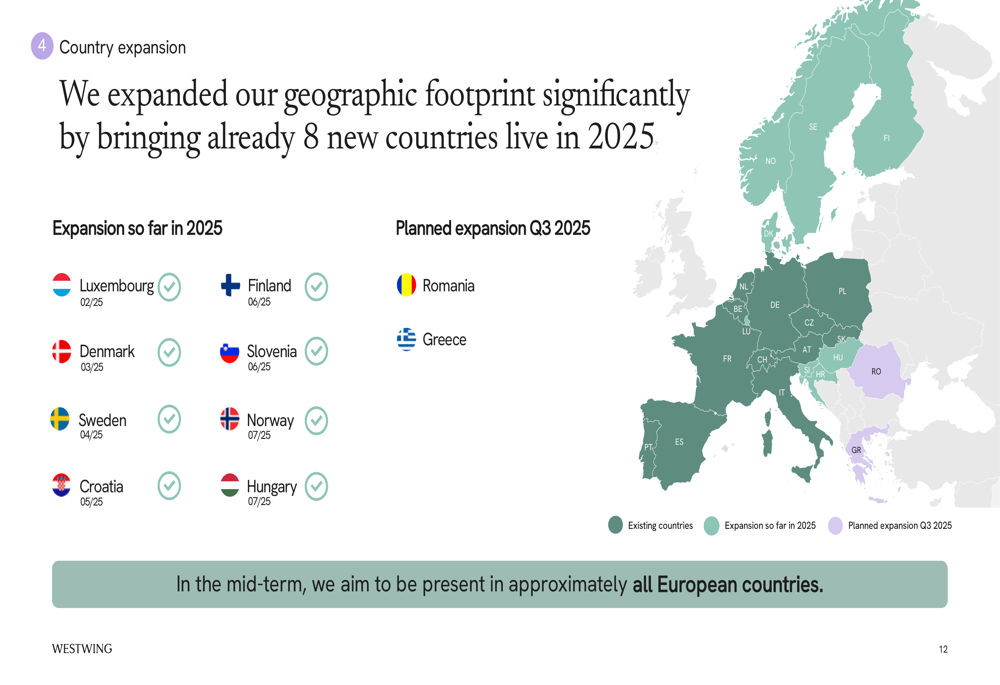

Geographic expansion represents another significant strategic initiative. Westwing has already launched in eight new European countries in 2025, including Luxembourg, Denmark, Sweden, Croatia, Finland, Slovenia, Norway, and Hungary. The company plans to add Romania and Greece in Q3 2025.

Simultaneously, Westwing is strengthening its physical retail presence, opening new standalone stores in Munich and Berlin while planning additional locations in Cologne, Dusseldorf, Copenhagen, and Paris through a mix of standalone stores and store-in-store concepts.

Detailed Financial Analysis

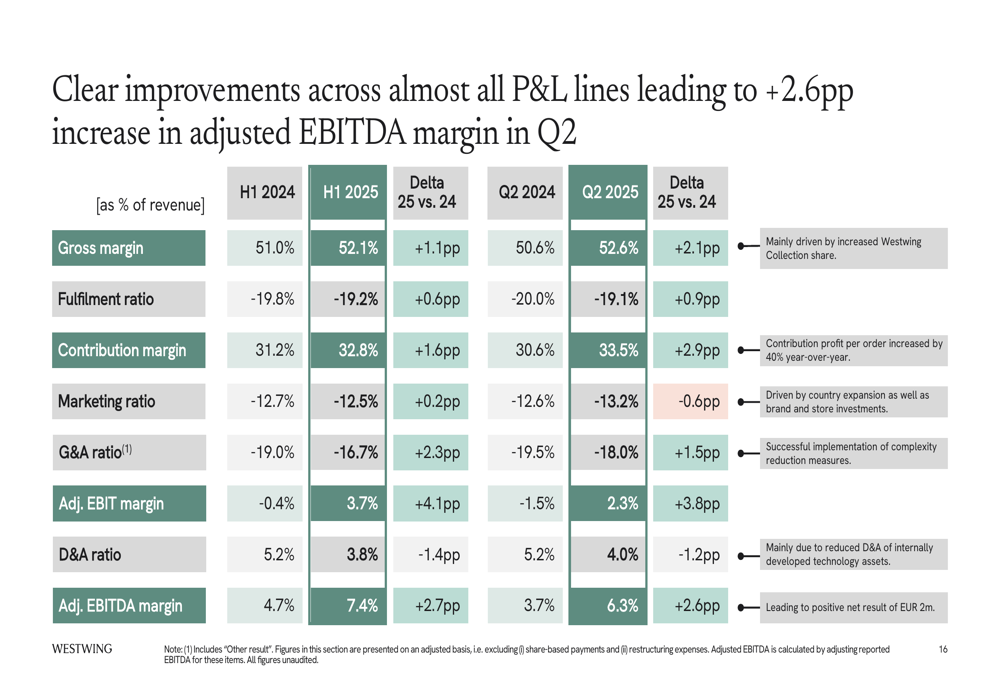

Westwing’s financial performance shows clear improvements across most P&L lines, leading to a 2.6 percentage point increase in adjusted EBITDA margin in Q2. Gross margin improved to 52.6% in Q2 2025 from 50.6% in Q2 2024, while contribution margin rose to 33.5% from 30.6%.

The detailed margin breakdown reveals consistent improvements across the business:

Both operating segments showed profitability improvements. The DACH segment (Germany, Austria, Switzerland) saw its adjusted EBITDA margin increase by 2.1 percentage points to 6.5%, despite a 9.5% revenue decline. The International segment performed even better, with adjusted EBITDA margin improving by 3.6 percentage points to 6.1%, while revenue declined by only 1.6%.

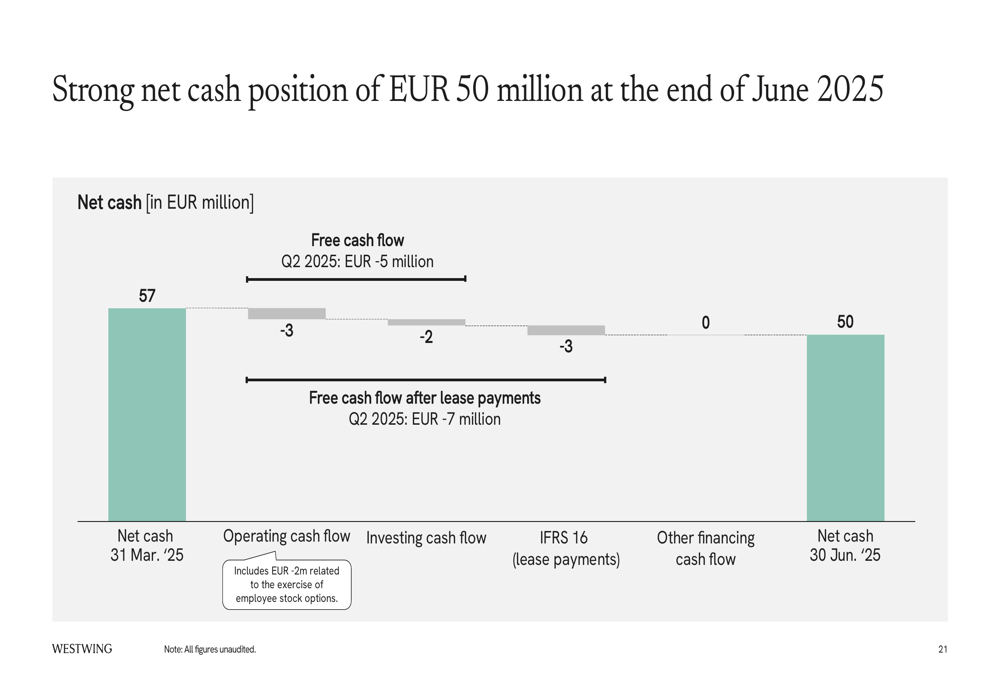

Westwing maintained a strong financial position with €50 million in net cash at the end of June 2025, though this represents a decrease from the €57 million reported at the end of Q1. The company attributed this primarily to a €5 million negative free cash flow in Q2.

Working capital increased by €16 million year-over-year, primarily due to reduced trade payables following inventory increases for new product launches. Management expects inventory levels to decrease in the second half of 2025, which should positively impact working capital.

Forward-Looking Statements

Westwing confirmed its full-year 2025 guidance, projecting revenue between €425-455 million (representing -4% to +2% year-over-year growth) and adjusted EBITDA between €25-35 million (corresponding to a 6-8% margin).

Looking further ahead, the company reiterated its ambition to return to high single to double-digit growth in 2026 while continuing to improve profitability. This growth is expected to be driven by market recovery, benefits from the 2024 product assortment changes, and the 2025 geographic expansion initiatives.

Investment Thesis

Westwing outlined five key investment highlights that form the foundation of its value proposition to investors. These include its unique customer value proposition, market potential, brand strength, margin profile, and strong balance sheet.

The company emphasized its path toward a mid-term adjusted EBITDA margin of 10%+ with strong cash conversion:

This investment thesis aligns with the company’s Q1 2025 performance, where it reported an 8% adjusted EBITDA margin and positive net result of €2.5 million, though the Q2 margin of 6.3% represents a sequential decline, likely due to seasonality.

Westwing’s strategic focus on profitability over short-term growth appears to be yielding results, with significant margin improvements despite revenue challenges. The company’s expansion initiatives and strong Westwing Collection performance position it well for its targeted return to growth in 2026, provided consumer sentiment in the home furnishings market improves.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.